Midweek Macro Note: A Looming Energy Crisis, Strait of Hormuz Update, Looking at our Energy Portfolio Strategy, Rate Cuts Disappear, Portfolio Strategy Update, and More

In this Midweek Macro Note - we discuss a looming energy crisis, talk about the Strait of Hormuz, highlight our energy strategy, talk about the pricing out of rate cuts, Six provides an update, & more

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers & Community,

This week has been a wild one thus far - starting the week off with fireworks in the oil and gas markets, to the massive interventions we saw by the IEA, G7, and Department of Energy that concluded with a fake tweet from the Secretary of Energy about US Naval escort ships guiding a tanker through the Strait of Hormuz. A lot of signals are emerging that global leaders are becoming much more aware and concerned about the current supply freeze in energy markets that is stemming from an effective closure of the Strait of Hormuz - currently being enforced by the IRGC through drone strikes and mines. As macro data has shifted to the back seat for the time being, oil and energy have taken the front seat.

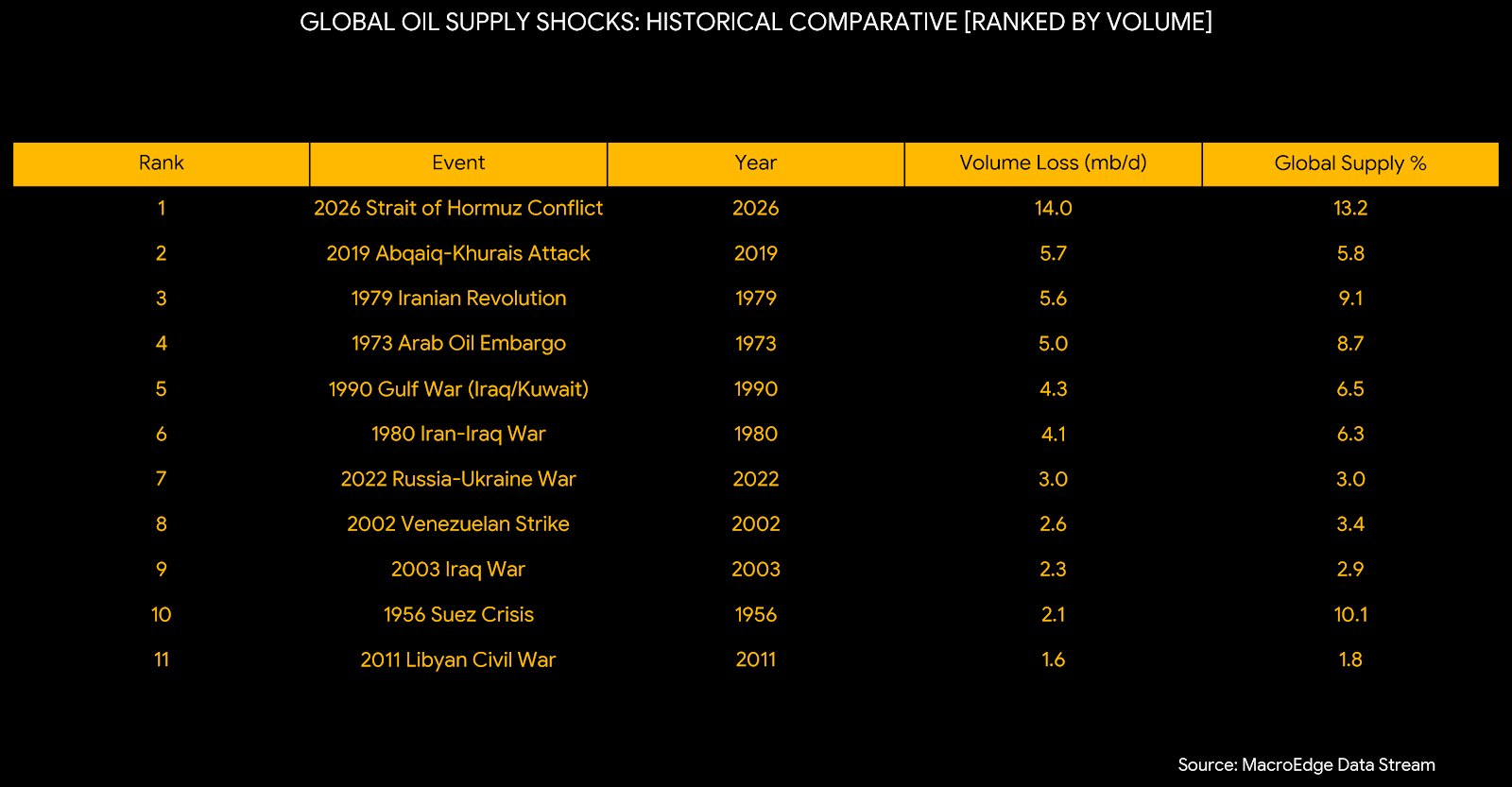

Comparing the current Strait of Hormuz crisis to other oil shocks puts this at the worst we’ve seen. The longer this goes on, the bigger the impact will be to the global economy. As we saw in 2008 as one example, oil eventually hits a threshold that begins to shut down economic activity - especially in the industrial and foodstuff economies - and things get worse from there… the inflationary slingshot results in the (dreaded ‘d’ word) that I’ve labelled as the deflationistas for the time being.

(Global supply shock above [worst in global history] - MacroEdge Data Stream).

For the time being, it looks as if Iran has dug their feet in on their current military strategy, and energy prices are going to be in the driver’s seat for the time being on things like rates. We came into the year with people screaming about rate cuts - and now we’ve priced less than one cut fully for the year, which has been a major change. The 10Y yield has surged higher amidst the energy crisis backdrop - nearing the 4.3% threshold.

With all that being said, and with energy in the driver’s seat (typically another late cycle signal), let’s see how the crisis evolves over the next days and weeks. There is a chance that if we see things escalate over the weekend, we end up with another huge Sunday evening move in energy futures.

Not yet a MacroEdge Ozone subscriber? Subscribe to Ozone through Substack and get all of our data, research, reports, and much more below:

Are you or your enterprise flying blind in times of uncertainty? MacroEdge Economic Advisory is at the forefront of intelligent decision-making for decision makers in governments, firms, and funds across the globe - learn more by contacting us at: macroedge.net/advisory

Let’s dive in.

