Midweek Macro Note 11/5: Walking the Superbubble Right into 'Too Big to Fail'

In this Midweek Macro Note - we discuss concerning comments from Nvidia CEO & OpenAI CFOs regarding their 'too big to fail' nature, talk macro data, election results, Hoover, and more.

(@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge Readers and Community,

As I still find myself in Arizona this evening, waiting for a much anticipated return to Florida on Saturday (we’ll see how these DOT flight limitations go…), we’ll continue with our briefer macro note theme this evening for the Midweek Macro Note. It’s of no surprise that the election results yesterday evening trended the way they did based on all of our broad gauges of consumer sentiment, economic happiness, and employment data. You simply cannot run an economy for the 10% forever, without consequence, though it appears the incumbents seem hellbent on doubling down on that while they have another one year stretch to do just that. Unfortunately, when we misconstrue the Frankenstein bubble of today that’s being inflated, with capitalism - as young voters often due - the result is oftentimes socialism and communism - which is a very, very concerning trajectory if these conditions continue to accelerate.

While it may sound like *doom* today, we continue to follow a unique variation of what I’ve dubbed as ‘Project South Africa’ that continues to seem to move just a little bit faster by the way. The problem for the leaders today is that they’ve now enabled the bubble itself to get so large, broad, and intertwined with the actual economy and consumer spending that even a 2% drawdown terrifies them… in the 5% KOSPI / 4% Nikkei drawdown of yesterday - it was all hands on deck at Asian central banks, with leaders saying they were watching closely with ‘grave concern’... similar sentiment was echoed in Switzerland…

Every day the game goes on, we shift more & more towards the rock & a hard place analogy, with the eventual outcome being something Americans shouldn’t desire.

Because of our (and particularly my) pragmatic approach to forecasting at MacroEdge, we continue to correctly see the future. One of the many examples arrived today with the CFO of OpenAI stating that they ‘want federal backstop(s) for new investments’...

