MacroEdge Redeye: Macro Update, Inflation, Technicals, What's Next for RESights

An update on MacroEdge RESights, the macro situation to start 2025 - including employment and inflation, and the broader market technicals.

Good Friday evening MacroEdge Readers and Community,

This evening I’m bringing a brief update to you all - still from Texas - before heading off towards Arizona and then Montana in the next few days as we advance our plans for RESights. It’s been a great start to 2025 for our team - RESights is off and running - and we’re going to be building out all of our core divisions here to start the year, including Vision, our Macro team - led by myself, and Intel - which will be our new service line offering our team resources - it’s going to be a great year. MacroEdge now includes RESights, Vision (Investment Research), Macro, & our service offerings for Ozone & enterprise subscribers. Our first half of the year priorities are to expand our RESights infrastructure, bolster our readership, and improve our current product offerings. We expect to add LuxePulse and Trident to our belt this year if our trajectory continues. All around - very exciting things and progress for our organization.

Whether it be a smaller community bank needing a full outsourced research arm, or data warehousing for real estate enterprise data projects, we’re going to be doing it all in 2025. If your company has a gap, get in touch with our team and see how we can do for you.

A special shoutout to John Galt on his very accurate employment forecast for today (unemployment down, payrolls hot), and the continued accuracy of our team across the board has been fantastic. From RESights to Vision, we’re putting accuracy and data at the forefront of everything we do. You can read much more from them with MacroEdge Ozone - where our insights are delivered weekly, & sometimes more - spanning our areas of expertise:

With all that being said, we’re going to introduce our two RESights pilot cities by the end of the month, and hope to have data coverage initiated before the turn of Q1 at the end of March. If successful, we’re going to expand the markets covered by RESights - and will add one market every month or so from that point until we bolster our resources for further data coverage. All in all, exciting things to report on.

…Jumping into the macro. The real point of this note outside of delivering a note is discussing the what of what’s going on to kick off the 2025 year in markets. Thus far, it’s been a rocky start to 2025. The Nasdaq (and semiconductors in particular, which I’ve harped about since August) - gave up the last 6 months of gains again, pushing them back to July 2024 levels.

