Midweek Macro Note: Oil Spooks Administration, the Objective Energy Outlook, Natural Gas Discussion, Nonfarm Preview, Portfolio Strategy Note

In this Midweek Macro Note - we discuss the $82WTI spook that we saw today, Russian sanctions lifted, provide an objective energy outlook in a short-term overbought environment, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge readers and community,

In this evening’s Midweek Macro Note - we’re going to keep the introduction brief - and focus on the latest updates in energy, employment, and our portfolio strategy. While the evolution of the war continues in an interesting way, it does not appear that we’re seeing any ‘off-ramp’ develop for the time being, which was briefly priced into WTI today for all of ten minutes. Upon a spike above $82/bbl, we saw an immediate market intervention on the news that the Treasury Department may begin utilizing oil futures and open short positions against the commodity to lower prices. Ironically, this actually sets up the conditions for a much higher squeeze, though in an obvious fashion technically - oil is now on the daily timeframe in ‘extreme’ territory on the RSI.

I’ve called tomorrow the last real ‘marker for a deal’ though I am extending that over the weekend as it’s become apparent that leaders worldwide are fearful of what an energy shock could do to already very fragile, and over-levered economies and financial markets.

On the Strait of Hormuz front - traffic remains effectively zero - though a few ships continue to pass through the Strait. Without insurance and protection, most shippers have already implemented their re-routing plans, though energy supply out of the Middle East remains frozen to a great degree for the time being. This afternoon, we saw sanctions lifted on Russian oil tankers temporarily, allowing them to dock at Indian ports and unload product. Given that the product was already on the water, I am not sure why this headline in particular caused a brief dip in WTI… it was really about the Treasury taking a potentially proactive approach through financial markets to combat rising CL.

For the employment report tomorrow, the ADP & Revilio signals provided a mixed picture for the month of February, and I think the right tail is actually a bigger risk to equity markets right now than the other way around (especially with commodities and yields surging higher). The MacroEdge team & Six have done a stellar job on the commodity opportunity identification and positioning, and it will remain a thematic I lean into heavily as the opportunity remains on the table to profit from.

Not yet a MacroEdge Ozone member? Our Ozone community now lives exclusively on Substack. Get all of our research, data, reports, equity research, & much more by upgrading below:

