Midweek Macro Note: Huang's World Slows Its Spin, Drilling Deeper, Portfolio Strategy Update, Liquidity Impulse Signals, & More

In the Midweek Macro Note - we discuss Jensen Huang's problems as Nvidia fails to push higher, highlight energy sector opportunities with a potential geopolitical event, discuss liquidity, and more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

This evening I am joining you all from Midland, TX - in the heart of the Permian Basin… It’s been a productive work trip thus far as we continue to expand our industry capabilities under our Macro Research & Transform umbrellas - and I am making it a core priority for us this year to continue expanding our transformative solutions to oil and gas operators. I’ve had several media interviews over the past week to discuss the latest on AI, market concentration risks, data centers, and much more - and if you follow me on X (which many of you do) you will see me sharing some of those articles and quotes there. Without our fantastic community sharing what we do, I wouldn’t have the opportunity to share our data, so I appreciate all of you who go above and beyond to share our data, reports, and much more.

We’re in a very weird era of market dynamics, with 24/7 retail obsession and clickbait being pervasive beyond anything that I’ve seen in modern market history. While the parallels to the Dotcom cycle continue to pile up, timing this cycle has been incredibly difficult due to pandemic-era money printing that has created complex economic distortions and delayed traditional lag effects of Fed policy. The mini-macro cycles that we’ve seen time and time again over the last 24 or so months have continued to evolve, revolve, reset, and then do it all over again - and it’s important, given these dynamics, not to jump to any conclusions until the entire picture becomes clearer.

Tonight, we’re going to dive into some of the Nvidia dynamics, as Jensen has faced increasing troubles propelling his stock higher. Nvidia has spent tens of billions financing purchases of chips, and the circular financing spiral continues to worsen. In my opinion, without a profit moat at many of these LLMs, we’re going to see some sort of bailout of some magnitude as the industry problems mount. Because of the size of the bubble that’s been created - and the weighting it now holds in numbers like our GDP growth (ie, data centers) - politicians are going to be very cautious to let it deteriorate. The broad distributive patterns in tech (particularly in the Nasdaq) and individual names like Nvidia further highlight continued concentration risk - and I expect to see the semiconductor index and data center index come under further pressure as scrutiny increases over the course of 2026.

Next Reports in our Sequence

Portfolio Strategy Note & Trident Note (Friday evening)

Data Center & AI Update - February Data Releases / AI Bubble Update with guest article from The Coastal Journal (Saturday morning)

Weekly Macro Note (Sunday evening)

Transform(ing) into 2026

This year, we’re focusing on expanding our Macro Research & Transform capabilities across four key sectors. We’re building upon transformative solutions that we’ve implemented across enterprises in these sectors, and 2026 will be a year of great growth for us across the United States.

Learn more about our Transform solutions:

Huang’s World Slows Its Spin (Further)

Nvidia’s fiscal Q4 2026 earnings report, delivered on February 25, 2026, was a masterclass in “beating and raising” that nevertheless left the market with a sense of “valuation exhaustion.” The company reported record revenue of $68.1 billion (up 73% year-over-year) and earnings per share of $1.62, both comfortably ahead of Wall Street’s lofty expectations. The Data Center segment remained the undisputed engine of growth, raking in $62.3 billion as the Blackwell architecture ramped up at a pace Jensen Huang described as the arrival of the “agentic AI inflection point.” Despite a robust Q1 revenue guide of $78 billion, the stock’s reaction was uncharacteristically muted… after an initial 4% pop in after-hours trading, shares settled into a tepid gain, signaling that investors are now demanding more than just “standard” blowout numbers to sustain a breakout.

