Midweek Macro Note: 'On the Ground' Report Series, Back to the Bubble?, An Update on the Real Estate Situation, Portfolio Strategy Note

In this Midweek Macro Note - we discuss the latest developments in the last two trading days - including a 'back to the bubble' component - with tech & AI stocks bidding back to ATH, & much more...

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers and Community,

It’s great to be back for another Midweek Macro Note - as we continue to accelerate progress with MacroEdge this year - there are so many positive things on the horizon - such as our new ‘On the Ground’ report series that we will cover below. As we continue to navigate a very interesting and fast-moving start to the year, we are continuing to progress with our vision through Macro Research, Transform, & our Media/Partnerships division.

For some reason on the equity market front - and I still haven’t figured out the exact *why* (I have many speculations - there remains a relentless passive bid behind everything - and most notably the lowest quality garbage with zero profit moat into the next year, 10 years, 50 years - whatever timeline you want to look at it with. While the exact reason may never be known, the brief war dip barely shook retail investors from these positions, overall leverage exposure is still barely off of the highs, and the macro picture is now in the rear seat with momentum and oil assuming the first position for now. As discussed in the brief energy note - oil prices recovered today - with US spot crude around $99/bbl at the time of this writing. There still needs to be some stabilization from a price standpoint, but as long as the channel remains intact from a technical standpoint, that will be quite positive structurally for higher price levels.

In the AI & data center investment sphere - those equities continue to push higher… The people selling the investments don’t seem to care at all about the technologies and investments they’re selling as long as they keep selling. The vision there is key - and below - in the ‘On the Ground’ breakdown - we’re going to talk about why we’re initiating coverage on the data center space, which remains one of the last few economic drivers in the current economy as cyclicals continue to struggle.

In the overall equity overview - the question I’ve posed to readers and our community-at-large - is whether or not the price action we’re seeing represents our *Zimbabwe moment*... or Venezuela/Argentinian style markets globally - where the new norm is just a permanent crash up in nominal terms as more and more is fired into the system year after year. Obviously - as has been discussed for years - this is completely untenable in the long-run given things like the long-run, demographic outlook for countries like the United States (and places that are in much worse shape like Europe and East Asia) - it’s always a question of how long the insanity and nominal euphoria can continue. For the time being, the key barometers to observe remain things like our ‘Global Bubble Gauge’ basket below - and we continue to seek out opportunities that aren’t in the headlines by being first to the party. Chasing with crowds is rarely a philosophy I endorse - and with so little understanding and so much hype continuing.

Table of Contents for this Midweek Macro Note:

On the Ground Report Series - Arriving in May

The Macro Club - Applications Open Soon

Back to the Bubble - A Look at Japan, the AI Trade, & More - Is This Project Zimbabwe… or South Africa?

An Update on the Real Estate Situation

Performance Comes First - Energy Update

Report Schedule for The Weekend

Tomorrow - keep an eye on the CPI report - the consensus for warm to hot - and this will directionally impact the 10Y and rate decisions from the June and on timeframe.