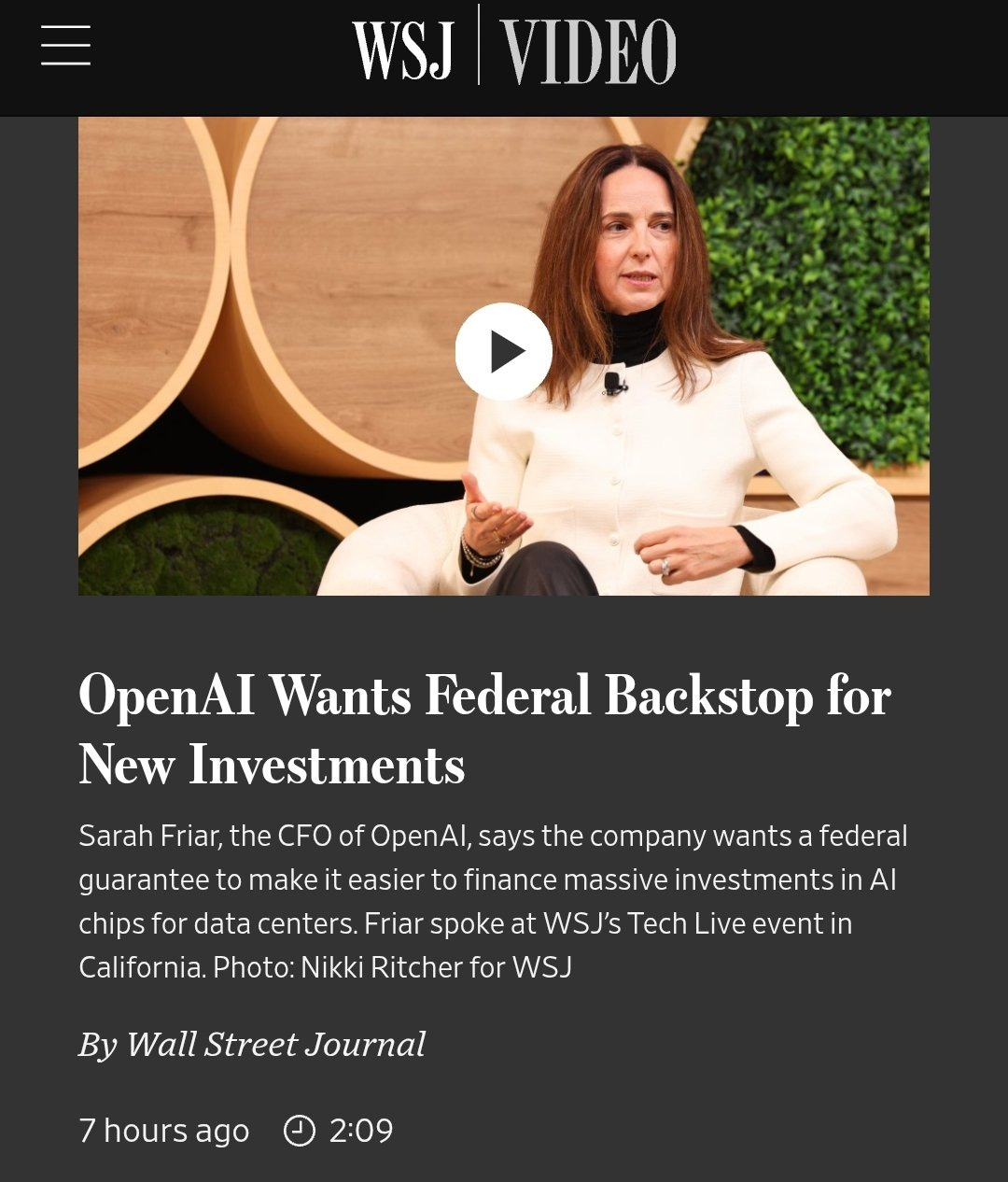

This should concern anyone with investments into data centers and LLMs. If the supposed gold standard, Altman’s cream of the crop, is now backing away from an IPO until they are pre-guaranteed bailouts, why should we trust any of the other companies following the exact same footsteps?

Like most bubbles that run away, this one is now far too progressed and far too big, that the government will again have to decide if they can tackle this national security risk (being the bubble itself) through the gradual deflation of it, or they continue to enable the parade and circus - resulting in far more severe consequences down the line. Maybe the outcome will be much the same as previous responses, in a new era where only a small select few are represented by policymakers, and then we’re left wondering why political outcomes will continue to grow more concerning…

For those thinking a *woke* trend is dead or disappeared, it’s simply hiding in the shadows, waiting to re-emerge with greater vengeance than ever before. With that being said, let’s dive into our brief note.

Macro Data for Rest of Week

We’re likely to see talks start to lift the government shutdown as quality of life for millions becomes impacted, data will resume by the end of month this month or in December - with Trump explicitly calling out the shutdown numerous times today. For the time being, it looks like the card was overplayed, and it hasn’t panned as GOP members were expecting it to.

Ozone Pro - The New Way Forward

We are continuing to release improvements and data additions to Ozone Pro this month, with a more robust live portfolio strategy interface on the way, that we have discussions on with another firm tomorrow.

MacroEdge Ozone Pro is for those looking for a far more in-depth experience than what those with Ozone are getting, including, in my opinion, most importantly - our two portfolio strategies - the MIRP & GMSP.

Get four week access to MacroEdge Ozone Pro, below:

Our Data in the News

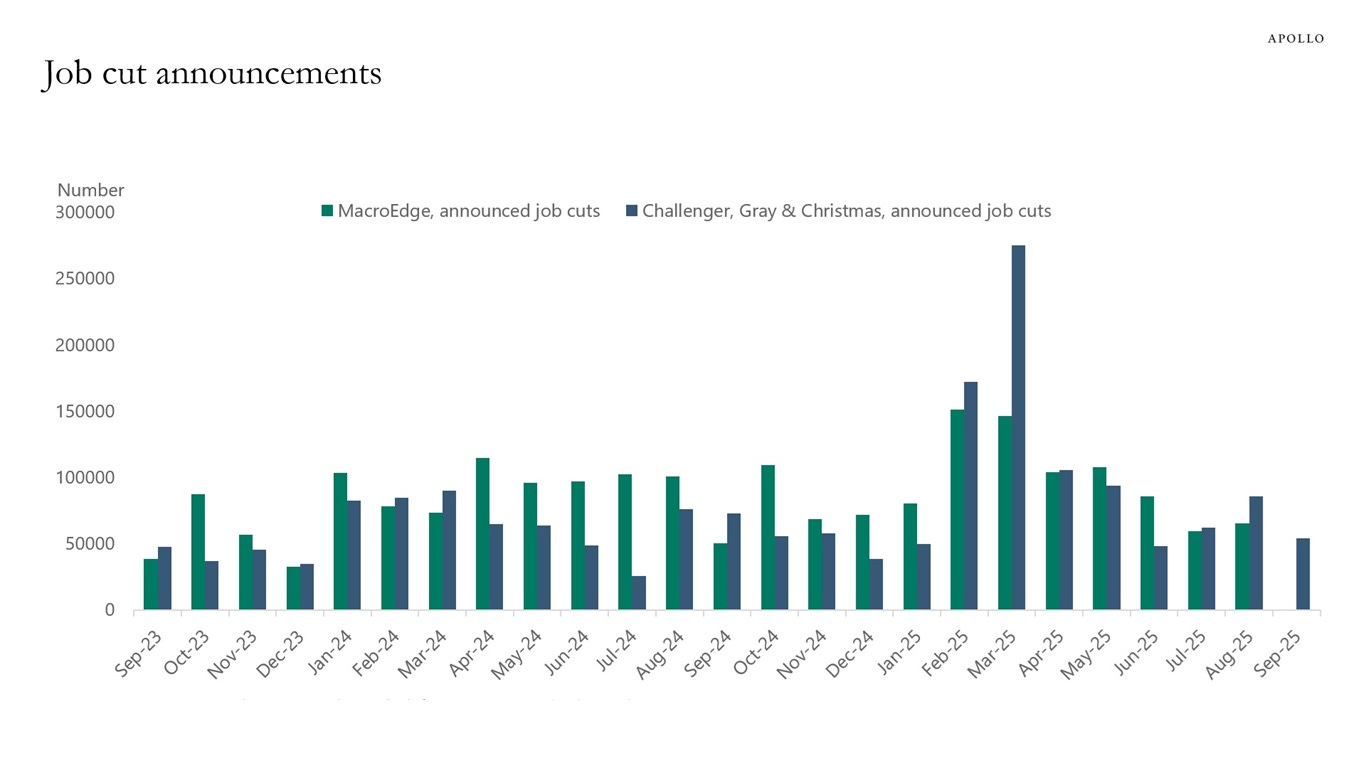

With the government shutdown at the top of mind, and with economists, funds, and companies seeking out alternative (and in our opinion - far more accurate data) we’ve seen MacroEdge data in CNBC, Bloomberg, Fox Business, Apollo over the past week, which is tremendously exciting. Many of these clips will go out on our YouTube page over the next two weeks…

MacroEdge highlighted as alternative labor market data provider by Apollo:

https://www.apolloacademy.com/alternative-labor-market-indicators/

We continue to lay the foundation for something much greater, and as we continue to expand our capabilities, and team, releasing superior research, data, and professional services work to our clients around the globe remains the #1 priority.

Too Big to Fail is Now a Business Model

While I am typically deeply critical & harsh of any business or business model that requires taxpayer dollars or funding, the developments with the comments from both OpenAI and Nvidia today are deeply concerning. Both companies are now framing their operations (and respective bubbles) as too big to fail.

In the case of OpenAI’s CFO, Sarah Friar, signalled that the company is seeking a federal back-stop to make massive AI-infrastructure investments feasible, suggesting the firm already views itself as “too big to fail.” Her remarks that the U.S. government could guarantee financing for data-centres and chip upgrades underscore a shift from private-sector risk to taxpayer exposure. If a private company expects public-sector guarantees to fuel its expansion, it raises serious moral-hazard and competition-policy questions.