(continued below: Huang’s World Slows Its Spin, Drilling Deeper - Energy Equity Opportunities, Liquidity Impulse Signals, Labor Market Review, MacroEdge Portfolio Strategy Update, & More)…

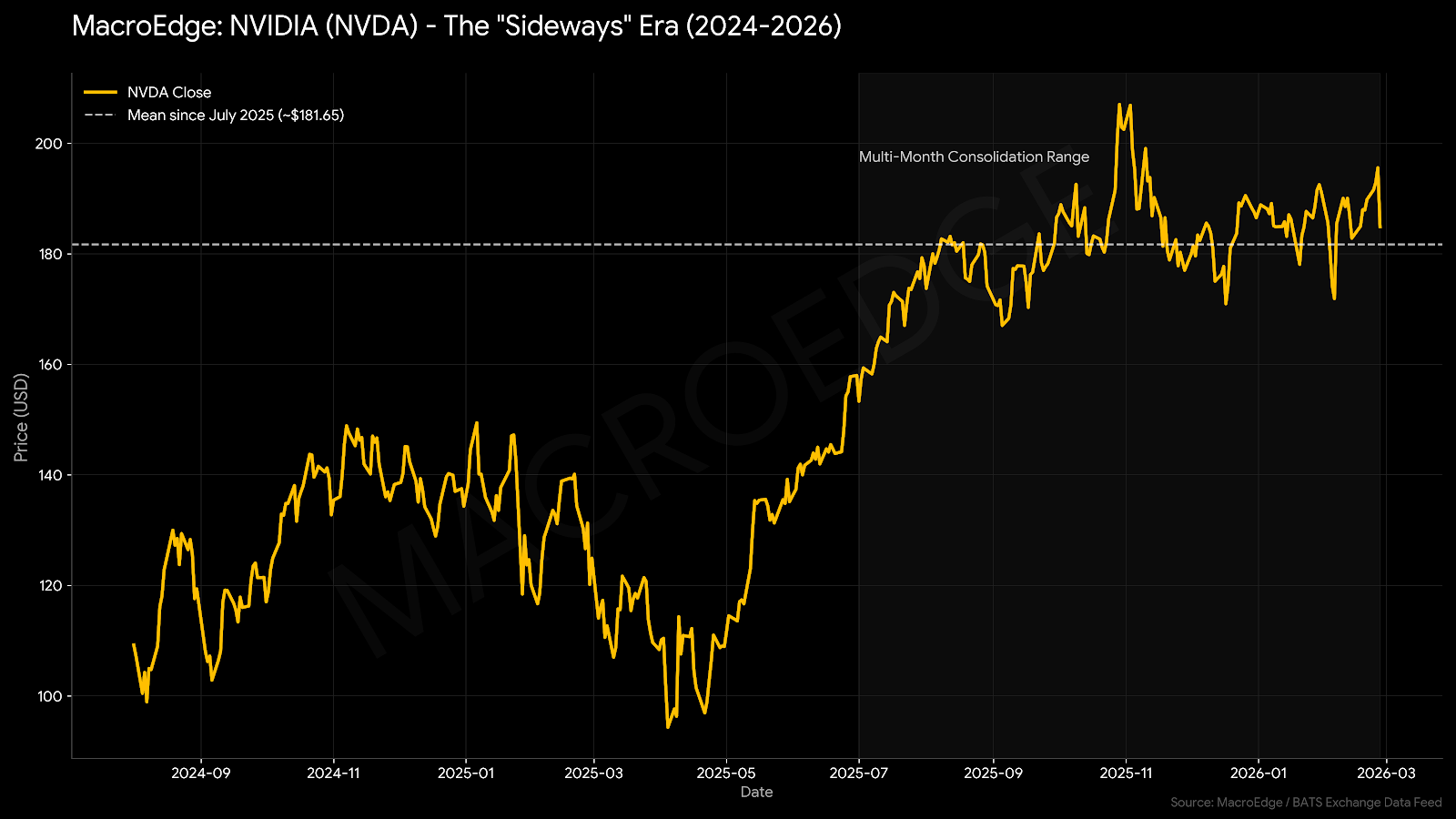

Behind the record-breaking numbers, a thicket of structural risks is beginning to weigh on the “AI and hardware” narrative. The outlook for data centers is increasingly wobbly due to physical constraints that even Nvidia’s software can’t solve: a mounting energy crisis where power availability has replaced chip supply as the primary bottleneck. Furthermore, nearly 50% of revenue still originates from a handful of hyperscalers (Microsoft, Meta, etc.), leading to growing “circularity” concerns. Investors are questioning the ROI for these customers as their capital expenditures (CapEx) balloon toward a collective $700 billion. This fundamental tension is reflected in the technicals: Nvidia has been essentially sideways since July 2025, churning in a volatile range between $170 and $210. This eight-month consolidation suggests the market is no longer pricing in just “potential,” but is waiting for proof that the massive infrastructure spend will translate into sustainable corporate profits beyond the semiconductor sector… which I continue to believe is unlikely.

