Midweek Macro Note: Nonfarm Preview, Latest Energy Data, Asian Risks Part 2

In the Midweek Macro Note we discuss our nonfarm preview for payrolls tomorrow, highlight the latest energy data, look at Asian risks, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge readers & community,

This evening we’re going to take a look at the latest energy situation and data, and cover where we stand going into the longer than usual market weekend - with markets being closed on Friday. While banks remain open, markets will not, so trading in Asia will dictate how our week starts for the most part. Tomorrow we will also get our June labor market data drop - which should mostly be noise as most of these NFP prints have become. JOLTS didn’t give us that much information, and ADP came in softer than expected, yet yields surged as markets re-priced in a hike this year (which I could only see happening if Warsh decides that it’s time to pop the bubble). The asset economy is the widest I’ve ever seen from the income economy, and I am not sure policymakers understand this any longer - given the composition of where the policymakers come from/backgrounds - it’s going to take stopping nominal prices from rising to actually do anything to reverse this trend.

Tomorrow should be a very thinly traded session as the last of the serious shops packed up their bags for the Caribbean, Aspen, or whatever 2nd or 5th home fits the theme of the ‘America 250 weekend’. On Friday evening, we’ll have a brief recap and look at the employment report coming tomorrow - and for the remainder of the week - for those hanging around, it’s watching and seeing how Korea and Japan go the rest of the week (along with Taiwan to a degree). I expect that we will see another more serious intervention in the JPY soon, and continue to monitor the KRW. What we have in Asia right now is arguably the most serious bubble in decades, and I think downside in both the KOSPI and Nikkei will be more severe than here in the US due to an even higher degree of market concentration of the AI/semi/RAM names in Korea (like ~75% of the KOSPI).

This evening, we’re going to take a look at the employment preview, talk about the next report (coming on Friday), discuss Asian risks, and more. I also will note that I continue to expect distribution or higher price action until we see crypto crack further - right now we’re in a waiting pattern across the board as equity gains have mostly stalled since May-early June.

Next Report - Friday Evening (4th Preview, AI Wobbles, and June Employment Data Note)

In the Friday ‘Redeye’ Macro Note, we’ll cover the latest on the AI Wobbles - including coverage on the pressure on the sector as tokenomics begins to crumble, take a look at the second half of the year for MacroEdge, and our first half-year in review - including some of our most notable calls, and cover the June employment data. Don’t miss it.

Friday Redeye Macro Note Preview

A Look at the Second Half of the Year for MacroEdge

A Look at the Best Moments from 1H from our Team

The Latest AI Wobbles

June Employment Data Recap

Not yet a MacroEdge Ozone subscriber? Upgrade today at MacroEdge.world/subscribe for all of our portfolio strategy work, research, data, commentary, and much more from the MacroEdge team.

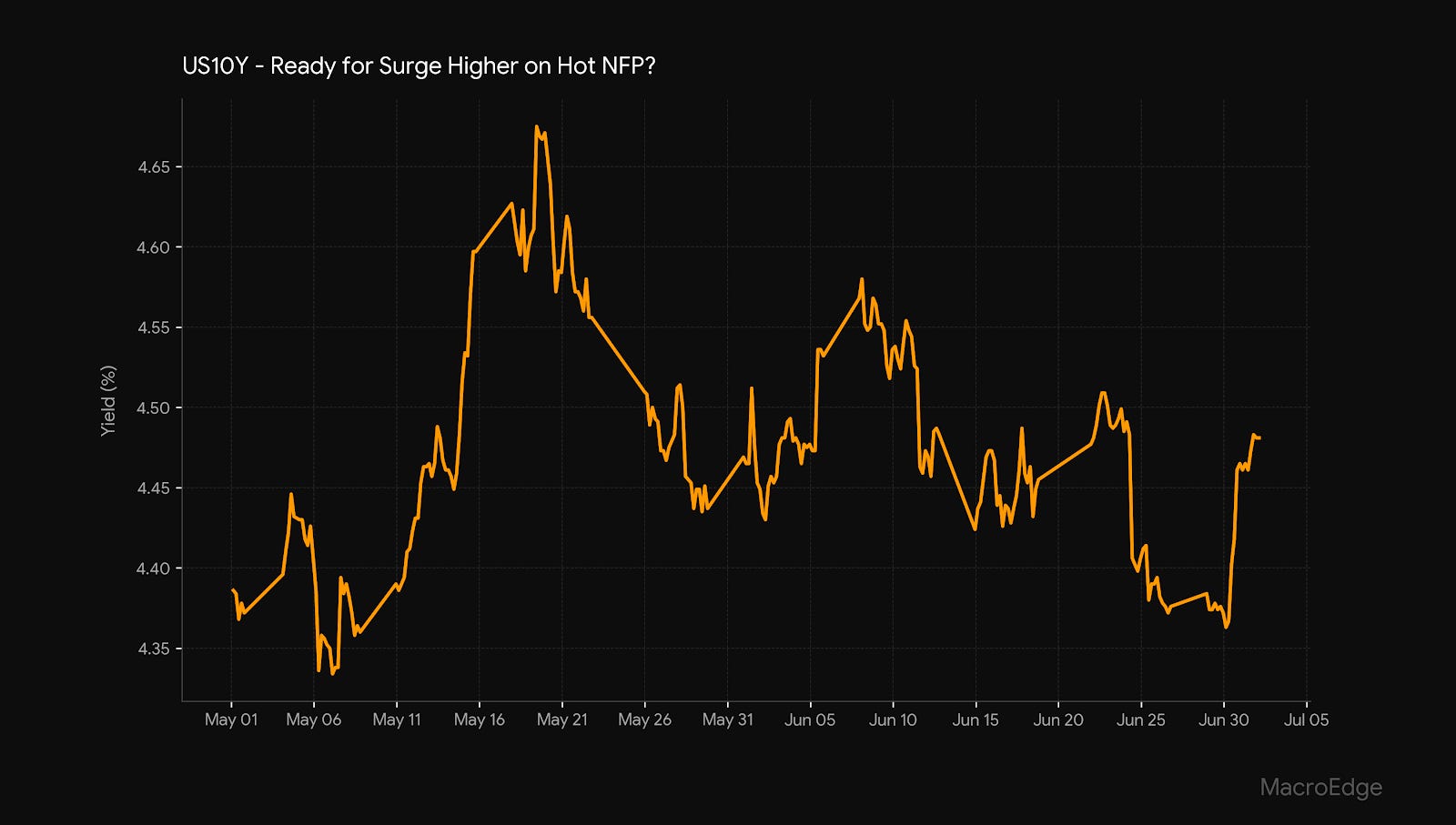

Employment Preview and NFP-Look

The NFP tomorrow is actually quite directionally important for the 10Y - which has been moving back higher as treasuries have sold off:

Continued below: Employment preview and NFP look, Latest Energy Data - what’s next?, Asian Risks Pt. 2, Latest Energy Data - What’s Next?