Jensen Huang warned that China’s rapid advances in artificial intelligence pose a “national-security risk” and that semiconductor leadership is now a battleground. He emphasized that the U.S. must retain dominance in AI chip manufacturing and ecosystem control to prevent adversaries from gaining a technological foothold. Are the national security risk comments I made from several weeks ago starting to fall into place?

Bubble Talks are Emerging

With the re-emergence of Burry on X - something I expected just 4 weeks ago, the UBS chair warning of similar signals to 2008, and even central bankers warning about these data center financing structures - there’s no shortage of bubble talk.

(Continued below…)

While the smart people generally know what they’re looking at and talking about, since history often rhymes, this should not be a timing instrument. This Administration will stop at nothing to defend Wall Street - especially given the prevalence of the mention of Wall Street of late, and that should be modeled into any left tail scenario.

Technicals are Weak, Globally

The technical picture, which we’ll cover again in much more depth on Friday, continues to look ugly - but requires great patience.

Bitcoin nearing its first monthly ‘sell’ signal on the MacD monthly timeframe since January 2022… and remaining our best real time financial conditions index.

The question of how long they can keep this circus act going is one that we will continue to fiercely contemplate daily. With socialism at the top & now mainstream in our big cities - the defense of capital misallocation and defense of what I’d classify as the ‘mother of all bubbles’, timing with surgical precision will be paramount when in fact we do start to see the house of cards waver…

The Last Possible Week of the Government Shutdown (@RealJohnGaltFla, MacroEdge Contributor)

If one is following these pages for gambling predictions, political predictions (yeah I picked Cuomo while intoxicated last December to win), or even sport wagering odds, please discount everything you are about to read.

However if you would like some in depth analysis of why the government shutdown must end by a specific time period for economic and political reasons, I think from a political-economy projection basis my readers might understand what I am about to project and why.