The Macro: Employment and Inflation

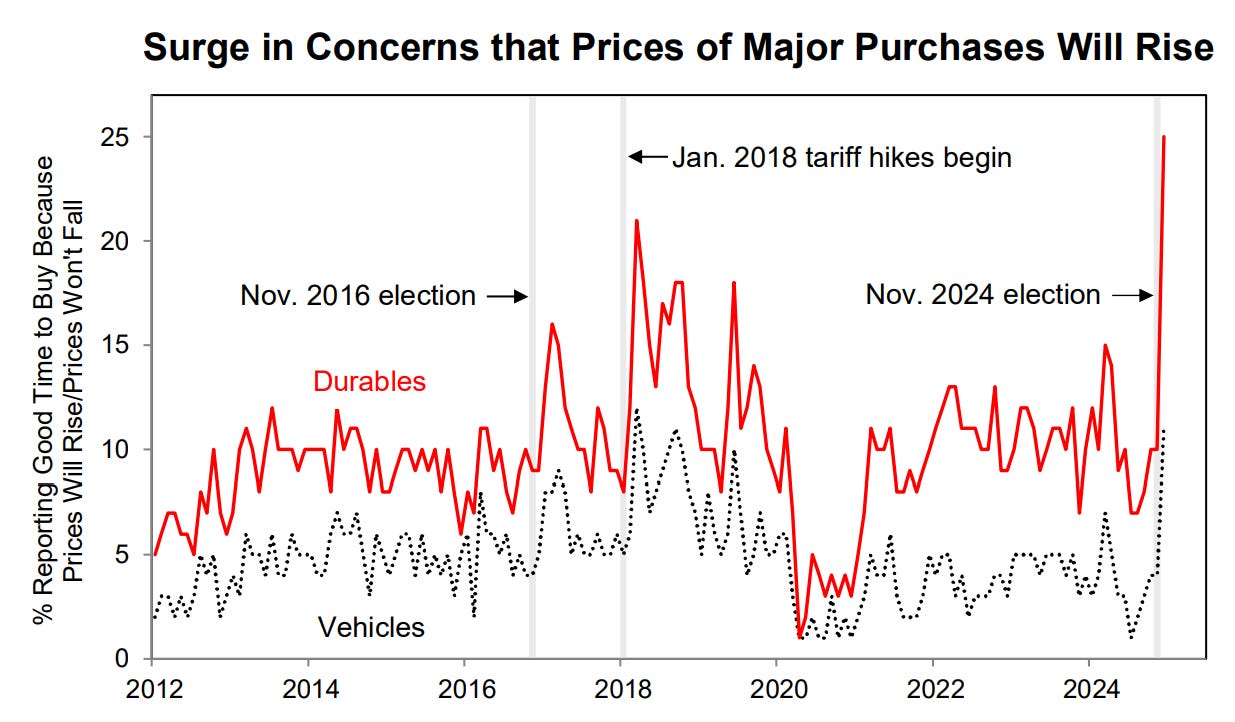

While we’ll cover much more in our Monthly Labor Market Report for December, the risk has again tilted back towards inflation after the December employment report came in hotter than expected. Adding the cherry on top of the UMich 1-Year Inflation Expectations ticking up to 3.3%. The Fed and policy errors over the last several months have now created a new risk storm of hot data, rising inflation signals - resulting in higher yields - which will likely slow the cyclical areas of the sector of the economy further. While I anticipate the December payrolls report to see negative revisions (as October and November saw more of) - sectors like real estate employment and manufacturing employment actually continued to cool. Another key takeaway with poor survey response rates and unemployment payments falling well below poverty levels in most states are that: employment data continues to get noisier. Certain signals are firing in one direction, while the aggregate fires in the other. With employment data falling to 4.1% (U3) - the risk has shifted back towards monitoring inflation, valuation, and bond market risks, which may contribute to a higher U3 later in the year - but even with the labor market being as soft as it is in so many sectors - the market is again caring more about yields, bonds, and inflation… One of the bullet points from the November UMich Survey stood out:

“Surge in Concerns that Prices of Major Purchases Will Rise” - hit it’s highest level in over 4 decades.

Outside of that - we’re seeing gold, copper, and most importantly - WTI Crude, advance higher alongside yields.

The higher 10Y means slower real estate sector activity (especially in the dead of Winter), pressure on equities at extreme valuations (+2 standard deviations from the mean), and a slowing in the larger cyclical sectors.

For those in the cyclical sectors (like CRE) and for those who pay attention to the technicals, this certainly isn’t how those folks wanted to start the year.

The Technicals

The technicals are shaping a lot like December 2021 - January 2022 (or late 99-00), but follow-through must be observed in the coming months. We have weekly bearish divergence signals on multiple timeframes

Tech Sector Weekly (QQQ) - Bearish Divergence Confirmed

Higher highs alongside lower highs… something that kicked off the 2022 inflation debacle.

