Midweek Macro Note: On the Ground Part 2.1 - Troubling Times in Ag, Fed Minutes Review, Portfolio Strategy Update and Commentary, Headline Jawboning

In this Midweek Macro Note - we discuss the headline volatility & why we should look beyond it to the fundamentals and technicals, discuss the Fed minutes, cover 'On the Ground' Pt 2 + more

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

This week has been largely uneventful - with some oil volatility in the 100-110 range (WTI spot) - the same old games with a lot of headlines that don’t really mean much - and a continued climb in technology and AI equities. We also saw a slightly hawkish pivot in the Fed minutes - and markets continue to change the rate pricing dynamic out, especially with almost a 50/50 chance of a hike this year. For the time being, it does not look like the Fed is still in any immediate hurry to hike, though other central banks have taken a tougher stance - and beyond Australia, which we called out early, we can turn our attention to Europe & Canada next for a barometer of where the Fed might head.

A look of the ‘West’ - the 2-year yield continues to move higher, and looking at the ‘East’ - in Japan, which is actually catching up to the EU02Y.

Going into the long weekend, it looks highly unlikely that we’re going to see any sort of resolution to wrap up the week with, though they’ve been very active in pushing the ‘deal’ narrative again the past 2 days in order to push WTI back to the $100/bbl level. The slop garbage merry-go-round is actually something that we’ve taken note of in targeting on X - namely, with accounts like ‘FinancialJuice’ which are publishing false and old information frequently - directly impacting front-month pricing. As @HFI Research notes - it’s death by 1,000 headlines… None of that impacts the actual supply drain itself - where we saw our largest crude drawdown in US history, with about 18 million barrels being removed from inventories on a week/week basis, drawdowns should continue to remain robust as driving season heats up. Really, at this point, the only outcome for the market is going to be outright shortages, an export ban, or some kind of massive under the table deal done to reopen Hormuz that will be paraded around as a massive victory-in-kind. In my opinion, regarding the next action, I believe that with the Chinese meeting in the background and the holiday ahead, the Administration has a window for escalation if they are going to pull off some kind of operation - especially regarding the Strait - though right now there’s still no definitive signal on if that’s going to happen or not. Risks are going to be completely ignored for the time being with the speculation occurring in equity markets - which has acted as a huge distraction away from the commodity and price sphere (for some in the economy), though firms like Walmart noted that the outlook is becoming much more cloudy as inflation rips, yields remain high, and the potential for a rate hike this year creeps back to the 50% level.

It still remains a mostly positive portfolio strategy environment for macro, and we will target opportunities as they come in. Below, I cover the energy portfolio strategy and much more, including Part 2.1 of the ‘On the Ground’ series from the High Plains, focusing on ags, so enjoy & have a fantastic long weekend.

PS… tomorrow should hopefully be quiet, likely another deal headline or two pushed through - though the asset ‘crash up’ still has winds in its sails for the time being.

Not yet a MacroEdge subscriber? Upgrade to Ozone below for two weeks:

‘On the Ground’ Part 2 - A Look at Troubling Times in the Ag Space

My coverage of the ‘On the Ground’ series from the Texas Panhandle will go in chronological order in the order in which I had my discussions - this will be called ‘Part 2.1’.

Hopping back into Part 2.1 of our ‘On the Ground’ series from Amarillo took me into a discussion with an individual who has been a grain broker for the better part of their lifetime (~40 years) - and I arrived sight unseen to this discussion, so I appreciate the time again for the opportunity to learn much more about the entire wheat-sphere and Panhandle farming environment. Additionally, after this discussion (which I will add more color to below), I embarked with Six over to West Texas A&M University for a possible discussion in their Agrilife Extension Center on our first day of data/discussion collection. I compiled the key discussion points into some high-level points below, which help shape the final comments section at the end. The discussion with the broker primarily focused on the impact of the Strait of Hormuz and how the market was actually mispricing the event - especially given all of the other risks materializing in the wheat harvest for the current season (which Six covered wonderfully a week ago). Part 2 will continue in the Redeye Macro Note tomorrow, and then over the weekend in a third Part 2.3 - which will lead us into the corn-focused (yes, corn) discussions.

