Midweek Macro Note 11/12: Macro Review, Government Reopens, Financial Conditions are 'Tighter', Data Pause Continues

In this brief Midweek Macro Note, we lay the foundation for our Ozone Pro report, talk about the latest from Pulte, discuss declining Presidential popularity, the government reopening bill, and more.

(@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge Readers and Community,

This evening I am writing our brief from yet another time zone as I wrap up a two-week travel stint - which has been both rewarding and productive. Markets continue to churn through the week, with some rotation taking place between technology and industrials.

The landscape has been complex during the data blackout, and the announcement today from the White House is that we’re likely to continue to see a delay in data releases until things are figured out at the data collection agencies. It’s also likely that we never see an ounce of the October data - both on the employment and inflation front - and we continue a very concerning shift towards countries that lack accurate information about the state of the economy. Data transparency is not desired by either political party at this time, and as soon as any immediate pain is felt, they continue to pull from the future through the form of near-record deficit spending, the importation of more bodies into the country (a phenomenon referred to as ‘human QE’)

With the absolute priority for the Administration falling into the stock market basket at this point - we continue to face an uphill and complicated picture for where things are going to head. Interventions will remain at an all-time high, and proposals such as the tariff rebate stimulus checks might be considered the ‘new norm’ for the time being - especially as the cyclical sectors remain in trouble. Households are all-in on markets, and this condition creates the unique left-tail risk scenario we frequently discuss.

The government reopening will begin now with the signing of the latest spending package that takes us through the end of January, when they will again have to deliberate on extensions of balloon subsidy programs.

Let’s dive into a quick Midweek Macro Note.

Don’t have MacroEdge Ozone? Get access for two weeks below and transform your economic insights:

Government Reopens

As of the time of this writing, the government will commence reopening imminently. That means things like ATC delays, etc, will begin to clear over the next week and we will be back to the status quo.