The November pop for Nvidia looks to be a major high for the time being, and with the data center index making a major lower high, that adds further headwinds to the sector.

Drilling Deeper

Expanding on our energy commentary from a few nights ago - I continue to closely watch developments in the oil & gas markets. While a lot of names have ripped higher in the last six-months, WTI has held the key $54bbl level for the better part of the last year. The technical pattern below is very constructive for a move higher, though they next key level is holding above the $70 WTI standpoint. If the backdrop gets more constructive for WTI and industry conditions improve, I am looking at a basket of five various E&P names to capture the upside (we discussed many of them a few days ago)...

There are plenty of catalysts for why prices could start to move higher here, and we can also acknowledge that the Administration in a midterm year is going to fight as hard as they possibly can to keep a lid on WTI right around this level, especially as inflation base effects wear off. The 10Y has dropped, move oppositely of oil for the time being, and is set to tick below 4% again:

Whether or not this moves lower is a factor of the inflation data tomorrow, as well as the employment data that will be released in the next several weeks. Given past market dynamics, I don’t think we should look at oil:10Y as a one-to-one relationship.

Liquidity Impulse Signals

Bitcoin is our best real-time liquidity proxy, and has stayed in this $60-$70K range for the last several days:

(Brief) Labor Market Review

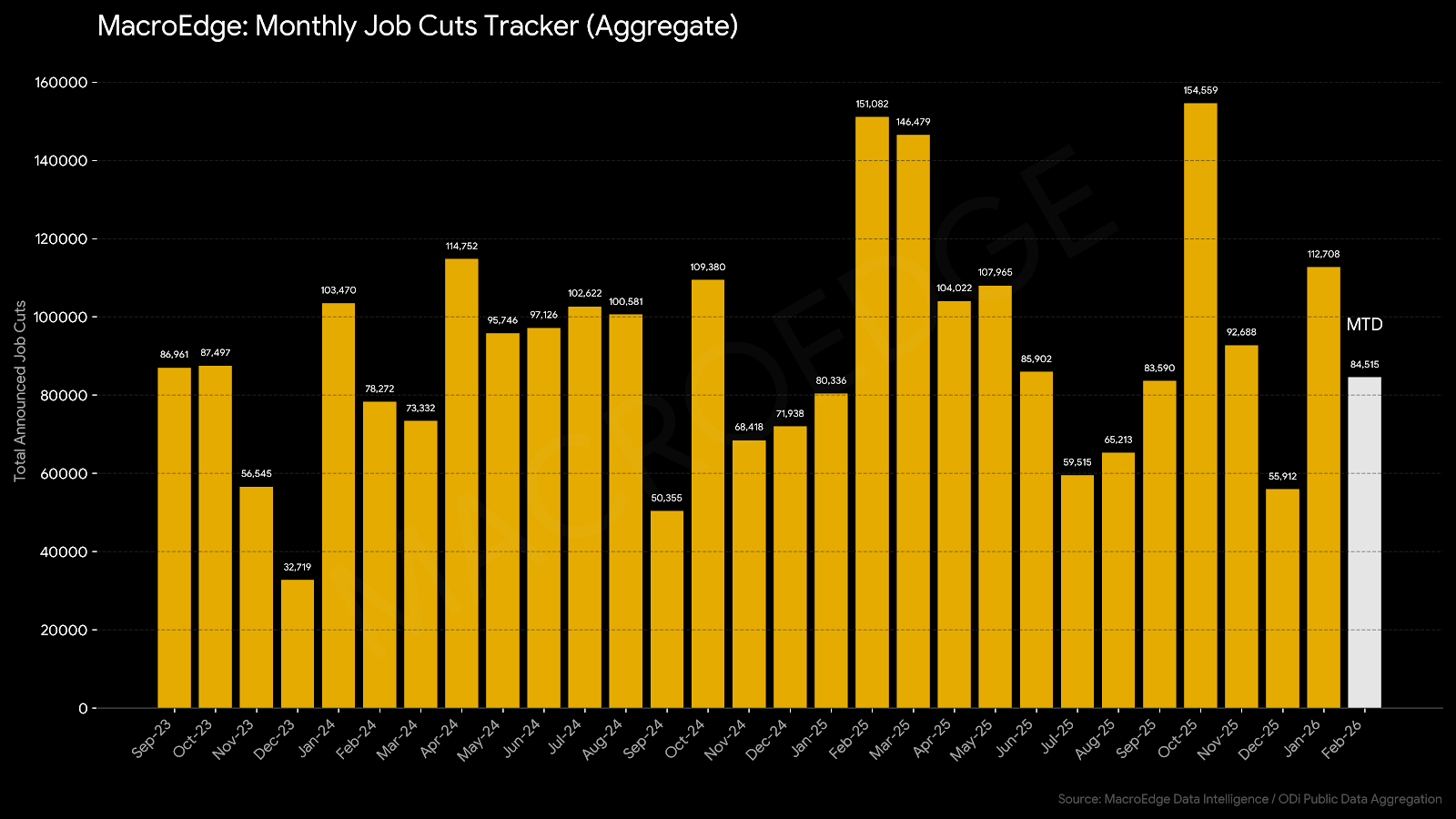

The labor market is sitting in a holding pattern through the month of February, with job cuts elevated and job postings still a bit off of their cycle lows. We’ll likely see the December and January improvement hit JOLTS come March or April, and I expect that the moves will be exaggerated to the upside, given issues with JOLTS of late from a data quality standpoint.

For job cuts (measured by us) → we’re above 84,000 on the month and will likely end this short month about 90K. The Block layoff today was sizable, and there have been other sizable cuts for the month.

