Midweek Macro Note: Central Bank Decisions Ahead, Why Initial Claims Mean Less Than They Used To, Commodity Analysis, & More

In this Midweek Macro Note - we discuss the upcoming FOMC & BoJ decisions, talk about why initial jobless claims mean less than they used to, look at commodities, and more. #MacroEdge

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

In this Midweek Macro Note - we’re going to cover ground from employment, to markets, and technicals, and take a look at the disconnect between initial jobless claims, U3 unemployment, and job cuts - which have hit their highest level (on an annualized basis) since 2008, excluding the pandemic lockdown period.

Markets have churned slightly higher this week on ultra-low volume, while the crypto space has seen a bit of a bounce. The rip in metals has stalled a bit through the second half of the week, and commodities like natural gas have continued to move higher. Oil has continued to be a notable outlier relative to to the sizeable move in commodities - which are again near breakout levels for higher levels across the board.

(CRB Index)

Natural gas today hit its highest level since 12/22:

With low base effects from oil beginning to roll off in the new year, the so-called ‘battle’ against inflation (laughable) will become more difficult. For the time being, the Fed has accepted 2.8-3.0% level as its acceptable target, and with U3 likely standing at 4.5%, and ending the year at 4.6 or 4.7%, the whole picture gets even more convoluted. This is one of the most complicated macro pictures we’ve ever seen, especially given the deterioration of data quality, though for the time being the equity market remains the #1 focus of the Administration until/if bond market issues arise.