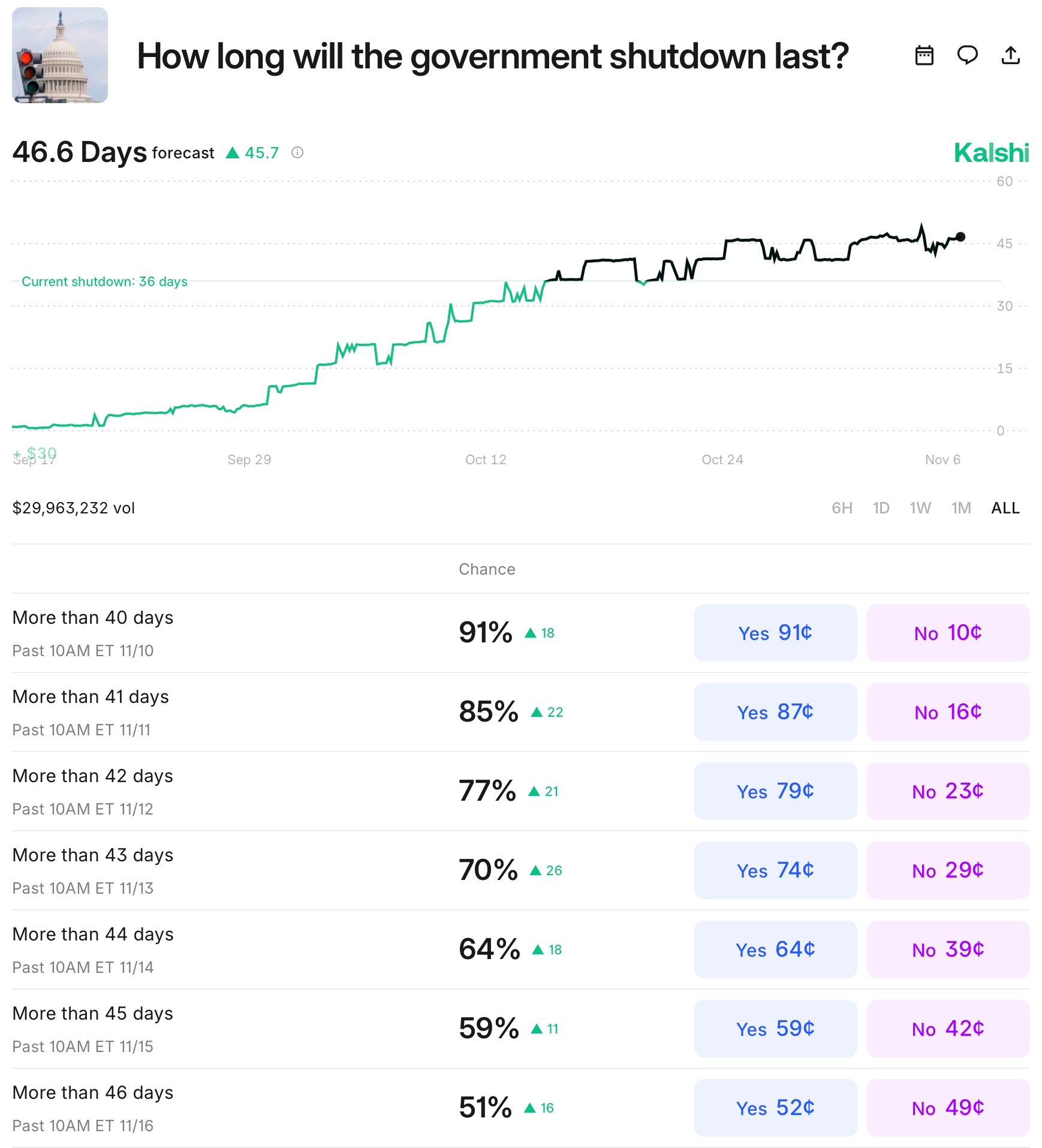

The Kalshi projections for this government shutdown are firmly into a territory which should terrify equity markets and retailers alike:

Kalshi Shutdown Length Market - View Below

Alas, the wagering happy public however is not the last word. Let us take a trip down memory lane, recent and the distant past back to Trump v1.0 to review why this shutdown may last a bit longer than the American public might possibly conceive.

I. Ego

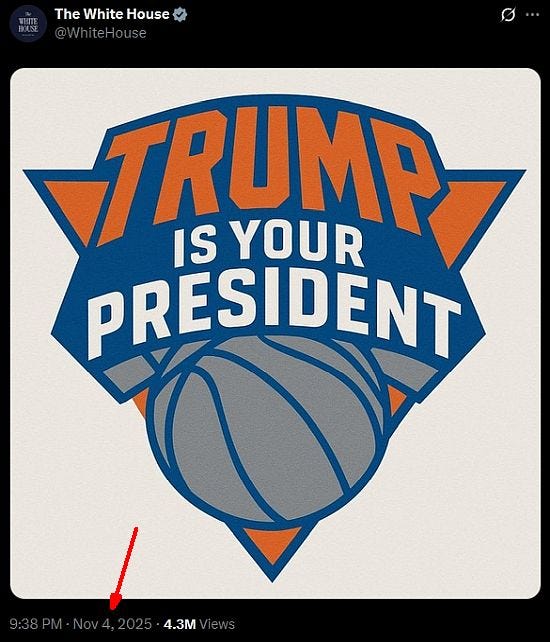

If anyone thinks the election results last night have had left any type of impression on the White House or the GOP leadership, I present to my readers this posting from the White House account on X:

This is not the sign of someone who believes that he’s lost any power nor that the economic circumstances in New York City are going to sway anyone from recognizing his omnipotent presence. What makes this worse is not the when it was posted but the idea that Trump has to remind New Yorker’s that he’s the man and that’s that on the night that they elected a socialist.

Instead of saying it was an isolated situation in a heavily Democrat city and ignoring it, once again the White House had to make it all about President Trump. This does not bode well moving forward as he has been demanding that it’s his way or the highway. To that end, what am I referencing?

Via Politico (subscription required to read entire article):

GOP senators hold firm on filibuster after Trump’s hard sell

This morning during a breakfast meeting with GOP Senators, the President pressed hard to enact the “nuclear option” in the Senate by demanding the end of the filibuster as part of the Senate rules. If one listens to the various business and political talk radio and television programs it was obvious that after last night’s elections, he got some serious push back from the old guard in the Senate.