A Looming Energy Crisis

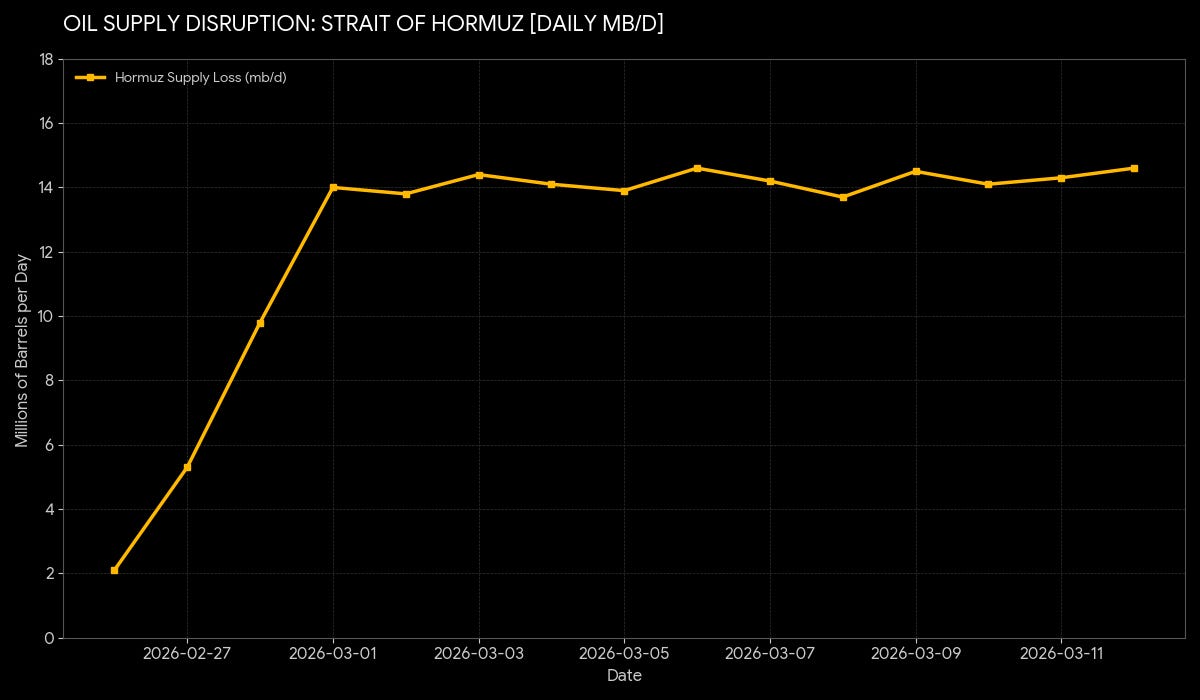

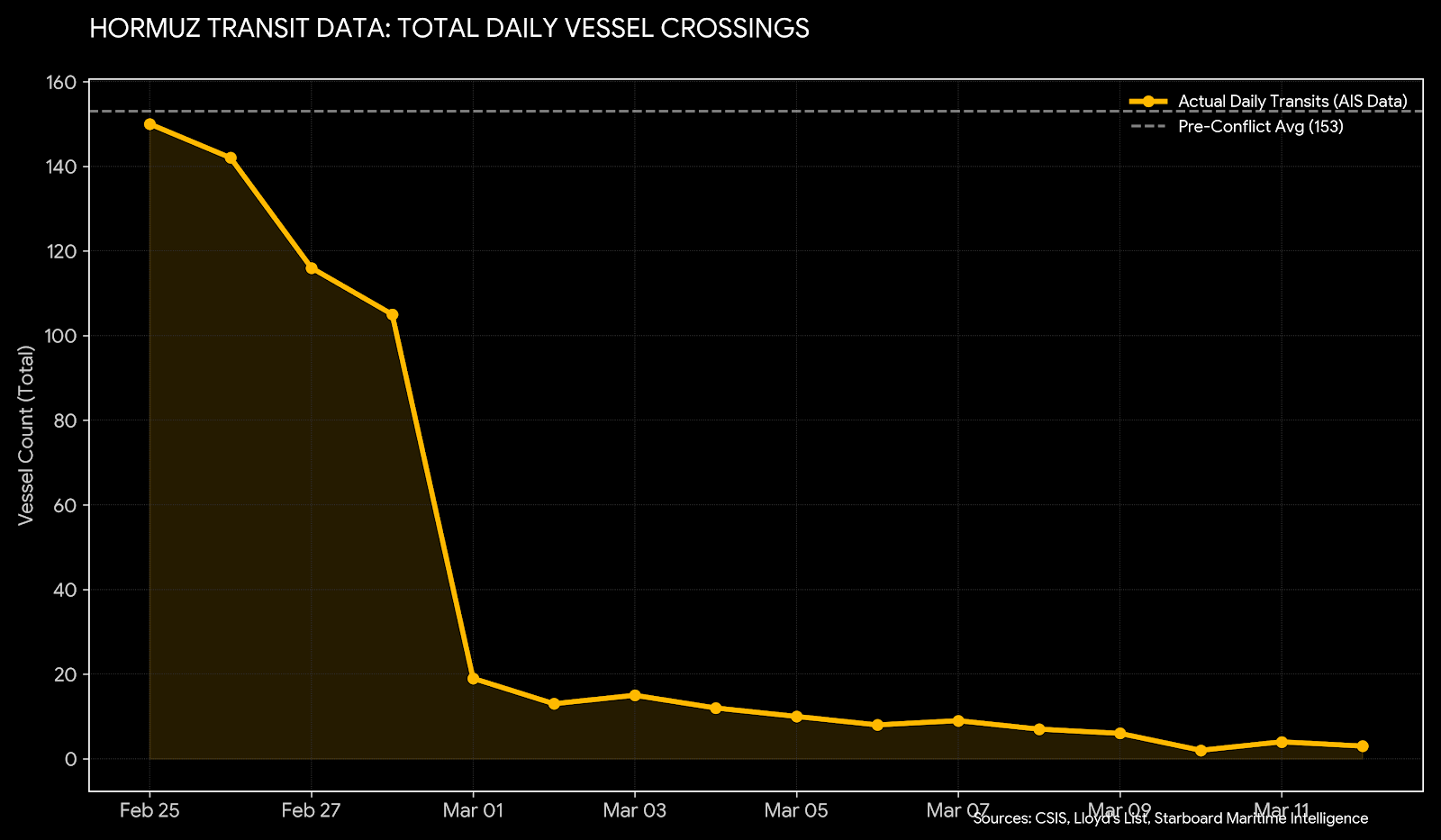

The effective closure of the Strait of Hormuz has paralyzed approximately 20% of the world’s daily oil supply. The halt of roughly 14 million barrels per day (mb/d) has created a structural deficit that the global market cannot currently absorb. As Iranian strikes on regional energy infrastructure remain consistent, and with US or Israeli counter-strikes deepening, tanker transits have plummeted by over 90% since the end of February. With Brent crude testing the $100 to $120 range, the risk premium has evolved into a scarcity premium. Unlike previous shocks, the persistent nature of these strikes means that even if the Strait were declared open, insurance war-risk premiums have reached levels that make commercial transit economically non-viable for most of the global fleet.

(Continued below: A Looming Energy Crisis, Strait of Hormuz Update and Data, Energy Portfolio Strategy - Don, Technical Overview from 30,000 Feet, Global Bubble Gauge Update, Rate Cuts Disappear?, & Portfolio Strategy Update and Commentary from Six)…

Continued below with Ozone.

If this deadlock is not resolved by mid-next week, the lag in the global supply chain will trigger a cascading inflationary shock. The 13-day lead time for SPR releases and the exhaustion of immediate commercial inventories mean that the just-in-time energy model is effectively broken. We are bracing for a scenario where energy-intensive sectors, from petrochemicals to global logistics, face a complete repricing of their input costs. This could force a stagflationary pivot that will redefine the terminal rate path for the remainder of 2026.

The current *effective disruption remains around 14mbpd - the largest supply shock in history.

Another spike of WTI to >120/bbl would put us into a ‘crisis mode’ and above $110, I expect to see the Administration roll out even further interventions, such as a potential export ban (not out of the question right now).

Are commodities… back in style?

(Life of us commodity traders over the next few weeks)...

Strait of Hormuz Update

The Strait of Hormuz remains effectively closed as of the time of this writing (1am EST - 3/13):

