Midweek Macro Note: An Uneventful 25BP - FOMC Recap, Stagflation, Technicals, the Wrath of Don

In this Midweek Macro Note - Don & John dive into our FOMC recap - covering the 25bp cut, global updates, the continued 80s-style Japan meltup and speculation, and much more.

(@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge readers and community,

This evening we get to recap a mostly uneventful and expected FOMC outcome. Markets went in heavily expecting the 25bp cut, and that’s what was delivered. A dissent from Miran on reducing by 50bp, and a single member wanted to hold rates where they are.The pathway for October will still have some bumps, as the 10Y fully recovered its initial drop by the end of the day, as anticipated. Given the current fiscal situation, it’s going to take more to bring the 10Y down, if they want to hold it sub-4 now. With central banks expanding their gold holdings globally (above those of their TSYs), it reveals the stance of central bank heads on the risks of holding US debt, particularly long-duration debt.

To join our Thursday Macro Roundtable (9/18 at 9pm EST) -> sign up here:

Limited to 20 seats right now.

As we see the tarnished Powell tenure wind down, he looked rather frail today, and notable takeaways are below:

Access MacroEdge Ozone for two weeks below:

Recap of the Meeting: Fed Leaves Huge Variation Open in Expectations

25bp cut - as expected

Fed avoided front-loading as they did last July - that means labor can continue to cool

Labor market risks tilt negative

Inflation still above target

No pathway for 2026 right now, wide variation is expected outcomes

Institutional Research – Expanding Reach and Remaining on Track for 10/1

On October 1st, MacroEdge Institutional Research goes live.

The system is built to dominate, not to imitate. The datasets are flowing at scale. The architecture is running exactly as designed. Trial accounts are already being provisioned. They will see what we see – the MacroEdge engine in its raw form.

October 1st is the inflection point for our research firm, and you can put yourself on the interest list below:

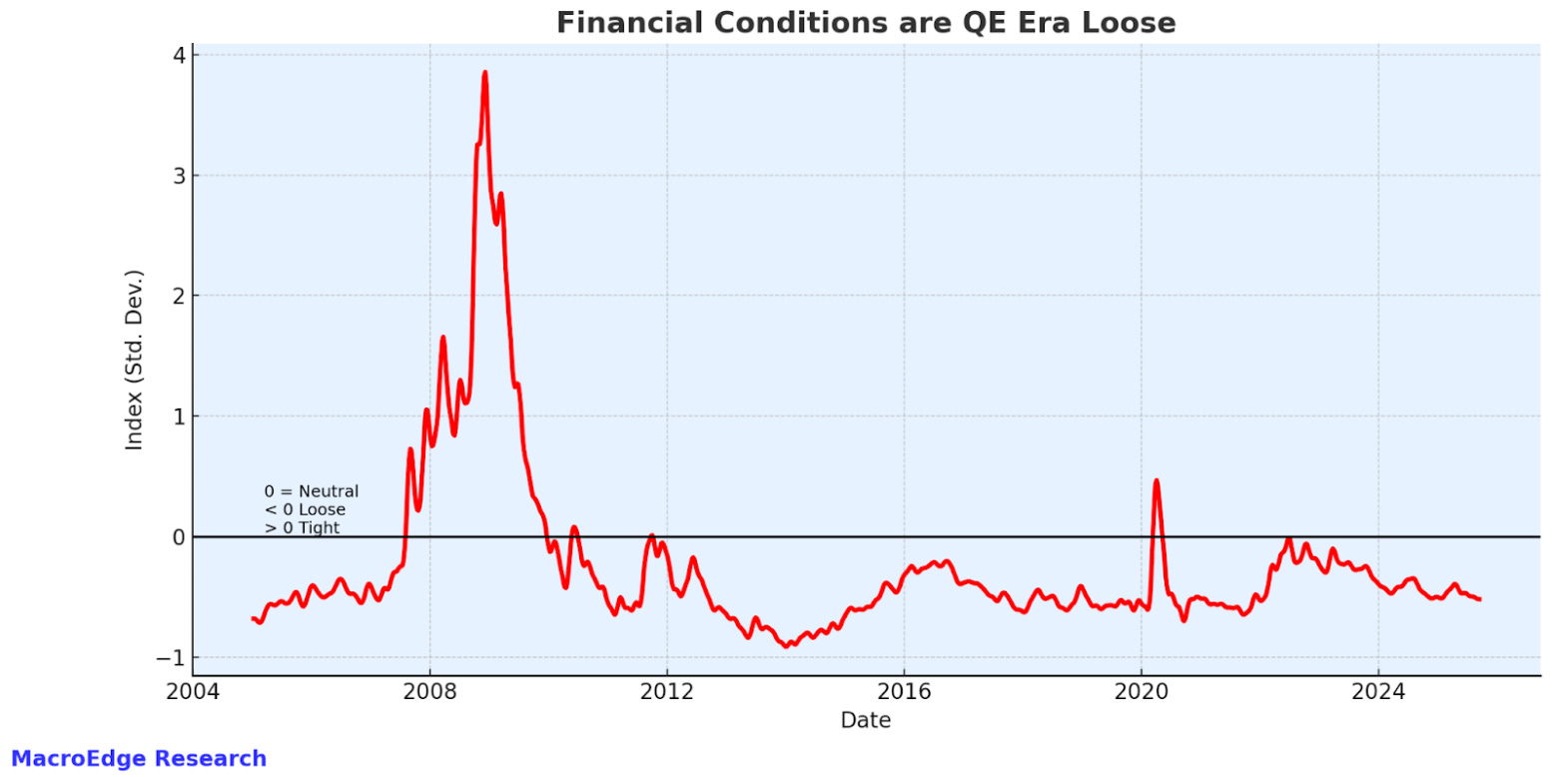

3% is the New 2%

In a continued theme we’ve talked a lot about over the last 18 months - ‘the Fed has appeared to set their inflation target right around 2.8%’ (Anna Wong - Bloomberg) - and that’s continued to reflect in complete mania across equity segments and asset classes, they’ve also continued to loosen financial conditions:

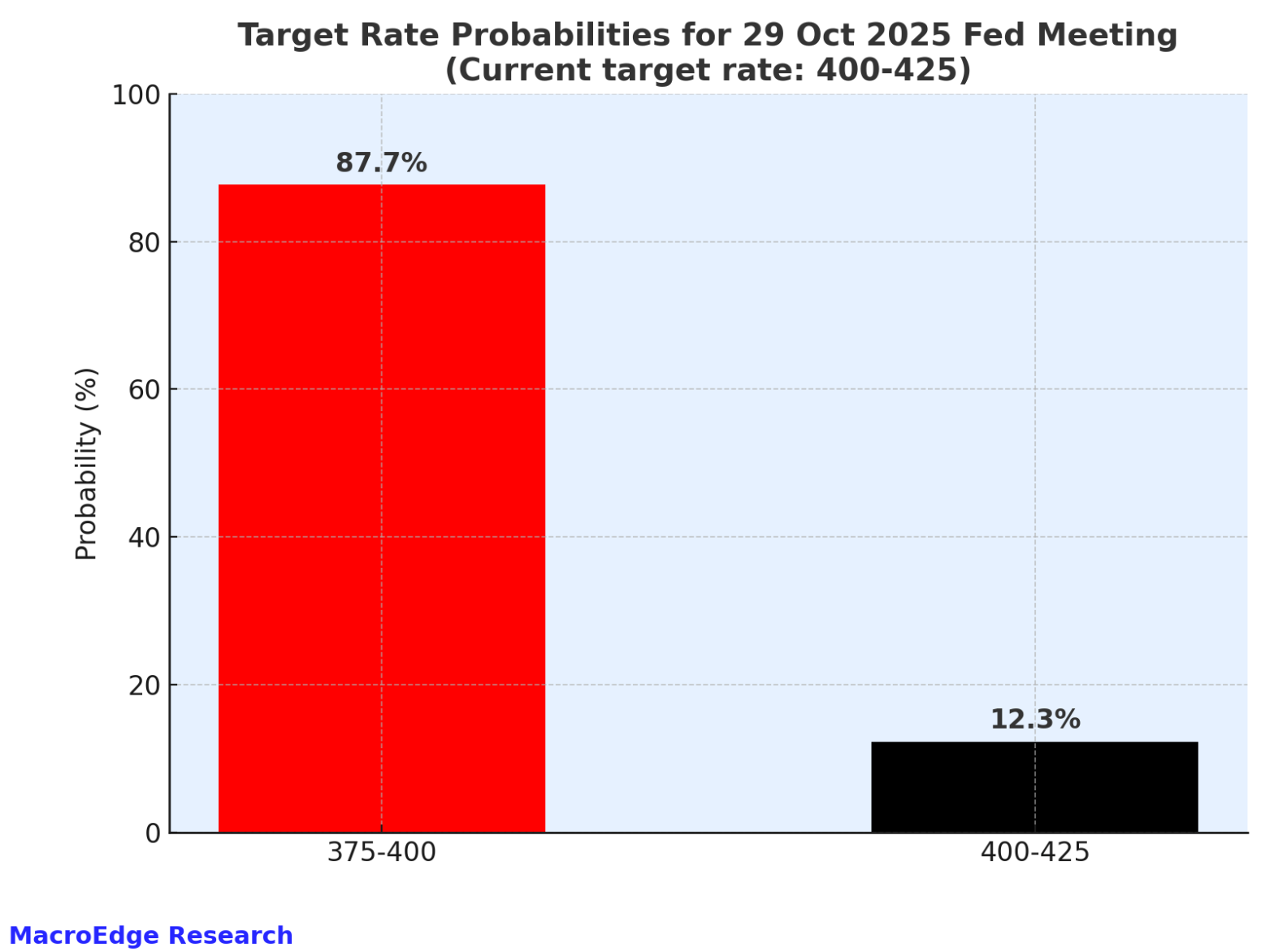

Looking forward to October - it’s looking like another 25bp cut is on the table.

What’s Ahead for the ‘Dual Mandate’

The likely addition of a third mandate at some point during the course of this Administration. (seriously).

