MacroEdge Redeye: "Staying Objective in Noisy Times and a Rant on the Reality"

*excuse typos on this rant and data deep dive in the latest edition of MacroEdge Redeye: Staying Objective in Noisy Times and a Rant on Reality - Six and Don tackle the latest...

I hope you all are having a great wind down to your March… it is perfect outside right now, not too hot and I am enjoying it thoroughly. Have been on a bit of a hiatus from enjoying some of the finer beverages in life, but some times a break from those things is a luxury in and of itself. It was a busy week on the data side of things with the FOMC presser creating a lot of news, those in the pro-asset price inflation camp telling us to worship a rising Dow like it’s some sort of weird cult, and things like ‘Solana’ tokens continue to make a few market participant success stories at the expense of many. This evening will be a but more of a rant… but I will make sure we’re data heavy always as well… Overall quite a weird week but I consider par for the course for a very weird world that we find ourselves in in 2024. My travel schedule is very light through at least the end of June now (outside of a trip coming up here in a month) so you will be hearing from me often… We find ourselves back in the casino with a whole lot of noise. Even with this noise - we’re continuing full throttle at MacroEdge - tracking the data that matters to you all through all this noise. Today we announced some of our first Ozone V2 features coming live this weekend, including Mint - our news aggregation service, which will be available Sunday. Join the special group of people that we’ve put together and get all of the features of Ozone at:

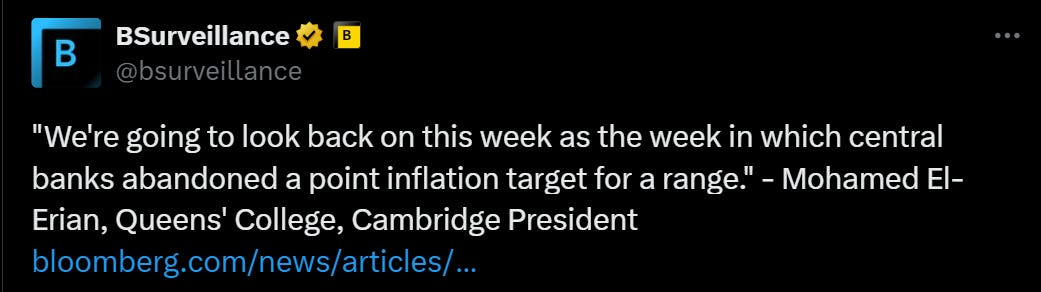

The rhetoric post-Powell’s presser (as well as some of the rhetoric I’ve stumbled across on X and in the financial media) was completely baseless. Just about every ‘permabear’/’doomer’ - or whatever stupid label is getting assigned to anyone not falling in-line with a rosy economic outlook - has capitulated on their previously less-than-positive outlooks… None of this is due to any of the underlying economic data having shifted dramatically, in fact, not much has changed at all in the last several weeks. In the face of a market that has continued to climb higher in this pretty ‘parabolic’ move on things like Initial Claims remaining low and the Conference Board now turning positive (largely due to S&P performance) we know that the Federal Reserve will care most about unemployment rising at this point in the cycle and Powell reiterated that it is something they are watching closely (with his pivot confirmation remarks). With those in the econo/political class beating the drum on prioritizing rising asset prices over price stability (higher inflation for longer) - I believe that this will lead to real problems in the long run if inflation expectations become unanchored thru higher oil prices and (obviously) higher inflation than Americans are expecting. Check out the remarks from El-Erian today from Bloomberg this morning:

“Abandoned a point inflation target for a range” should be quite concerning to most… But there have been many of us expecting that this would happen for some time:

The reality is… Powell announced that they’re ditching their 2% inflation target for whatever 'a ‘range’ means… aka above (higher inflation for longer). This appears to be the case globally as well with the Bank of Mexico beginning cuts and CPI being roughly 4.5%. It’s only a matter of time now before the ECB/RBC/RBNZ/RBA follow suit with the ‘higher inflation range forever’ policy as their near inflation target baseline.

