Midweek Macro Note: Countdown to an Energy Crisis, FOMC Recap, Portfolio Strategy Update, Equity Research Notes

In this Midweek Macro Note - we discuss the latest developments out of the Middle East as they pertain to the energy situation, highlight the key takeaways from the FOMC meeting, & much more.

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge Readers and Community,

A macro-driven landscape continues across global markets - and particularly in the United States, as Israel and Iran stepped up energy infrastructure attacks over the past 24 hours. We remain in a very dynamic landscape with about a fifth of global oil supplies remaining offline, and natural gas impacts becoming more notable in the last 24 hours after the impacts at South Pars. It appears that the US Administration has been unable to contain Israeli attacks on energy infrastructure to this point, though the backlash over the bombing of Pars was the most significant that we’ve seen voiced from the President directly. As we teeter towards a more serious energy situation globally (especially as it pertains to oil on the water) and natural gas supplies to countries like Japan, Korea, & other net importers like India, the shot clock for resolution becomes more significant. If we don’t see moves towards resolution by the end of the week, just as highlighted, chances for ‘off-ramping’ two weeks prior declining to near-zero for the immediate future if strikes continued, it’s likely that the risk for global energy markets continues to move up our right tail chain as highlighted earlier in the month. With the Pentagon requesting another $200 billion to continue the conflict, it does not appear that this ‘short-term’ military operation is going to be all that short. NATO & global allies of the United States have also taken a sharply different approach than previous Middle East conflicts, choosing to distance themselves from offensive strikes on Iran and focusing solely on defensive posturing. This departure likely has Administration officials spooked, as the US will have to expand into a broader ‘boots on the ground’ approach to do things like secure the Strait of Hormuz, which could take weeks or months to execute.

Another risk materializing from a strike standpoint - which was highlighted by our fantastic host John Galt on MacroEdge Radio #70 last night - is Houthi involvement in the Red Sea, something that we haven’t yet seen. If you haven’t yet listened to MacroEdge Radio #70 - you can find it here:

On the FOMC front - the Fed left rates unchanged as expected - and the Bank of Japan followed suit moments ago. The Reserve Bank of Australia opted for a rate hike this week, which we flagged as a possibility earlier in the year as Australian yields continued to surge higher. Adding in an energy price surge to the mix amidst a very hot PPI print makes the situation even more difficult for the Fed which once again finds themselves in decision paralysis from a combination of various macro forces all pushing and pulling concurrently.

Not yet a MacroEdge Ozone subscriber? Upgrade today below:

Trident - Our Forward-Thinking Macro Vehicle*

Building on the cutting-edge macro research, equity research, and portfolio strategy we deliver at MacroEdge, we are opening the doors to register interest in the Trident I Global Macro Fund. This boutique vehicle is engineered to capture high absolute returns by identifying structural inflection points across global FX, rates, commodities, and equities. Modeled after unconstrained mandates, the Fund moves beyond traditional benchmarks to capitalize on mispriced macro fundamentals through a disciplined, thematic process. For accredited partners looking to move from analysis to execution, Trident offers a focused path into high-conviction global themes with a rigorous emphasis on downside control and liquidity.

Complete the form below to get in touch with our team & learn more about how we’re turning real-time data into real-time strategy:

Countdown to an Energy Crisis

We’re shifting into a countdown to an energy crisis as the war between Israel and Iran drags on. The reality is that with a fifth of global oil supply frozen/offline and the risk to natural gas supplies becoming more pronounced, the shorter the window the world has to prepare for a real energy price shock that makes the last 30 days look tame. While $95-$100 WTI is manageable from an economic standpoint in the US - especially with the US being a net exporter of oil - above $120/bbl things start to look quite a bit different. We’re already seeing the impacts hit around the globe with mass airline flight cancellations, concerns around things like fertilizer prices grow, and consumers seeing the significant jump at the pump, but all of this has just been a warm-up act if they don’t figure out how to resolve the Strait closure & supply shut-ins in the next 14-21 days.