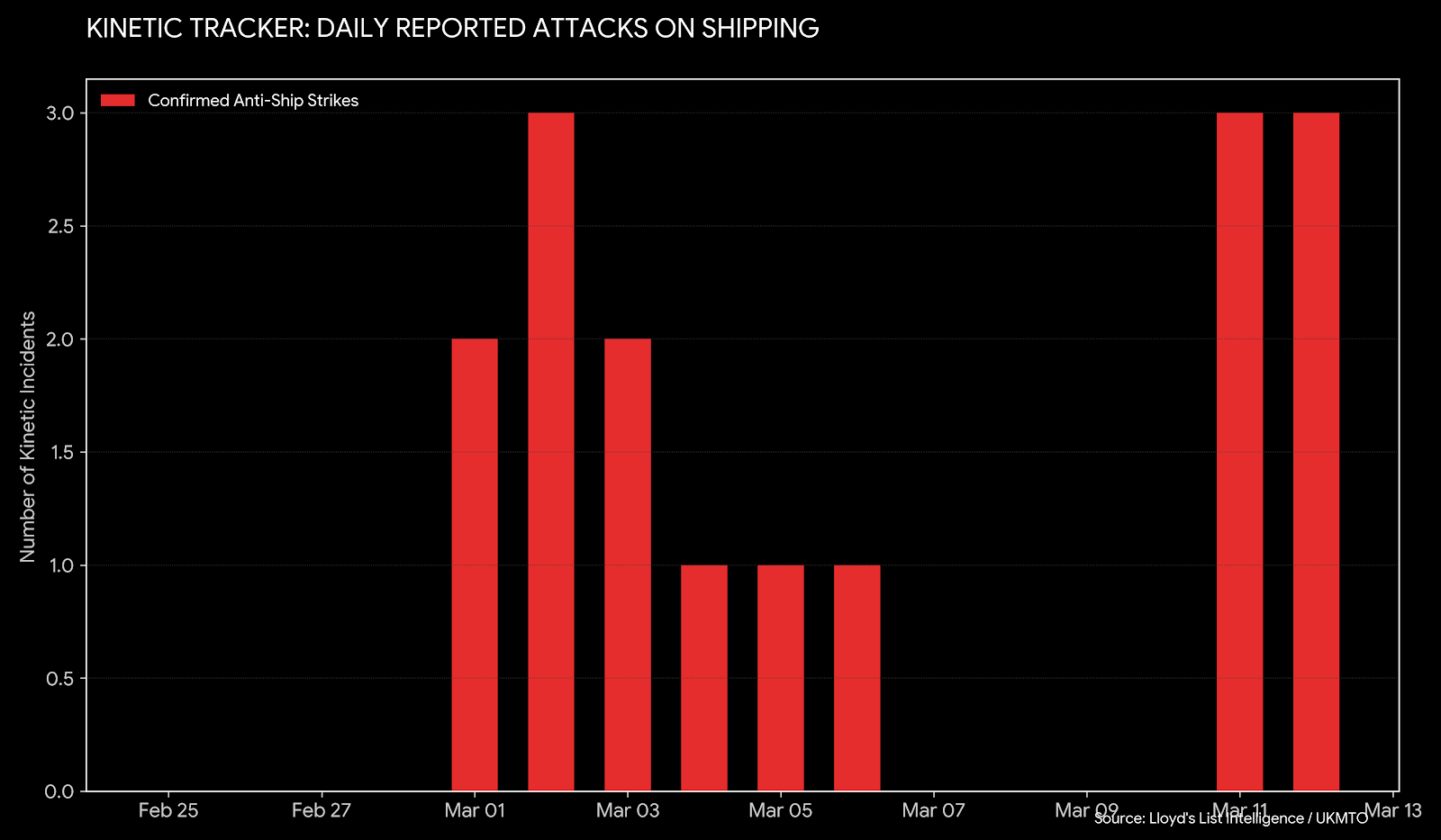

While some crude tankers are passing through the transit (going to India & China) - and that has been confirmed by the Iranian government - traffic remains near zero. Other ships have not fared as well:

Ship attacks have picked up over the last two days, with six occurring amid the US President telling ships to cross and take the risk. For the time being, Iran’s military still has capabilities to keep the Strait largely closed, which means the risk for oil prices is higher.

