Midweek Macro Note: January Employment Outlook - A Slow Burning Dumpster Fire Continues

In our January Employment Outlook - we discuss our forecast for the month and look at all of the data releases thus far. We also discuss the 'strong dollar policy' narrative nonsense, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Tuesday evening MacroEdge Readers and Community,

This evening we’re going to have a look at the employment data for January and cover our forecast for the month. The employment market continues to soften, as it has for the better part of two years. With government job cuts added into the mix, it’s enhanced the softening trend we’ve seen over that time period and added some fuel to the fire through higher unemployment and one of the slowest hiring paces we’ve seen since 2000. Outside of a recession, this is the weakest labor market (broadly) and will likely be the weakest month for employment since the early 2000s. Due to dynamics shifting in demand for labor, a more international workforce, and prioritization of foreign labor to fill entry-level roles in lieu of US graduates, things continue to shift in the labor force. While the Administration is citing ‘deportations’ for near record-slow hiring rates, it’s actually the pause on inbound migration contributing the most to this figure. The ‘human-QE’ effect we saw under Biden greatly inflated jobs #s, and tomorrow we’re going to see further revisions to the employment data from last year, potentially by a factor >1 million jobs subtracted away from headline payrolls. The revision trends continue to be greatly troubling from a data accuracy standpoint, and there’s a lot that needs to happen to improve data quality.