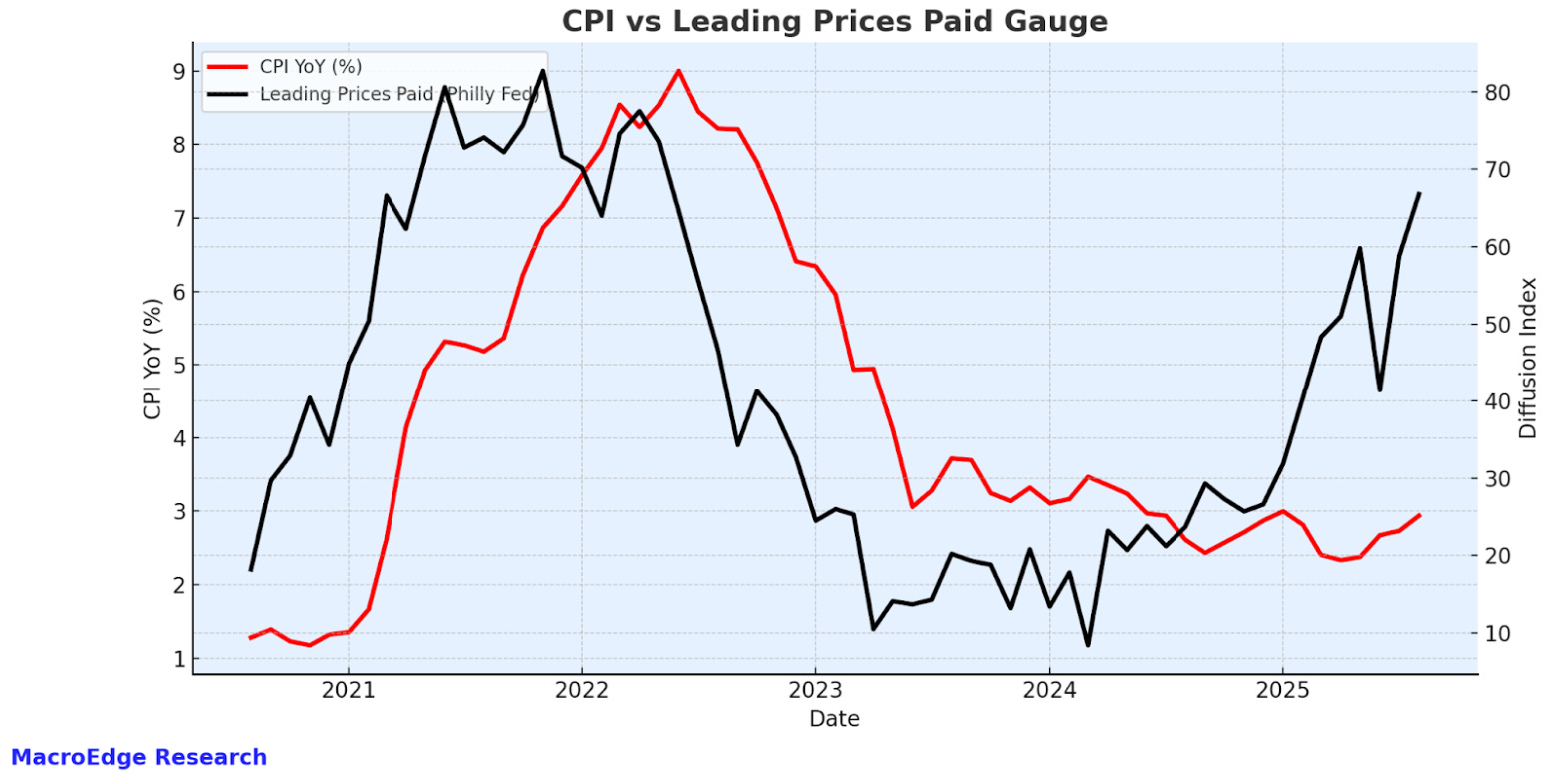

Inflation risks have not abated - and if there’s any meaningful rise to fuel/nat gas prices - expect CPI to tick back up towards 3.3-3.5%.

Higher CPI and higher unemployment (and a higher 10Y) would mean a very stagflationary scenario.

Employment risks also continue to rise - especially in the cyclical areas of our economy:

With deportations and a tighter labor supply as retirements surge due to rising asset prices, the breakeven rate is a lot lower (even seasonally adjusted) - and if the Admin truly wants lower rates, they’ll need to target employment.