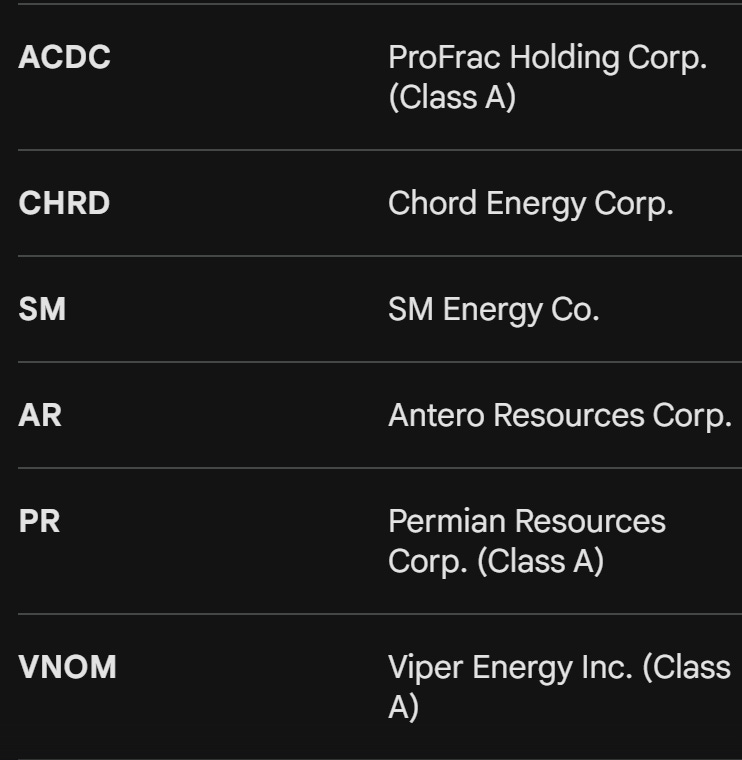

Looking at Our Energy Portfolio Strategy

Our energy portfolio strategy basket has performed very well over the last few weeks. Below are different names that we’ve initiated coverage on over the last several weeks - and from a previous post, if you go into the discussion where we broke down each name individually, you can learn more about why we set up the baskets/weightings the way we did. A new addition from late last week (ProFrac) - ACDC - shot higher from our Monday report, moving about 30% higher at the peak today. Given some of these huge moves in the names we’re choosing - I think that opportunities to enter are coming, though I also expect the sector to perform very well as long as WTI remains >$80bbl over the next several months. Many of the names that we modeled were in scenarios between $40 to $80bbl, and right now we’re pushing almost $100bbl (hence the outsized move in ProFrac).

There are going to be two to three other names that I expand our basket to over the weekend as I perform another deep dive into the space with WTI as elevated as it is, and E&P companies in particular - at least those unhedged - are literally printing money with WTI at these levels… I am going to make a return trip out to West Texas in the next few days on another Economic Advisory engagement - so I will also have another on the ground update for you toward the end of the month. In the Saturday Macro Note, I will provide another update on the technicals for the above name.

Technical Overview - 30,000 Feet

The technicals on the broader equity indices continue to look like a dumpster fire - really no way around that. The distributive pattern we’ve discussed now for the last 4+ months continue to play out, and we’re just churning along sideways, crushing both late longs and early shorts.

The Qs have been sideways now for 175 days:

A big contributor to that has been Nvidia losing momentum… This permanently high plateau that we’re painting is likely to resolve lower at some point, though that won’t be until we have a significant enough ‘macro trigger’ for that to occur. Downside has been largely minimized by an Administration that fiscally has all weapons pointed at any market downside, and steps on the headlines and throttle at any sign of trouble. For the time being, on the Iran situation, they’ve shown that they’re willing to tolerate the high oil and gasoline prices, with interventions, though I expect that if the situation gets dire enough, that too will change. The intervention in crude prices on Sunday night at the $119 level set a signal to traders that this is where a level of discomfort for the major governments becomes too high for them to tolerate, though I think the coordinated SPR release will go down as one of the biggest IEA mistakes that we’ve seen to date as it drives demand higher on the backside.

DIA (Dow) is sagging after the ‘rotator bros’ on Fintwit & CNBC expected their models to pan out:

That has also impacted the Russell (below) while the SPY (two below) is forming a rounded top.

SPY (rounded top)

Other major sectors like hotels and airlines are sagging as well, as air travel has declined on a Y/Y basis through the year thus far, and higher jet fuel prices will dampen profits dramatically until airlines readjust their margins.

Global Bubble Gauge Readings

Our global bubble gauge consists of the KOSPI, Nikkei, IBEX, and TSX. For more on why that is, please revisit our original ‘Global Bubble Gauge’ outline discussing the problems each of these indices faces, respectively.