(Try Ozone for a week above)…

Oil Spooks Administration

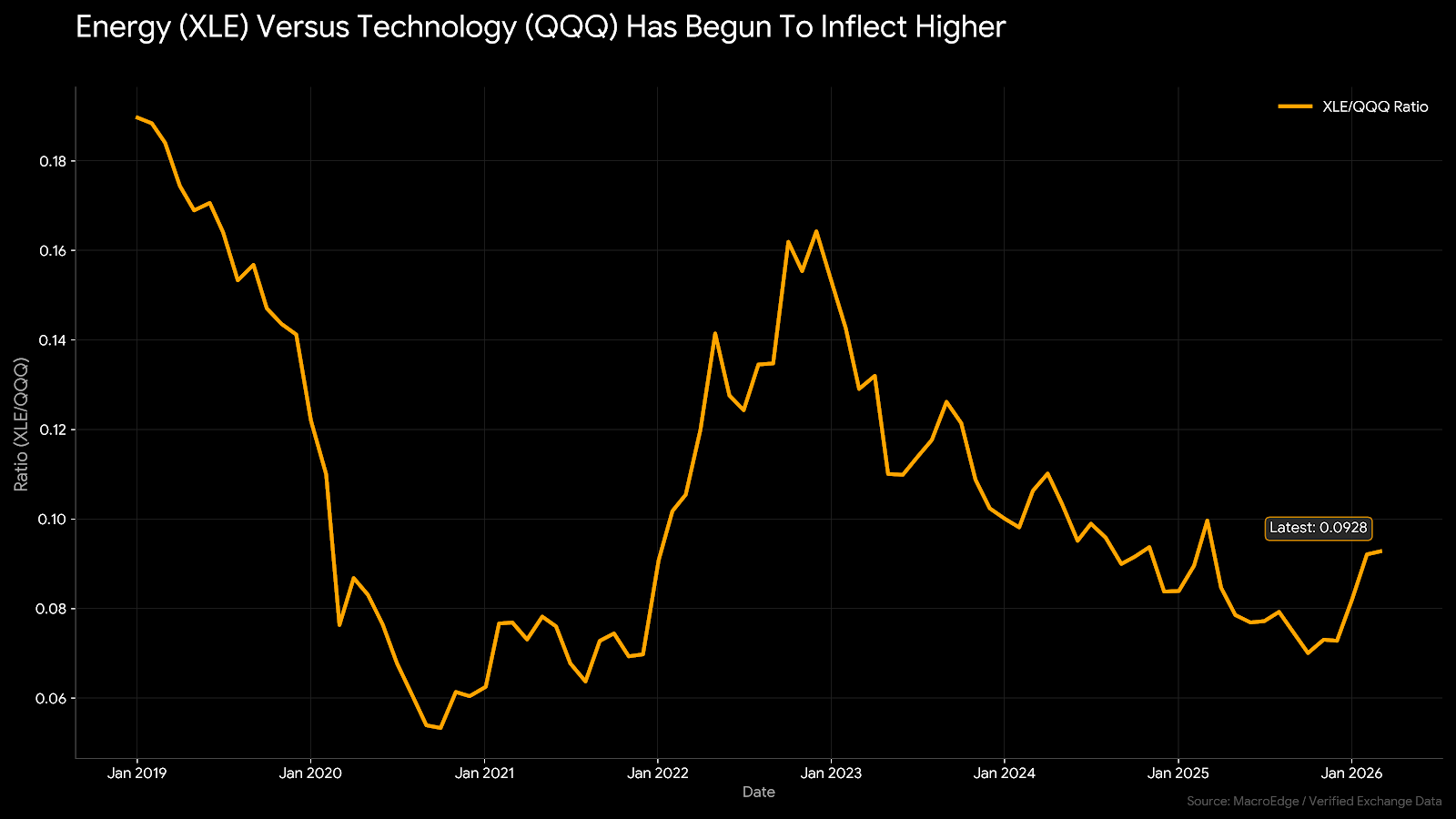

Today, we saw the first moment of public fear from the Administration over the spike in oil prices. Higher oil and gasoline prices are already hitting consumers, with the average consumer seeing an increase of gasoline prices of about 60 cents just this week. As highlighted a few weeks back, the energy (XLE) versus QQQ ratio has continued to inflect higher:

Continued below: “Oil Spooks Administration, Objective Energy Outlook, Natural Gas Discussion, MacroEdge Portfolio Strategy Update - Six)… upgrade to Ozone and try for one week, below:

This is a similar pattern that we saw post-06, and in the major inflation wave of 2021-2023. Oil stocks tend to lag the underlying a bit - which is why the correlation isn’t 1:1.

The Objective Energy Outlook

Even with technicals being on the extreme side - which is something that we should absolutely be wary of - the long-term technicals (monthly/3m) look very supportive of the early innings of this move on those time frames. As WTI reprices higher, it drags our beta-torque basket higher - especially in names like CHRD that have better direct correlation with WTI pricing being a Bakken producer.

1. China’s Export Ban Triggers Regional Supply Shock

Following the NDRC’s order to Sinopec and PetroChina to halt diesel and gasoline exports, the Asian refined products market has entered “panic mode.” Singapore gasoil cracks (refining margins) have surged by 22% in a single session. This move signals that China is bracing for a multi-month blockade of the Strait of Hormuz, prioritizing internal social stability and military readiness over export revenue.

2. WTI and Brent Near Critical Inflection Points

Crude prices are holding firm near recent highs. Market technicals in the short-term (daily) timeframe are getting extreme, but the monthly timeframe looks extremely constructive. The spread between Brent and WTI is widening as European refiners scramble for non-Middle Eastern barrels, specifically targeting West African and North Sea grades.

3. The “Hormuz Wall” and Maritime Paralysis

The Joint Maritime Information Center (JMIC) confirms that tanker transits through the Strait of Hormuz have effectively hit zero for commercial vessels. A massive “parking lot” of VLCCs (Very Large Crude Carriers) has formed in the Gulf of Oman, known as the “Hormuz Wall,” as insurers refuse to provide “War Risk” coverage for any vessel north of the 26th parallel.

