Midweek Macro Note: A Preview of the Second Half, Energy Portfolio Strategy Update, the MOAB, NFP Preview, Portfolio Strategy Update

In the Midweek Macro Note - we discuss what's next for MacroEdge, highlight the latest for our Energy Portfolio Strategy, talk about 'the MOAB' in South Korea, Japan, and AI in the US, and much more.

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

It’s been a relatively slow week thus far in US markets as momentum traders have lost some ‘pep’ in their steps and both companies and investors are getting more wary of the AI ‘super’ bubble… I’ve upgraded this from a run of the mill bubble since this disaster that they’ve created is one that’s going to either require massive government intervention to save, result in a full credit cycle, or both. Right now we’re sort of in a ‘wait & see’ pattern, and they’re bringing in the final liquidity batch, as made evident by the elimination of the pattern day trading rule, a reduction in the SpaceX investor minimum for the pre-IPO round, and I can go on for days as I have many instances over the last 24 months. This cycle is unique in that the government is likely going to provide unprecedented support and a backstop as soon as things look a little bit wobbly - with how broken the ‘real’ economy is. Couple that with the Strait of Hormuz closure (now over 90 days, which we’ll discuss more in the Redeye Macro Note), and the political Administration is looking for any straw to grasp at this point.

The Nasdaq and other indices are starting to show weakening technicals, and internals are softening outside of the AI-sphere, even as the Dow led the rally higher today on slightly higher rates:

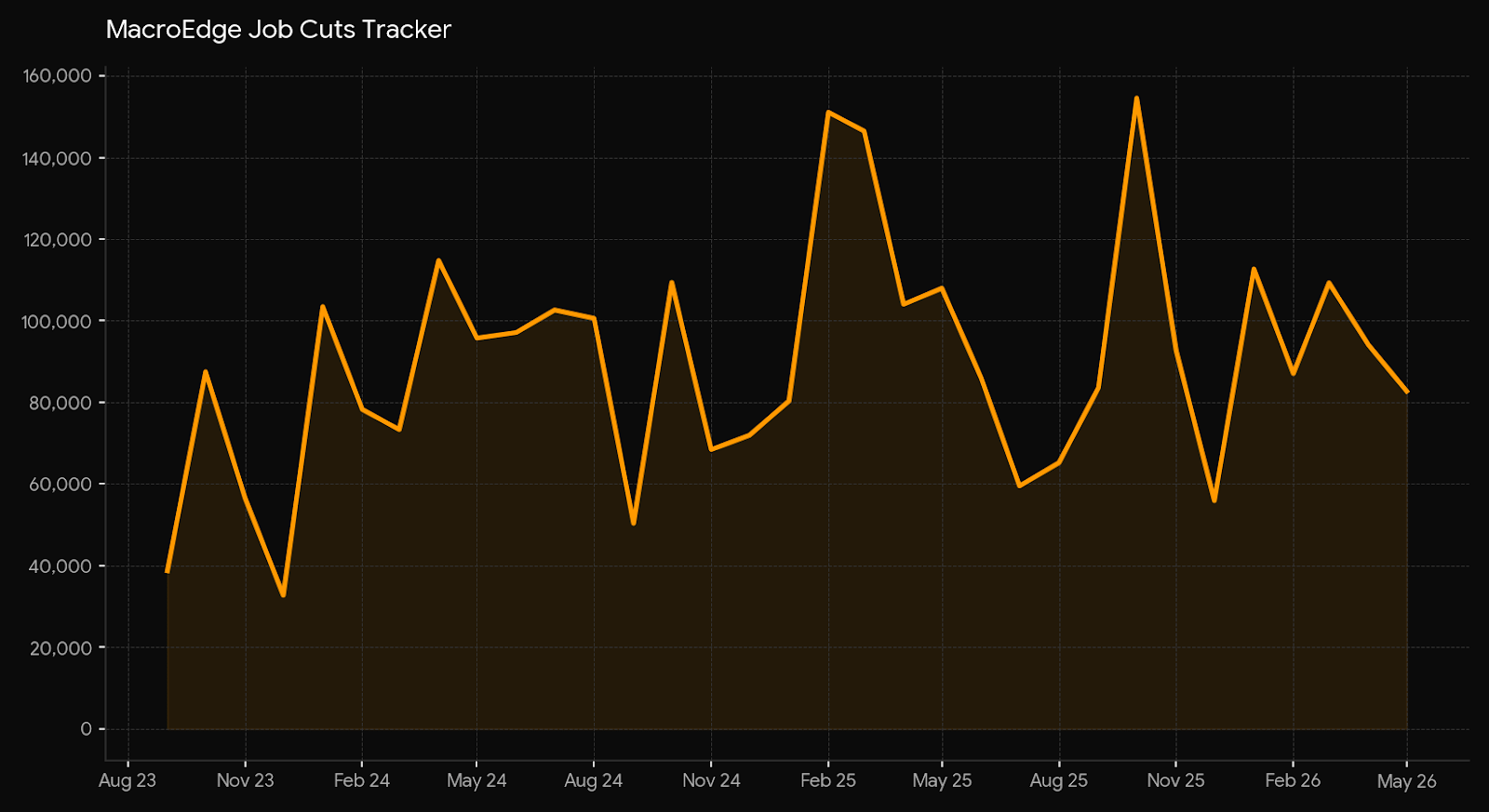

One of the larger risks now is what’s happening in Asia - so keep an eye on Japan and Korea in the coming days - namely, with how weak the Yen is, and how the carry trade has supported this massive bubble across our indices, and with Korea having the most severe reading in the MacroEdge Global Bubble Index reading. Tomorrow is more nonfarm payroll noise - which comes in the face of once-again elevated job cuts in May. Job Cuts in May landed at just over 80,000 - per the MacroEdge Job Cuts Tracker - at 82.7K:

Tomorrow - I expect to see an okay nonfarm reading - but for many of the wrong reasons that we’ve discussed for the past few months. The data center buildout (which is a more ‘supersized’ version of the shale boom from 2011-2014) continues to mask some of the cyclical labor market weakness - and contract employment is acting as a boon as well. With demographics as poor as they are and with retirements surging, a trend that will continue for the remainder of the year, this is keeping unemployment at a structurally low level in appearance, though not in reality. Job seekers know (as highlighted in some of the data below) that the actual job search reality is telling a much different story than the data itself right now, and much of the data itself is becoming more & more noisy, making it less and less useful in how we approach the macro reality both here & abroad.

The idiocy and failure of policymakers to prevent the bubble that they’ve supported in places like Korea will have massive ramifications around the globe, and we need to work through the next round of IPO-exit liquidity here in the US before meaningful downside opportunities are generated. I expect that we will see policymakers attempt to balance their bubbles with interventions and other short-term policies that will eventually be bulldozed by reality when that day comes.

Additionally, we’ll take a look at a preview of the second half for MacroEdge and beyond - there are a lot of exciting things we’re bringing to the mix - especially with Portfolio Strategy. While we had planned to include The Macro Club as a second half addition, we have decided to merge this in functionality with Portfolio Strategy so anyone upgrading (or signing up for) Portfolio Strategy will also get access to all of the community elements and functions we’ve been wanting to introduce.

A Preview of the Second Half - MacroEdge & Beyond

The second half of the year is going to be a busy one for us. I will be in the Dallas area next week to expand our footprint as we continue to expand the oil and gas side of our business - not only on the Macro Research & Transform front - but also through our partnership with an upstream firm located in the area. We’re continually innovating and adapting to this rapidly changing world, and even in a landscape of new X algorithms and changes to things like our Transform business, Macro Research remains at the heart of everything we do.

As promised, there’s a lot coming in the second half of the year - specifically with our oil and gas partnership, with Portfolio Strategy - under our Macro Research umbrella, and with our Substack in terms of how we continue to grow and expand our community here. I will also be starting media appearances in the second half of the year - and this is something that many, many people have requested for many years now.

What’s new in H2:

Portfolio Strategy (Macro Research)

Trident

Announcement of our Oil and Gas Partnership

Expansion of our Substack Capabilities

& More…

Look for more in-depth information in the Redeye Macro Note.

Not yet a MacroEdge Subscriber? Upgrade below, and get all of our research, data, portfolio strategy, and much more.

Energy Portfolio Strategy Update

The Energy Portfolio Strategy has had a very strong week. Even with our trimming of SND, the remainder of the basket: ACDC, CHRD, and KGEI have had a fantastic week.

Continued below: Energy Portfolio Strategy Update, The Moab - Korea, Japan, & the AI trade, NFP Preview, Portfolio Strategy Discussion - Six, Driving in the Rearview Mirror - John)

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.