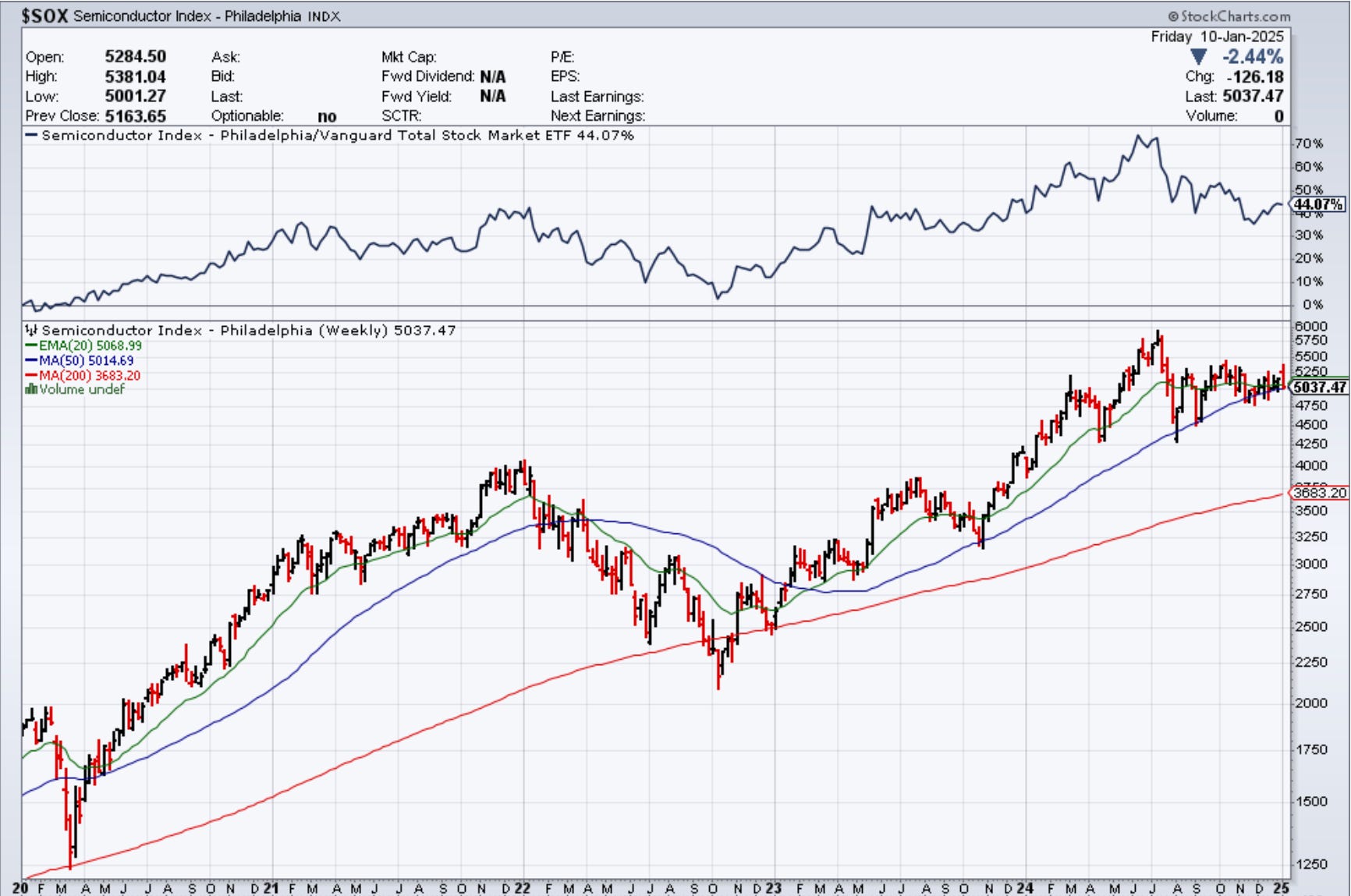

Semiconductors

A break below the 50ma would be very bearish for semiconductors, more broadly. Especially if Nvidia rolled over.

