Midweek Macro Note: Letting the Dust Settle, Trump Caves to Bond and Currency Markets

In this Midweek Macro Note - we dive into the historic 'Las Vegas' style market action experienced today, discuss how they impacted equities, and how Trump was forced to fold by the bond market.

Good Wednesday evening MacroEdge Readers & Community,

Today, we finally got the Trump put from rising financial market stress indicators that included credit, bonds, default risk, and more. As I (and our team) was highlighting overnight yesterday - things began to go poorly in Japan and the Bank of Japan and Ministry of Finance convened an emergency financial meeting, signalling an interim short-term put, aka bailout in layman’s terms, for markets. With the VIX parked near 50 at the beginning of the morning and headline expecters lighting up the tape prior to the Trump post on Truth Social. This risk for central bank and fiscal intervention was high as I noted in the opening of our Sunday evening Weekly Macro Note. In modern era investing - especially when capturing the left tail events - you always need to be paying attention to intervention actions for shorter-term moves like the ones we saw today - which ironically resulted in a right tail risk materializing.

The reality check for some people is that there is no 5D chess being played here. The bond market - which Trump was watching as his tariffs took effect - caused him to capitulate as the basis trade and whatever levered up HF crap of the day out of Japan began to unwind. Retail completely took the bait today, sending volume multiple standard deviations above usual, and people declaring that their follies were over as a new era of speculation was just over the horizon. Myself and our team just don’t think that way - nor do we let outlier moves abruptly change the broader view here for 2025. It was a combination today of a squeeze, bailouts, the Trump put, and excitement about tariff delays that let the markets crush volatility for an afternoon and send the elusive bears of the 2023-24 era hunting for better opportunities in waiting. Today’s move was the largest jump in the Nasdaq since January 3rd, 2003 - when a Fed put sent markets up over 14% in a single day, and for the S&P the largest since the bailout package was announced in late 2008. Historic, nonetheless, and the speculators of today can walk away licking their wounds from the rather abrupt yet forecasted 27% pullback on ^IXIC from late February to Sunday evening.

