MacroEdge Redeye: Spring Break Rolls On... For Some, Jobs Data, Revisions, and More

No plane travel for Don this week, John gives us an update on the market 'weather' and we dive head first into the data... grab your beverage of choice and let's get right into it.

In this edition of the Redeye report - I finally don’t have to share some important data with you all from my mobile or some mediocre AAL Wifi (seriously… only one carrier with Starlink right now and that’s JSX). Having a Gatorade this evening and have been generally taking a break from the intraweek beverage enjoyment with much of my time spent elsewhere currently… Trying to of course observe the ‘Spring Break’ activities as well from afar.

This week we saw an interesting shift in some of the reactions towards inflation, labor, and economic data as the wheels of the economy continue to turn in different directions. John will talk about the markets and I will briefly cover some of the economic data released today, yesterday, and earlier in the week… One of the key risks here remains the Fed failing to quash inflation with a hot PPI read, and yields began to advance higher again (especially on the long end) which was initially positively received by markets which shifted sharply yesterday and today. Going to keep things a bit shorter tonight since it’s been a long week on my end and I have a long update coming in the Sunday weekly Ozone report… you can get these by joining us:

Hopping right into the data. One question remains and was posed by Dr. Estrella… did a recession begin in December 2023?

This question is even more relevant given the information we have now on the Household data being much closer to reality than the BLS nonsense being released time after time and revised lower. If construction employment and state-level data begins to weaken, then odds will increase that the official *employment* downturn began in December. In Canada and elsewhere, unemployment has also begun increasing at a brisk pace (certainly faster than our national U-3 figure right now)… For employment though, the trend is not the ‘bulls’ friend…

On industrial production, January’s # was revised sharply lower and then Feb was posted as a ‘gain’:

Capacity utilization also fell again and was revised lower:

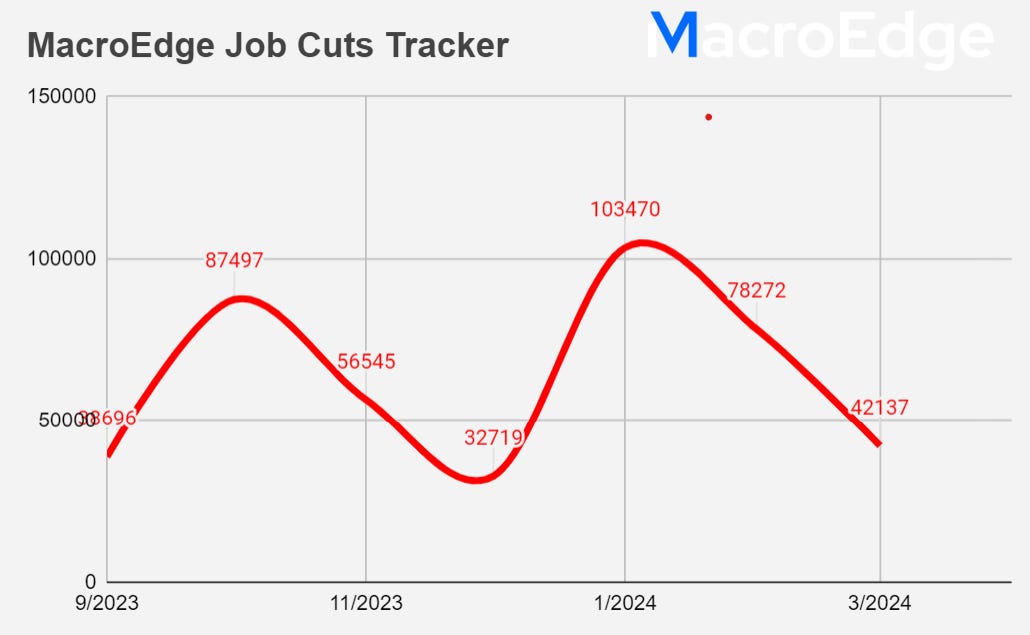

Job cuts remain somewhat elevated this month, although April/May could see further labor market weakness if the market sees impact (particularly in tech):

On rate cuts… everyone is watching the Fed, and for now there’s likely to be no cuts until they see labor market data weaken further… (bear in mind they did pivot in December)… Risks abound in the labor market + equity bubble and that will continue to be the target of much of my focus in the next two quarters to come.