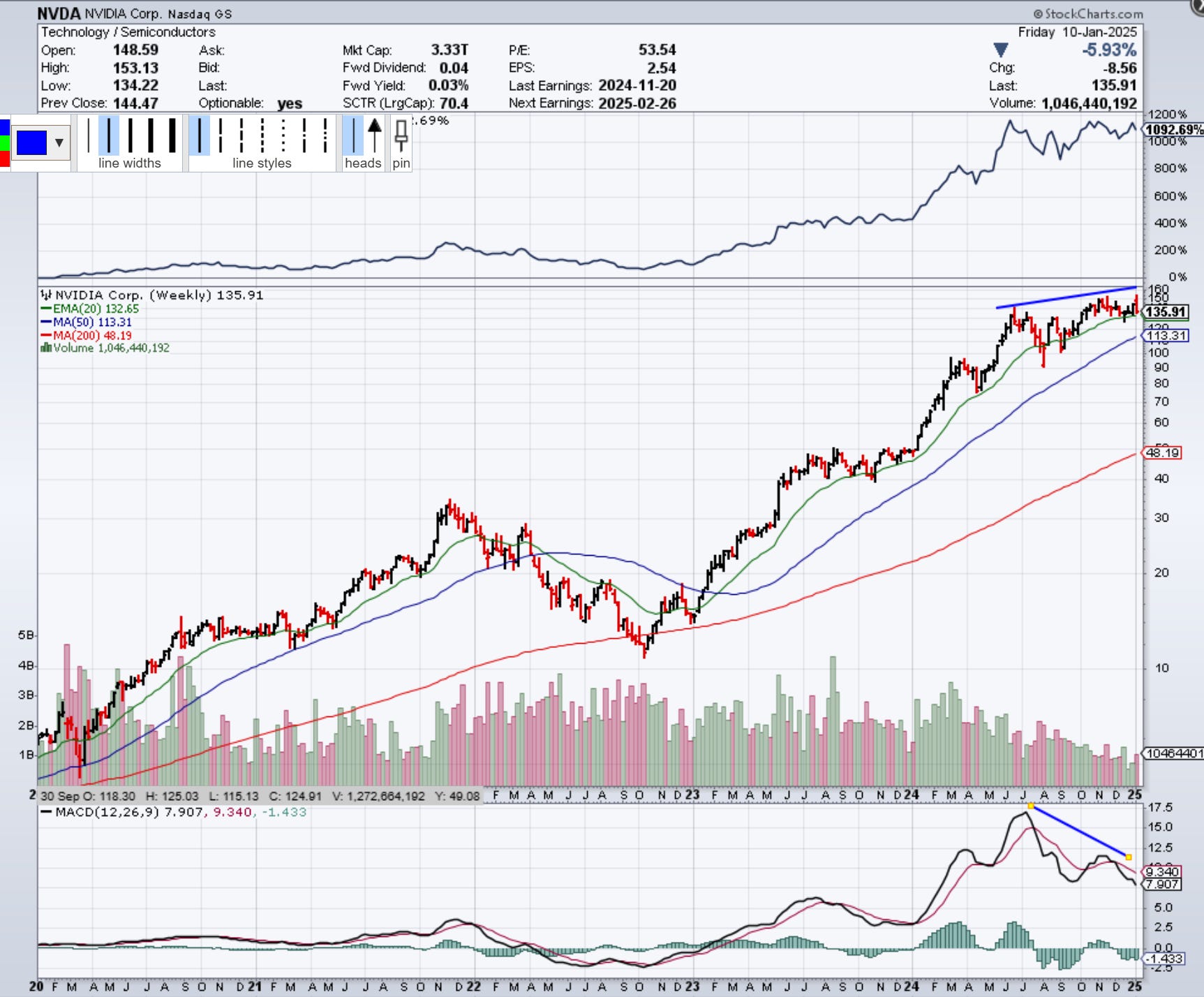

Nvidia - A Key to Tech

Notable bearish divergence

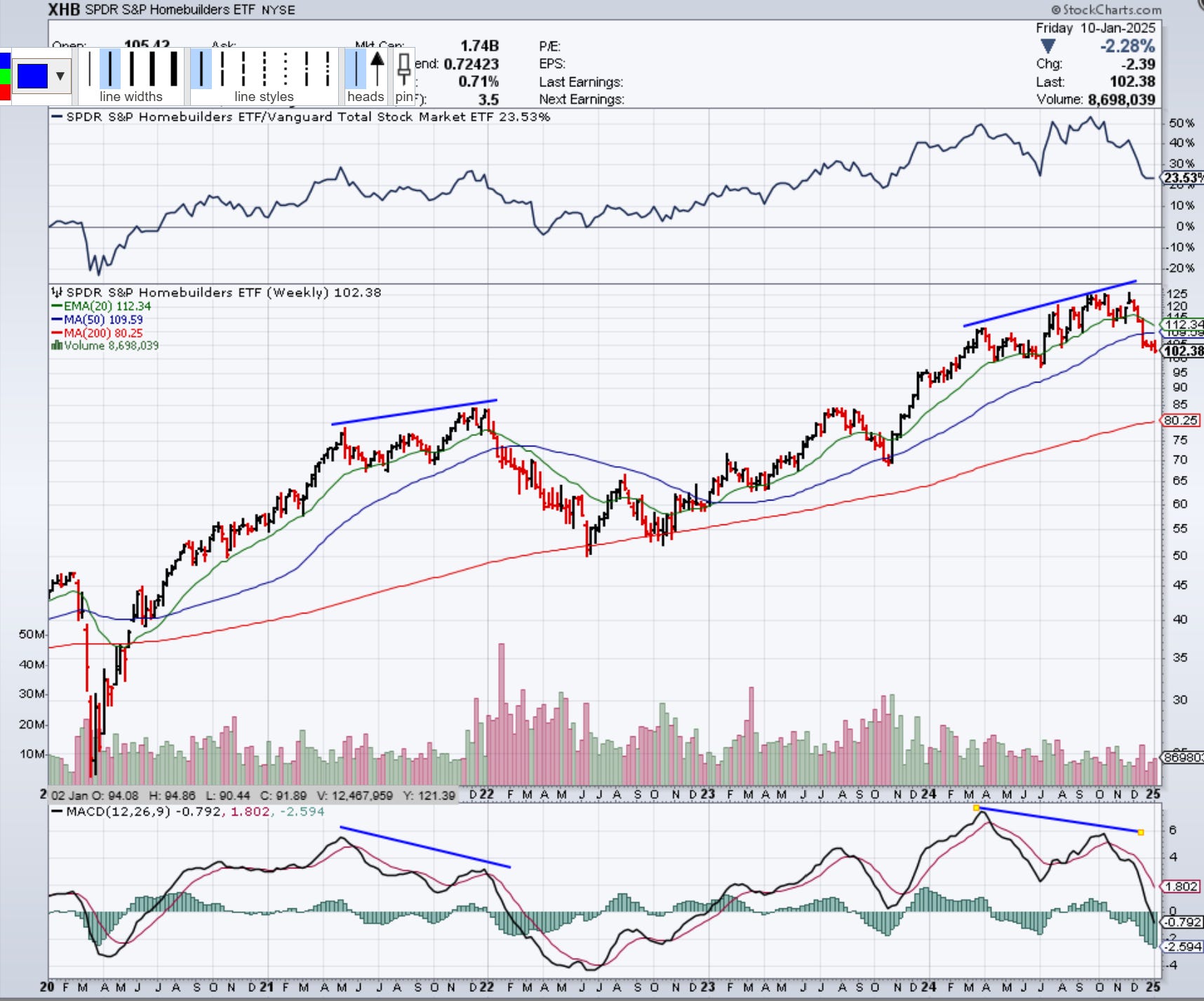

Housing - XHB - Gasping Under Higher Rates

Housing is following a similar setup that let to a year of decline in 2022, with a weekly bearish divergence confirmation and breakdown. More follow-through needed, but speaking to the impact of higher for longer on this particular sector./