Thus with the GOP infighting intensifying between the new MAGA wing of the party, the President, and the old guard, look for paralysis in the weeks ahead on a political solution while Democrats relish watching the Republican Party elites fight among themselves.

II. The Stock Market FAFO

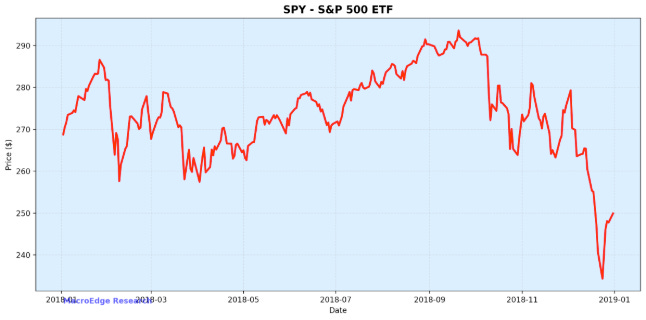

For those “new new” investors to equities, credit, and commodities the idea that the US Government would “f” around and find out seems impossible. But in late 2018 during Trump’s first term, the United States came perilously close to major financial crisis that would have hit the first week of January 2019.

The equity market did not lie and it told a tale of woe that should terrify any sane investor and ask “how could this happen” while the gaslighting business media and political elites gloss over this as “just a gully.”

What happened in December of 2018 is a great reflection of what could happen now if the shutdown situation is left unresolved along with several other issues. To what am I referring to from that era?

I present my readers with a blip from the December 27, 2018 Market$ense section from PBS from which this excerpt might almost sound like a current day repeat to some degree:

But this year a number of other factors outweighed those positive economic indicators. President Donald Trump’s trade war with China, the slowdown in global economic growth and concern that the Federal Reserve was raising interest rates too quickly all contributed to a pessimistic reaction from the stock market. The federal government shutdown that began early Saturday has only added to the anxiety.

Emphasis added by yours truly. But what else created the unease? More from the same article:

Five major tech companies — Facebook, Apple, Amazon, Netflix and Google — make up 11 percent of the S&P 500 index.

When those companies are doing well, they can lift the S&P 500 as a whole, but when they perform poorly, they can drag the index down as well.

Thankfully we have seven this time.

But what happened to scare the living crap out of investors and the world in December of 2018?

Was it really that terrifying though?

According to the NY Times on December 10, 2018, yes:

Are You Ready for the Financial Crisis of 2019?

Excerpt:

For moneyed Americans, most of the past year has felt like 1929 all over again — the fun, bathtub-gin-quaffing, rich-white-people-doing-the-Charleston early part of 1929, not the grim couple of months after the stock market crashed.

Sound familiar?

Of course it does. But what happened in 2018 was extraordinary and the consequences of which impacted individual and corporate investing to this very day.

III. Merry Federal Reserve Christmas

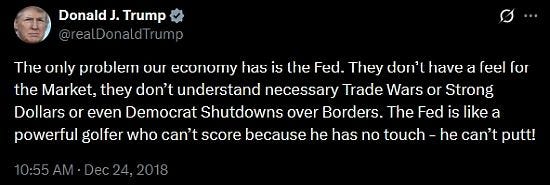

On December 24, 2018, President Trump sent the following “Tweet” out attacking the Fed, let me know if this sounds familiar:

Remember the first part of this, his ego, and why he will never accept responsibility for poor decisions be they political or economic. While many speculate from certain circles that this Tweet is what caused what happened next, the reality was that there was a major liquidity crisis occurring in the US financial system and it was starting to impact the stability of the banking system.

So much so after a dramatic decline in equity markets during the shortened Christmas Eve holiday session, the Federal Reserve “leaked” a move which shocked the world. A non-leak-leak was issued to the financial media that the Fed would be omnipresent and provide liquidity support to markets as their recent FOMC actions should not impact financial markets after minor rate increase adjustments.

The perceived reality is that this was a non-QE Quantitative Easing and the markets took that to heart skyrocketing 5% on December 26, 2018. The truth is that there were were banks running into problems rolling over short and intermediate term debt and liquidity was becoming an issue for the system.