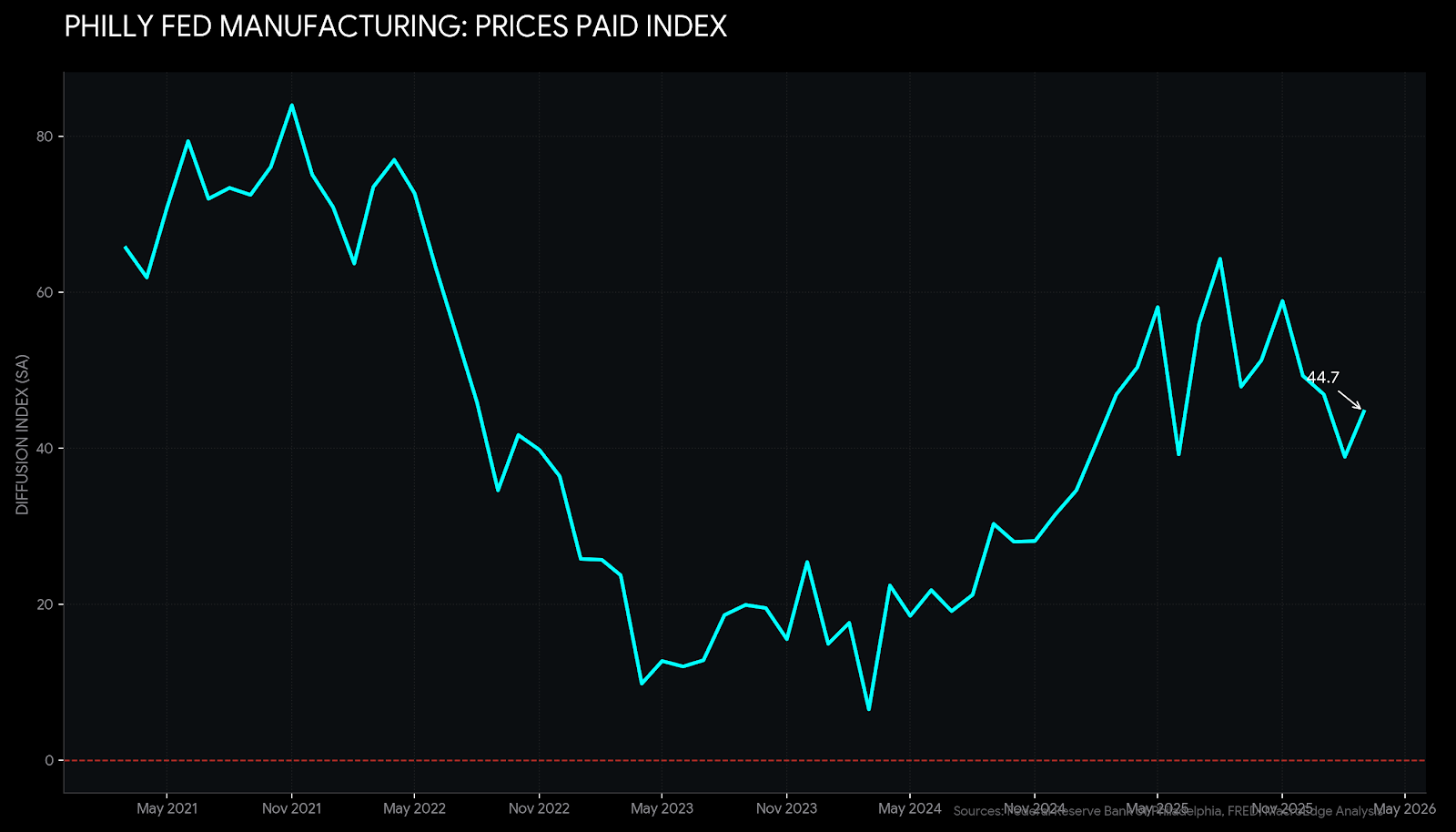

The Philly Fed Prices Paid indicator for March came in warmer than expected (and PCE was also hot today):

‘On the Ground’ Report Series - Arriving in May

Given the popularity of our energy sector and data center reports in February and March, which both incorporated a significant amount of anecdotal information collected on the ground, we’re going to expand our ‘on the ground’ data and research with this new series.

Agriculture: A Deep ‘On The Ground’ Dive Into Wheat and Corn - May 2025

Data Center - The New Shale Series - May 2025 and on

Energy Pt. 2 - An Update from the Permian and Bakken - May 2025

Aviation - America’s Favorite Public Utility - June 2025

Given the speed of news, market data, and price action of late, I don’t want to chain all of our coverage down to slower processes and methodologies, which are all designed with profiting from a portfolio strategy or basket as an absolute #1 priority. The above is designed to be a starting point for us being early to trends, and then follow-up on them as we capture the opportunity (ie: energy), which is really part 3 of the series since it will mark our third visit to the Permian in the last few months.

The Macro Club - Applications Open Soon

As part of our community building efforts, we’re going to be expanding our community internally and migrating community features to ‘The Macro Club’ come late June 2026. While Substack will continue to serve as our primary email distribution place, it lacks the community engagement and professional feel that we’ve been desiring as an organization over the past year, since this was first conceptualized. There was no happy medium between the abandoned X communities feature, which they’ve almost killed off, and the Substack community features, which are isolating for individual users, as they make it difficult to actually connect with other users within our community internally.

The Macro Club will serve as our private community for serious investors, money managers and financial professionals, financial authors on platforms like Substack, and business executives.

Submit an interest form through the button below:

https://club.macroedge.world/tmcinterest

Back to the Bubble - A Look at Japan, the AI Trade, & More - Is This Project Zimbabwe?

The price action over the last week is a rapid return to pre-war mania, in fact, it’s more reminiscent of April and May 2025 price action, where traders, CTAs, banks, and retail all piled in at once to push things higher.