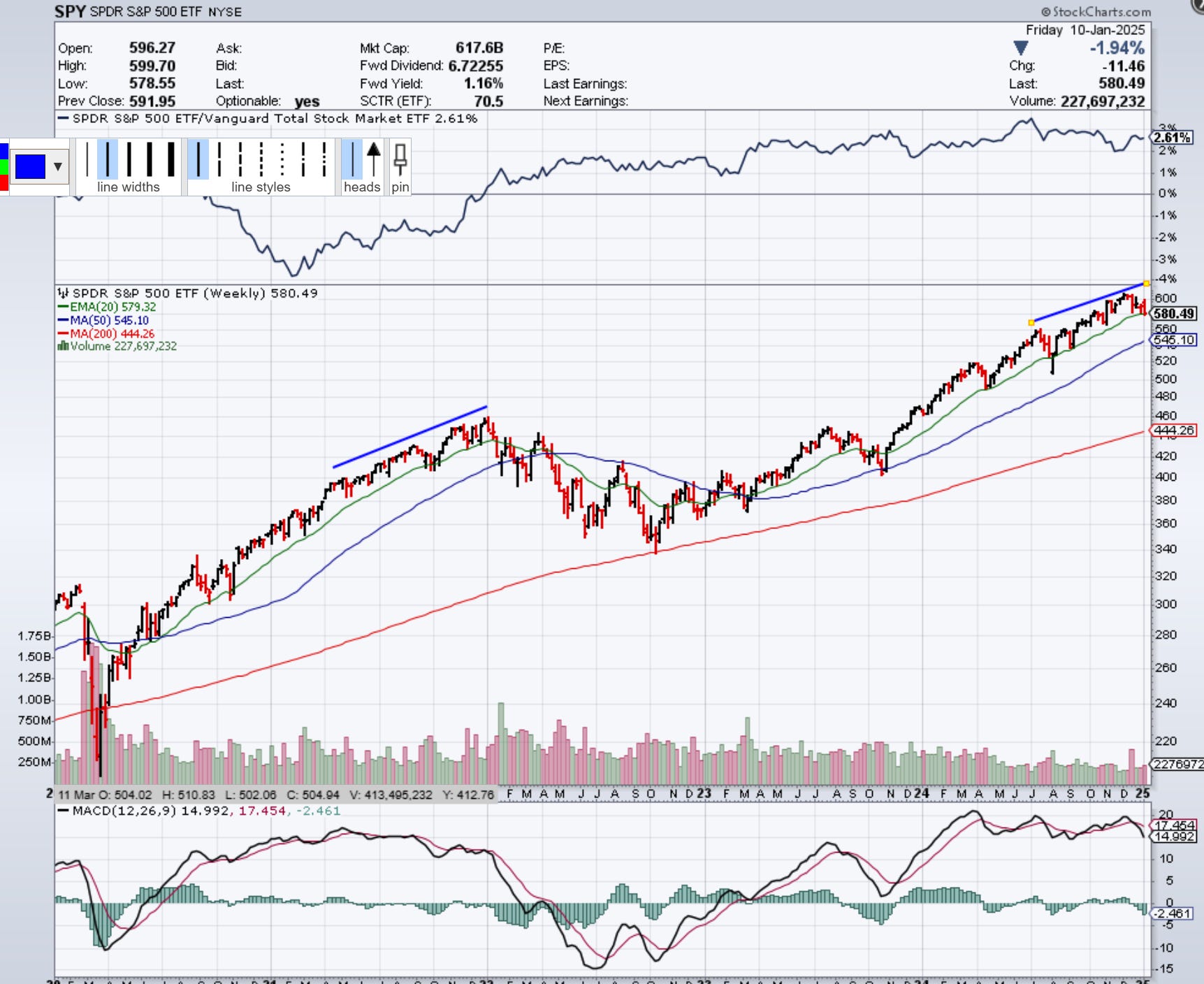

SPY - (S&P 500 ETF)

More obvious warning signs, especially if this confirms below the EMA (20) to end January.

