Midweek Macro Note: BoJ Hikes, Carry Trade Alive & Well, Dancing thru Holiday Landmines, Major Move Coming

In this Midweek Macro Note - we explore the BoJ rate hike and its implications, look at the carry trade - which has wound the AI trade into its web, talk about holiday landmines, and a move on the way

Good Thursday evening MacroEdge Readers and Community,

This week we’ve been able to process some important data - including in employment, inflation, in housing, and more. Pending sales have dipped sharply this month as the dip in rates has come to a halt, and for now - it doesn’t look like the Administration is going to push the 10/30s lower without additional intervention (talking, or policy). The Fed’s policy pivot to balance sheet expansion is now fully underway, in our latest rendition of ‘not QE’. The CPI data today was a comedy clown show, with imputations in data near record highs and entire datapoints in the calculation entered as 0% for things like OER, would take with a grain of salt for the time being from a data standpoint - though things like gasoline and rent prices have backed a softening from the 3.0% YoY CPI level. The U6 unemployment rate is nearing 9%, supporting much of what we’ve been tracking this year.

With the Bank of Japan meeting now behind us, there were few surprises from it. A notable fact was that this was the first time in 3 decades that Japanese YoY inflation had registered higher than that of the United States. I also continue to anticipate that we start seeing more trouble in global markets & with the global macro landscape as Japan eases, rather than the other way around. The pendulum is still roughly in balance - though it appears that Europe is done reducing rates for the time being, and the UK is also shifting its tone. With little in the way of fiscal sanity still in the world - the 10Y is still looking constructive, here in the US:

This isn’t hugely concerning, below 4.21%, for the time being - however. Commodities also continue to move with the long end.

The Yen didn’t appreciate a fairly dovish BoJ - that was only in-line with expectations, and nothing further:

The Bank of Japan still remains sharply behind on tightening this cycle - as evidenced by the massive bubbles that have been blown in both the Nikkei & the TOPIX. As we highlight below, and have discussed more in recent weeks - this will have impacts on the US AI trade, tech trade, and more.

Note the BoJ 2Y still pushing higher after the 25bp hike:

There’s a unique window of opportunity for some late-December & January volatility given the current conditions and complacency, but we still need a catalyst for a broader downside move that has yet to materalize. For that to occur - we’ll need to see participation in the MAGS and AI generals (yes, Oracle has gotten smacked…). Overall, the indices are not reflective of a lot of the course correction going on under the hood - and there is many reasons for that… concentration being one of them.

Employment / Inflation + Fed Overview

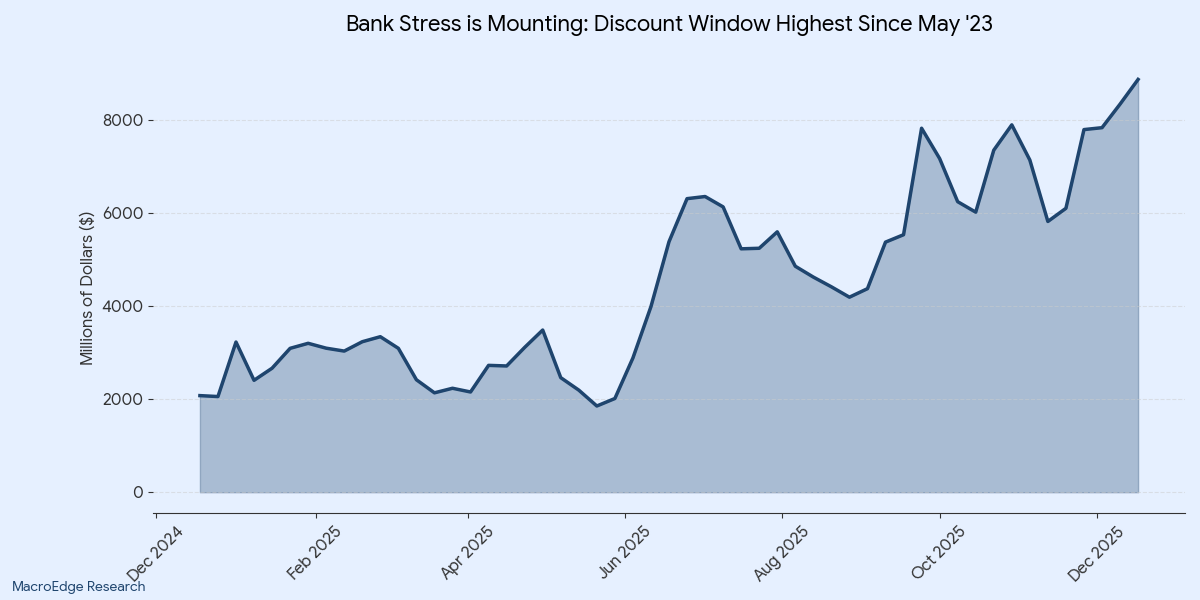

The Fed is facing a cooling labor market coupled with rising bank and funding stress. The Discount Window hit its highest utilization since May ‘23 today - and if you recall, that is when we saw SVB and several other sizeable banks fail. This is something to definitely keep an eye on, as it’s not a positive signal for at least some in the financials/banking sector. As we’ve theorized, there are likely several mid-large community & regional banks facing severe pressures, and this is being reflected in the rising utilization of just one of the many Fed ‘soup kitchens’.

Don’t have MacroEdge Ozone? Get access through Substack below & never miss a beat:

CPI YoY View

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.