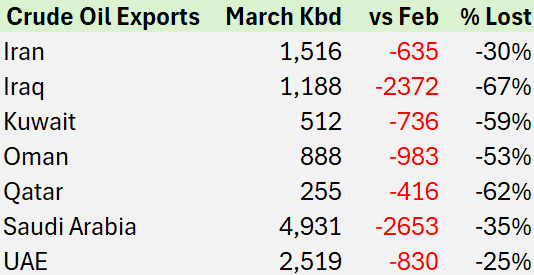

Current oil outages by country…

(source: @OilCFD on X)

Brent/WTI spread started to blow out again today as Brent ~$110/bbl. It’s likely that we’re seeing direct US involvement in the futures market to suppress WTI oil futures.

There is additional speculation that this may be another signal that the political Administration in the US may be closer to pushing for an export ban, which would be a disastrous decision.

(continued below: countdown to an energy crisis, additional oil and natural gas data, portfolio strategy update - energy focus, equity research notes, Portfolio Strategy Update & Commentary - Six, Head of Research)

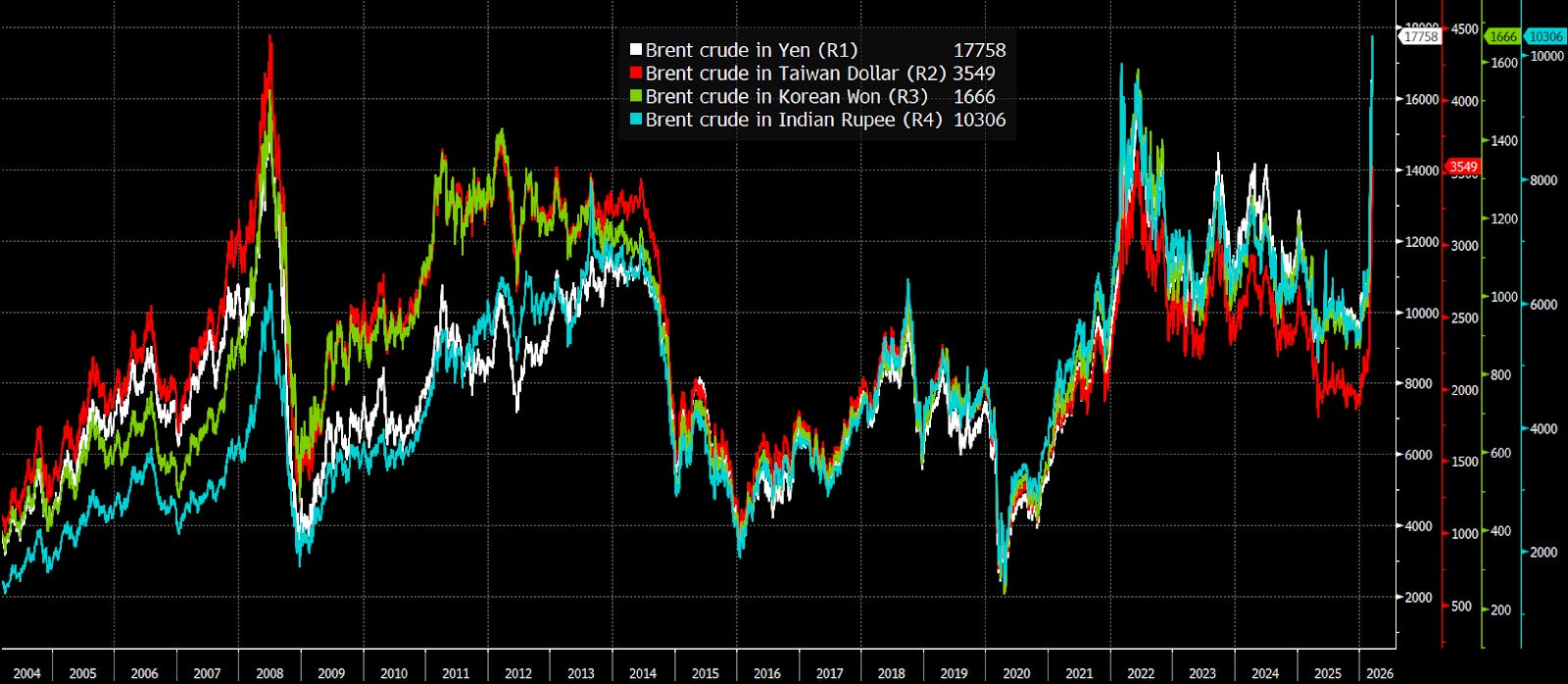

Brent pricing in foreign currencies:

Source: PauloMacro

The highest on record, with the exception of 2008, which quickly shut down global economic activity.

