MacroEdge Redeye 8/9: Employment Situation Update to Past Cycles, Road to Rate Cuts Volatility, & Lagging Claims

The soft landing is transition into a soft liftoff (and flight) continues with employment data continuing to weaken. #MacroEdge

Happy weekend to all MacroEdge community members, readers, and new folks joining us for the first time.

This will be a short Redeye - since we like to keep these short - but we will be providing our Q3 update for our 2025 Roadmap tomorrow so keep an eye out for that.

There’s been a lot of excitement surrounding earnings and various volatility in markets this week, which we’ll discuss in more depth in the Sunday weekly Ozone report. Join us for two-week access and experience all of our data and research at:

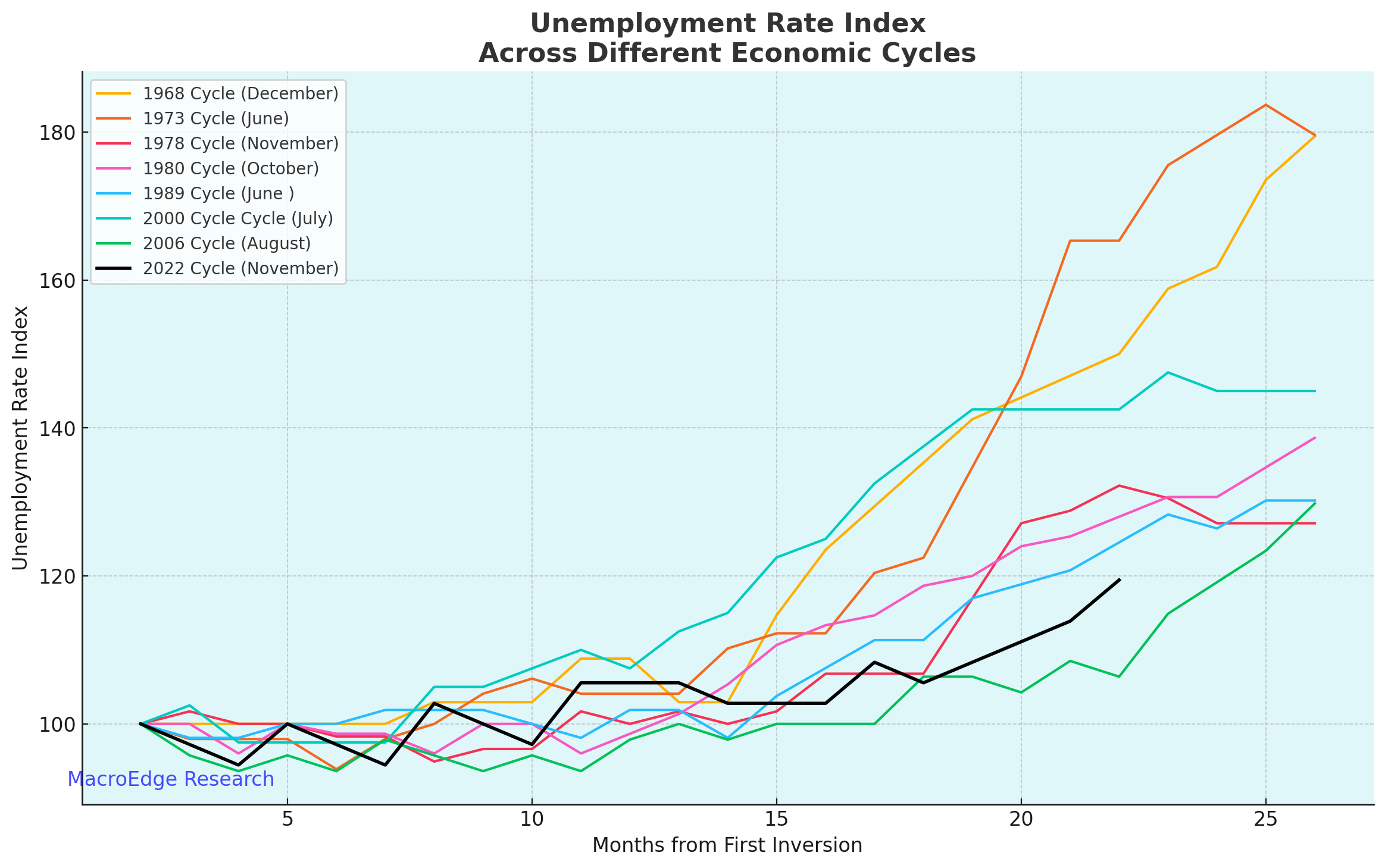

Employment Situation Update to Past Cycles:

The unemployment rate is tracking as we expected it to - between the 1989 cycle lags and the GFC. We will continue to see the U3 index increase over time from here on out based on past historical cycles, although the uniqueness of each cycle sees variations in unemployment trends.

