Midweek Macro Note: Commodity Melt Up Continues, Dollar Alarm Bells, FOMC Review, Earnings Discussion, Oil the King, Portfolio Strategy Commentary and Update

In this Midweek Macro Note - the commodity melt-up is gaining attention in the media and central banks continue to chase safety... we also discuss dollar alarm bells, FOMC, oil, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge Readers & Community,

I’ve had a few days of adventure on the road while my ~3 months of travel to both meet our current & new clients continues around the globe. I landed this evening after a beautiful afternoon in San Luis Obispo, CA, and am back in the air Friday late afternoon to Europe. There will be no change or adjustment in the timing & delivery of our reports, so don’t expect any change in our report sequence.

Tomorrow we’ll have a full update on our 2026 vision for Ozone that we’re implementing - including on the wind down of our legacy client platform and user interface through MacroEdge.net, and our shift for Ozone to a full-substack focus for data, community, research, reports, and more. While we will continue to utilize the MacroEdge.net client portal for Economic Advisory & Transform engagement clients, the interface and back-end end up creating duplicative functionality to what we’ve already got on Substack, and this eliminates the need to maintain two separate logins, user management portals, and send out reports twice to you, the reader. If you don’t have access to our data, reports, research, portfolio strategy, and more, you can access it here:

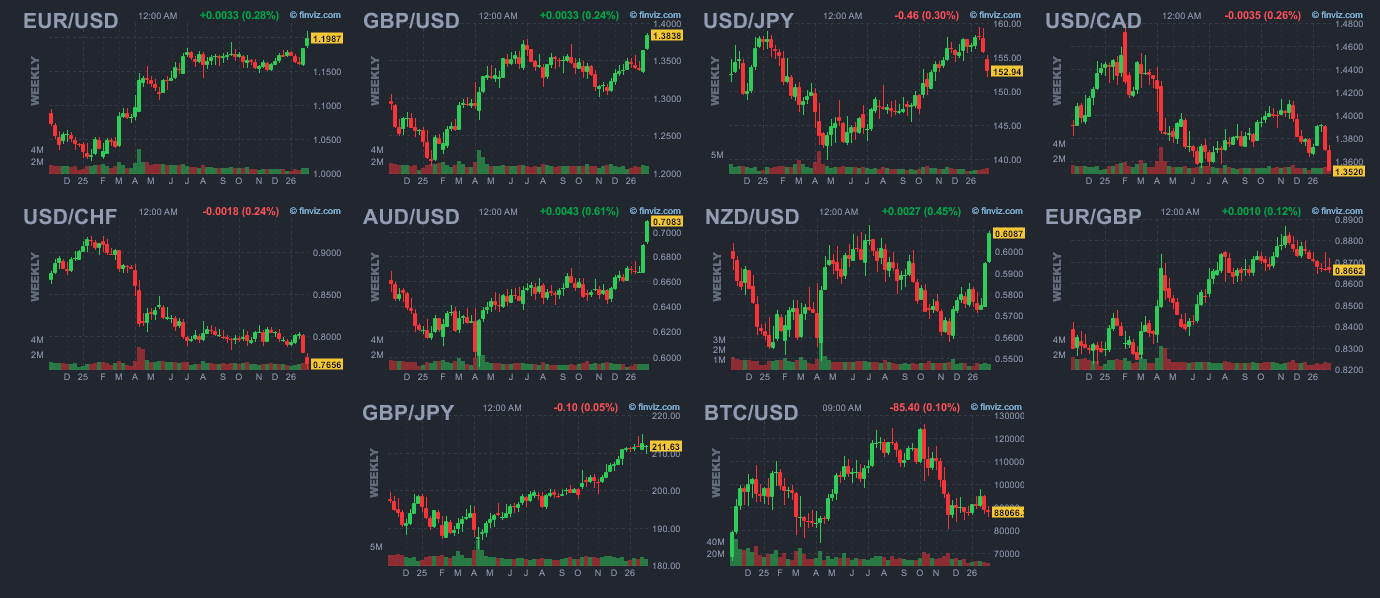

Scott Bessent today reversed some of Trump’s earlier comments about the dollar weakness, which briefly sent the dollar index higher - that has been short lived as that move is fading into the overnight hours while commodities continue to surge. While portfolio commentators on the major networks are continuing to call this period for ‘equities’ - they’re getting decimated by commodity outperformance (which is why few even attempt to acknowledge the moves we’re seeing), and fail to mention the decline of the dollar… The dollar index lost a key uptrend support that’s held since 2011, though we may see an attempt at a reclaim and fail again as the most likely outcome. Further downside would result in additional inflationary pressures, which we’re already starting to see in things like gasoline prices.