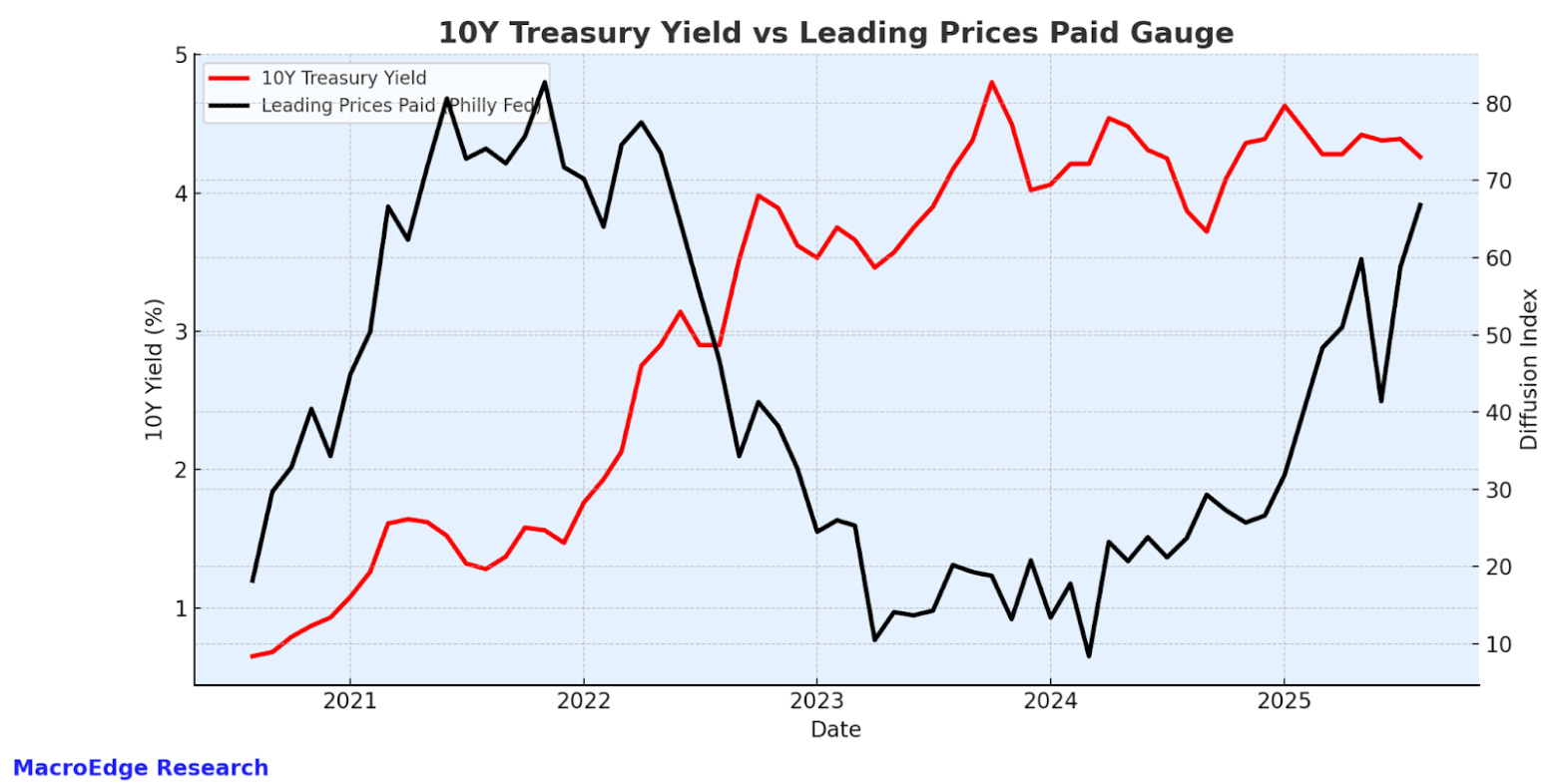

10Y Stays on Its Feet – Energy Asymmetry, Yet Again

As the rate cut decision was announced, there was a quick bid on bonds that was immediately sold off as Powell started talking. The 10Y again found support, though is hanging on by a thread, any signs of a wake-up in CPI/PCE/PPI and energy prices, and likely bounces back towards the mid-4.2s. If the employment situation cools any further than a U3 >4.4, and initial claims move higher, this will weigh on prices and we’ll get an opportunity for catching a bond bid.

Technicals - Music Starting to Slow, but no Signs of Stopping

From a technical standpoint, crosscurrents remain the name of the game.

USD - Dollar DXY Index

Came very close to breaking down initially today, though recovered some of the dip by end of day. A monthly chart -so a major, major pivot point.

USD / JPY - Dollar / Yen

Nothing too critical here

Dow Jones (DJIA)

VIX

Finding a nice base again.

Bitcoin

We have an exciting partnership to announce here for new data.

No new high here on the largest cryptocurrency, diverging from equity all-time highs. It led in April higher, likely leads next direction, too.

Nasdaq 100 - Technology

This remains the most important chart for the year (and likely the next 6-12 months of equity price action). Similar setups in the MAGS have been breaking out to the upside:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.