Midweek Macro Note: A Look at the Macro Data From the Week, An Analysis of Trump v Warsh (Project ZA v AR), Portfolio Strategy Note, and More

In the Midweek Macro Note we take a look at the macro data from the week, we analyze Trump v Warsh (Project ZA v AR), Six provides a portfolio strategy note, and more...

Don Johnson (@DonMiami3), Chief Economist

Good Thursday evening MacroEdge Readers and Community,

This week has turned out to be quite interesting as the Iran-US conflict seems to be heating to a ‘peak fever’. Oil prices are right at the threshold where the President can continue to push, escalation and we’ve seen that over the past 8 or so hours as infrastructure attacks have resumed, and we’re right on the edge of Iran resuming potential energy infrastructure attacks. The war seems to have transitioned from an Israel-Iran war to one almost exclusively between the US and Iran, though the longer this goes (past Sep/Oct), the more likely we are to see it escalate once again.

From a technical standpoint - things are degrading significantly. While Korea (KOSPI) is on a holiday today during market hours, the Nasdaq is below the diamond pattern in the technical setup. These usually retest the downside trendline - and I expect that we will get some kind of TACO on Sunday evening if the war escalates further through tomorrow into the early weekend, which could be a short-term ‘war climax’ per se.

A look at the Nasdaq ‘diamond top’:

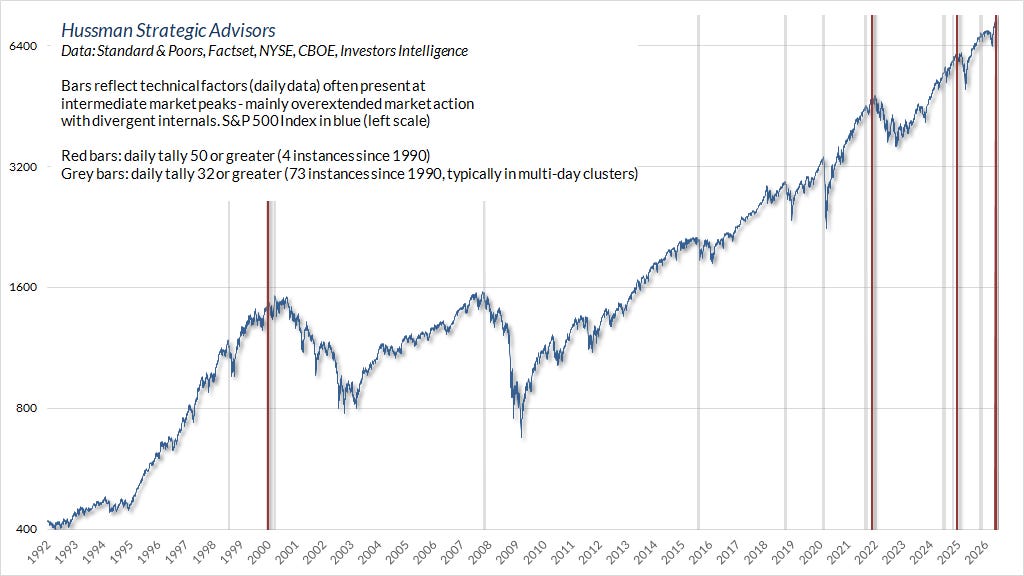

From early June following the triggering of the ‘Motherlode’ technical signal:

Red bars = tally > 50 or greater, 4 instances since 1990

In Korea - the market is on holiday, but the market is at the major parabolic uptrend that resulted in this blowoff move:

I will have more on the technical front tomorrow evening.

What we saw this evening in the press conference was totally uneventful from a market impact standpoint. I continue to see this Administration operate with a myopic view towards the stock market - it is the only measure they care about going into midterms - and I think they continue to have several reserve tools to keep the train at least near the tracks until that period of time. Right now, however, the train is vibrating violently - and the engine of the US economy right now - data center spend, and AI is currently sitting on the verge of a major slowdown come the 4th quarter. While investors may bury their heads in the sand for a period of time on hype, lenders are growing much more wary that data centers are ever going to have any payback (they won’t)

Next Wednesday we will have the second AI and data center report of the year, which you do not want to miss. This is a follow-up to our February and March reports on the state of the AI bubble and data center data. While we privatized much of the data after a wave of publicity earlier in the year, we will once again be making as much data public as possible through Ozone. We’re taking a look at construction status, moratoriums/bans, AI debt risks, things like the Oracle-OpenAI arrangement, and more.

Next Reports on Deck:

Redeye Macro Note - Friday: Reviewing the Close of the Week, Binary Market Outcomes for 2H 2026, Technicals, Asian Review Pt. 4

Saturday Macro Note - Non-Op Oil and Gas Opportunities - Our Partnership for the Future

Sunday - Weekly Macro Note

Next Wednesday: State of the AI Bubble and Data Centers - July 2026

Not yet a MacroEdge paid Ozone subscriber? The time to upgrade and get all of our research, data, portfolio strategy, commentary, and much more - is now:

A Look at the Macro Data from the Week

In Korea, the Bank of Korea hiked rates by 25 basis points amidst a massive market bubble (the worst in Korean history). While financial journalist hacks on X are posting about record low valuations - they’re not factoring that market cap concentration in the key index is just a few names representing >70% of the index. SK Hynix went public on US markets - and others are rushing to now (see chart above):

Upgrade below to continue reading ‘A Look at the Macro Data from the Week,