Lower dollar = inflation pressures are going up…

Versus foreign currencies like CHF/EUR/GBP - the dollar has been getting clubbed:

… Even against the JPY, the dollar has shed some strength. While the Administration might not be concerned about a weakening dollar, to boost exports and inflation, American companies and consumers certainly will be, even if they aren’t paying attention yet.

Data In Review / for Remainder of the Week

This week, we’ve had some macro data that hasn’t really had any impact on equity markets more broadly. Consumer confidence continues to print dumpster fire readings - as we saw in the latest Conference Board readings. Friday, in the UMich data - the same trend is likely to continue (validating the ‘i’-shaped economic theory)... I use this phrasing because the K-shaped economy misrepresents the actual weighting of the bottom 50% of the economy, which is now more like 80-90%. With the top few % points in our economy driving half or more of consumer spending, the phrasing and labelling of the ‘i-shaped’ economy makes much more sense for the time being.

(Continued below: Data for Remainder of the Week Cont., FOMC Review and Many Questions, Earnings Discussion, Commodity Melt-Up Continues, Oil the King, Portfolio Strategy Update and Commentary) - get all of our research, data, discussions, portfolio strategy, and more → by trying Ozone for one-week and more:

There’s not a ton of important data for the time being, but we will get PPI on Friday, and PCE data was delayed. If we get another government shutdown - even for a few weeks - that could have a huge impact on data for the next several months again - pushing old data into the late spring and even early summer. While that is not my base case, it is looking possible (about 50/50 at the time of this writing) that we see funding lapse for a short while. With midterms, the Administration will be looking for new ways to get people worked up and out to the polls - which is extremely tough in off-cycle midterm years.

FOMC Review - Many Questions?