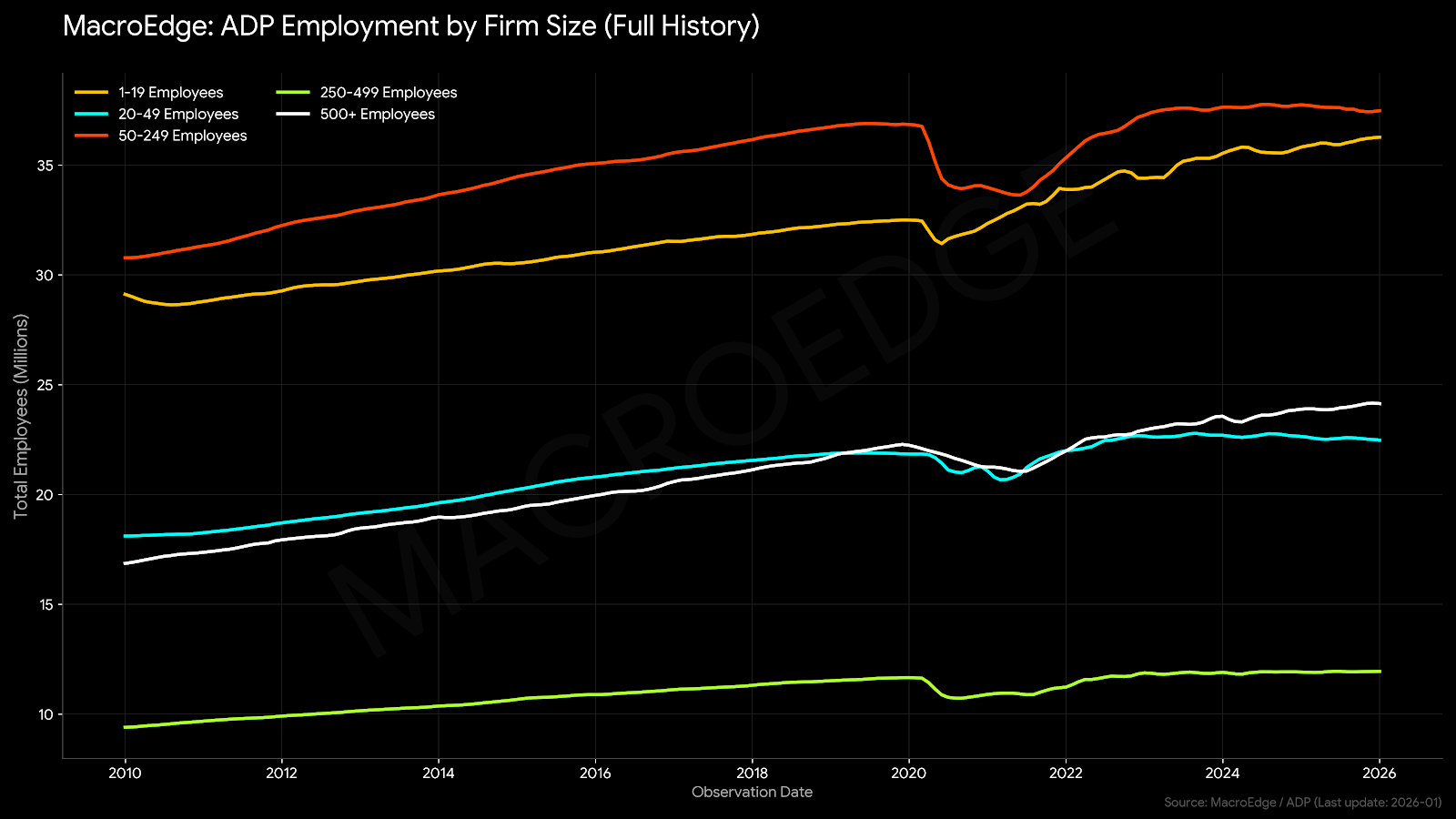

ADP weekly job data has improved a bit, with the monthly run rate (4WK MA) back at about 40K. Small business employment continues to lag, which is part of the ‘i-shaped’ economic dynamic we’ve seen over the past 18 months. All employment growth is currently coming from the smallest firms (1-19) segment, ie, self-employed individuals, and what I expect is likely AI firms and other small technology firms. On top of that, the 500+ category continues to expand, since they are able to shoulder the higher burden of high healthcare and labor costs, as well as take advantage of things like visa-based employment.

MacroEdge Portfolio Strategy Update - February 26, 2026 (@SixFinance, Head of Research)

Software has been absolutely decimated. No question about it. Hardware stocks are rallying. The memory players are melting straight up. The positioning on both sides is highly aggressive. As I write this after market close on 2/26, XYZ has announced that it will lay off 40% of its staff to lean into AI. Software doesn’t like the headline. While the market is focusing on software disruption, it is ignoring the elephant in the room: who in their right mind is going to eliminate their core, AI-enhanced operating systems of record as they are laying off large swaths of their workforce, a much larger part of the corporate budget?

Additionally, software companies spend more than double the SPX average on labor as a percentage of revenue, with many software companies spending over 50% of revenue on labor, benefits, and stock-based compensation. Every software CEO is watching the market reaction to XYZ layoffs today.

Regardless, positioning is highly stretched. If you can wrap your head around Jensen Huang’s statements about AI being a tailwind for enterprise software instead of a headwind, along with extrapolating forward the consequences of the market heavily rewarding a large software/fintech company for reducing headcount, you have the ingredients for a monster sector rally.