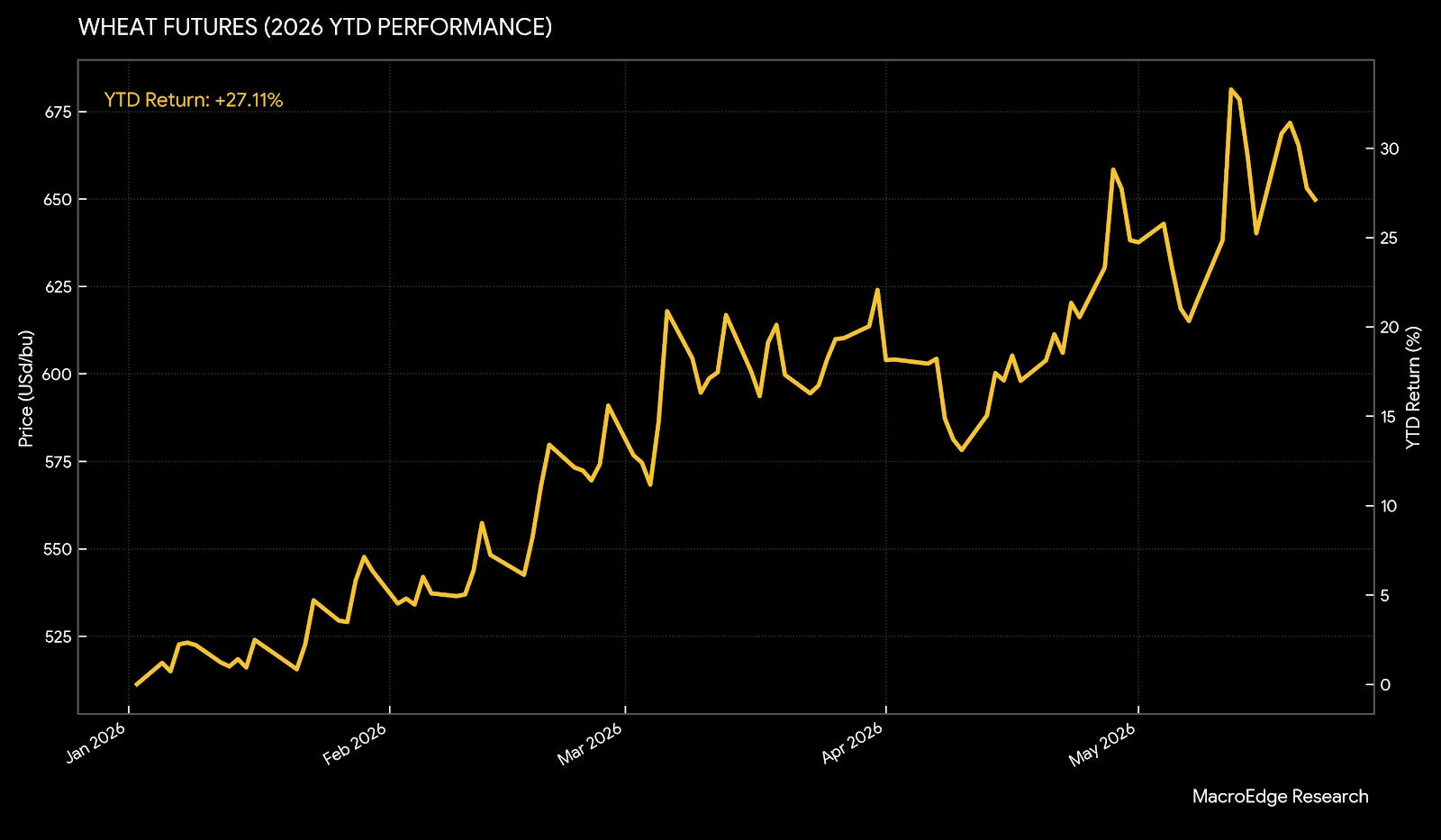

Wheat has continued to enjoy a positive year from a price standpoint, which absolutely does not reflect the pain that farmers are feeling, especially in markets like Amarillo. Input prices are the top cited issue this year, with weather and other issues coming up in a more distant second. In the immediate term, while some farmers hedge events like the Strait closure, one might think they benefit from the higher sale price of the crop, but that doesn’t help if a farm is not producing it. Wheat performance YTD sits around ~30%, obviously a steady gain, but nothing like what we saw back in 2022 or 2008 (for the time being). Whether or not we get there depends on just how long the Strait remains closed, which is looking like until mid to the end of June or beyond right now. The US & other Western countries are not going to accept a tolling system in the long-term in Hormuz, which leads us to two resolutions: one being the payment and release of funds to Iran with a lifting of sanctions, or actions by US forces to secure Hormuz, both of which I am undecided on being more likely at the current time. It appears that China has gotten more involved on the Iranian side in recent days, which makes sense due to their oil price sensitivity. With how reliant China is on Iranian crude, expect them to continue to try and force Iran’s hand to the negotiation table in a controlled fashion, even though China would prefer that Iran retain control over Hormuz transits for commercial vessels. Travel in Hormuz for tankers and commercial cargo ships is still between 5-10 a day, so not zero, but just enough to keep some ships going out, while a few go in on a weekly basis.

Wheat YTD gain:

Below, I am including my key discussion notes from the discussion with a grain broker who has been in the region for the better part of 40 years. There are many takeaways, and most highlight how difficult the current environment is for wheat production in the High Plains. Ironically (or not), very large wildfires and dust storms swept through Amarillo on my final 3 days in the region, highlighting just one of the risks that are materializing against this critical industry. In some of the other discussions, I was able to ask more politically oriented questions - focusing on things like another round of stimulus for farmers & another potential farm bailout - which I hope you all find interesting in this holistic look at the wheat, corn, and fertilizer picture.

(Below: ‘On the Ground Part 2.1 continued’ - Part 2, Fed Minutes Overview, On the Headline ‘Merry-Go-Round’, Portfolio Strategy Update & Commentary - Six)

Upgrade below to get all of our research, data, commentary, and much more - below:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.