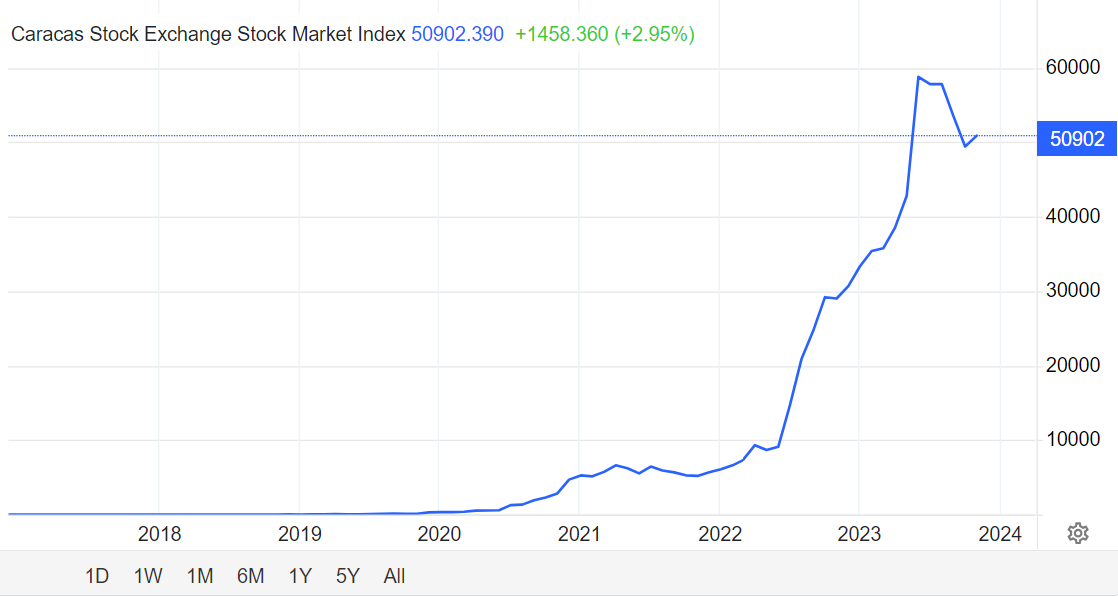

Pundits and experts alike continue to be baffled why the everyday W2-American is the most pessimistic that they’ve ever been on the economy and that’s because most of these pundits and experts are 50,000 miles detached from the reality of the everyday experience that most Americans have when they go a trip to the grocery store (where it’s $300 to feed a family of 4), a stop at the pump (to see that prices have again risen by 20-30% in most states), paying property and home insurance that has run out of control relative to the baseline CPI increase they cite… the list really goes on and on here. My point is - when these people attempt to make a point - they show their true colors and ignorance. Some on X like Ryan Detrick (with his honorary CMT badge) wonder why Americans are unhappy that the Dow hit 40,000 - roughly half of America doesn’t even half exposure to the equity market itself. He also wondered why CPI mattered anymore given the fact that ~60% of us have fixed rate debt on cost of living expenses (tell that to those of experiencing huge home insurance premium shocks, property tax increases, et al.). There are countless examples of countries that have prioritized the value of paper assets against their long term future and that certainly hasn’t ended up well throughout history. This isn’t a ‘doomer’ point as some pea-brains may call it on whatever platform of choice you choose to engage with people on, it’s reality. The pathway we are on as a country is not only completely irresponsible, it’s completely unsustainable in the long run and we should be very cautious of celebrating rising asset prices in the case of hundreds of other issues resulting in said asset price increases… From 30,000 feet you might think this is a country with a thriving stock market, but this is the performance of Venezuela’s stock exchange since 2018, up 500% in nominal terms… I wonder why the people of Venezuela are not celebrating in the streets at their new found paper riches

(Why are the poors pissed?!)… On things like housing, rent, etc… we’re headed in a very wrong direction. Incomes are only marginally higher than pre-lockdown money printing in real terms and the cost of everything else is up 50-200%. This doesn’t pen for America and neither does a new absurd ‘inflation range’ to justify permanently higher acceptable rates of inflation in light of this:

Back to rising assets here in the US, the pivot in December provided that runway, the pivot this time in my eyes is one of a different nature. Can asset prices continue to rise? Of course, and they have in other cycles and in other countries. Powell is attempting a ‘95/19’ early pivot repeat here with conditions worse for a broader swathe of the population which is why I don’t think it will pan out, even in the wake of approaching being the longest inversion following inversion of the 10y3m curve on record. With that being said and with my short rant about the nonsense label of ‘doomer’ (which is a intellectual cheap shot at best by low IQ individuals) out of the way - let’s dive into the data.