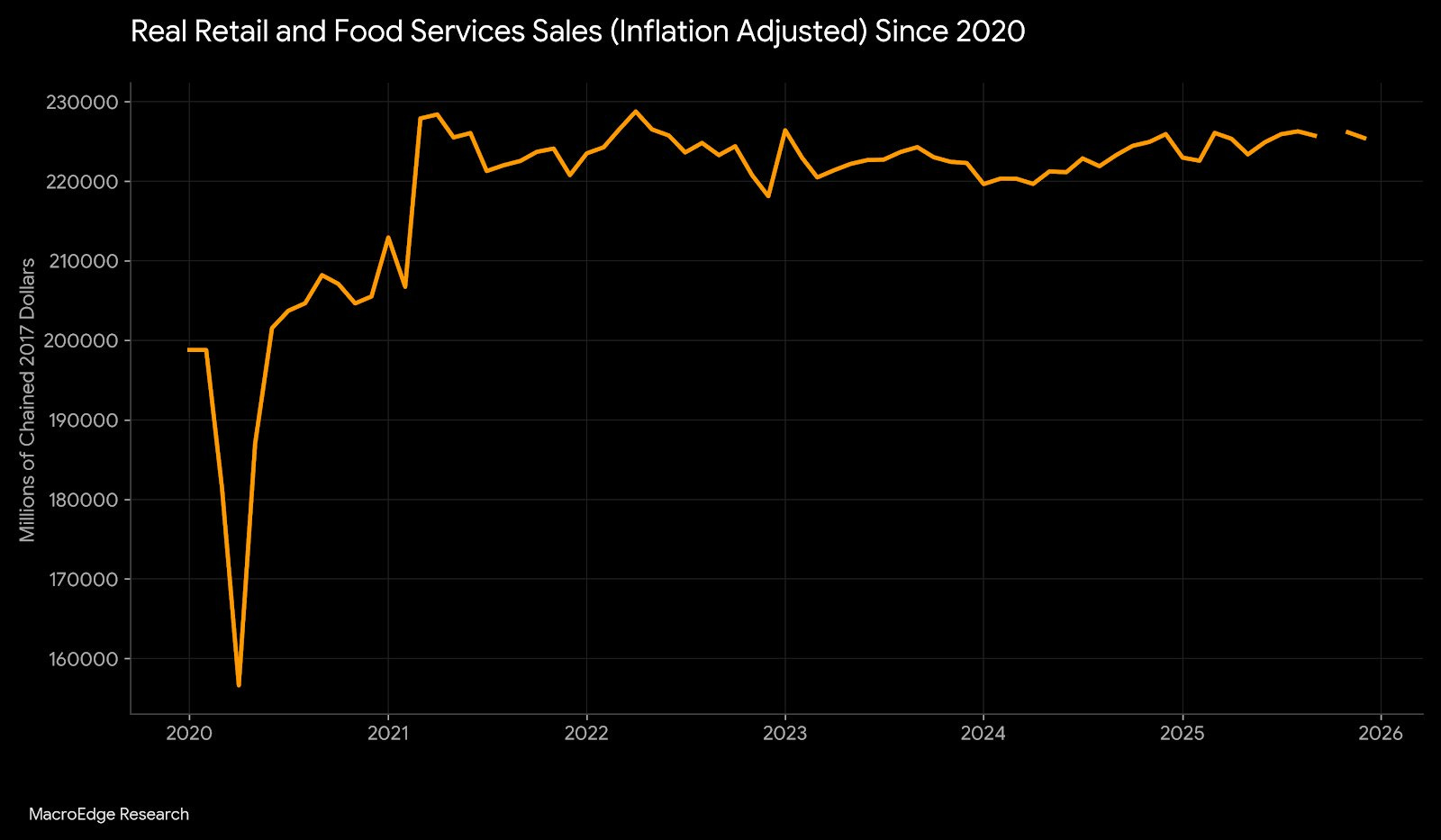

The Administration is going to want soft labor prints now through the remainder of the Powell term if they want further rate cuts, and the Fed is in a standby mode until the data continues to cool. While there’s been little reason for rate cuts based on past months data, we’ve also seen retail sales (especially on a real - inflation adjusted basis) go nowhere. Simply put, all of the nominal growth we’ve seen has been a result of inflation of the past several years. The pandemic-era money printing did a lot to distort the nominal figure, which is why the real retail sales figure gives us the best look:

Remember: politicians and policymakers absolutely love nominal figures… because ‘number go up’. This is a pretty clear indicator of the ‘i-shaped’ economy we’ve been discussing for the better part of the last 1.5 years now.

Below, we’re going to dive into the January data released so far, talk about our January employment projections, highlight the strong dollar charade that we’re seeing with the Administration, and lay the groundwork for the Friday Macro Note - where we’re going to cover a whole lot more - including a portfolio commentary update.

Arriving soon - we have our own hiring momentum data, which will be another useful tool for those of you seeking accurate employment data in a time of great obscurity. This data, while not a substitute for ADP Payrolls & Revelio data, will provide more useful color into public hiring announcements, hiring trends, and more - stay tuned for updates as we prepare to roll out additional data throughout the 2026 year.

Not yet a MacroEdge Ozone subscriber? We’ve migrated the entire Ozone ecosystem to Substack - from community, to reports, research, our data, and much more - it’s all here. Join us on our Macro Research mission of being a top 10 Substack account in the finance space. As the only in-house macro data developer on Substack, we’re leading the way in more ways than one as we continue to pioneer new macro-driven solutions.

January Data is Bleak (So Far)