That’s all for tonight’s brief update on some important data this week that helps round out the bigger picture. Hope it helps and have a great start to your weekend.

See you Sunday,

Don

p.s: to those saying the labor market is ‘tight’ - look at the data:

Weekly Market Review: A Weather Change (@Real JohnGaltFla, MacroEdge Contributor)

For those of my readers not familiar with this time of year in Florida, it is not only spring break where traffic becomes an infernal hell, but also when the annual hurricane forecasts start to get published. In fact, I dug up an old photo (above) from 2008 about the “eye of the storm” to illustrate where our nation is now, as then, as far as the markets and economy pertains to this bizarre reality we are in.

Hurray, uh, sort of.

Needless to say, we can not build underground bunkers, but if we could this author would based on the early forecasts from some of my favorite meteorologists.

Is this weather change that is upcoming indicative of bigger problems? Probably.

Much like the weather change from winter to spring and the violence which sometimes is felt by the markets. Especially after a mild winter with an overly ebullient market period of speculation, AInsanity, and stupidity based on political and media propaganda.

This was a key day in the markets with option expiration and quad-witching which increases market instability in both up and downdraft days. The markets this week and today were no exception. Before we begin however, let’s review the terminology for any new readers.

If one is unfamiliar with the “quad witching” day, here is the official definition from Investopedia:

Triple- and quadruple-witching days occur when three or four of the following expire: stock index futures, stock index options, single-stock options, and options on stock index futures. Triple witching happens four times per year, but quadruple witching is rare. The concentration of expiring contracts on these dates can catalyze higher market volatility and heavy trading volumes.

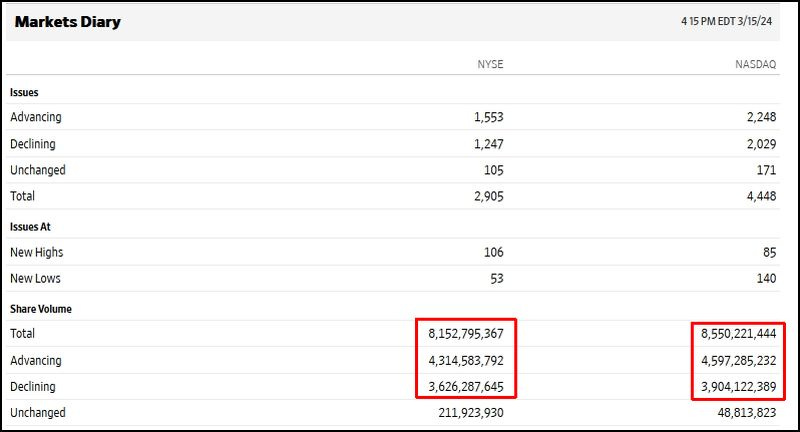

Today, needless to say, was another eye opener. Ignore the price action and check out the volume levels (via the Wall Street Journal Market Data page):

Massive volume, mixed results for up/down volume and issues. Add in a bizarre twist of downgrades, warnings, and hints of management incompetence at some of America’s largest, most valued companies and it truly made for a day to behold; potentially historically as a marker.

The NYSE, one of the broadest indexes finished on a daily basis with a somewhat auspicious pattern at the close:

Not good, not terrible, but potentially a short term game changer. A decline to the 21 then 50 DMA is not out of the question here.

The weekly chart however is somewhat more ominous:

In “technical” parlance, that could easily be read as a shooting star, and if so a major downtrend could emerge in the weeks ahead.

The NASDAQ Composite is not too terribly different either:

A break below the 50 day moving average (DMA) means that 13,000 is easily open and a normal 20% correction is probably in the cards.

Why is this “convenient” for the bulls?

A 20% correction before Memorial Day, remember “sell in May and go away,” along with the layoffs and credit availability contraction (as predicted by these pages), would provide the cover for the Federal Reserve to initiate one more speculative frenzy into the election period and allow insiders to liquidate their dogs before a real bear market and potential stagflationary recession takes hold.

Stay nimble, know what limits of risk one can undertake, and enjoy the show.

The next ten months will be of such historical importance, both in markets, politically, and internationally, that few will understand the long term implications.

Profit from it now, while one can.