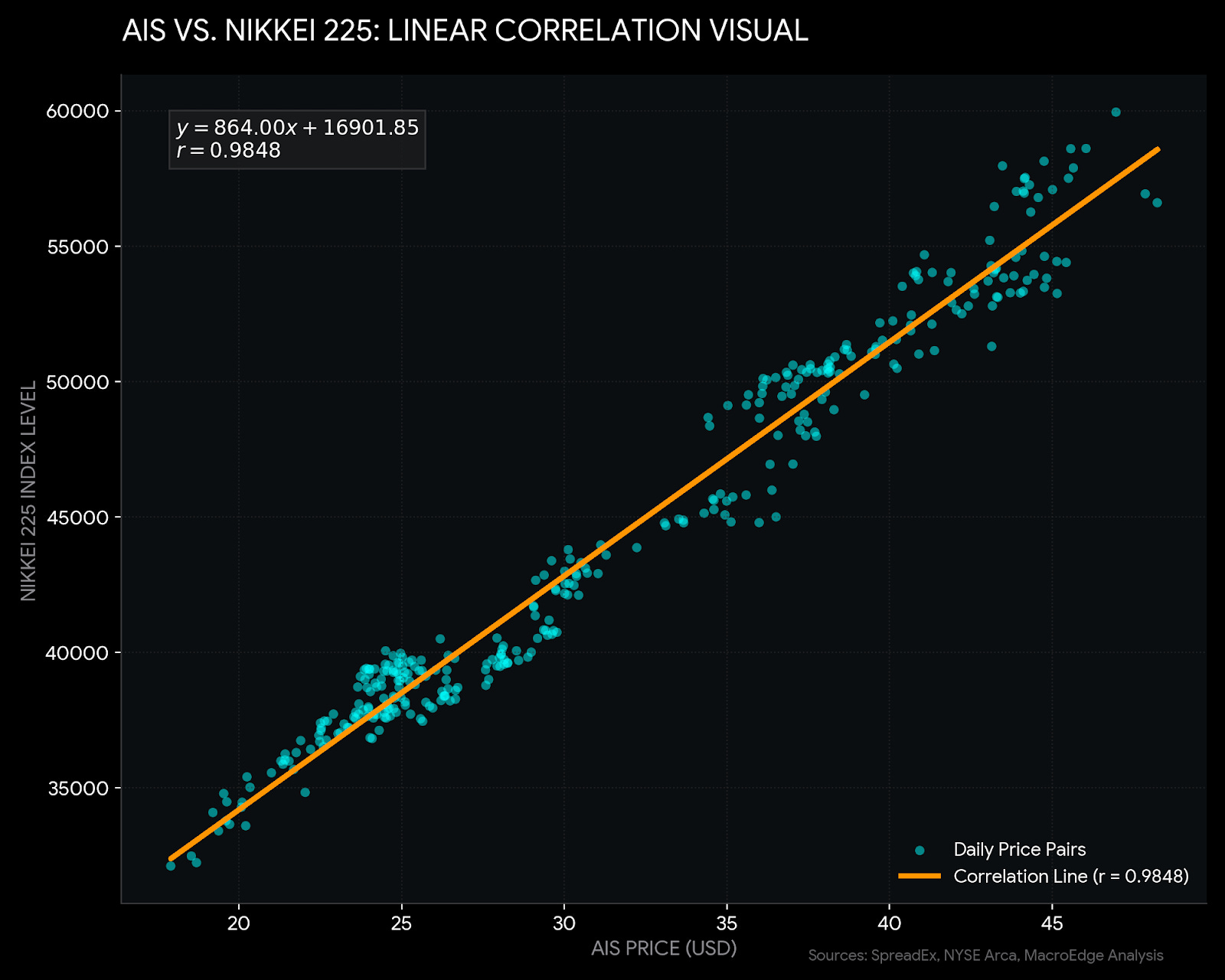

The Japan/US AI trade continues a shocking correlation as it continues to advance higher, and the BoJ’s policy of being too loose with a weakening Yen has spurred a continuing melt-up in a select few Japanese equities. It’s even more egregious in markets like Korea (which we also highlight below).

In line chart format:

The question now remains whether we finally see a higher low to see these markets break lower, or if this is just another staircase to new highs from here.

My thoughts: what a stupid market this has become:

Korea continues to push higher relentlessly:

(Continued below: Back to the Bubble (cont.), An Update on the Real Estate Situation, Performance Comes First - Energy Update, Portfolio Strategy Note and Commentary from Six)…

Not yet a MacroEdge subscriber? Upgrade below and get access to all of our research, data, reports, and much more →