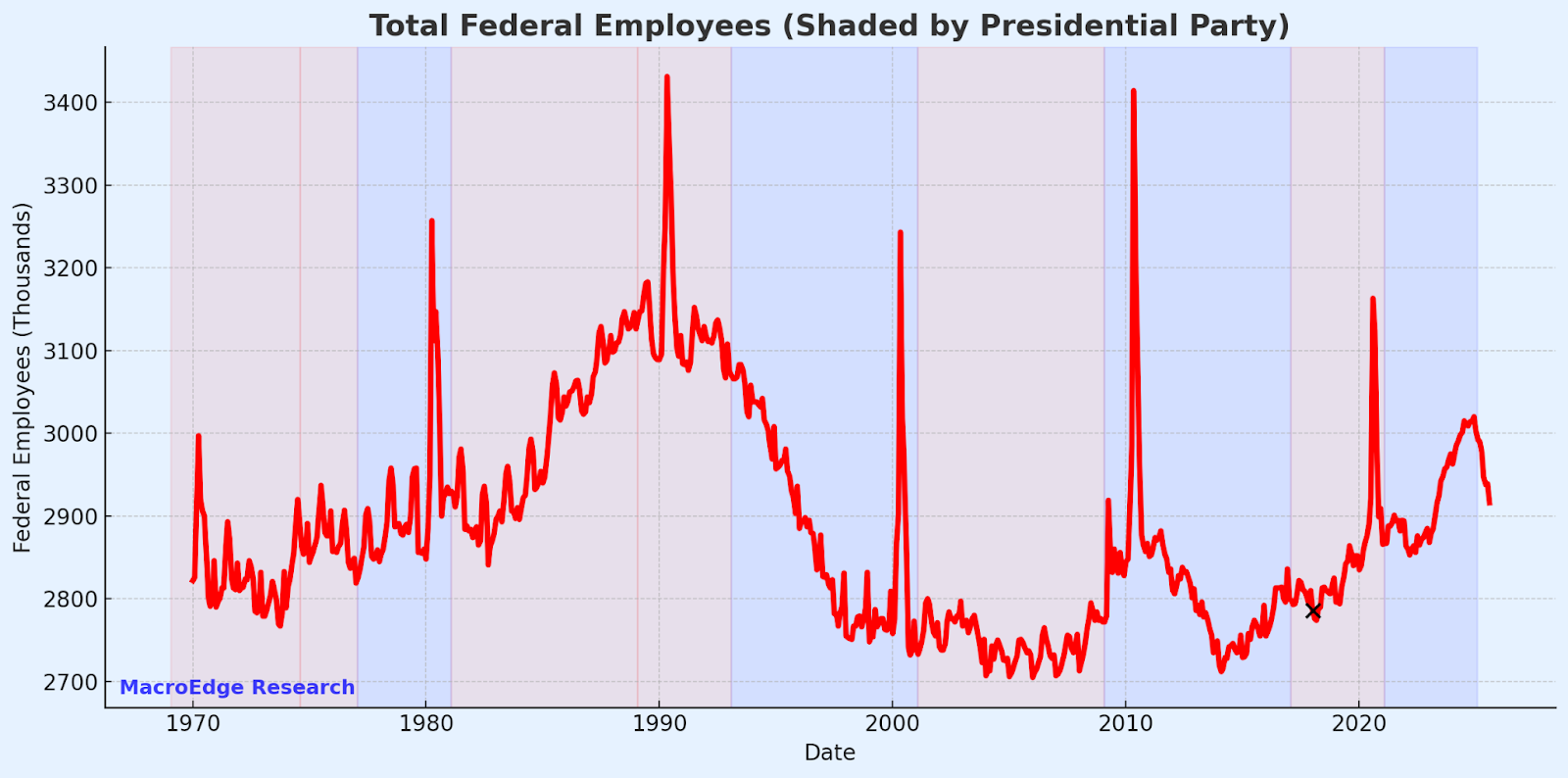

One of the interesting things we should not underweight is the potential for the federal workforce to begin expanding again as we head into 2026. In the first Trump term, there were similar-sized cuts in the early days, and if the economic landscape weakens any further - we could likely see some fear around the federal workforce.