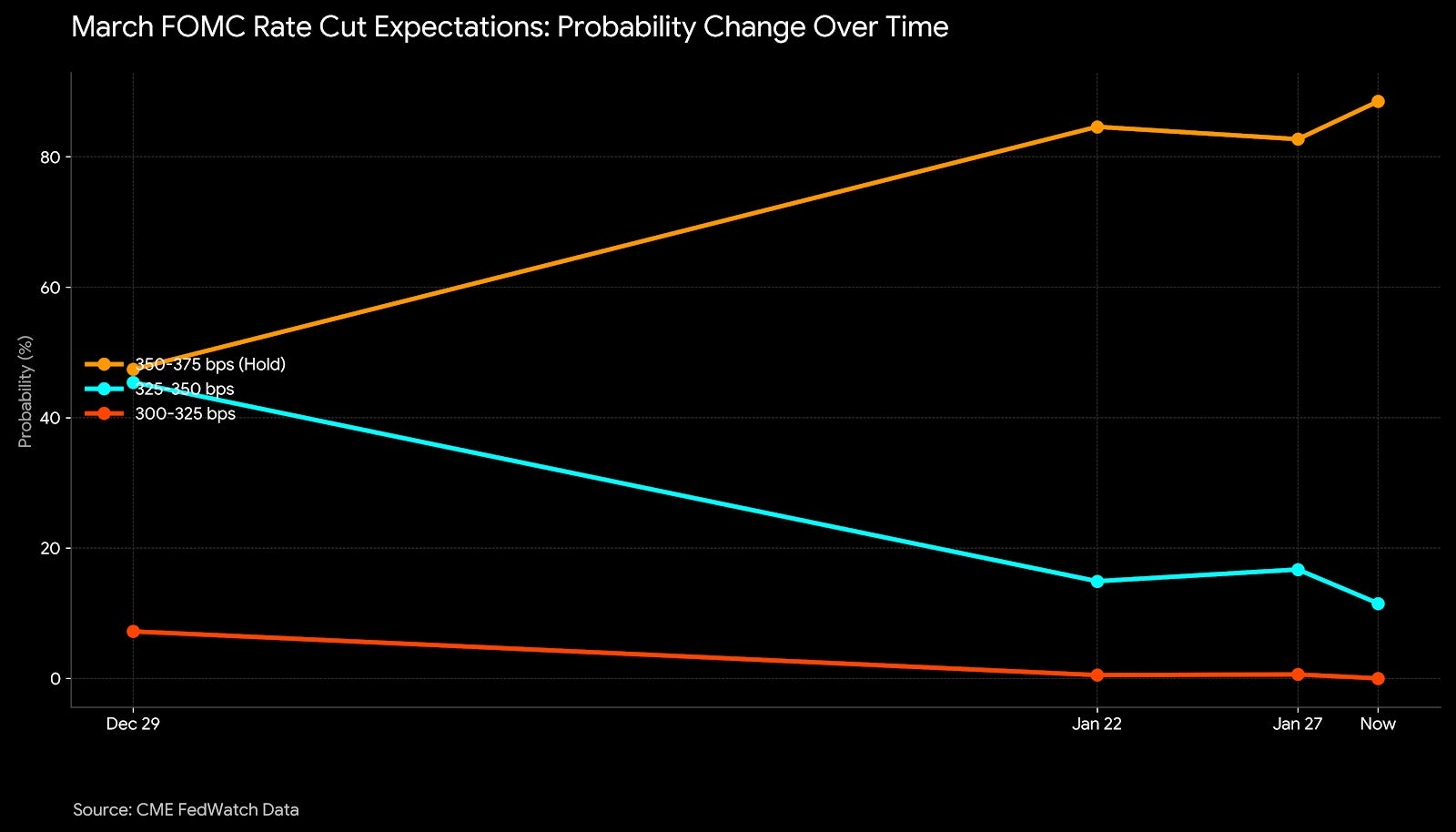

As we (and I expected) - no rate cut today. The question is now how long the hold will last… or even how long before a hike could get priced in? EU policymakers were also very clear this morning in holding rates now, and the easing cycle is over for the time being in Canada.

For March, the cut has been almost fully priced out already:

Interest Rate Pause: The Fed kept the federal funds rate unchanged at a target range of 3.50% to 3.75%. This marks a shift to a “wait-and-see” approach following three consecutive quarter-point cuts at the end of 2025.

Upgraded Economic Outlook: The official statement upgraded the description of economic growth from “moderate” to a “solid pace,” citing surprisingly robust consumer spending and GDP growth despite earlier recession fears.

Stabilizing Labor Market: Chair Jerome Powell noted a “clear improvement” in the economic outlook, stating that the unemployment rate (currently at 4.4%) has shown signs of stabilization, reducing the immediate urgency for further “insurance” rate cuts.

Internal Division (10-2 Vote): The decision was not unanimous. Two members, Christopher Waller and Stephen Miran, dissented in favor of another 25-basis-point cut, highlighting growing internal tension as the Fed nears its perceived “neutral” rate.

Political and Legal Headwinds: The meeting occurred under a cloud of external pressure, with Powell refusing to comment on the ongoing Department of Justice investigation into his past testimony or President Trump’s search for his successor as his term ends in May.

In both the short-end and the long-end, there is no reason to be lowering rates right now. Especially with PCE at 3% and CPI (STILL!) near 3%. End of story. If there was one thing that loved Powell’s tepid (and mixed dovish/hawkish sentiment), it was gold, which continues to laugh at everything policymakers are saying right now in this ‘collapse higher’:

Gold has blown any major equity market out of the water now over the last 25+ years, including many major technology equity names. Sound money is getting great notice now in this era of major debasement and no way out.

Earnings Discussion

The earnings season is shifted into overdrive today with a clear “show me the money” sentiment taking hold of the tape. Despite Microsoft ($MSFT) delivering what appeared to be a powerhouse report, with revenue hitting $81.3 billion and Azure growing at 39%, the stock is under pressure, down over 6%, as the market balks at the massive $37.5 billion quarterly capex spend required to fuel its AI engine. Conversely, Meta ($META) is finding some air; while it also hiked its 2026 capex guidance to eye-watering levels, strong ad revenue and a rosy Q1 outlook have pushed the stock up 9% in recent action. Tesla ($TSLA) managed to squeeze out a 3% gain after-hours as gross margins held up better than feared, but the real test comes tonight when Apple ($AAPL) steps up to the plate. As the S&P 500 flirts with the 7,000 level, the message from the desk is clear: the AI hype phase has transitioned into a heavy infrastructure phase, and the street is starting to count the cost of that transition.