The current ~19 mb/d impairment represents a global supply shock of unprecedented scale, exceeding the 1973 Oil Embargo and the 1979 Iranian Revolution combined. If this crisis extends beyond the next 14–21 days, the structural integrity of global energy markets and East Asian financial stability may face a “point of no return.”

Unprecedented Global Impairment: At 19.5 mb/d, approximately 18.4% of global production, this is officially the largest energy supply shock in modern history, eclipsing the combined impact of every major 20th-century disruption.

The “Burn-Through” of Oil on Water: The global economy is currently subsisting on “oil on water” (tankers already in transit), but this floating storage will be exhausted within the next 21 days; once these ships reach their destinations, there is no replacement fleet to follow through the blocked Strait of Hormuz.

Parabolic Price Risk for Brent and TTF: If the blockade is not broken within 14 days, the “scarcity premium” will likely drive Brent crude toward $150–$180 per barrel and send European TTF natural gas prices to record highs as the loss of Qatari LNG and regional supply becomes a permanent structural deficit.

East Asian Economic Contagion: Japan and South Korea, which rely on the Persian Gulf for nearly 80% of their energy imports, face an immediate industrial shutdown; the lack of fuel for power generation and manufacturing will likely lead to a double-digit contraction in regional GDP if the “14-day window” for resolution is missed.

Currency “Whirlpool” Risk: The shock is creating a violent devaluation risk for the Japanese Yen (JPY) and Korean Won (KRW) as these nations are forced to sell foreign reserves to pay for hyper-expensive spot-market energy; we are tracking a “currency whirlpool” where the JPY could breach 160–165 against the USD as imported inflation from the $150+ oil price destroys the region’s trade balance.

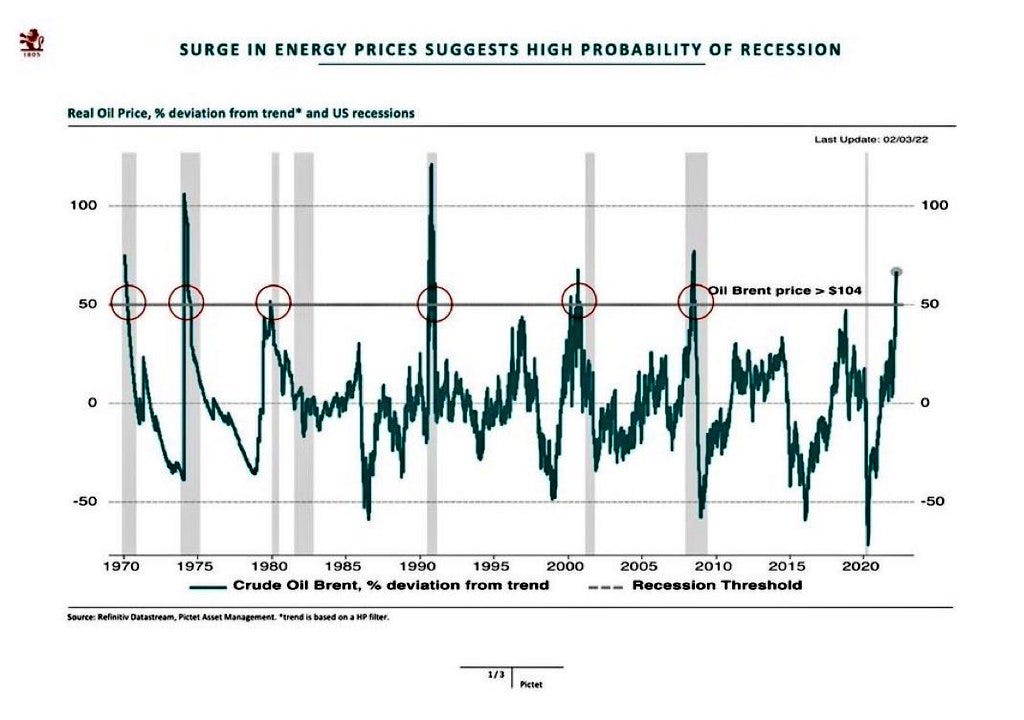

Energy price shocks often lead to broader global macro shocks:

The risk for on-water storage ‘running dry’:

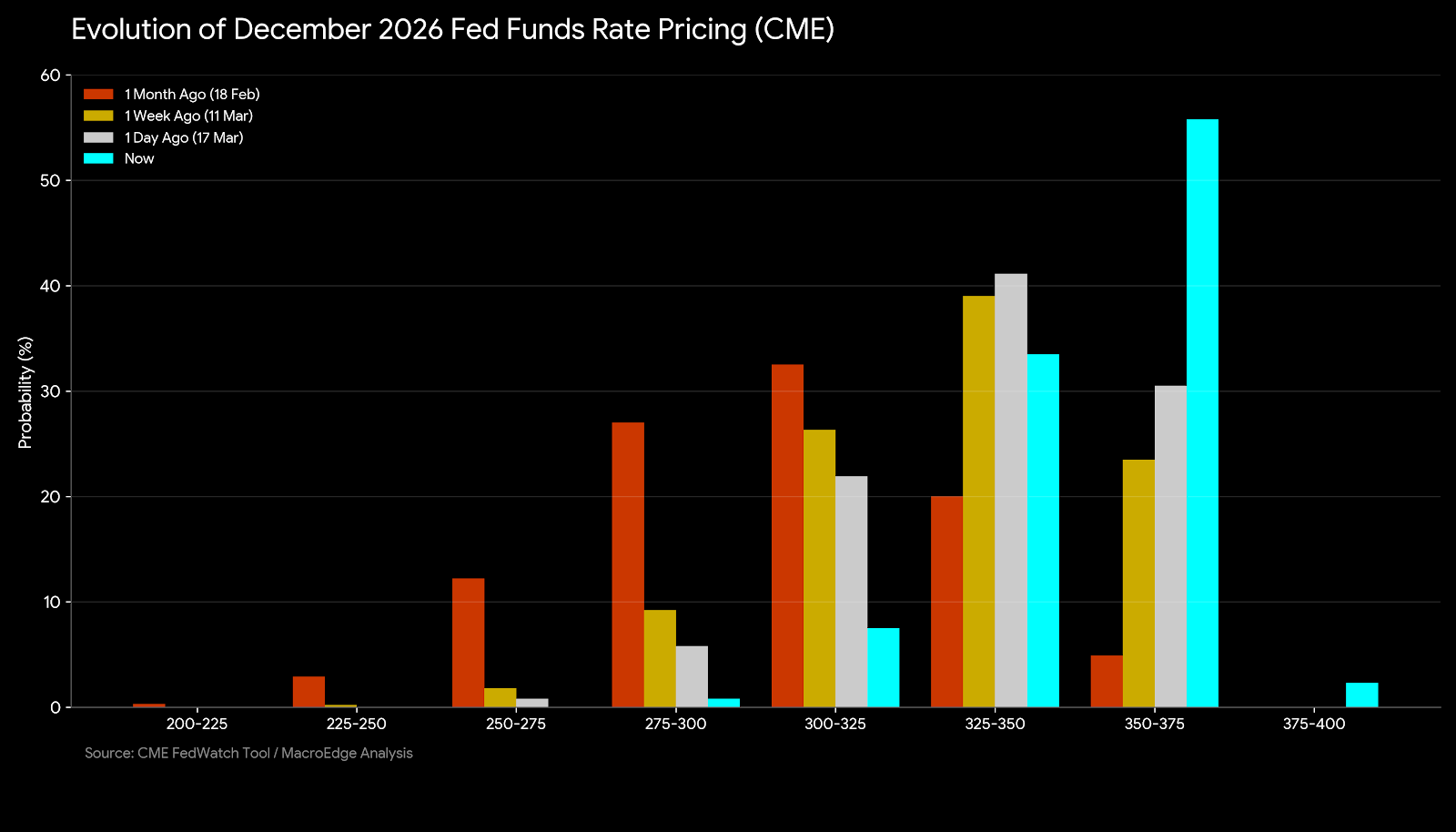

FOMC Recap

The Federal Reserve maintained the federal funds rate at 3.50%–3.75% today, but the accompanying Summary of Economic Projections delivered a significant shift in market expectations by signaling a structurally higher inflation floor necessitated by the ongoing global energy crisis. In his post-meeting presser, Chair Jerome Powell adopted a notably hawkish tone, emphasizing that the “scarcity premium” driven by the 19.5 mb/d global supply impairment has introduced a “persistent inflationary whiplash” that precludes any near-term easing. This rhetoric, combined with a revised “Dot Plot” that showed a majority of officials now favor holding rates steady or even hiking further, has led the futures market to aggressively price out rate cuts for the entirety of 2026 and even into the first half of 2027. Investors are now grappling with a “higher-for-longer” regime as the Fed prioritizes price stability over growth, effectively acknowledging that the 18.4% global oil output loss has fundamentally reset the neutral rate, at least for the time being (see chart above on energy price shocks and their impact on the economy).

Portfolio Strategy Update - Energy Focus

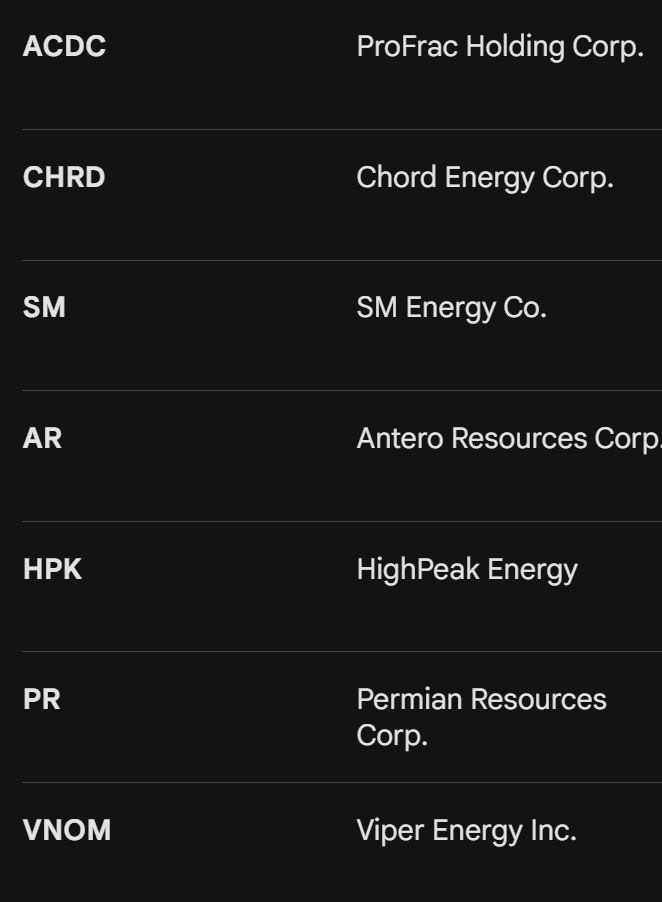

The high-torque oil and gas basket, with some minor adjustments from my first writings on the matter a month ago:

I really like how things are holding up here across the basket - though there’s been some softness in performance from Viper & Permian Resources for the time being. The unhedged high-torque names are leading the portfolio strategy higher - and the risk balance provides for general support at the lower end of the performance spectrum here. While there are higher-torque names and risk could be cranked up to volume level 100, I haven’t seen any highly attractive names like many of those in our oil & gas strategy basket, which covers and captures upside and bullish momentum in the sector.

Equity Research Notes

As Six highlights below, and I agree with the sentiment, natural gas could be setting up for a significant move higher if we start to see broader attacks on natural gas infrastructure in the Middle East. Countries will literally ‘bid whatever’ in order to keep natural gas flowing from wherever, whenever - if it appears that they are going to see any impact to domestic supply.

Our energy strategy benefits from a dual-catalyst environment: first, the direct expansion of unhedged margins for our E&P names, and second, the surging utilization and pricing power within our service sector allocations as drilling activity accelerates. At $100 oil, the “valuation gap” for these small-cap names effectively collapses, as the market is forced to re-rate their massive, undervalued inventory and debt-reduction capacity, potentially delivering triple-digit returns that far outpace the broader energy indices. There may be one or two other names that we seek out amidst this positive environment for oil & gas - but I am happy with the composition for the time being, as highlighted above.

