Midweek Macro Note: Oil Crisis on the Horizon Pt. 3, Latest Oil Shock Data, Portfolio Strategy Update, Homebuilder Situation Update

In the Midweek Macro Note we discuss the oil crisis on the horizon (in part 3 of our energy crisis segment), talk about the latest oil shock data, deliver a portfolio strategy update, & talk builders

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge Readers & Community,

This afternoon, I departed the West Coast after a productive two weeks in Arizona and California, and I am heading to the Permian Basin again for several discussions on the state of all things oil and gas.

The market-at-large remains in a standby mode - as it has been now for the bigger part of 200 days (on the Nasdaq) as I highlighted earlier through a post on X. This was the fifth consecutive close below the 200dma for the QQQ, and longer term signals continue to point toward the last six months being a period of distribution and institutions setting up to roll things off onto retail. Retail trading activity has dipped lower in the past few weeks - as evidenced by both trading volumes, and the fact that total margin balances outstanding have begun to dip as well. For the S&P, it’s a similar story, with the index rejecting the 200dma today, and also showing weakness. This weakness is notable, and the blatant manipulation of WTI through crude oil futures was largely ignored by the end of the day, with oil prices closing flat on the day. As we discuss below, given the magnitude of this supply shock, there is still a fair chance that WTI prices move considerably higher than their Sunday overnight high from two weeks ago. Even if that doesn’t materialize, this $90/bbl environment provides huge tailwinds for the sector - and the names in our portfolio strategy basket.

Five days below the 200dma for the Nasdaq:

On the geopolitical front - until we have actual confirmation from both sides of a meeting, I would take a lot of the latest *developments* as noise. There’s a lot of manipulation going on right now in markets - and people are paying for certain stories to get attention to benefit their own positions. On the energy shortage front, we’re starting to see problems in East Asia and Australia, with about 10% of petrol stations in Australia now facing supply issues. Over the next week, that figure could get in the 30-50% range, since it will take months to get the energy supply chain stabilized after this shock. Bids for tankers still need to go a lot higher in my opinion, and WTI is still underpriced given the entire risk profile of where things stand in this conflict. $100/bbl WTI is clearly a panic threshold for the time being, but the setup without immediate resolution by the end of the week is going to be one where we see WTI begin (again) to reprice into a higher price floor than this $85+ level we’re now seeing it settle into. With all of that being said, let’s take a look at the latest data below, and we’ll have more on Friday evening as the week progresses.

In addition to the price pressures, war, and oil trends, we’re going to take a brief look at the latest update for homebuilders, which have faced great equity selling pressure from the beginning of the war.

MacroEdge Economic Advisory

Our state-of-the-art Economic Advisory offerings are driving impact around the globe - and our team is ready to help guide you and your enterprise through the complex modern macro landscape. From monthly conference call connections to specialized reports, data collection, strategic guidance, portfolio strategy, and much more, the MacroEdge team is ready to deliver results for you.

Get in touch with us today, and find out how our Economic Advisory solutions can deliver a tailored impact with our urban economics approach: https://www.macroedge.net/advisory (contact section is available at the bottom of the page).

We work with oil and gas firms, individuals & wealth managers, and executive teams to guide you to success.

Our 24/7 monitoring of the situation in the Middle East will continue as long as it takes to get the correct data out to our community and clients across the globe.

Get in touch with us today by filling out the form below:

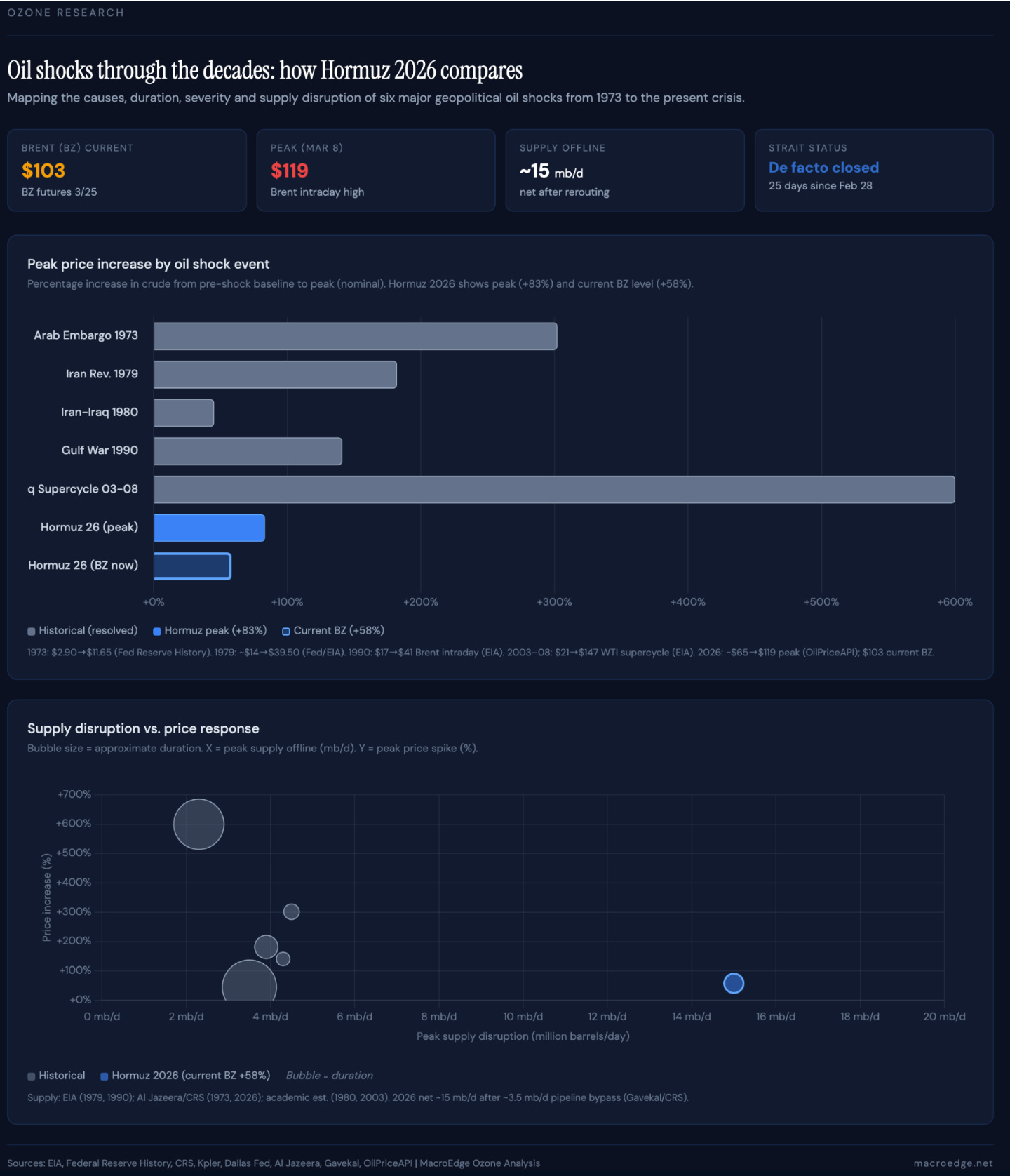

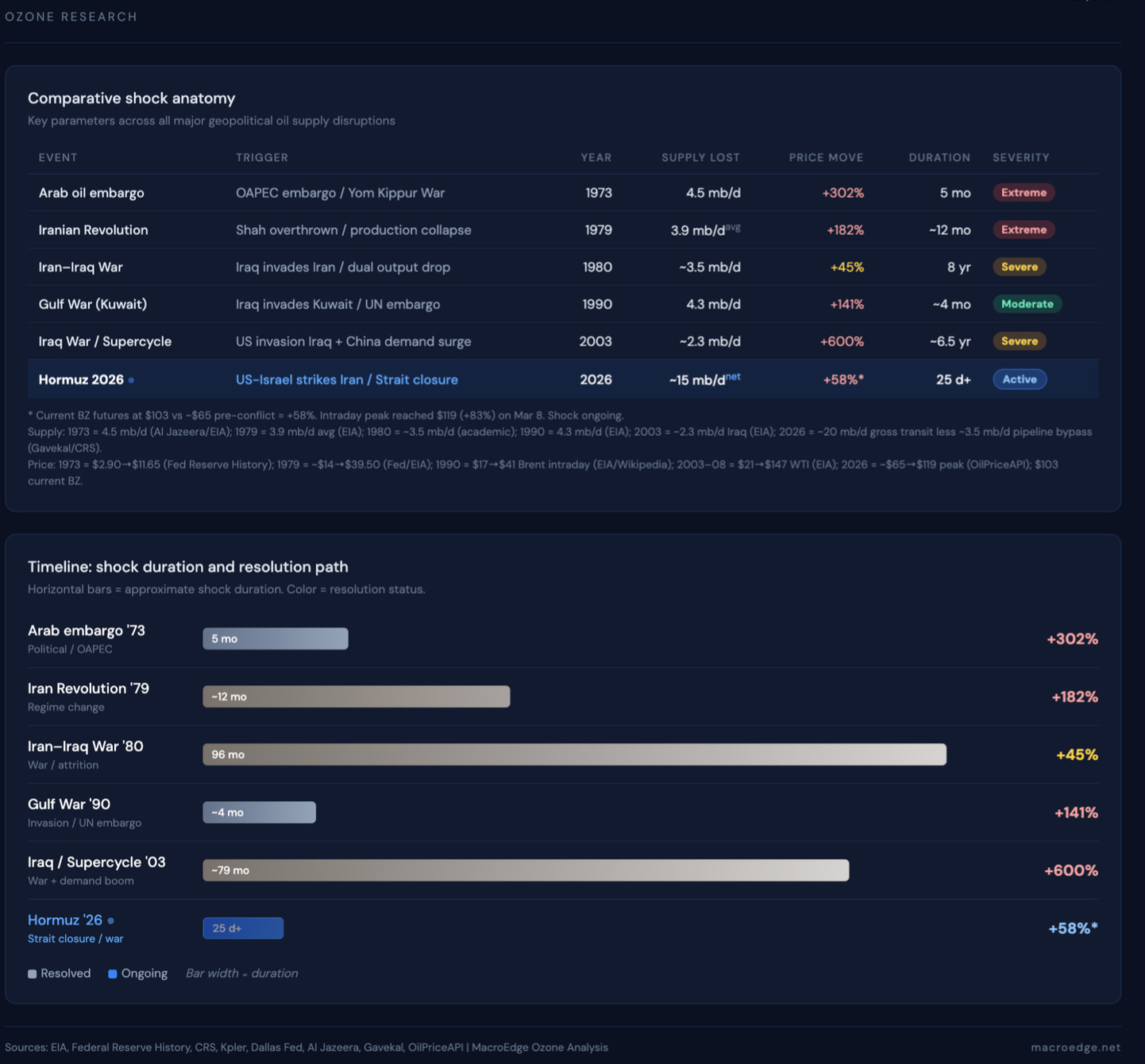

Latest Oil Shock Data

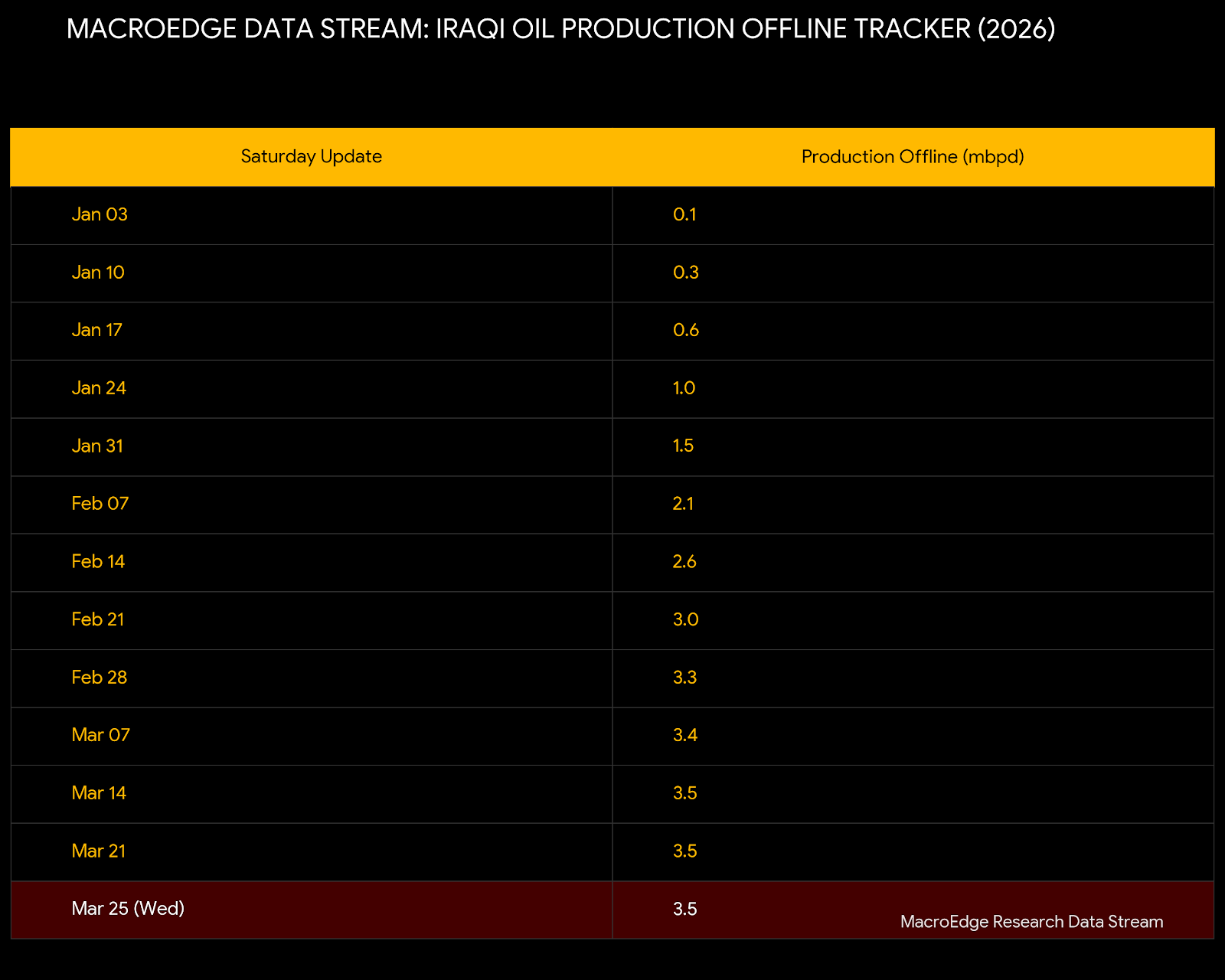

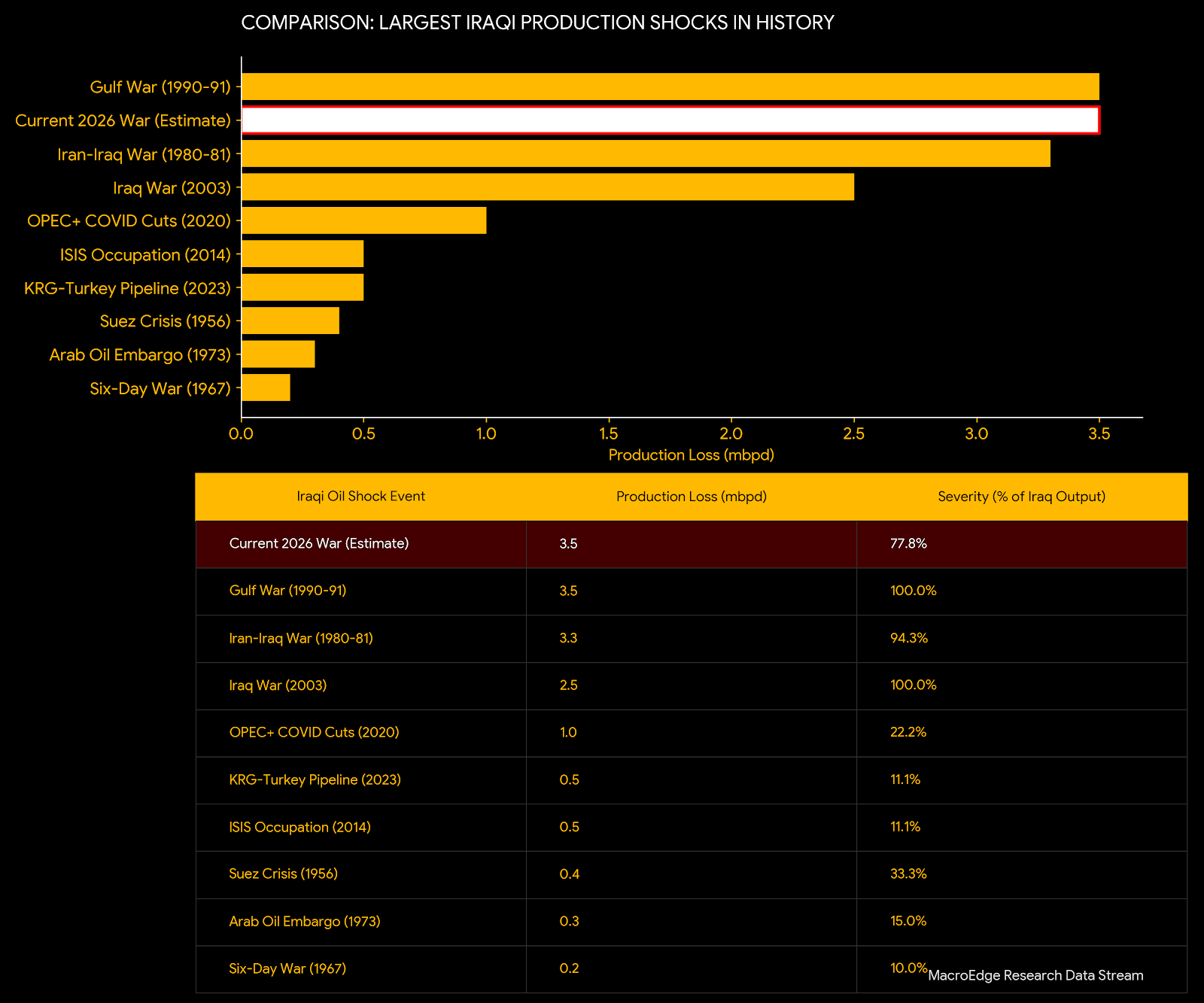

