Midweek Macro Note: Fed Liquidity Cannon is On, Energy Discussion & Strategy Update, Portfolio Strategy Update

In this Midweek Macro note - we cover the latest on the Fed liquidity cannon (which has begun firing once again), highlight the latest developments in oil and gas + market interventions, & more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

It’s been an interesting week thus far as the equity melt-up persisted through the close. Tomorrow could mark the longest winning streak for the Nasdaq in history (yes - lots of those ‘once in a lifetime every day’ recently). The market intervention is back on banshee mode and leading inflationary signals are starting to rear their head, which would be very ugly for the lower ‘i’ in the ‘i-shaped’ economy… As I say daily, we’re on a very bizarre pathway as a country - especially from a monetary policy standpoint - and are taking on different elements of South Africa, Venezuela, and Argentina in terms of different elements that I am seeing strung together into one piece. Wealth inequality will take another leg up and that may set up our next *monetary reset* which seems inevitable at this point if we faced anything like the 2021-2022 wave of inflation.

It’s been unbelievable to watch the collective delusion around the Strait of Hormuz closure and the impacts the situation is already having on the world economy. This is a pandemic-sized shock in terms of impact, with oil demand needing to go the same way that we saw from the pandemic to eventually get prices restored. With physical barrels hitting as high as $268/bbl in countries like Sri Lanka - and jet fuel pushing $198/bbl global average - these are at all-time high levels… but the question I am getting asked frequently in both calls and on X is whether or not this will reflect into the futures market, I undoubtedly think it will, barring any immediate economic shock. By pumping equity markets back to the highs, and with the Fed unleashing balance sheet expansion now as commodities rip, that will not sour demand in developing nations, and thus prices will have to go higher toward demand destruction levels in order for the market to find equilibrium. Here’s Urea prices as one example of this mounting commodity shock that is still one of the most obvious, given the fact that the Strait of Hormuz remains effectively closed, and the 13mpbd of oil supply remains offline from the market:

As onshore inventories of crude stock in the US begin to draw down, I expect that is when we start to see the first ‘reality check’ signals and traders begin to take bigger risks. Right now, in this ceasefire on/off headline whiplash environment, large traders have stayed sidelined for risk of getting squeezed out by these interventions - though today marked the first time in about 2 weeks that we saw the market dampen the impact of the headlines and announcements.

I say this with a great sense of concern and urgency in that if the Strait of Hormuz is not reopen within the next 30 days, (and/if) things escalate further to something like a closure of the Bab-al-Mandab Strait - Global South economies are going to get hit by an economic and inflationary tsunami, and American consumers that aren’t seeking out safe havens in things like assets are going to be in for a very rude awakening. The reality is the reality, and right now, the reality of the Strait being closed this long is absolutely shocking… You cannot mess with the energy and food supply to this degree without grand consequences, regardless of flooding the system with additional liquidity to pump equities higher. With how controlled the futures market has been in crude, I expect that when they ‘let off the gas’ for interventions, it all might just happen quicker than we all expect.

With that being said, maybe it’s time I secure a flight to a secure island destination for the time being…

Not yet a MacroEdge Ozone subscriber? Get all of our research, data, reports, and much more below.

‘On the Ground’ Series Begins on Saturday

Our new ‘On the Ground’ report series begins on Saturday. We are kicking off the first of the series with a background and introduction into our first target in a first of a four-part series under the ‘On the Ground’ reports - being the ag sector. As we continue to monitor and adjust positioning given the latest inflation impulses, it appears that we are once again on the verge of a move higher in inflation. Yes - commodities have rallied a lot thus far (just look at copper and oil) as one example - but there are plenty that still haven’t participated (ie: natural gas) and others that are critical to our food and input cost chain that we will be discussing in the first part of this series.

The real question we want to ask is: is it as bad as some of the stories say right now, and if so, how will it impact both inflation and the broader economy in the months to come? If not, is there still an opportunity to capitalize on, or should we focus on better, more opportune baskets that exist (like energy equities at $95/bbl).