4. Force Majeure Cascades Through LNG Markets

It’s not just oil; the energy shock has hit the natural gas sector. QatarEnergy has officially declared Force Majeure on several LNG cargoes destined for the UK and South Korea. Because the Strait of Hormuz is the only exit for Qatari LNG, the global gas market is facing its most significant supply disruption since the 2022 Nord Stream crisis. JKM (Asian gas) prices have jumped 15% today in response.

Natural Gas Discussion

While most fuel and energy related commodity prices have surged, Henry Hub has not been one of them…

The divergence looks supportive for a move higher in the days to come, and US LNG prices have lagged the huge moves we’ve seen in East Asia. Exposure through rock-solid names like AR is possible.

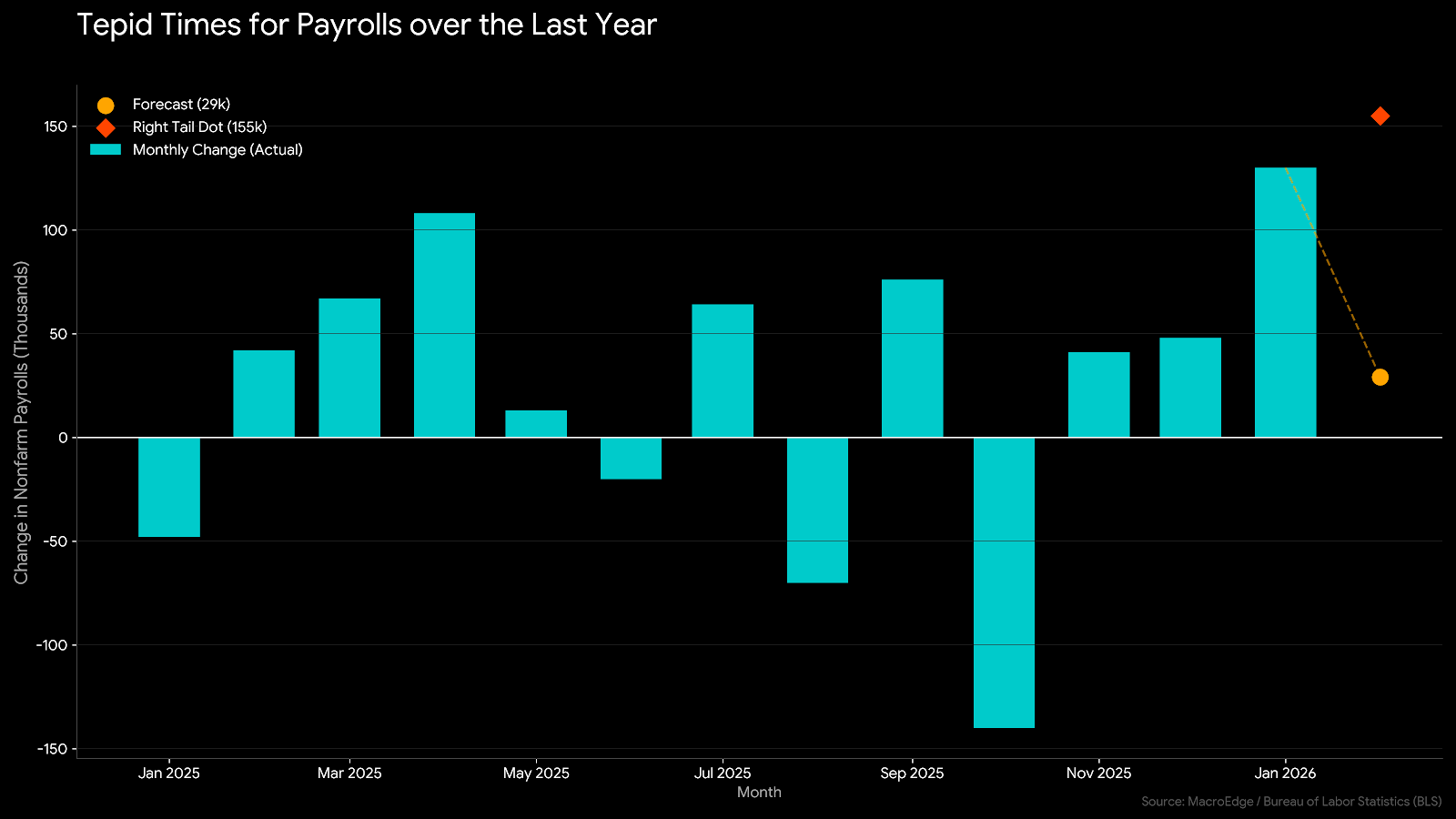

Employment Data Forecast - February

Tomorrow we will get the non-farm payroll data for February. With the spike in yields in the last few days due to the surge in energy prices across the globe, the Administration is going to want lower yields again, as higher yields slow down things like real estate activity going into peak season in many states (as well as lending, etc.). Rate cuts have now effectively been priced out through September, and an energy shock was the least forecasted scenario a month ago - especially from many of the academics on X in the oil & gas space who I follow closely and oftentimes find myself wondering how they came to their conclusions.

A hot print tomorrow is a slight right tail risk for yields and energy tomorrow, and given the issues with data quality, I actually foresee it as being probable. Below (the right tail risk - orange) and our forecast (yellow dot):

MacroEdge Portfolio Strategy Update - March 5, 2026 (@SixFinance, Head of Research)