With major Ukrainian strikes on Russian oil output, and Iraq oil exports now being shut-in to the tune of 3.5mbpd, this oil shock continues to make records versus previous shocks.

In Iraq, production outages now total 3.5mbpd:

(continued below: oil shock data continued, the latest WTI look, oil & gas portfolio strategy, homebuilder situation, & much more, all below):

This is tied for the largest Iraqi production outage on record:

The Latest WTI Look →

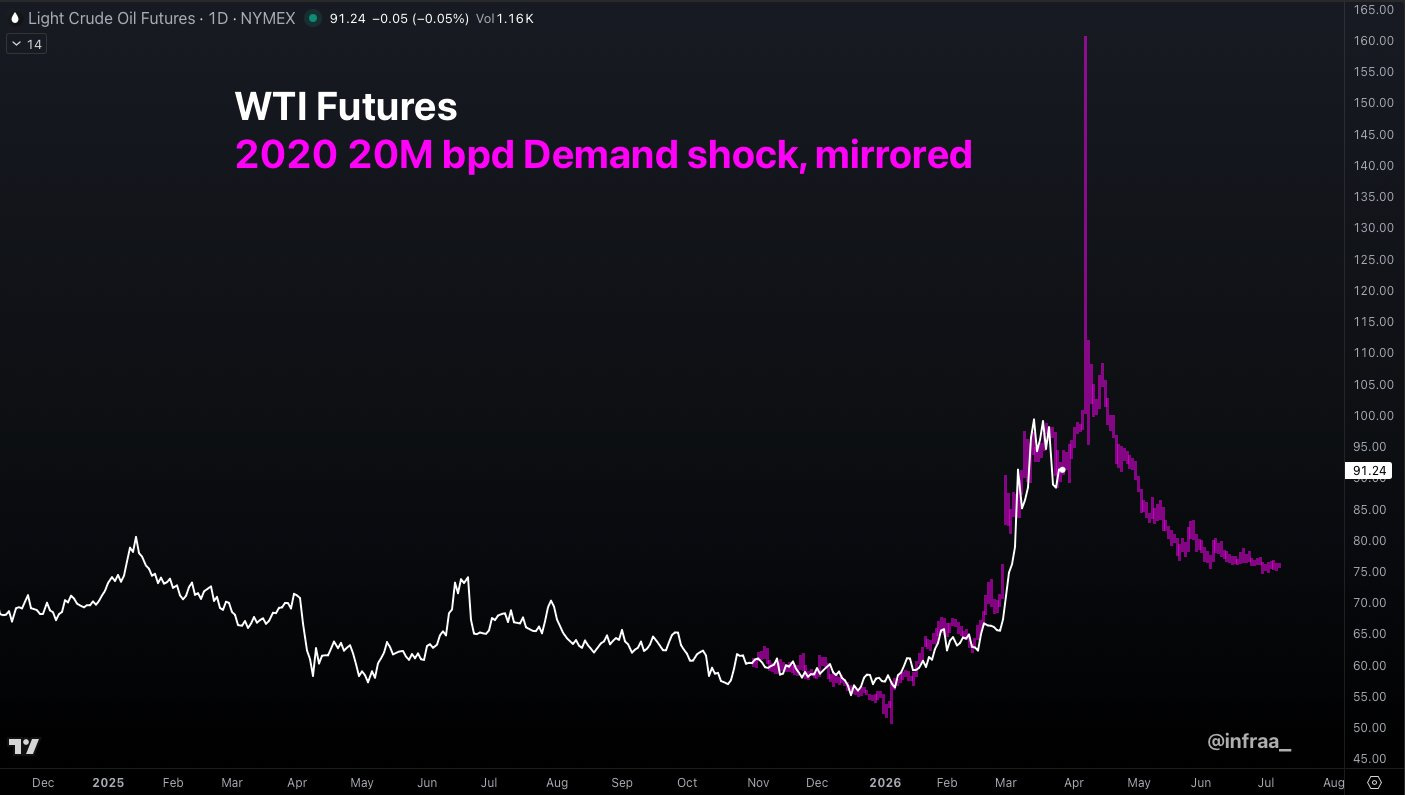

The latest WTI technicals are constructive (4hr) and pointing to higher price levels in the coming days.