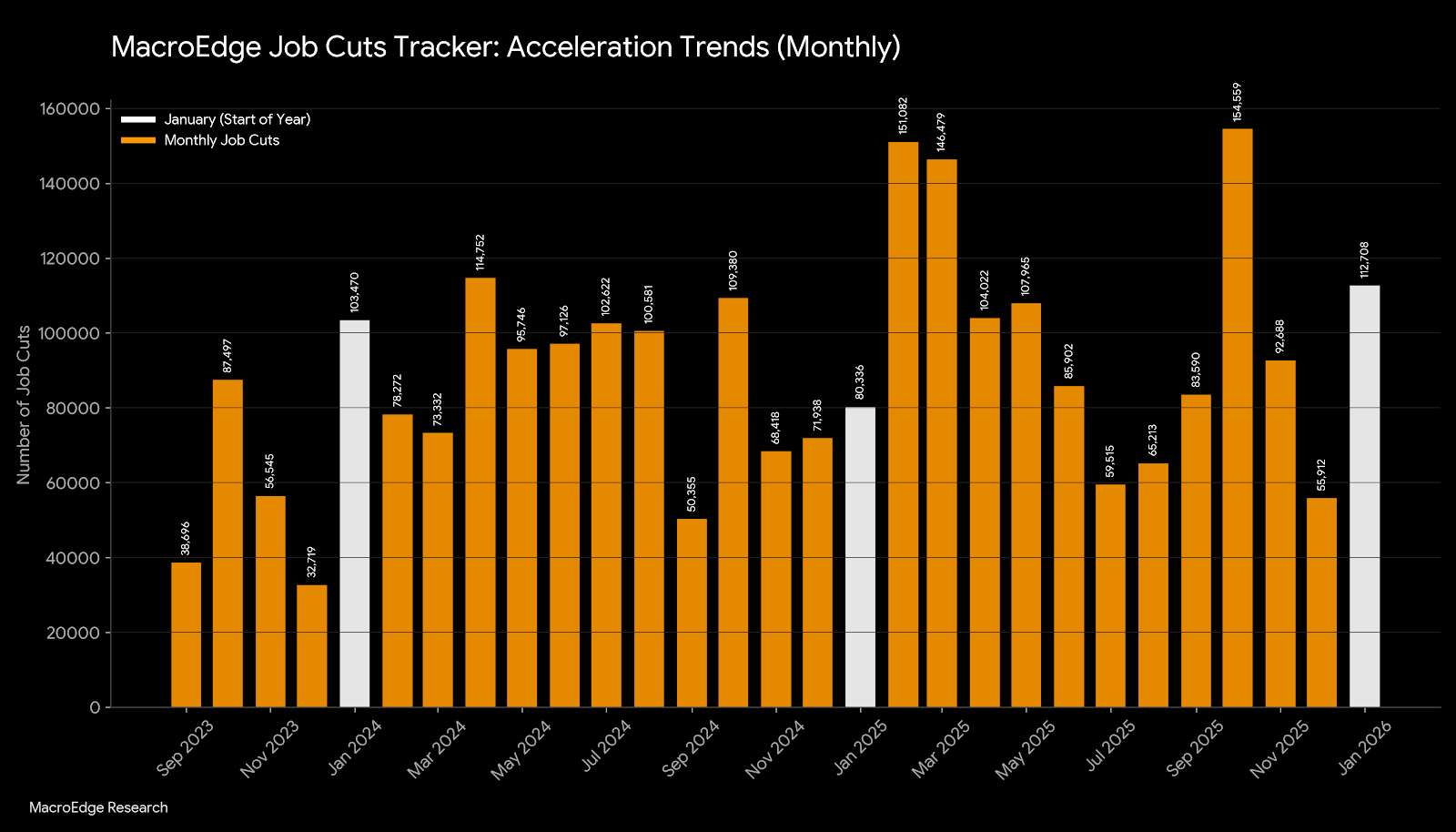

MacroEdge Job Cuts Tracker - highest January since we began tracking the data series

Our outlook is for a similar number of job cuts this year as last, and this pace gives momentum to the figure for the year. This month is trending elevated as well, and the spring/fall usually see the highest job cut months as companies assess their first quarter performance. While we won’t have the same # of DOGE cuts as we saw in 2025, hiring remains very soft, which signals the potential for further layoffs into the year.

Challenger Job Cuts -

Challenger job cuts for January were their highest level for January since 2009, while hiring for January fell to its slowest pace on record