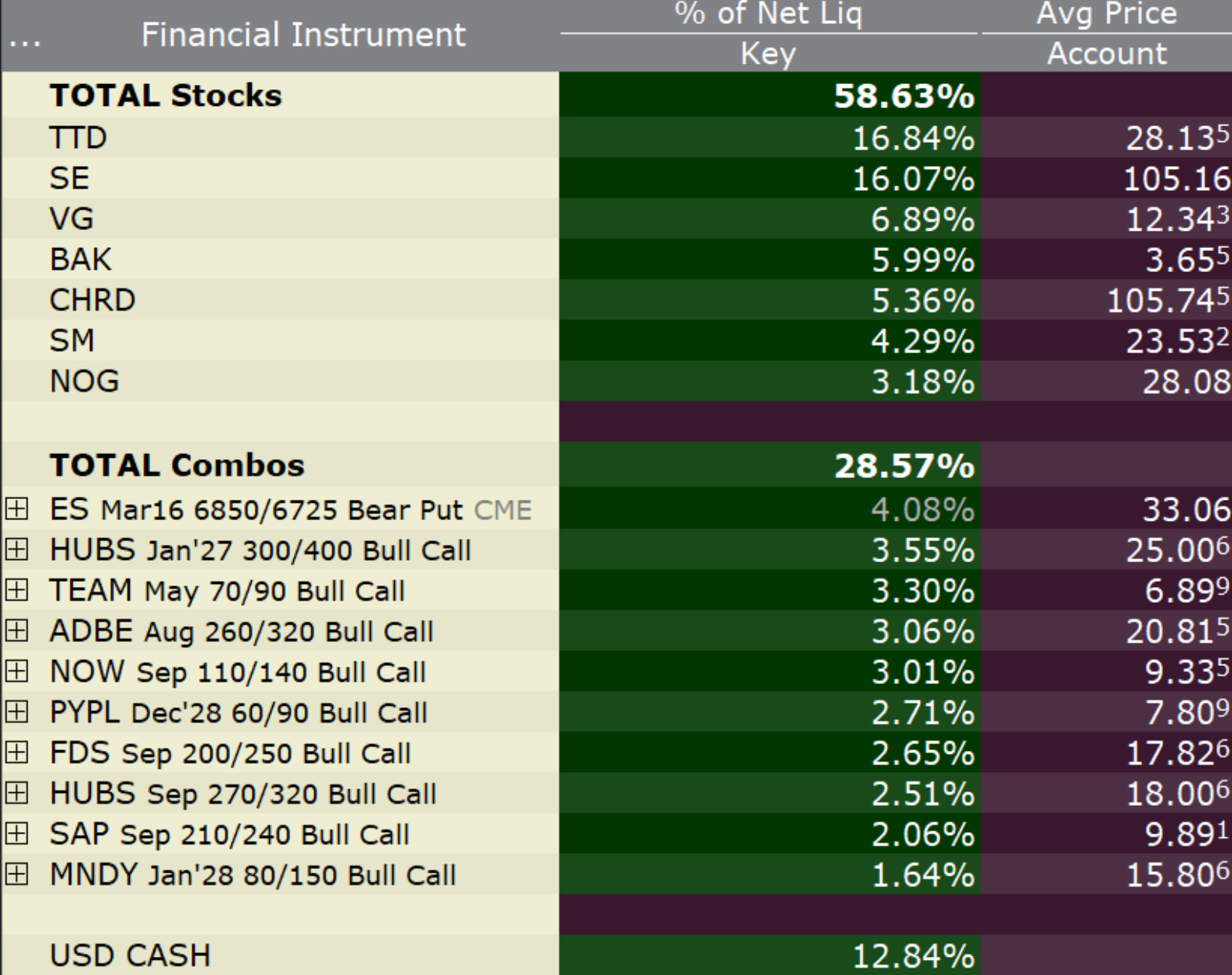

Current Exposure

It has been a fruitful yet wild week in the market, and an interesting start to the year. The levered software basket is performing ahead of schedule. I am nearly flat again after transitioning to IBKR on January 15th. February was a tough and mentally draining month.

The market is flush with opportunity. The recent volatility spikes globally have caused substantial degrossing, and one of the most popular hedge fund trades over the last year has begun to unwind. This is the most substantial outperformance of software over semiconductors on a percentage basis that I can find on record in such a narrow stretch of time.

Hedge funds have been aggressively long semis, and aggressively short software since the April lows. My target, as evidenced by the short legs of my bull spreads, is, in most cases, simply a rally back to their January 1st, 2026 area over the span of the coming months. This is not an area where I want to overstay my welcome, as the next AI headline is always lurking in wait for the software sector, and the technology is constantly evolving. This trade, for me, is purely tactical.

Bessent has moved to suppress oil prices and is believed to be selling oil futures, assumedly to deliver SPR reserves against them. The administration is seeking to dampen oil price increases. They are now issuing general licenses to allow Russian oil to be delivered to India. The longer the Strait of Hormuz stays closed, the longer we can expect energy to be well bid. Aside from adding additional oil exposure here (I am already well exposed), I have now added VG to the portfolio.

While US Henry Hub prices have not yet made a material move, global LNG prices have made a large move higher, as Iran has caused widespread natural gas infrastructure shutdowns across the Middle East, and the longer that supply remains offline, the more persistent the global LNG price premium will be. Dutch and Platts (asian) LNG prices have rallied over 50% this week relative to /NG (Henry Hub).