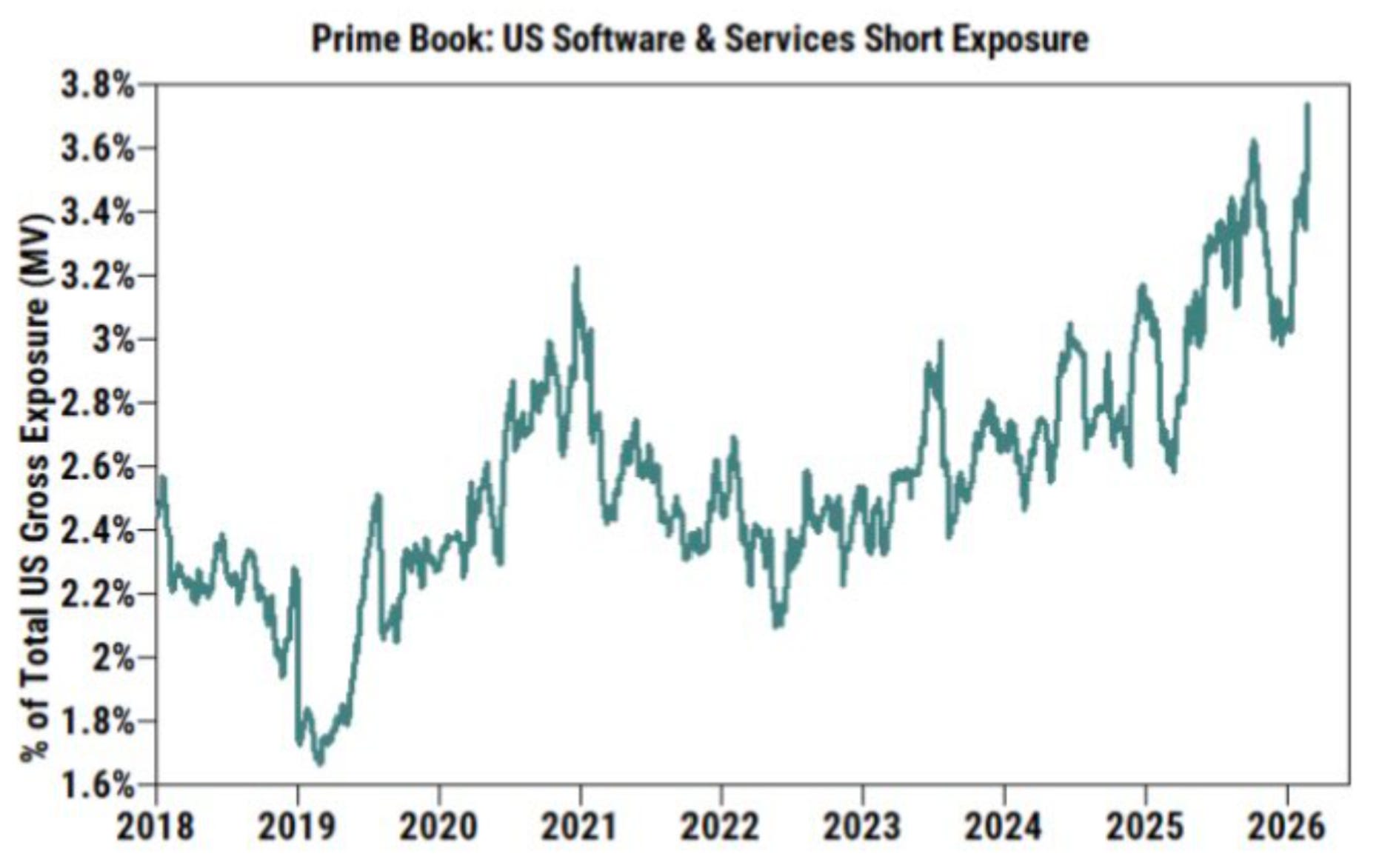

(Goldman Sachs Prime Book)

Hedge funds are as short as they have ever been on software. While hedge funds are aggressive sellers in the hole, retail (who have been largely correct since COVID, in bull markets anyway) has been aggressively buying in the hole.

Software volume is exploding higher. Using IGV software ETF as a proxy, we can see enormous capitulation-style selling price action the last couple of weeks, with enormous up volume this week, as the dip is bought. This is exactly the type of action you see at climatic reversals.