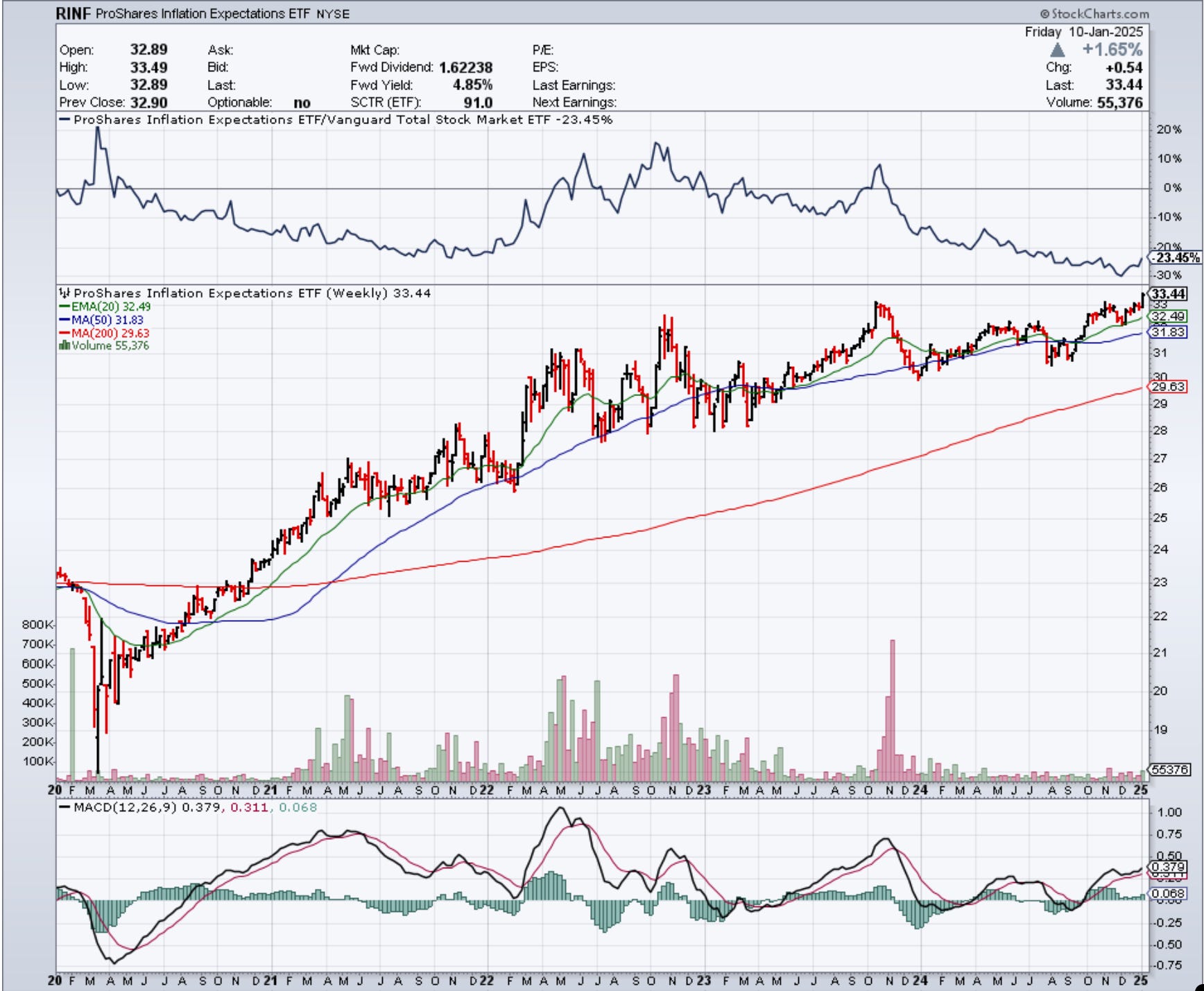

and lastly… Inflation Expectations (RINF) - speaking to our above points about inflation:

I’ll leave it with a comment I tweeted out on January 3rd… “I like to buy volatility when it’s cheap…” and that’s especially true after VIX’s usual performance following rate cuts… One thing (outside of technicals to keep an eye on) is long-term bullish investor sentiment:

Until our fiscal lunatics can get their books in order and under control - and the Fed takes seriously again the re-emergence of inflation risks, expect the inflation theme to catch a ride in the front seat - especially if the CPI numbers start to re-accelerate further next week. Higher inflation is not infact ‘bullish’ for equities if the 10Y advances - (see 2022)…

Those are the risks for now - if inflation falls (or comes in lower than expected) you may get some fresh tailwinds for equities - but for now yields are in charge.

Have a fantastic weekend and may the risk management be in your favor.

Don

(and don’t forget about Ozone)

Those expectations of higher prices definitely not great - that's what we saw before 2018 and that was really a poor year to be in stocks. The bear market during Christmas was a disaster for the administration and the only reason they found a way to get to a truce with China after starting the Trade War. Would be terrible to see that re-run on the television again.