While the administration is targeting the suppression of oil prices (I remain long the E&Ps), the lack of a price surge in US natural gas prices implies that the Treasury will not be your counterparty in this section of the energy market (at least not yet). Venture Global VG is currently the most levered US LNG exporter to global spot prices. The primary driver of this high degree of operating leverage to global spot LNG prices is its massive uncontracted cargo base. While its peers in the US LNG export space maintain upwards of 90% of their output under long-term price contracts, VG, per their earnings call earlier this week, retains a 31% portion of their export capacity exposed to global spot rates. Per management, every $1.00/MMBtu increase in the spread between US prices and Dutch/Asian LNG spot adds $575m-$625m to their annual Adjusted EBITDA. VG’s 2026 guidance was based on a spread of $5-6/MMBtu (post shipping and cooling fees). That spread is over $9/MMBtu today, and is likely to continue to expand in a lengthened conflict.

TTD

I have taken a large position in The Trade Desk. The news coming out last night that they are in early-stage talks with OpenAI to support their emerging ads business seems a lot more credible and concrete than the headline would lead you to believe when you see that it was paired with the CEO buying $148m in shares on the open market in the three days leading up to the headline. This stock was a previous darling, and the massive vote of confidence via the CEO putting a huge amount of money where his mouth is tells me that the business may be about to substantially inflect, and that a growth reacceleration may be ahead.

I also added the ES 6850/6725 bear spread seen above on my sheet as a hedge for more extreme risk off. I plan to carry that through the weekend unless we break through the local lows tomorrow, and I can capture the majority of the spread’s value.

For more details, please refer to our Terms and Conditions.