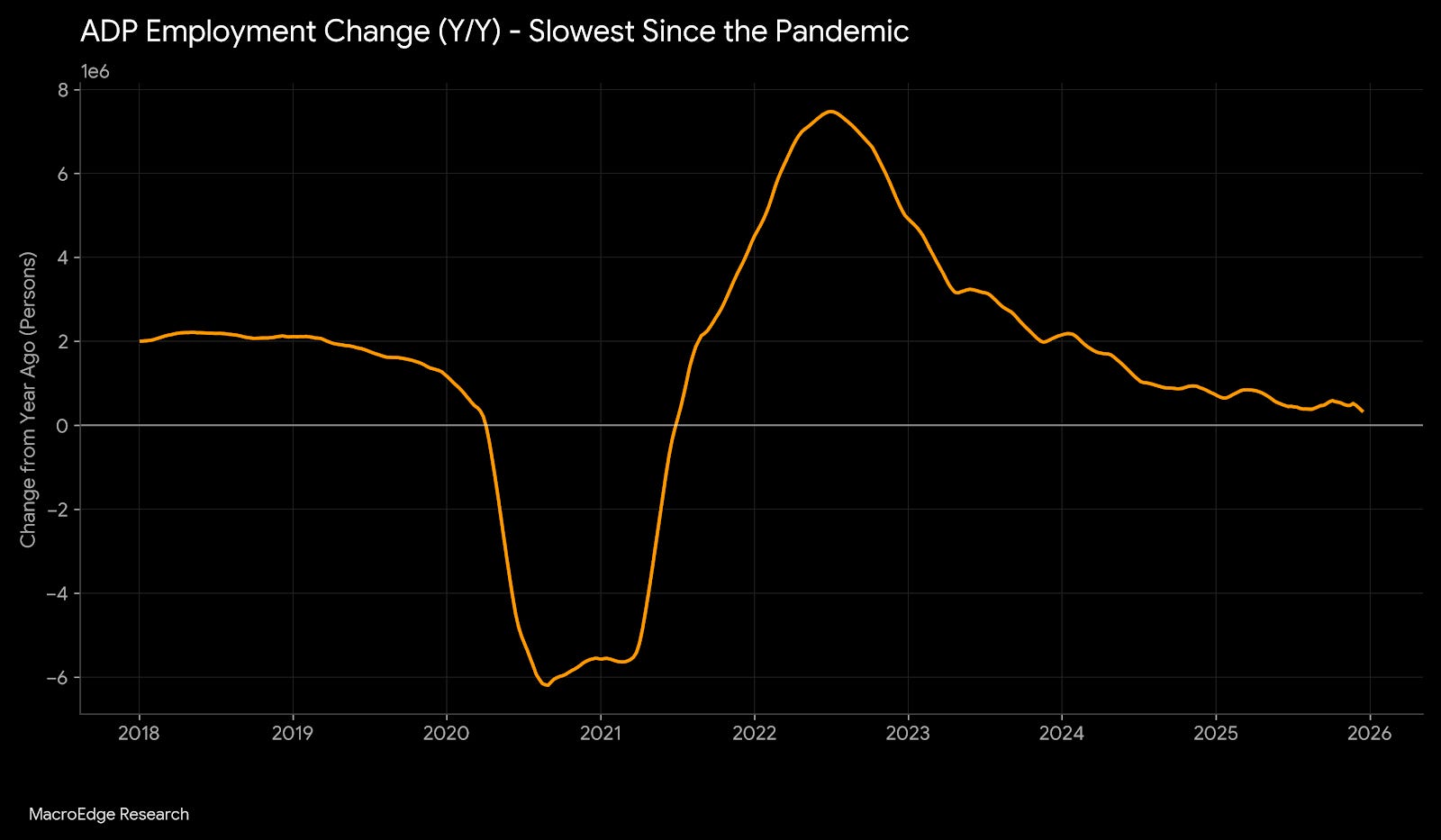

ADP Employment Change - slowest growth since the pandemic

Almost all labor market signals continue to point in a single direction → weakening