KOSPI - finally an ‘87’ US or ‘89’ style Japanese chart? The similarities are three:

Both the KOSPI and Nikkei are closely correlated to the US AI trade:

(Green above - US AI trade) still a near 1:1 correlation with the Nikkei since January of last year.

If you think the DAX is the issue in Europe, the IBEX is the fat pig, landing itself in slot three in our bubble gauge:

Notice the similarities (and differences) between the three charts above?

Toronto is also running on borrowed time:

That’s the latest on our Global Bubble Gauge. With some of these indices finally rolling over, we can expect to see broader issues and pressure develop in the global macro landscape.

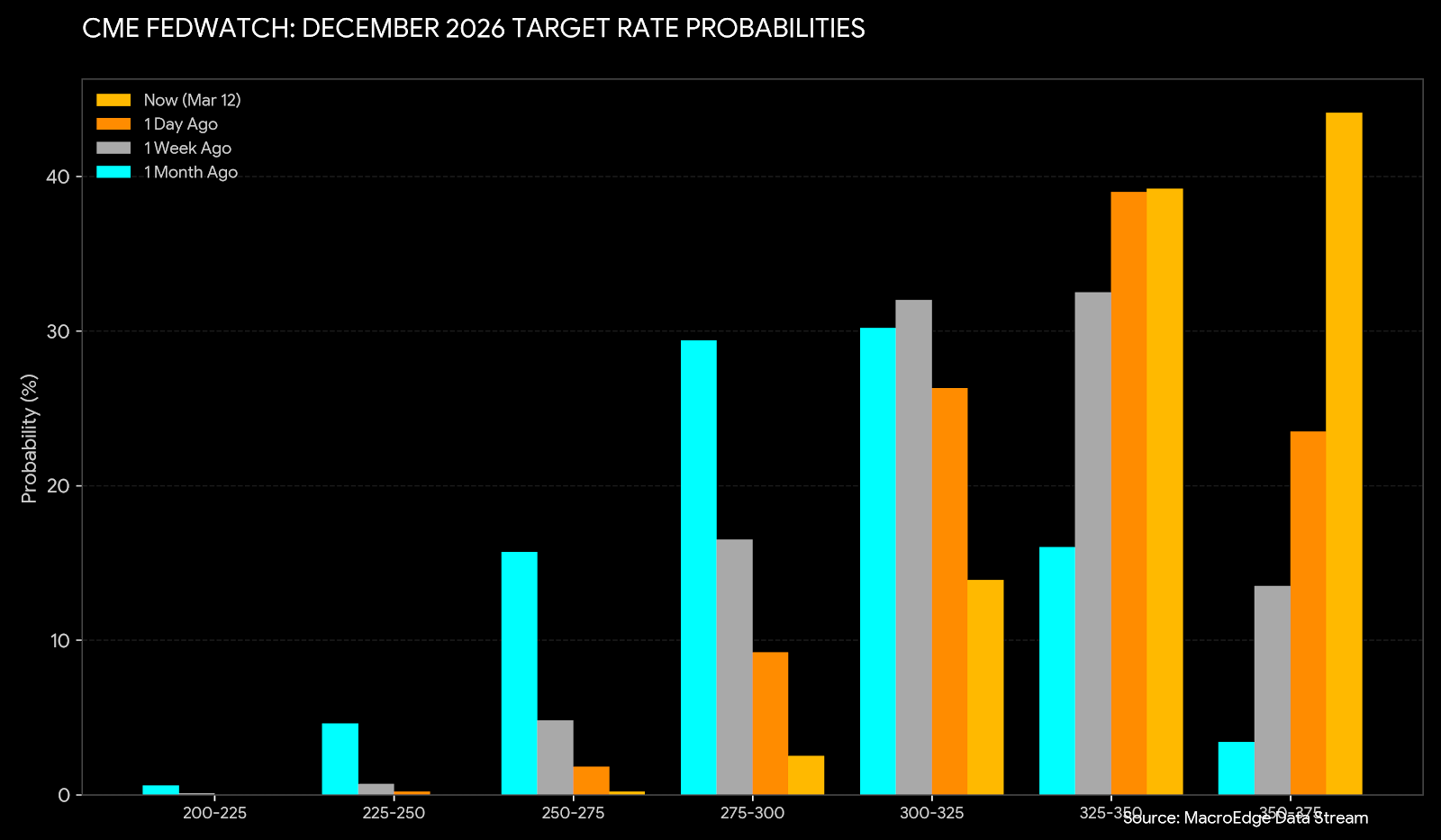

Rate Cuts Disappear?

Rate cuts have almost been fully priced out for the year, with less than one cut fully priced in. The earliest chance has shifted to December, as the market expects the energy price shock to feed into input prices on both the consumer and producer side.

This has been a significant shift from the beginning of the year, and now an energy cost crisis could result in a scenario where we even start pricing back in a hike late in the second half of the year if the price acceleration trends continue.

I hope you have a great Friday and start to your weekend, and I will see you for the next Redeye Macro Note.

– Don

MacroEdge Portfolio Strategy Update - March 12, 2026 (@SixFinance, Head of Research)

Well, the Strait of Hormuz is... still closed. The new Iranian Supreme Leader has done about what we expected: stayed with the recent Iranian regime goal of continuing to drive energy prices up, pulling on their only lever. Until energy crisis fears and private credit redemptions cease being at the top of the Bloomberg headlines each and every day, this is not an environment where I want to be long a lot of risk assets.

This, too, shall pass? Maybe. On the other hand, we have classic late-cycle behavior. Oil prices are aggressively ramping higher on top of an already weak consumer, and credit stress is building within the private credit complex. Redemptions are surging. Private credit default rates are surging. The default rate on Fitch US privately monitored ratings (PMR) hit a new record high in 2025 of 9.2%, up from 8.1% in 2024, with the largest losses concentrated in issuers with EBITDA of $25m or less. Interestingly, for all the fear in the software sector, the private credit technology software sector default rate on a trailing twelve month basis FELL from 7.5% TTM ending January 2025 to 1.9% TTM ending January 2026, per Fitch.