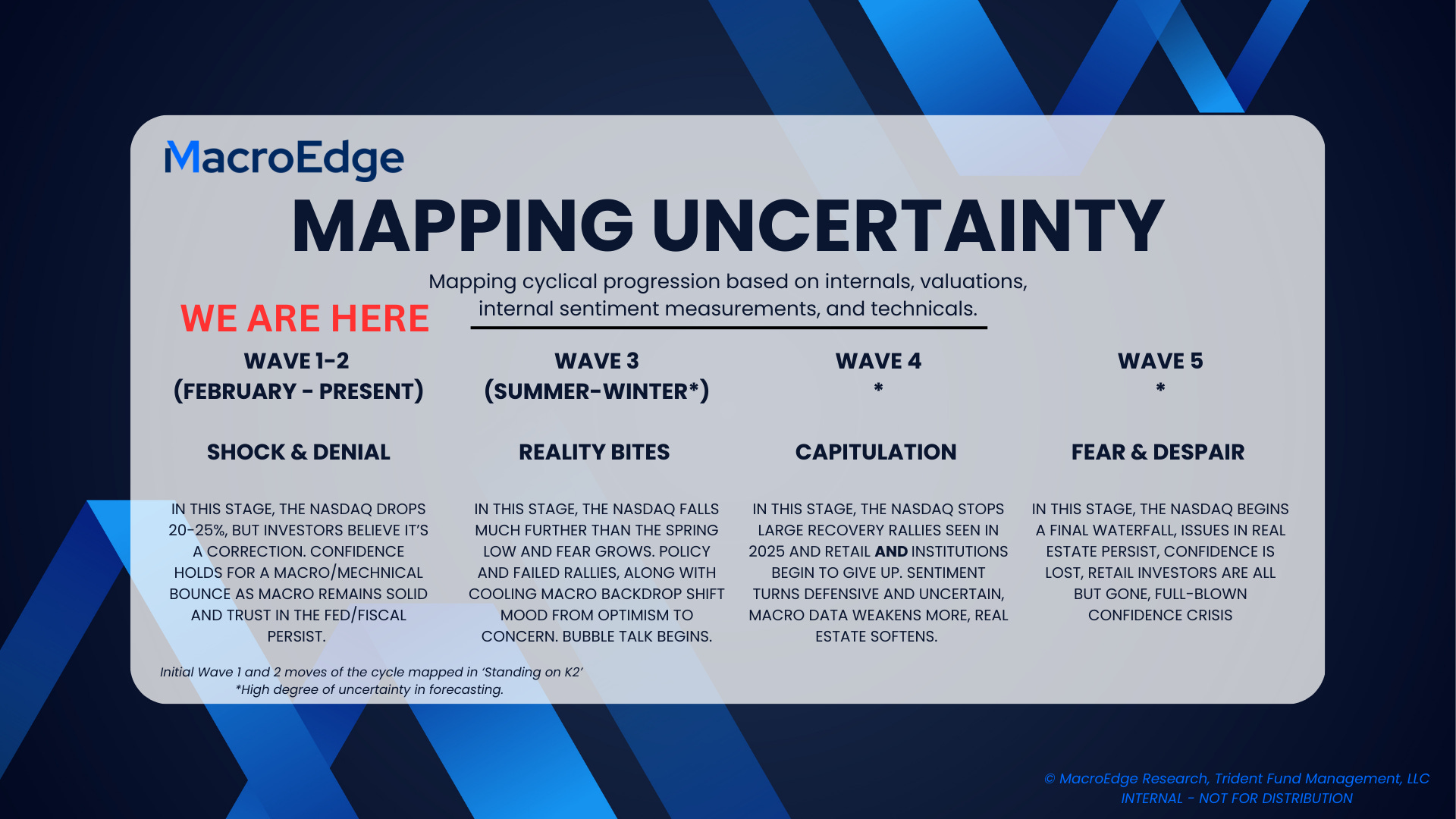

What this move does not do - is change our market view. In crafting our macro-driven forecasts - I am factoring more than single-day price action - and turning to a broader view of technicals, internals, and valuations to drive our outlook for markets. While the Trump Risk Matrix remains at top of mind - and one of those key risks abated today as Trump got tepid on his more aggressive tariff packages - there are still risks including additional Chinese responses to the tariffs, the continued Yen carry trade risk, inflation/employment risks, and near-record high valuations that signal caution in the equity markets. Our broader framework and timeline remain outlined below, now as we see retail get more comfortable in firing off high-risk bets again.

Copyright © Trident Fund Management, LLC

We’ve already temporarily downshifted out of the shock & denial stage - and people ate up the fiscal put today from Trump / Bessent - which is why we saw the reaction that we did. Similarly to other major market tops and weekly breakdowns historically, we see sharp reactions like the one we saw today as investors attempt to claw back their ‘up only’ glory days of the blowoff rally. I encourage readers to pay close attention to past failed rallies that result in second major lower highs as I expect we are on course for. The reason I expect that is that Trump is lacking the support of the Fed today - unlike in his 2018-2019 days where he was able to successfully jawbone Powell into reducing rates to near zero to get economic activity moving again. That’s not to say that Powell and Bessent aren’t discussing, or even collaborating on their policy moves, but the Trump impulse for breaking the Fed’s back isn’t as powerful as it was (at least thus far) in his 1st term. If the Fed does pivot to a more supportive stance - it’s important to leave open a more 2018-style scenario - even though the valuation and internal backdrop is starkly different. As we progress into late Spring - we’ll begin to reflect changes in the above uncertainity map - it’s rarely the impulse 1 & 2 move that gets investors offsides enough to stop shoveling money into the third most expensive market on record, by our measures. One thing I do want to happen is a quieting down of the ‘retail bear’ crowd that seems to still be especially loud - this happens as things settle down and we get lower (than 35) on the VIX)

Without rambling - and to keep our Midweek Macro Note concise - let’s dive into our commentary below.

Trident

Learn more about our private global macro fund in development - focused on capitalizing on substantial inflection points in both major asset classes and individual securities - by submitting a contact form through the link below. We’re delivering on a high-concentration investment philosophy focused on critical market inflection points and left-tail events. Much more in a full post coming shortly on Trident…

Accredited investors only. SEC 506(C) Reg D

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.