Technicals have cooled way off from the major Sunday night run-up two weeks ago, and that’s allowing WTI to settle into a higher price level.

From @infraa_ on X - the inverse COVID situation for oil prices overlaid highlights a very similar pathway (but in the opposite direction):

This scenario is completely possible given the data and production shock that’s still yet to be realized across the globe. While the US may be more insulated from a true crisis of going to the pump and being unable to get fuel, we may not be able to afford that fuel (hence demand destruction), and oil is a global market with global pricing…

For the time being, drilling activity is not yet ticking higher, though we’ll keep a keen eye on rig counts and frac spreads for signs.

Our Oil & Gas Portfolio Strategy

Our oil and gas portfolio strategy has continued to perform well since the beginning of March. There are likely a few minor adjustments that will be made here over the coming week - as I seek to optimize our high-torque upside with Six. The past 30 days have validated the core thesis that structural underinvestment in the global energy complex is creating a significant valuation gap. As WTI Crude exhibits volatility in the $91–$97 range, the market is beginning to reward operators with high capital efficiency and unhedged exposure to the barrel.

We are currently evaluating strategic adjustments to our ownership in particular equities to capture greater torque. This may involve rotating out of stabilized “anchor” positions into higher-beta names that offer more aggressive operating leverage in a sustained high-price environment. Below is a look at our basket on an individualized basis.

ProFrac Holding Corp (ACDC)

Performance: Shares have added approximately 78.9% YTD, significantly outperforming the broader market despite a reported Q4 loss. Revenue surpassed estimates by nearly 12%, signaling a resilient operational engine.

Tailwinds:

Power Infrastructure Pivot: Expanding into power generation and data center infrastructure offers a decoupled, long-term revenue stream.

Credit Extension: A recent amendment extended the company’s credit facility maturity to late 2027, providing a cleaner runway for its transition.

Headwinds:

Debt Servicing: High interest expense remains a primary hurdle for a full valuation re-rating.

Earnings Consistency: The company has missed EPS estimates in three of the last four quarters, necessitating flawless execution in 2026.

HighPeak Energy (HPK)

Performance: Momentum has surged in March, with the stock up 25% over the past two weeks and trading near $6.90.

Tailwinds:

Capital Discipline Shift: A new 2026 strategy prioritizes free cash flow over production growth, including a 50% reduction in capex.

Unhedged Exposure: As an independent producer with significant unhedged oil production, it acts as a high-beta lever for rising crude prices.

Headwinds:

Small-Cap Volatility: Daily price swings can reach 10%, making it a high-risk/high-reward instrument.

Revenue Miss: Q4 revenues missed estimates by 13.5%, highlighting the sensitivity to localized operational performance.

Permian Resources (PR)

Performance: Up roughly 31% YTD, recently achieving investment-grade credit ratings from S&P and Fitch.

Tailwinds:

Efficiency Leader: Reduced D&C costs to $700 per lateral foot, a 14% year-over-year improvement.

Increased Returns: Management recently raised the quarterly base dividend by 7%, reflecting confidence in FCF durability.

Headwinds:

Valuation Ceiling: Trading near 52-week highs, some analysts suggest the stock may be reaching a “fair value” plateau relative to cash flow.

Antero Resources (AR)

Performance: Shares surged 5.4% recently, hitting a 52-week high of $44.02 earlier this month.

Tailwinds:

Liquids & LNG Edge: Superior transport portfolio to the Gulf Coast provides a price realization edge for NGLs and natural gas.

Deleveraging Success: Long-term debt has been slashed to $1.4 billion, down from over $3 billion at its peak.

Headwinds:

Gas Price Volatility: Despite the oil spike, sudden shifts in Henry Hub pricing remain a core risk to the revenue profile.

Chord Energy (CHRD)

Performance: Trading near $137, the stock has seen a strong 37% run since mid-February.

Tailwinds:

Bakken Consolidation: Integration of new assets is proceeding ahead of schedule, with 40% of 2026 wells planned as high-efficiency 4-mile laterals.