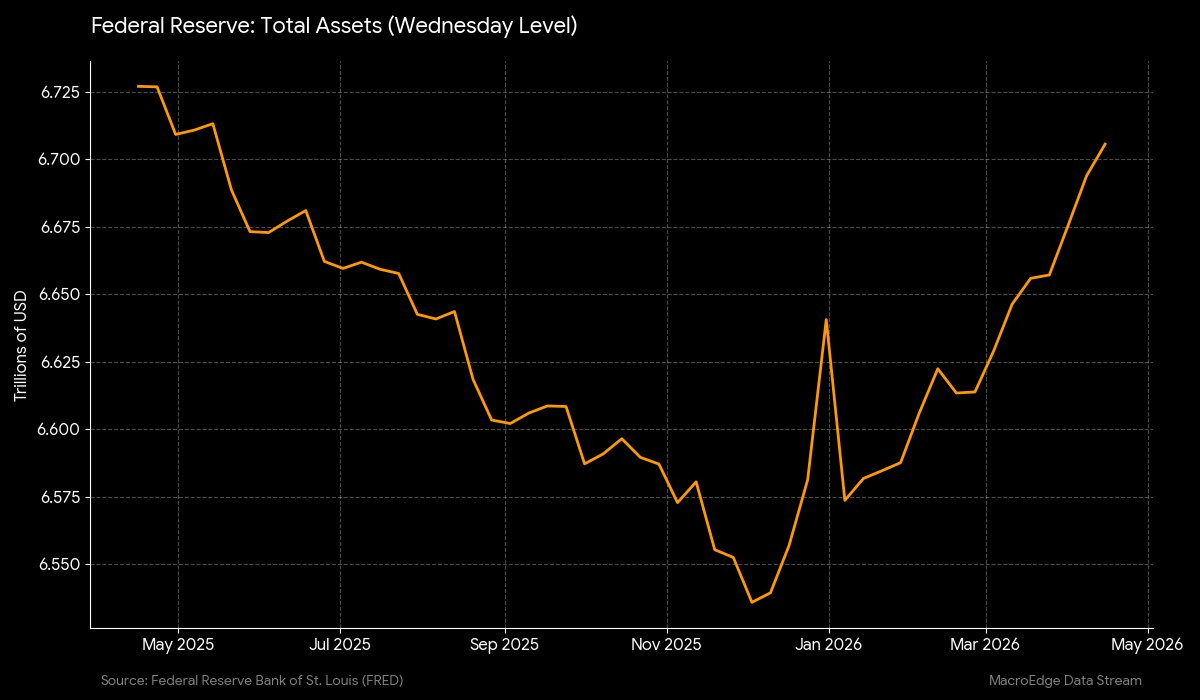

Fed Liquidity Cannon: Activated

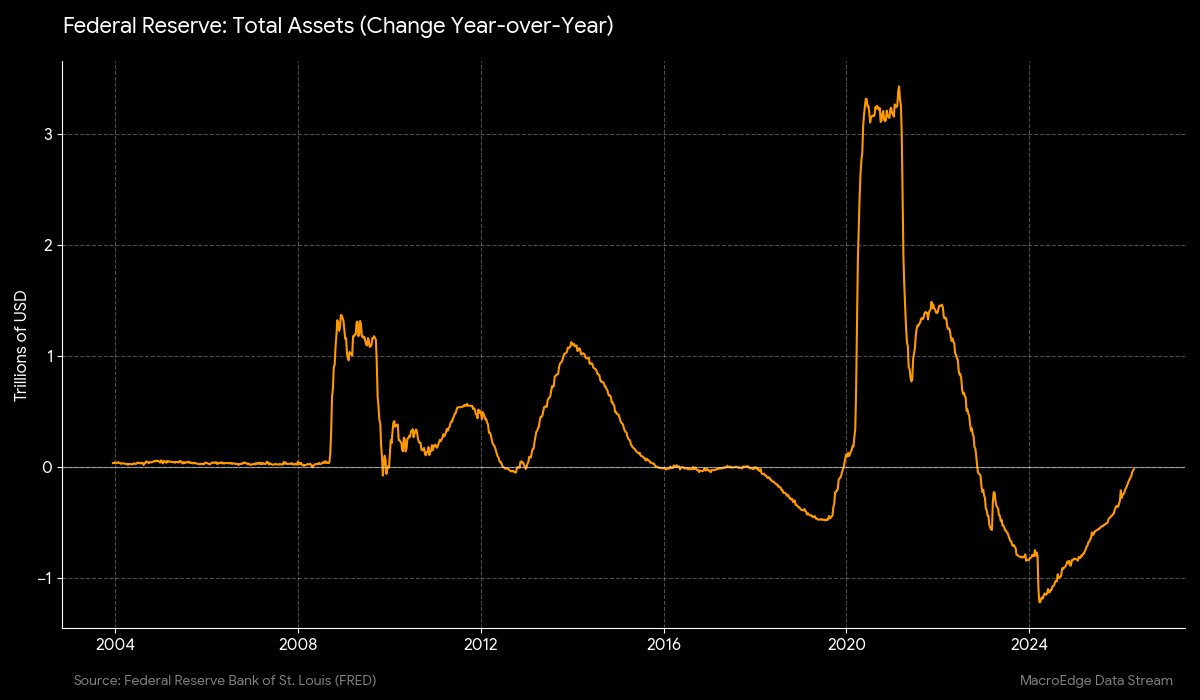

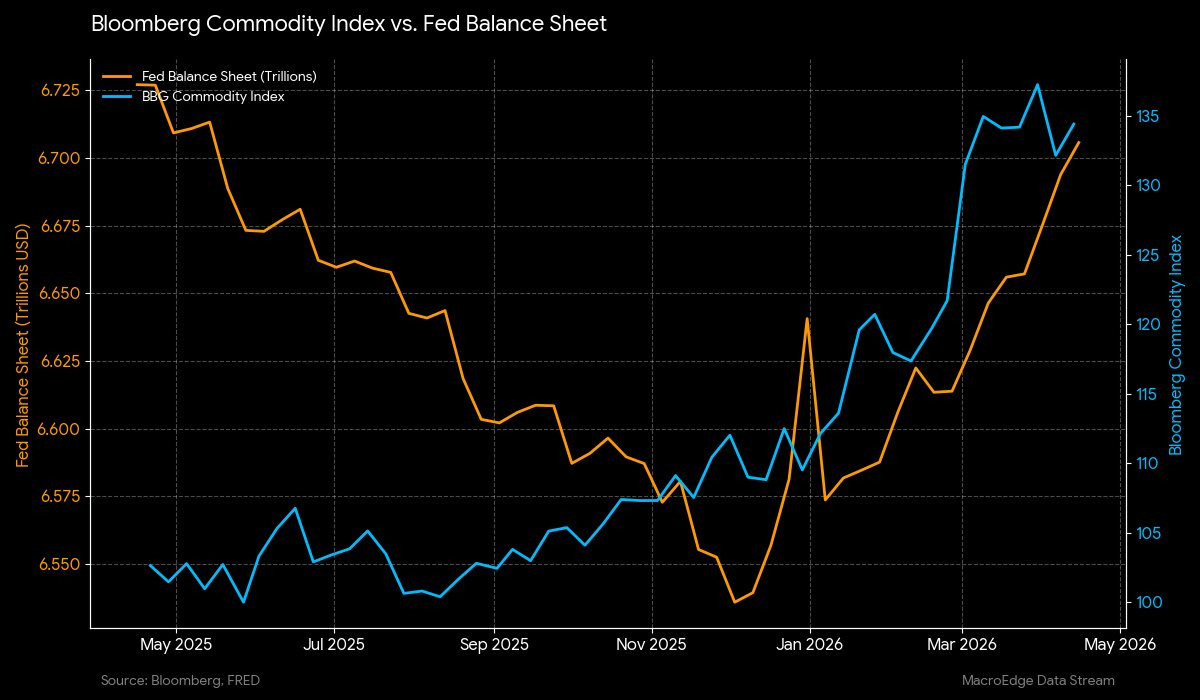

Fed balance sheet expansion is well underway and has accelerated rapidly in recent days. The status quo would tell us that the balance sheet is going to go considerably higher from here - and that looks to be the case if we continue to step on the inflation gas into this economy that will be unable to absorb another across-the-board increase in price levels, especially in the lower ‘i’ - 90%.

The impact of this is clear on commodities and equities, and the CPI relationship is relevant as well.

Fed balance sheet since last April, almost positive on the y/y readings now:

On the y/y view:

Fed balance sheet versus Bloomberg Commodity Index:

Continued below: Energy Discussion & Strategy Update, Preview of the Redeye & Weekend Reports, Lockout Rally v Reality from Six, and Wash - Winse - Repeat from John Galt

Not yet a MacroEdge Ozone subscriber? Upgrade below:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.