The Federal Reserve glossed over this in the opening assessment in the Tealbook release from January 18, 2019 p. 1 opening statement:

A key question for our projection is how to interpret the financial market movements over the past several months. Among possible interpretations, one is thatfinancial market participants are more attuned to an underlying weakness in the economy than we are, that the nonfinancial indicators we monitor are just lagging behind, and that the prospective slowing in economic activity will be sharper than we are projecting. A second possibility is that financial market participants are only now coming to grips with the idea that waning fiscal and monetary policy stimulus will cause economic activity to decelerate. This second interpretation suggests that a soft landing can be a little bumpy if

not everyone has anticipated it, but it would not suggest a need for a major recalibration of the forecast. We are currently placing more weight on the second interpretation, and our baseline projection reflects that judgment. This assessment is in line with the predictions of near-term GDP growth from statistical models that take into account the conflicting signals from a broad set of financial and nonfinancial variables (see the box “Recent Financial Market Movements and GDP Nowcasting”)

Emphasis once again my own, but one has to scan through the reports to page 51 to find the money line:

Investors’ risk sentiment deteriorated over the early part of the intermeeting

period, spurring increased volatility and declines in the prices for risky assets. Later in the period, however, sentiment turned, and risky asset prices rallied. On net, equity prices ended the period notably higher, supported in part by communications of FOMC participants later in the period that were interpreted as signaling greater flexibility in the conduct of monetary policy in response to adverse macroeconomic or financial market developments.

Emphasis this author’s once again.

Communications you say?

There was no statement, only a leak to the banks and financial media on December 24, 2018 after the market crash and close that day which triggered a 5% rally on December 26, 2018, after the markets being shut down for Christmas Day. This disturbing misstatement of facts is why one invests on the edges, heavily hedged, before a boomerang is created by the Fed and the dangerous idea that all investors are bailed out to ‘save the economy’ is not too outrageous of a theory, despite the inherent risks that lie within this investing strategy.

IV. The Deadline of 2025

Unfortunately for the Federal Reserve, much like 2018, the next FOMC meeting will occur in an environment of a government shutdown, a trade war, and worse, no data to rely on worthy of trusting for accuracy beyond anecdotal and limited regional survey information. This means that whatever statement they produce on December 10th had best be loaded with more details outlining concerns in long term rates, economic conditions, the government shutdown, and the trade war.

A strategic cut and pause would be viewed as extremely bearish while no action, while good for containing future inflation, would be a disaster for risk assets.

This brings this article full circle to the potential and predicted deadline week for the settlement of the government shutdown and why.

With the FOMC meeting on the 9th and 10th weighing heavily, the bigger issues are as follows:

Payroll to government employees to salvage the Christmas shopping season. If the MacroEdge team stays ahead of the game and prescient as always, outside of the top 10-15% of the population, Black Friday and retail sales will probably be far below the inflation adjusted average.

Air travel nightmares during Thanksgiving will pressure DC to resolve the situation before the two week year end Christmas flying season.

Equity markets need an impetus for a massive Santa Claus rally and odds are increasing of a financial accident between now and December 8th where markets are substantially below current levels by upwards of 15% or more.

The Supreme Court will probably wait until the morning of December 12th to release it’s ruling on the validity of IEEPA tariffs and if the letter of the law, not politics, is actually upheld (a novel concept), President Trump’s ability to use this law in the method he has will be overturned. A ruling like this, in sudden coincidence with a ‘deal’ to end the shutdown probably would result in an epic short squeeze.

With Hanukkah starting on December 15th and ending on the 22nd, trading liquidity will thin out and so will the government’s ability to salvage an equity rally before year end.

Trump can claim credit for the deal, whatever it is, and some degree of normalcy will return to economic data, government functions, and a tad of stability for global markets into year end.

Hopefully some sanity returns before that week, but in 2018 there was no sign of relenting until the pain was too severe. Odds are it will take both a horrible Thanksgiving shopping week and shocking market decline to force all parties into a deal this time also.

If this author is correct, look for a massive year end Santa Claus rally providing insiders a chance to engage in distribution and set up the retail bagholders for a massive shock in early 2026.

For more details, please refer to our Terms and Conditions.