Shareholder Yield: Declared a robust $1.30 quarterly base dividend with a commitment to returning 50% of FCF.

Headwinds:

Technical Resistance: High RSI levels suggest a potential short-term cooling period after a nearly parabolic run.

SM Energy (SM)

Performance: Up 12.3% in March following a major $1 billion debt refinancing move.

Tailwinds:

Balance Sheet Optimization: New 2034 notes at 6.625% replace higher-coupon debt, lowering long-term interest costs.

Uinta Basin Potential: Strategic focus on high-return development projects in its expanded asset portfolio.

Headwinds:

Logistics Bottlenecks: Continued reliance on Uinta Basin infrastructure remains a risk to realized margins.

Viper Energy (VNOM)

Performance: Maintaining a steady profile, up 5% recently, trading near $47.60.

Tailwinds:

Fortress Balance Sheet: Recently closed a $617 million non-Permian divestiture, nearing long-term net debt targets.

Royalty Model: High-margin business model with zero capital requirements provides a stable floor during volatility.

Headwinds:

Lower Beta: As a royalty play, it typically lacks the explosive daily upside seen in service or unhedged production names.

The Homebuilder Situation (Yikes)

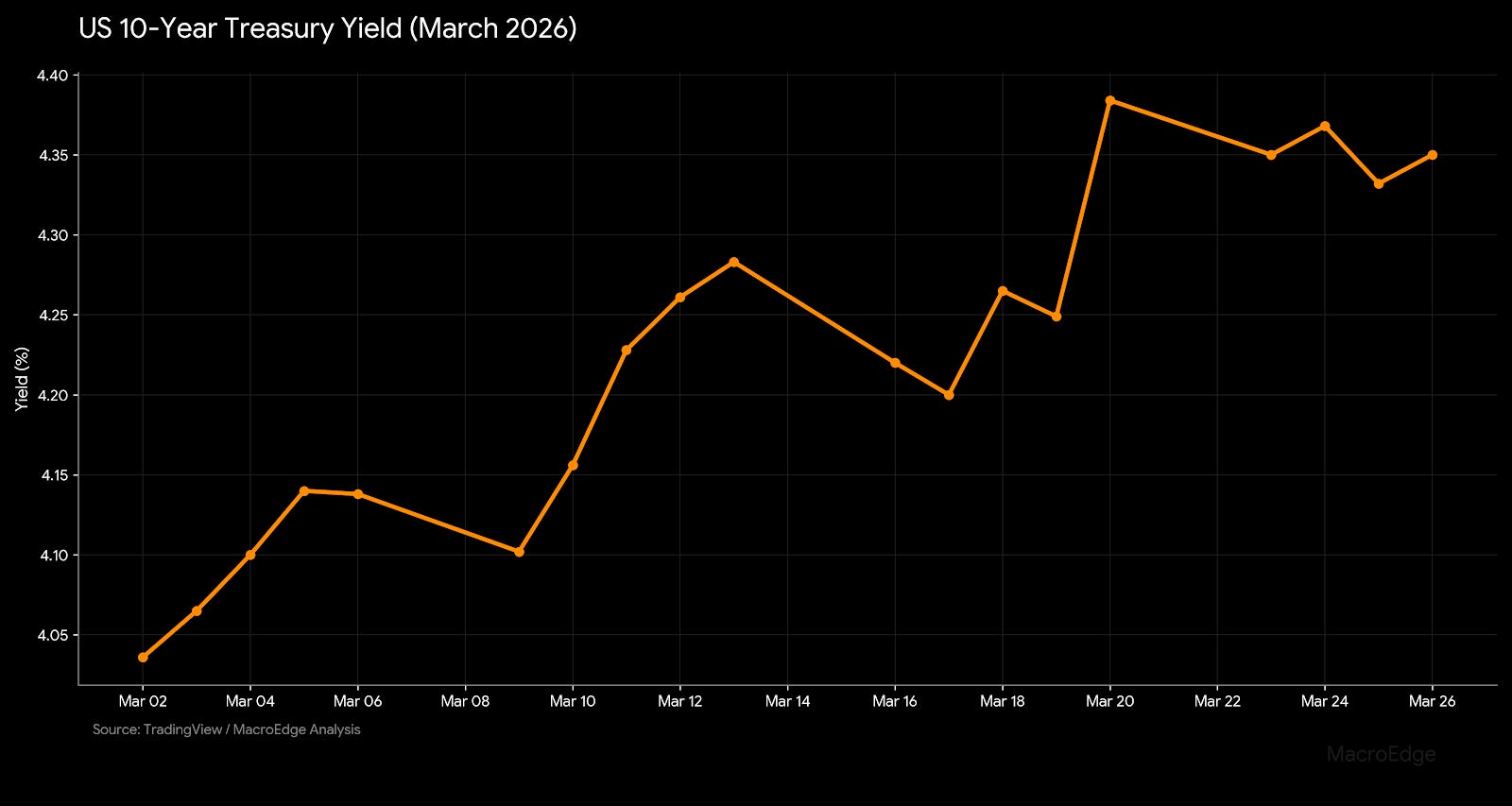

The situation for homebuilders was expected to be markedly better coming into 2026. With the 10Y originally dipping lower and optimism just ticking ever so slightly higher on the macro picture, that’s all been reversed with the Israel-Iran war in full swing. The 10Y is now back in the 4.4% range, and the Trump Administration has a ceiling at about 4.45% when they begin to intervene… that situation is exacerbated by the fact that the US government has to refinance approximately $10 trillion in debt over the next 12 months… primarily in short-term debt.

Homebuilding equities like Lennar are suffering greatly as the math on American housing continues to make zero sense:

Even premium builders like Toll Brothers have suffered:

There’s a lot happening right now and very quickly, and I look forward to my next update from Midland. If you would like to learn more about all the fantastic things we’re doing with our Economic Advisory solutions, don’t hesitate to email me at Don@MacroEdge.net.

Have a great Thursday!

MacroEdge Portfolio Strategy Update - March 25, 2026 (@SixFinance, Head of Research)

The Iran war continues to weigh on markets, but green chutes of optimism have reemerged, coinciding with at least a local top in oil prices. It’s anyone’s guess - unless you are subscribed to the early bird Truth Social special - how near-term price action resolves, but clear attempts to arrest global bond market volatility and de-escalate tensions have also arrested the decline in equities. While POTUS certainly cares about the Dow Jones Industrial Average, the drastic spike in the MOVE index on Friday was much more certainly the culprit behind the forced TACO on striking Iranian energy infrastructure threats. While the yield spike in US sovereign rates were nothing to sneeze at, there were even more significant impacts in certain ex-US markets, like UK 2-year yields rising 120 basis points in just three weeks.

