MacroEdge Redeye: Canadian Whiskey Meets 'Oh' Canadian Unemployment, Labor Market Softening, Respecting the Lag...

After listening to our latest MacroEdge Radio - I just had to hit the keyboard to discuss labor, the markets, and the lag in great depth... #MacroEdge

@DonMiami3, MacroEdge Chief Economist *excuse typos

Hi all - it’s getting quite late here again in the EST but thought I would do a quick write-up on some of the market news/data for the week. Hopefully, some of you got to enjoy our latest edition (#2) of MacroEdge Radio (don’t miss next Friday), I certainly did while enjoying a beverage or several… I did a whiskey tasting this evening of some of Canada’s finest - and let me tell you that while they may have mastered their whiskeys (fabulous), their labor market isn’t look as good as the beverages. Tonight I will dive into the Canadian unemployment picture, labor market, job cuts, yields, and oil which are painting a complicated picture of the markets. If you haven’t yet joined us in the #Ozone - where we’re transforming the way individuals like yourself and enterprises view and have access to live comprehensive market data, or are wanting access to our brand new MacroEdge Vision Equity Research desk - join us for tomorrow’s Ozone Labor Market Report and more:

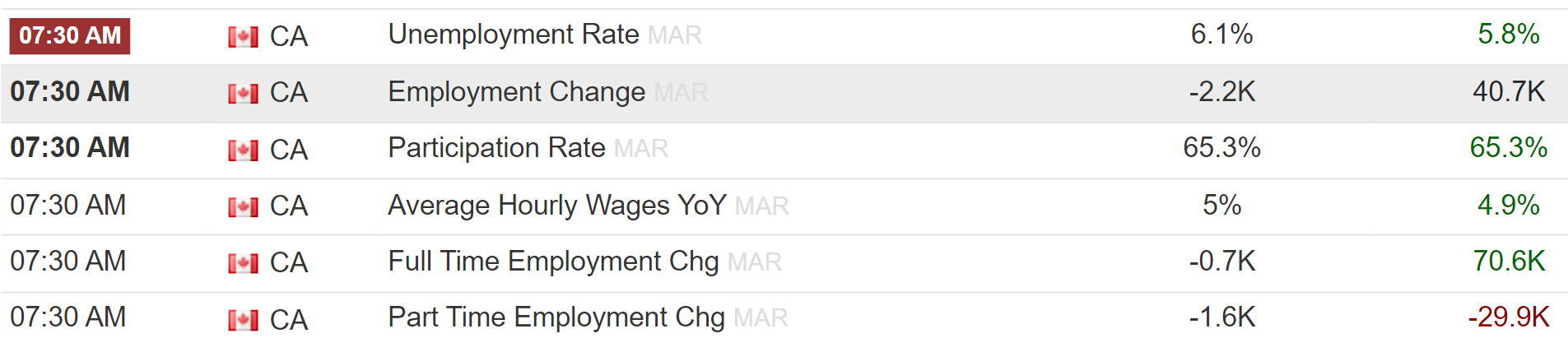

In Canada - which I very much enjoy traveling to - our friends are having a difficult time with their economy. The Bank of Canada has been astute in holding rates thus far but it looks like a June cut from the BoC is nearly certain after the unemployment and employment data continues to point to the Canadian labor market ‘breaking’. While some are citing supply-side issues with labor as the primary driver (this is of course a reason with record Canadian immigration) - demand for labor remains very weak. The labor market on the aggregate - among both part and full-time jobs actually contracted:

Unemployment rose to the highest level of the cycle, inflation remains present, and the Canadian Dollar continues to struggle. With net demand for jobs from companies way down in Canada, the picture will likely continue to get uglier over the next year as they face a broad array of issues in their economy from high price levels to very weak job openings data/hiring data, and new costs for lower and middle-class consumers like the ‘carbon tax’ just having taken effect as of April first. The overall unemployment picture (measured by all age 15+ in Canada continues to worsen, per StatCan):

I’ve noted Canada as a country leading us this cycle (going back to some of my comments from last year) and it appears that their roll-over is now well underway. The Bank of Canada cutting rates in June will only, in my opinion, give us confirmation of acknowledgment of the recession and broader labor market issues that are facing the country. This story will be the same here, but on a bit of a slower timeline. Canada, like the US, saw a small uptick in their unemployment rate, but the labor market dynamics are at present very different than what both of our nations faced in that time period (the 1990 recession was much more devastating to Canada than the US labor market), as well. We’ll continue to keep an eye on Canada as a proxy for foreign Central Banks out-doving the Fed in the coming months as the labor market picture becomes more obvious across the board.