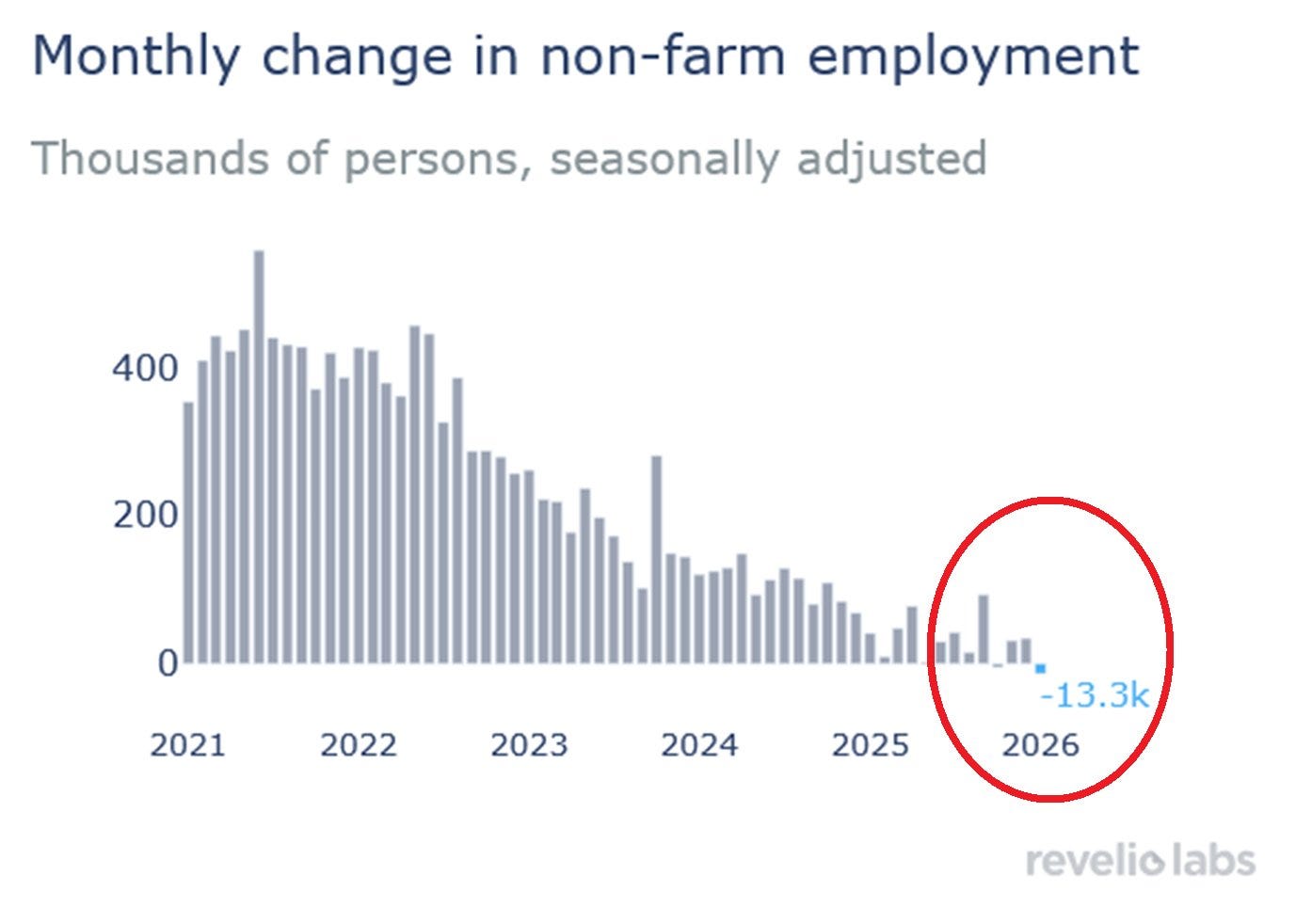

Revelio Labs Payrolls (Private)

Showing a significant decline in the data series, with a net loss of 13.3K jobs

Bloomberg Economics is forecasting a print of 0 for the month, with huge revisions to the 2025 payrolls data.