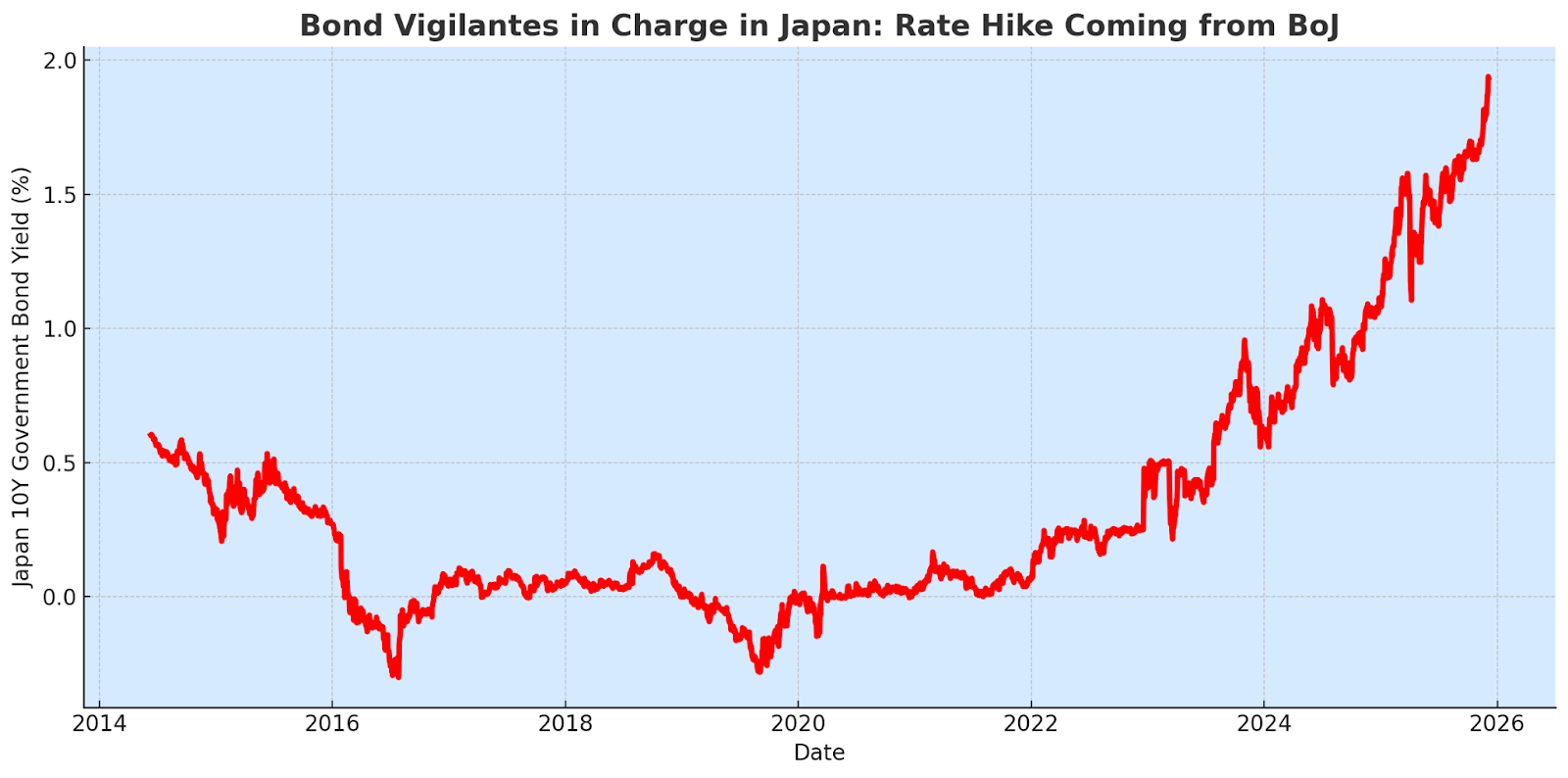

In Japan, which we also discuss below, the 158 level held on the JPY, as the dollar index has ticked lower. Japanese yields continue to blow out to the upside, with the 2Y/10Y/30Y/40Y all pushing towards multi-decade, and record highs. There’s now a 9 in 10 chance that Ueda & the BoJ raise rates again this month. Also note from previous discussions that larger concerns usually arise for global markets when the BoJ begins an easing process. While we stand around and wonder where the so-called bond vigilantes are for the time being in the United States, they’re busy slapping around the BoJ like nobody’s business. We got another soft ADP employment report for November, which bolstered rate cut odds domestically, and further back the ‘macro disconnect’ that’s only accelerated as fiscal has gotten more active in equity markets since the April lows.

Key chart to watch in 2026 will be investor margin debt:

Funding stress continues under the hood, setting up the groundwork for more volatility again in 2026. For the time being, with such low volume and active daily market intervention from fiscal, the story stays the same. One of the things I am looking at exploring in 2026 will be new thematics around broader macro trends impacting both the economy here in the United States and abroad. We’ll explore complex and difficult questions, topics, and trends, and as I brainstorm new themes and subjects, we’ll outline them over the next several weeks.

Wall Street is triumphing over ‘Main Street’ in a bizarre Gilded Age 2.0.

Get two week access to MacroEdge Ozone below:

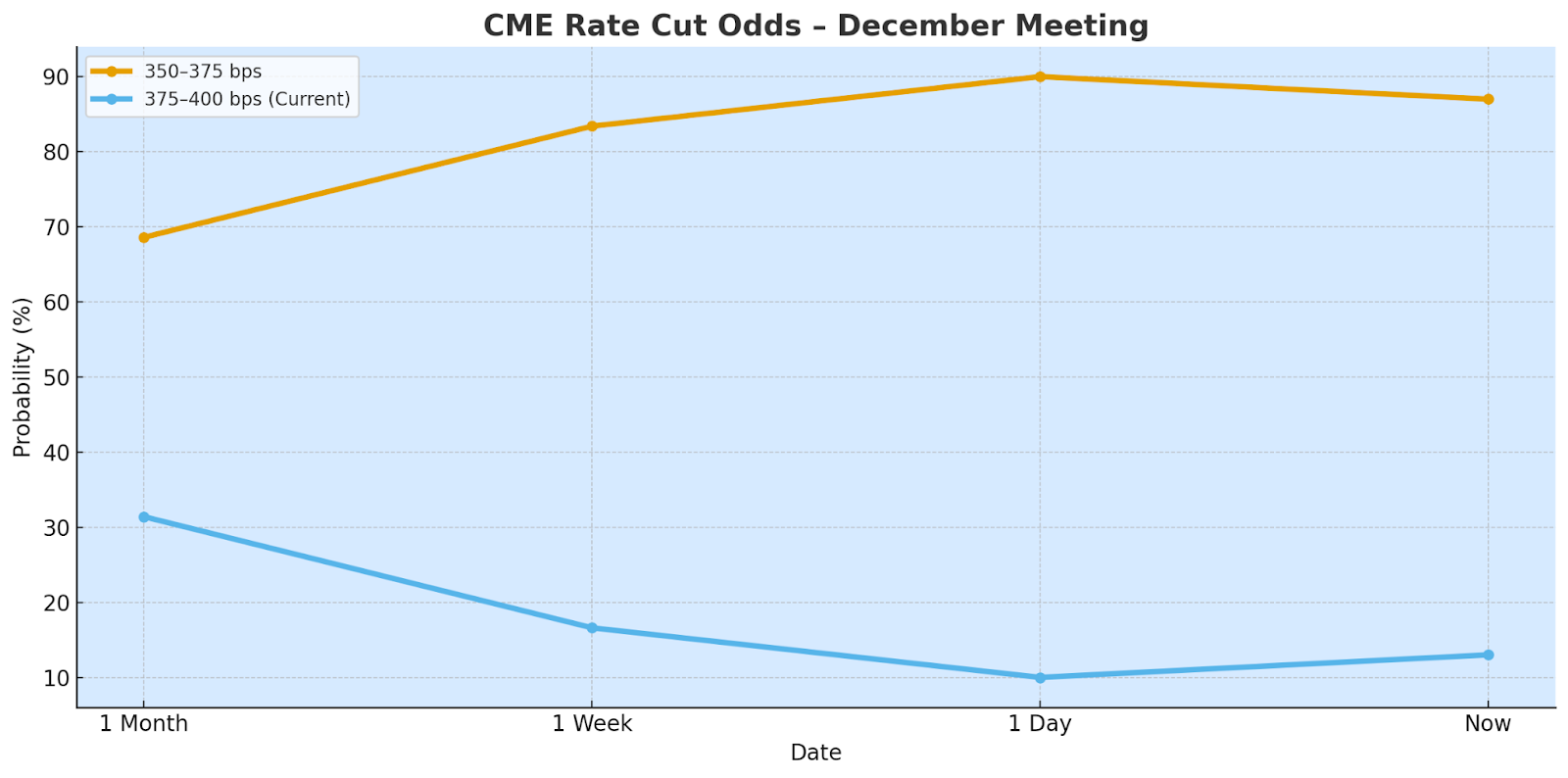

December FOMC/BoJ Preview

Odds of a rate cut are about 87% and with PCE tomorrow will directionally lock in the move for the meeting. In Japan, odds of a hike are up to 90%. The 10Y is below:

Claims Disconnect - A Look at the Five Largest States

One of the most common questions emerging in recent weeks has been regarding the substantial disconnect between job cuts (tracked by us, as well as Challenger G&C) and initial jobless claims. While demographic headwinds will change labor conditions and the way we approach things like the unemployment rate in the years to come, and migration has slowed rapidly over the course of the year - these do not explain the disconnect between the near-record level cuts versus lack of claims that we’re seeing.

For the time being - it’s a cost of living crisis issue, and an economic evolution. As we’ve evolved away from the traditional white-collar corporate structure for a broader swathe of the economy, the gig economy and 1099-NEC world has grown drastically to service the upper 80-99.9%ile of the economy (yes, Uber - but think Amazon delivery, and so many other roles we might not traditionally think are 1099-NEC). This is all part of a larger evolution in our employment market that one might call a mean reversion away from the middle class, and the growth of a much larger permanent asset-free underclass (think, Project South Africa - as I describe it frequently).

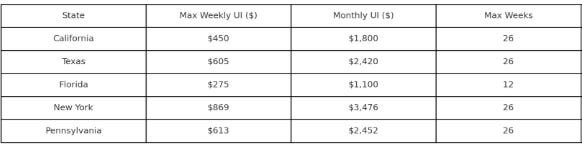

With that being said, most rational individuals who are impacted by a job cut will not immediately pursue UI benefits in their respective state. UI benefits are well below the average minimum cost of living threshold, as shown below in our table:

Versus average monthly cost of living (total sum) in each state being:

> California: $5,403

> Texas: $4,358

> Florida: $4,884

> New York: $4,950

> Pennsylvania: $3,500

Now, compare that side by side to the average Uber driver income:

While we can go into nuance for those that might not have a vehicle, Uber is not the only available 1099-NEC work today, with dozens of options for those able-bodied individuals in larger metro areas.

Low claims are largely about high cost of living versus extremely low UI benefits and not labor market strength in 2025, it’s important to understand the nuance, as job cuts continue to roll out from companies, small and large, at elevated levels. As readily available 1099-NEC income earning opportunities remain, it will continue to serve as a superior substitute to UI for the time being, unless UI benefits are boosted dramatically, which is a political discussion.

Canadian & Spanish Speculative Gauges (TSX / IBEX)

Our speculative gauges in Spain & Canada (might as well throw South Korea in the bucket - where young investors have given up their homebuying dreams to speculate in leveraged products) continue to move higher.