Rising Asset Prices

Asset prices have been on a tear since December (largely, across the board)… Commodities and oil have joined the fray as well. Whether the former comes to the halt (the ‘techquity’) market or not remains to be seen, but in my view a lot of this will come down to the labor market (see below). Don’t discount that chart two charts above though as the reckless and feckless individuals in Congress deficit spend like there is no tomorrow during an election year.

Inflation

While economists and pundits obsess over over whether the ‘Supercore’ is this or Inflation minus food, medical treatment, car expenses, insurance, fuel, and housing is dropping below a 2% threshold, most are facing this reality of inflation:

The path of the last 3 years is a new trendline being established backing the ‘higher inflation forever’ narrative with our current permanent deifict regime in place on the fiscal side of things and the new ‘inflation range’ laid out bare by El-Erian this morning.

We’re winning! As they tell us…

The United States was able to put makeup over its pig-like inflationary problems following the last wave of explosive inflationary y/y CPI growth back in the 80s but the cat came out of the hat in 2020 after we were told that MMT would work out well for us and inflation was just a transitory phenomena. A higher inflation ‘range’ doesn’t look like a very positive trend!

Has inflation found the bottom at a permanently higher baseline (>3%?) - that remains to be seen, but both Congress and the Fed alike seem committed to making it our new reality.

Unemployment Currently, Past Unemployment Cycles

Claims are low - yes, unemployment is still low at 3.9% (U3) - quite low, yes, but rising, U6 - rising, and as I highlighted this week (along with our Unemployment Index post 10Y3M inversion) - the largest increases in unemployment follow the Fed unwinding high rates which means at maximum employment that the largest risks are ahead for labor, not behind us:

& current cycle by 10y3m inversion (from Eric at EPB Research):

The current cycle is unprecedented in that you have fiscal policy and monetary policy actively working against each other while the Federal Reserve is attempting to lower inflation through higher rates…

With all that said and me needing to actually sit down at the restaurant… I leave you with that data for now, and let’s continue to focus on the ‘signal from the noise’..

Good evening everyone, great to be back. I missed you all this Sunday nursing a combined 103 fever from the actual flu, as well as a case of the post St. Patrick’s day flu. The ENPH short played out swimmingly last week, from a Monday open at ~130, to a Friday close ~107.

For this week’s Redeye i’ll keep it light, with a more comprehensive alpha drop this sunday, how I’m positioned.

FOMC was a bit of a hot mess this week. Powell had the opportunity to push back on financial conditions and the recent hot inflation prints, and instead was accommodative to the rate cut planned 3 cuts. Powell continued by announcing that QT is soon to come, which gave the market continued lift. When asked about the recent hot inflation data, Powell mentioned 1H inflation typically being hotter, and said the numbers did not instill additional confidence. He did not give those numbers enough credibility to warrant a further hawkish stance as of yet. Powell’s comments largely danced around his and the FOMC’s clearly observable bias to cut rates. Further hot inflation data points may tell a different story however.

My honest late-night thoughts after these last few weeks are that this equity market pricing is buoyed on dreams, but the price is the price, and if you’re on the wrong side of it, you’re wrong. That being said, not even during COVID-19, when the Fed was buying $100b per month in Treasury and Corporate bonds, did we see such a steep and steady ascent with essentially nonexistent pullbacks. What keeps me up at night is pondering whether this market bid is a bet on a “soft landing” or a bet on a dovish Fed/Treasury duo who will allow inflation to run above trend while dumping “Fiscal QE” into the markets in the form of deficit spending, or some of each.

Regardless of reasoning, the price is the price, and the trend is up. With the QT taper coming into more imminent focus for the Fed, especially with the Reverse Repo Facility down from a ~$2.4t level to ~$400b level, liquidity management is becoming a more imminent priority to the Fed. In light of this, as well as the affirmation of the same 3 rate cuts, inflation sensitive assets could be poised to do well in the immediate term, at least until next month when we get our next suite of inflation data. Crude oil futures put in a YTD high on Tuesday, briefly breaching 83 handle. A break of ~$80 support would leave me on the sidelines, while a hold and bounce on this level would get me interested in more upside.

MacroEdge is a reader-supported publication. To receive new posts and support our work, consider becoming a free or paid subscriber.