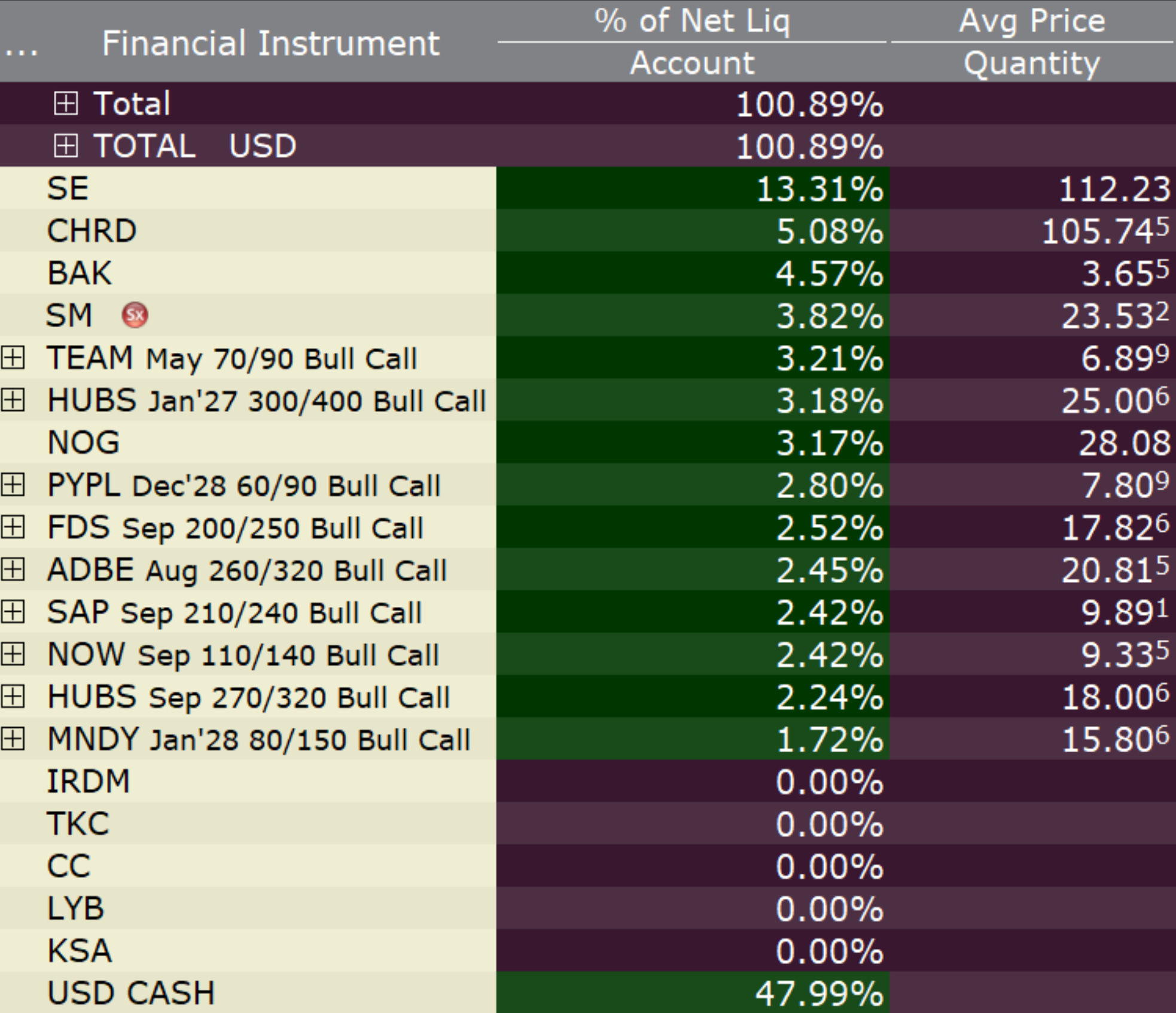

Now there are several ways to capture value from this trend. I was in the market buying call spreads on Tuesday in TEAM and FDS before piling in much deeper today. I want large exposure to the theme, and I want to be leveraged to a substantial relief rally if I’m right. I will also be quick to cut my losses if I am wrong.

Here are the portfolio changes made thus far:

Going beyond short-term tactical trades… can we actually own this sector in the future? The answer is yes… with nuance.

The key beneficiaries within the software sector are going to be the data pools, benefitting from API utilization, while the user interfaces will be increasingly at risk. Companies that have wide data moats and are deeply integrated into business operating systems like NOW, SAP, FDS will be the winners in the long run and likely benefit from increased, not decreased, utilization. If Bloomberg were publicly traded, it would almost certainly be in a large drawdown, and I would be buying it with both hands, but Factset is a worthy alternative.

Note* Businesses massively overhired during the COVID era. “AI” is now giving them ample rope to right-size their businesses. If a large chain of layoffs begins to materialize, there is not much that will be of interest in being long besides bonds and their derivatives.

For more details, please refer to our Terms and Conditions.