Full Macro Review

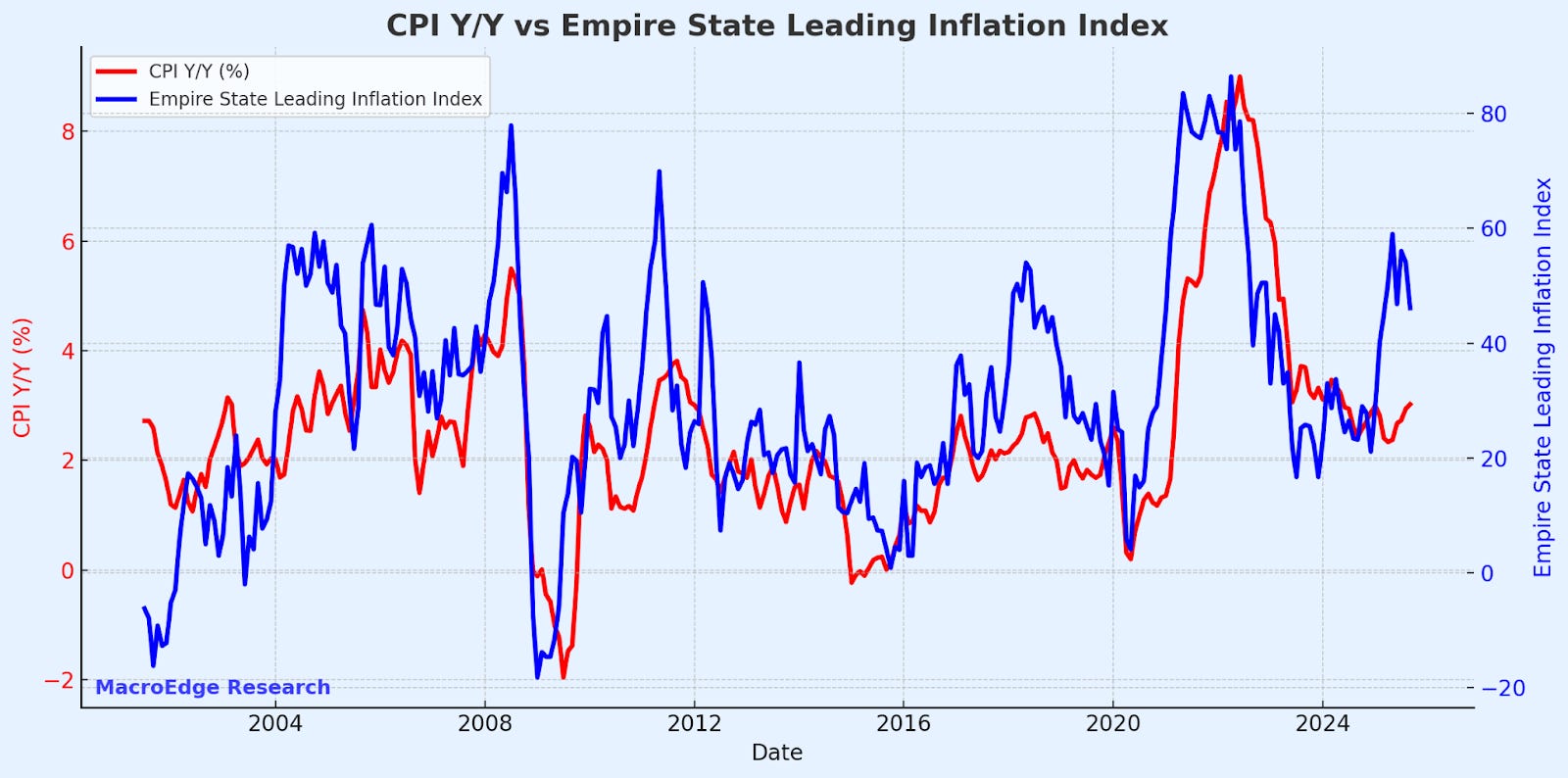

US inflation update ->

Inflation continues to remain sticky, at/near the 3% range. Leading indicators continue to point towards a few decimal points higher here.

US employment update ->

Employment growth in the United States continued to slow dramatically… before (and continues to slow through the data blackout).

US growth update ->

The bulk of growth right now is due to the AI/data center thematic and aggressive government promotion of domestic technology spending. This quasi-private sector growth will not continue indefinitely into the future, and we should expect that the parade ends when investors and funds start to question when they’re ever going to get a return (likely never on 90-95% of these firms).

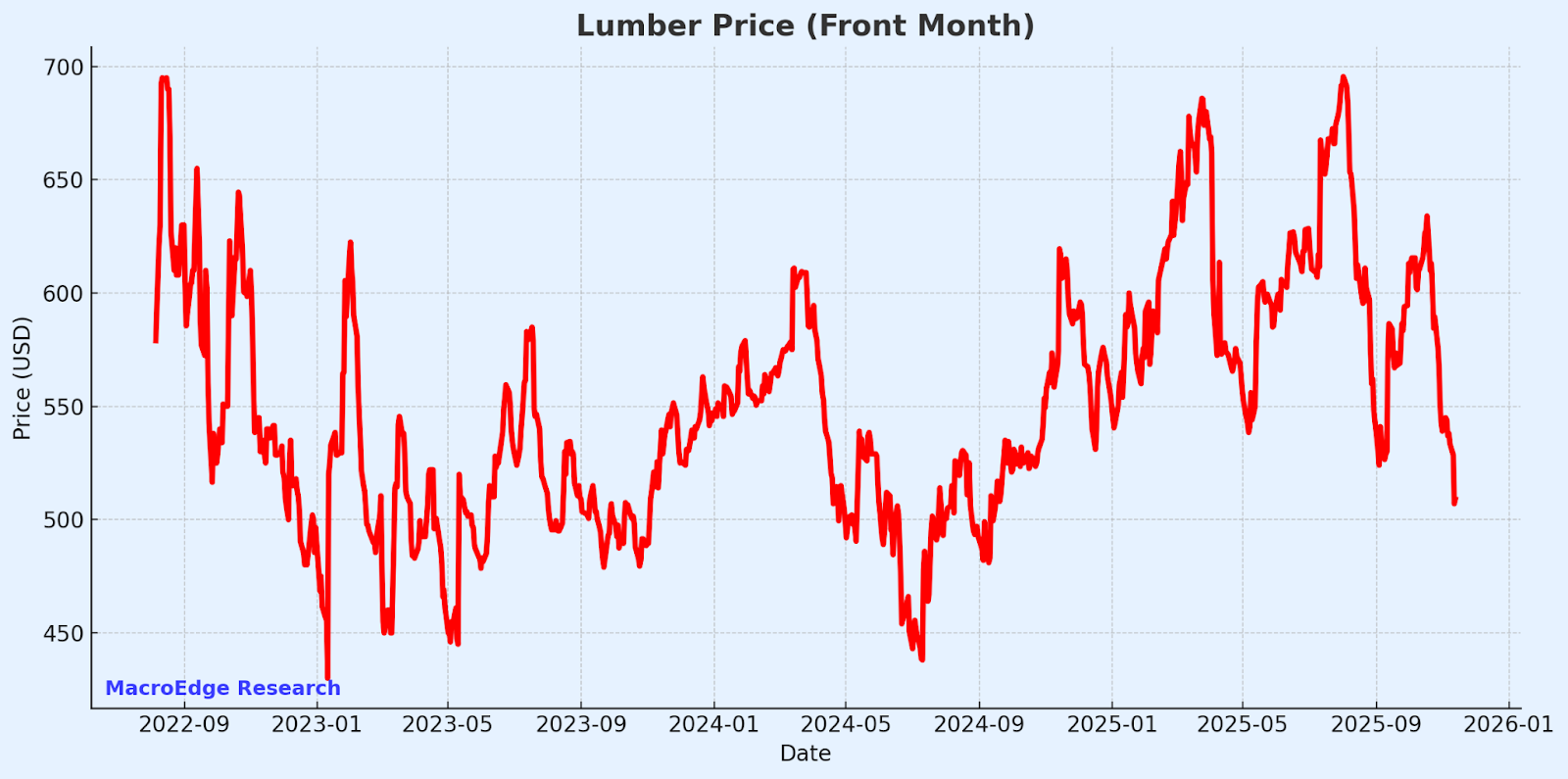

Lumber continues to point to softness in the housing market - particularly in the new home segment:

Gold recovering its all-time high is another macro warning signal - either for inflation or growth:

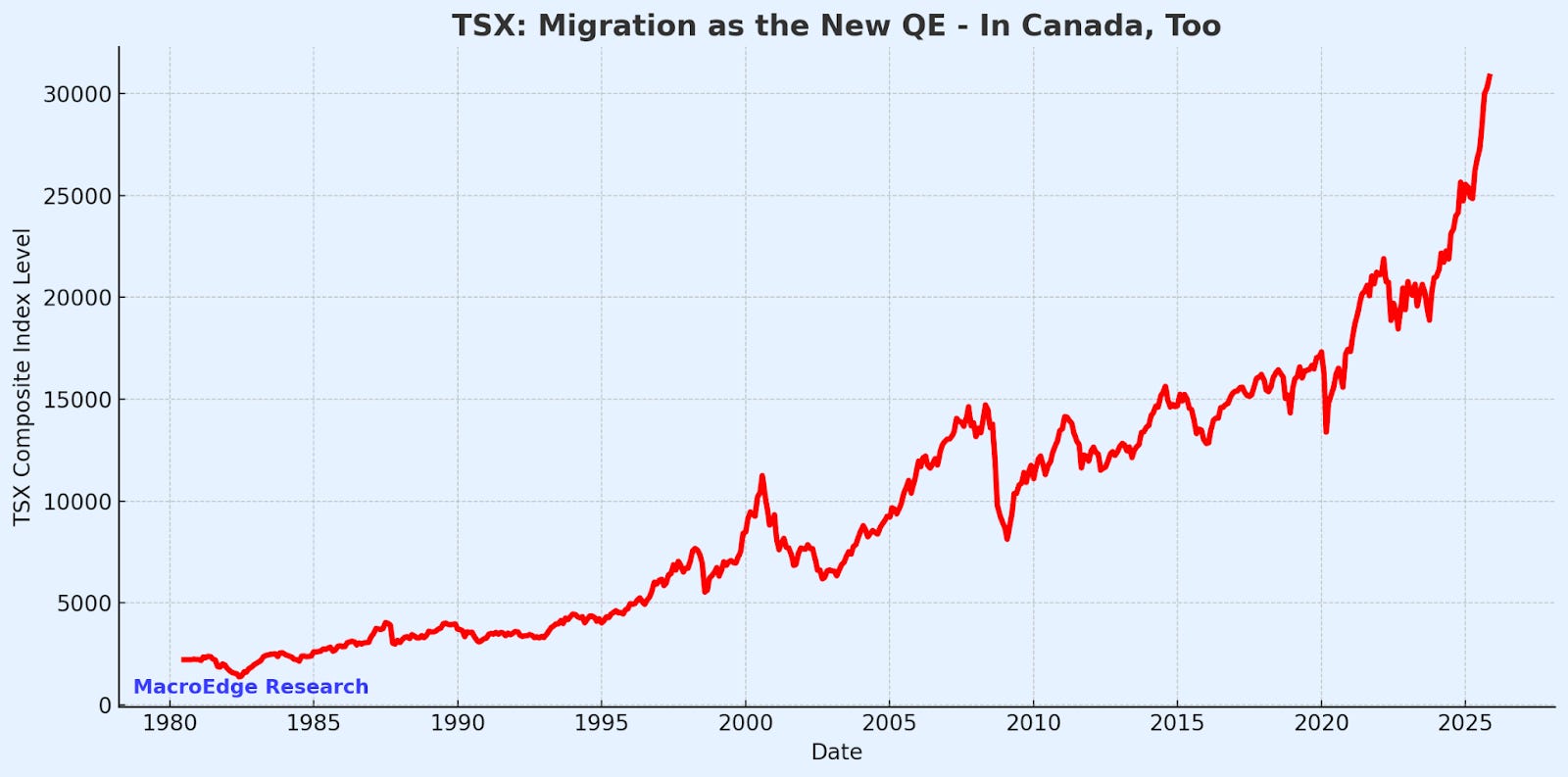

Spain continues to push towards near highs - a continued ‘risk-on’ signal for the United States until this trend reverses:

The index is now at an all-time high, surpassing the previous highs set in 2007. The same story goes for Canada (TSX / S&P):

These two give us a pretty good speculative signal for the US markets.