Overall, a very mixed picture from the labor market reports today - the Household Survey continues to paint a recessionary picture of the full-time employment market while the BLS headline # looked ‘strong’ again (there are a variety of reasons behind this)… Overall, the labor market continues to cool and maybe the market is starting to take note of this (and an end-of-week ‘hawkish’ Fed pivot)… The Household Survey saw the ‘creation’ of 691,000 jobs and the loss of 6,000 full-time jobs:

I have a very hard time believing that this is something to be doing victory laps over… Many are grasping for further explanations in our very choppy labor market data as of late - from record foreign worker job adds to those taking on second jobs to make ends meet as credit card APRs exceed 30%+. The reality is - all of those are valid explanations for the complex and cloudy labor market data coming out. The full-time labor market has been in recession since December (now down over 2+mm jobs, a number larger than 1995 which some have noted as the most recent soft-landing seeing a drop in HH employment levels):

On the U-3 side of things, which does not included marginally attached members of the labor force, this cycle is now tied for the slowest increase of unemployment per our Employment Index, following 10y3m inversion:

Of course, this doesn’t invalidate previous theory on prior economic indicators - it rather reinforces that the lag this cycle is unprecedented coming off an unprecedented amount of money printing during the lockdown/QE4/bailout all mid-large+ businesses era that we saw from 2020-2022 as we were told that inflation was transitory (as we now track South Africa’s CPI rate). There are other warning signs as well, from those falsely identifying this labor market as one that is secularly tight, as it loosens, and those claiming economic data and signals are no longer valid (as has happened in many past instances):

(The ultimate inverse of the last decade has consistently been Puru above all else re: past economic cycles).

On our Job Cuts Tracker - I am very proud of the work our team has done to pioneer the first ‘near’ live job cuts tracker available in the realm of economic data. Our Q1 job cuts saw 255,100 versus Challenger’s 257,200 and it speaks to the incredible accuracy and work that we are striving for here at MacroEdge as we continue to expand.

This month - the trend continues to look concerning on the job cuts front - with the 99 Cents Store closure acting as a huge boost to the headline figure this month. This shows us that the ‘invisible’ consumer at the bottom rungs of the American economy have been pulverized by inflation and stores like these were unable to pass along price increases to their consumer base that was unable to bear these higher costs for goods (in some cases, just 25 cent increases). This speaks further to my theory on America eventually looking much more like South Africa in the way our demographics and economic landscape operate, where some have and there are most that ‘do not’ - which is where we continue to trend and will likely experience a worsening in this trend post-Fed policy of next cycle given the many conundrums they now face. We are currently on track for around 100,000 job cuts this month so it remains to be seen in the coming quarter if we trigger our ‘recession warning’ marked by 2 consecutive months >100,000 job cuts. Job cuts for Q1 were the 7th highest quarter going back 30 years, so notably high, as well. As job openings continue to shore up on a national basis, the labor market will continue to soften even though we haven’t seen the initial claims # budge yet with gig-dynamics et al continue to play a force for why that (ICSA) number has remained so low. Again - complex, but slowing, labor market picture:

(This chart should be useful for you all to visualize the lag on a 12-month smoothed basis playing out in real-time). Notice the uptick across all groups, and the sharp increase in youth unemployment as other groups continue to rise. The labor market continues to move like a BNSF train and not a TGV train as it cools further:

Yields made an interesting move this week along with commodities (gold, silver, etc) to the upside, as higher for longer language was parroted out by the Fed later in the week with speaker after speaker parroting a new narrative about inflation or labor. For equities - the risk has two likely pathways here - yields breaking to the downside and fast based on a rapidly weakening labor market (the less likely scenario) which would weigh on equities, or the inflation risk rearing its head as commodities soar and yields on the longer end forcing the Fed to continue the H4L narrative. Higher yields were bad for equities through much of the hiking cycle so the risks are multi-faceted at current equity risk premiums (at all-time highs). The reversal Thursday was noted by many simply because there wasn’t a reversal of this nature yet this year so people were surprised that sell-offs can still occur. In an inflationary or resumed QE environment, we may see inflation rear its head again and act as a boon for asset prices across the board - but I am waiting until the Fed pivots for more clarity on that. I anticipate that oil, gas prices, gold, etc will need to take somewhat of a breather at some point given their very sharp rises of late although this may signal consolidation before the next legs higher… see our Tuesday write-up on oil for more on that front. Powell continues to face a huge (and growing) number of risks on his platter and it remains to be seen when the labor market will finally force the Fed’s acknowledgment, but the next quarter is going to be an interesting one (especially into earnings season again for Q2).

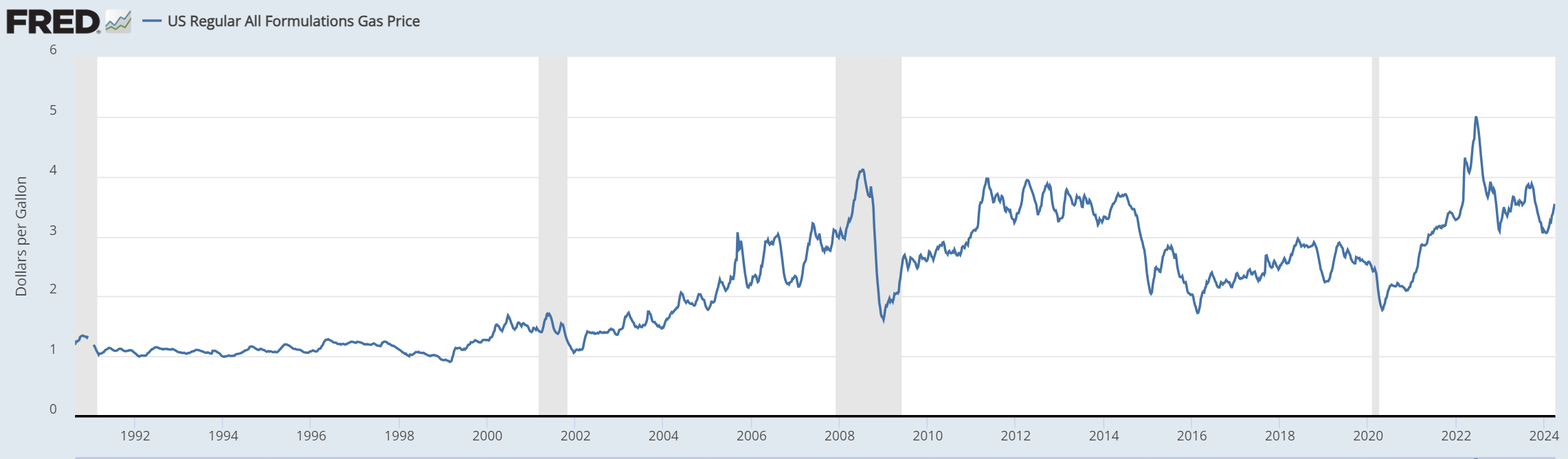

Gasoline prices… up we go (I felt this at the pump today for a $92+ fill-up):

I remain neutral here on the overall market at these levels, somewhat positively slanted towards commodities, and am closely tracking the work of our new research desk Vision, led by Six to see what evolves on that side of things over this important quarter. That is visible for you current Ozone members here on the Substack and in the X community. It’s a damn complicated market with some damn confusing labor market data, but the data we’re putting together helps paint a clearer picture of what remains ahead and the risks that continue to exist and evolve in the current economy.

Hope to see you all for tomorrow’s labor market report and see you in the Ozone…

Don’t forget to join us in the Social Club as well if you currently in Ozone and haven't yet joined: https://twitter.com/i/communities/1774595054994088213

Have a great weekend,

Don