Report Schedule (Rest of Week)

Friday: Redeye Macro Note - Introduction to Trident

Saturday: Saturday Macro Note

Sunday: Weekly Macro Note

Have a great start to your Thursday.

Don

MacroEdge Portfolio Strategy Update - March 18, 2026 (@SixFinance, Head of Research)

Opening Long: Henry Hub Natural Gas

Since the beginning of the Iran “excursion”, Henry Hub natural gas has been little changed. This was largely predicated on the fact that we were simply seeing a supply disruption, and the US already utilizing near-full export capacity, thus being relatively isolated from the demand pull of arbitrage opportunities to spiking global prices.

My long thesis is predicated on a fundamental regime change that was catalyzed today by the ongoing military conflict, which has now escalated from a transit disruption into an active supply destruction event. As of today (3/18/2026), Israeli air strikes have struck Iran’s South Pars gas field, the largest natural gas reserve in the world, and Iran has retaliated by launching missile strikes against Qatar’s Ras Laffan Industrial City, the complex housing the world’s largest LNG export facility. QatarEnergy has reported “extensive damage” to Ras Laffan, which was already offline following earlier Iranian drone strikes.

I believe Henry Hub is materially underpricing the second-order transmission effects of this crisis. With roughly 20% of global LNG supply offline and the primary production infrastructure physically damaged, the global gas market is entering a structural deficit that positions US LNG, and by extension US domestic gas, as the world’s last resort swing supply.

Today’s events, in my view, mark a decisive turning point in the characterization of the natural gas supply shock. Prior to today, markets could reasonably treat the situation as a logistics disruption. Qatari LNG production was suspended largely as a precaution, the Strait of Hormuz was restricted, but the underlying infrastructure remained intact, and a diplomatic resolution could be reasonably expected to restore flows within weeks.

While the extent of the damage done is not yet clear, physical destruction of production and processing infrastructure does not immediately reverse with clearance of passage through the Strait. The 2022 European energy crisis, which drove Henry Hub from approximately $3.50/MMBtu to nearly $10/MMBtu, provides a similar analogue. Russia cut approximately 150 Bcm/year of pipeline gas to Europe by shutting down Nord Stream flows. This supply was delivered via pipeline with no immediate means of substitution (similar to Hormuz-dependent supply today), and Europe was forced to replace it with waterborne LNG. European utilities, governments, and trading houses panic-bought every available LNG cargo in a price-insensitive fashion.

This thesis is predicated on a similar panic buying beginning today. In 2022, the world’s largest flexible LNG supplier, the United States, saw a maximum export pull on a tightened domestic market.

Certainly, caveats exist. We are in a more sluggish demand period as we are not in peak heating or cooling months currently. Exports are already running near full capacity. Diplomacy could prevail.

However, Qatar’s disrupted capacity alone rivals the scale of the Russian supply shock. This supply was concentrated on one demand center, Europe. Qatar supplies both Asia and Europe simultaneously. The competition for replacement cargoes is therefore occurring on two fronts rather than one. Further, in 2022, Russia’s supply cutoff was a political decision that could theoretically be reversed. As the pipelines were already shut off, the Nord Stream pipelines were sabotaged, creating a similar dynamic to that of today.

The qualitative shift from supply disruption to supply destruction has begun, and, absent a quick resolution, I expect panic buying of global LNG to rapidly begin to push Henry Hub higher. On a RISK basis, the lack of a substantial structural repricing in Henry Hub prices since the outbreak of the conflict should create a lower downside profile to a quick resolution than the Dutch or Asian futures, which have already repriced over 75% higher since the onset.

*Important Disclosure: This post is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any interests in Trident I Global Macro Fund, LP. Any such offering will be made only by the Private Placement Memorandum (PPM) and Subscription Agreement. Rule 506(c) offerings are limited to Accredited Investors only. Investing in private funds involves high risk and is not suitable for all investors.

For more details, please refer to our Terms and Conditions.