Financial conditions have tightened considerably. Rate cuts have been priced out of the forward curve. In many developed markets, one or more rate hikes are now priced in. The RBA has already hiked twice this year, and the BOJ has reiterated its commitment to hike again. Raising interest rates is undoubtedly the wrong medicine to deal with a supply shock with no accompanied positive demand impulse. If global central banks make this error, they risk ending the business cycle.

SPX continues to reject the 200-day moving average to the upside, but also isn’t moving lower. Undoubtedly hoping for an imminent resolution and a normalization of the Strait of Hormuz. While the energy shock is severe, and there are many reasons (private credit included) to be bearish, it is important to examine the case for continued upside in equity prices. In my view, the pathway to equities shrugging this off COULD look something like this:

A palatable deal gets done that normalizes Hormuz traffic.

Unprecedented global oil reserve release adds consistent supply as Gulf countries restart production.

Energy price volatility collapses.

Interest rate hikes priced out of the global curve, financial conditions ease.

Equities refocus on secular thematic trends, news flow moderates, business as usual.

It may not be quite that easy, but it’s important to keep an open mind.

Alternatively, if a deal does not get done, especially one that Israel cannot sign off on as they seek to “settle all family business” in the Middle East, US troops are moving into position for potential boots on the ground. The risk of additional “Hail Mary” strikes on regional infrastructure by Iran is still present, and if done at scale, has the potential to take oil prices to new highs and introduce extreme volatility across asset classes.

The main takeaway is that we simply do not know at this stage, and rather than be a cowboy, I would rather barbell long energy and ags against a large SOFR long. I continue to accumulate H8 SOFR futures, as the weak labor market and supply shock without a positive demand impulse seems clearly pointed toward lower future short term interest rates. If oil prices were to really blow out to the upside here, I also see the potential for short term interest rates to fall off a cliff.

Despite disagreements over which direction the next $20 per barrel Brent is heading, most can agree that this conflict will raise the oil price to a higher base, and continue to carry a risk premium.

With such a large relative oil shock on a bpd basis relative to prior shocks, and capacity unable to come immediately online in conflict resolution, we can likely expect sustained premium pricing, at a level that allows energy firms to continue to prosper. A stabilization above 75 but below 90 would likely be the most bullish outcome for the energy sector over the balance of the year.

For more details, please refer to our Terms and Conditions.