While credit stress builds in the private credit sector and risks spilling over into public high yield markets, the rapidly accelerating supply shock in energy markets seems to be underpriced by risk assets. Two rate cuts have been priced out of the forward curve in as many weeks, and the S&P is down roughly 2% from pre-war levels.

I am currently holding a highly speculative long volatility position, as I see potential for a waterfall in risk assets if this supply shock does not resolve quickly. It is not my base case, but it still feels to me that the market is slow to price in this massive supply shock, and the payoff profile is attractive if that happens. It will depend on whether the administration is able to quickly broker a deal with a regime whose new radicalist leader has just had his father and wife killed in airstrikes. The market is currently about as well hedged as it has been in the last year on a relative basis, so I assign a substantial likelihood to this trade not being profitable. However, it currently is, and the asymmetry is such that I will leave it on, if not hedge it into the weekend.

At the same time, I have begun buying rates today, expressing that by buying the front of the curve (Z7 SOFR Futures - Similar to buying 2-year notes) with leverage. I will continue to accumulate a larger position for as long as rising oil prices remain the primary driver for higher yields. The most recent major supply/demand shocks in investor memory are the covid shocks. The supply shock, resulting from a breakdown in shipping as the pandemic broke out, is similar to that seen today. The major difference in my view is that supply shock was also accompanied by a major demand shock. Massive stimulus was injected into the economy to match the supply shock, driving inflationary growth. In this case, the supply shock is hitting the economy at a time when rates were already well bid going into the beginning of the war. Now, roughly two rate cuts have been priced out of the curve, and the only thing that has changed is that the already weak lower K in the economy is being hit with yet another price shock, dampening demand.

For more details, please refer to our Terms and Conditions.