Indeed Live Job Postings - continuing a softening trend after a brief seasonal bounce

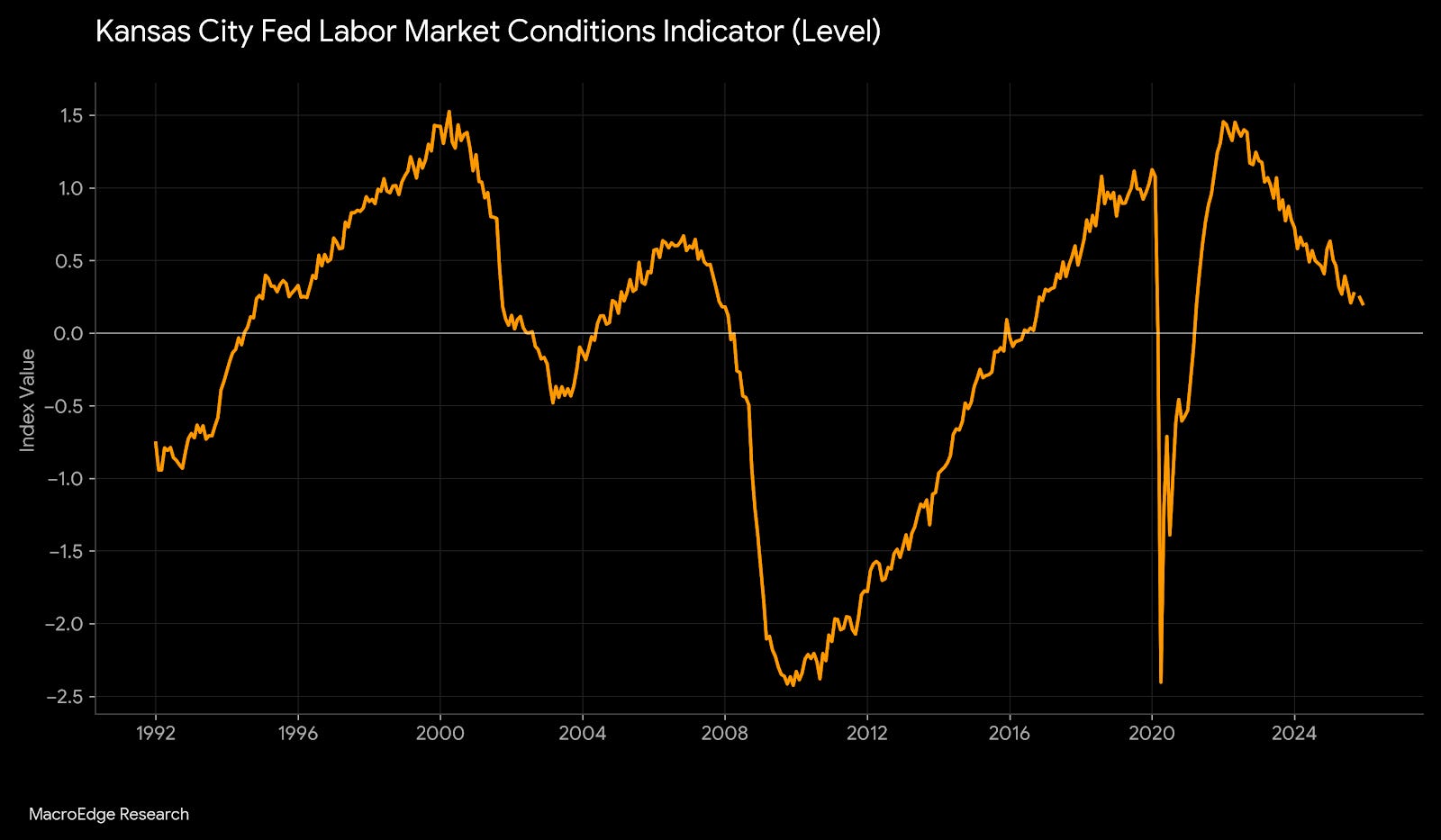

KC Fed Labor Market Conditions Index - heading to a new cycle low tomorrow

JOLTS Survey - Hiring Rate v Job Openings

Our January Employment Projection

(continued below → our January employment projection & expected market reaction, strong dollar ‘charade’, Friday Macro Note preview, & more)

Try Ozone, now exclusively through Substack for 7-days at:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.