Commodity Melt Up Continues

If the commodity rally (finally) reaches oil and gas, we could be in for major consumer pain, which translates into business pain and even things like social unrest:

Oil the King

Gold is enjoying a nice bounce off of the $54 range lows that held half-a-dozen times over the last year. I have been highlighting this support level over the past 6 months, and the move higher is supported by very positive technicals, geopolitical volatility, and a weaker dollar.

The biggest opposer to any move higher will be the political apparatus, which is terrified of oil and gasoline prices moving higher into a midterm year. With the current price action in commodities - similar could happen in oil if we saw a ‘shock’ style event, in something geopolitical of nature, or 08 of nature, when oil saw it’s largest nominal $ rally higher on record.

Gasoline prices are up about 40 cents from their lows - don’t expect base effect victory laps here if we continue to move higher:

Below, Six will continue with our portfolio strategy update and commentary section - discussing opportunities in spaces like robotics & more. In our Redeye Macro Note - on Friday evening or Saturday morning - I will talk more about the direct beneficiaries of these moves, and how we’re positioning.

Next in the Redeye/Saturday Macro Note →

A Silver State Deep Dive

A Deep Dive Into Energy Opportunities

Air Travel Troubles Continued

Final Data Center & Employment Data – MacroEdge

The next portfolio strategy note & commentary will be available on Sunday.

MacroEdge Portfolio Strategy Update - January 28, 2026 (@SixFinance, Head of Research)

FOMC today was relatively uneventful. Powell’s tone seemed to be one of optimism in the economy, and another source of potential volatility has been removed from the market. A missed flight home from Park City on Monday and a large drawdown concentrated in my Frontier Aerospace positions, following the government shutdown odds spike, caused me to refrain from adding more risk by taking on the software positions, which is probably for the best, as their gap-up on Monday has thus far marked the weekly high. I think I may have misjudged the bottom and may have more time to buy them, possibly at even lower prices.

I have removed PSN from the portfolio and added TKC at a 10% of NAV weight, delevering slightly. I would like to reduce my risk exposure to US equities, as the dollar has plunged and rate cuts are pushed out for the near term. I would like to continue to reduce my US exposure and pick up additional international exposure.

TKC presents an interesting setup, as Turkey is one of the few EM countries that has not yet rallied aggressively with the rest of the world’s EM rally. A neighboring country to Iran, Turkey may be a prime beneficiary of a Middle East peace dividend should the Iranian regime fall. TKC would be a natural partner to provide the backbone for data traffic through Iran in a more pro-capitalist regime. As the most liquid stock in Turkey, through the TKC ADR, it is a natural point of inflow for capital in this scenario.

Additionally, TKC is the preeminent “hyperscaler” of Turkey, and at the end of 2025, it inked a $3 billion partnership with Google Cloud, with Google committing $2 billion over 10 years, and TKC investing $1 billion into data centers and infrastructure. TKC is now becoming a regional AI trade, trading now just at legacy telecom and fiber business valuation. This deal is a game-changer for this business as it allows Turkish data to stay within Turkey, meeting the strict local data residency requirements of the country. TKC can now capture high-value contracts from the Turkish government, banking sector, and defense industry, sectors which previously were barred from using global public cloud infrastructure.

Simply put, this company can see substantial revenue and multiple expansion in two different ways: cloud business scaling and a regional peace dividend. Ideally, both.

Hyundai shares have aggressively rallied on advances in robotics, as their Boston Dynamics stake has finally caused an inflection in their stock price. While Toyota is not yet commercializing robotics, its Toyota Research Institute builds the software that powers the cognitive layer for the Boston Dynamics robot. In short, Toyota’s robotics research division builds the brain that powers the leading robot on Earth.

Arguably, no country needs robotics more than Japan. With over 120 million Japanese and fewer than one million births in 2025, their demographics are a nightmare. In addition to the global robotics interest and capital flow tailwinds, robotics advancements solve a real problem in Japan, not a solution searching for a problem. I, for one, would much rather buy Toyota pre-robotics revenue at ~10x earnings than buy Tesla for Optimus at ~200x. I will be initializing a position here and adding to it further once Toyota more clearly articulates concrete plans for a go-to-market strategy on robotics, as Hyundai did weeks ago. Out of all mega caps, I believe this is one of the greatest global opportunities for a substantial multiple rerating over the coming years.

For more details, please refer to our Terms and Conditions.