Once the Fed begins to ease, that’s usually when we see larger magnitude moves in the unemployment rate. Recall that the employment situation in the US (on the unemployment side) really moves at the margins - so it’s good to monitor U1/U2/U3/U6 for broader views respectively, at the unemployment.

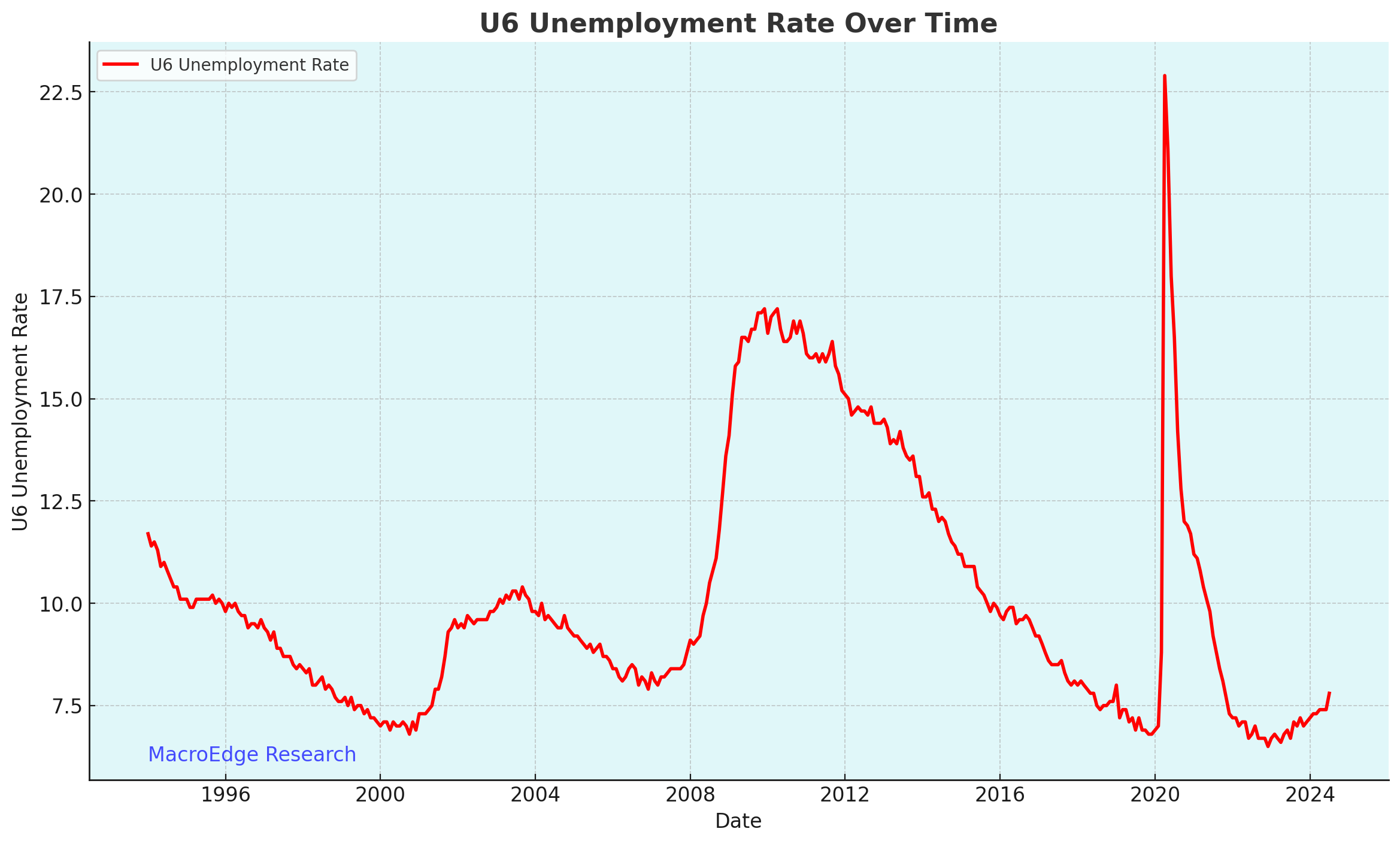

U6 also snapped upwards by 40bp last month (and not because of Cat 1 Hurricane Beryl, in our opinion):

The lag continues to play out as we’ve seen August with a very large start to the month on the job cuts front with companies like Dell announcing over 10,000 job cuts, to other companies like Stellantis and Paramount Global who are laying off thousands each as well. We will continue to monitor the job cuts as they happen.

Go back and read

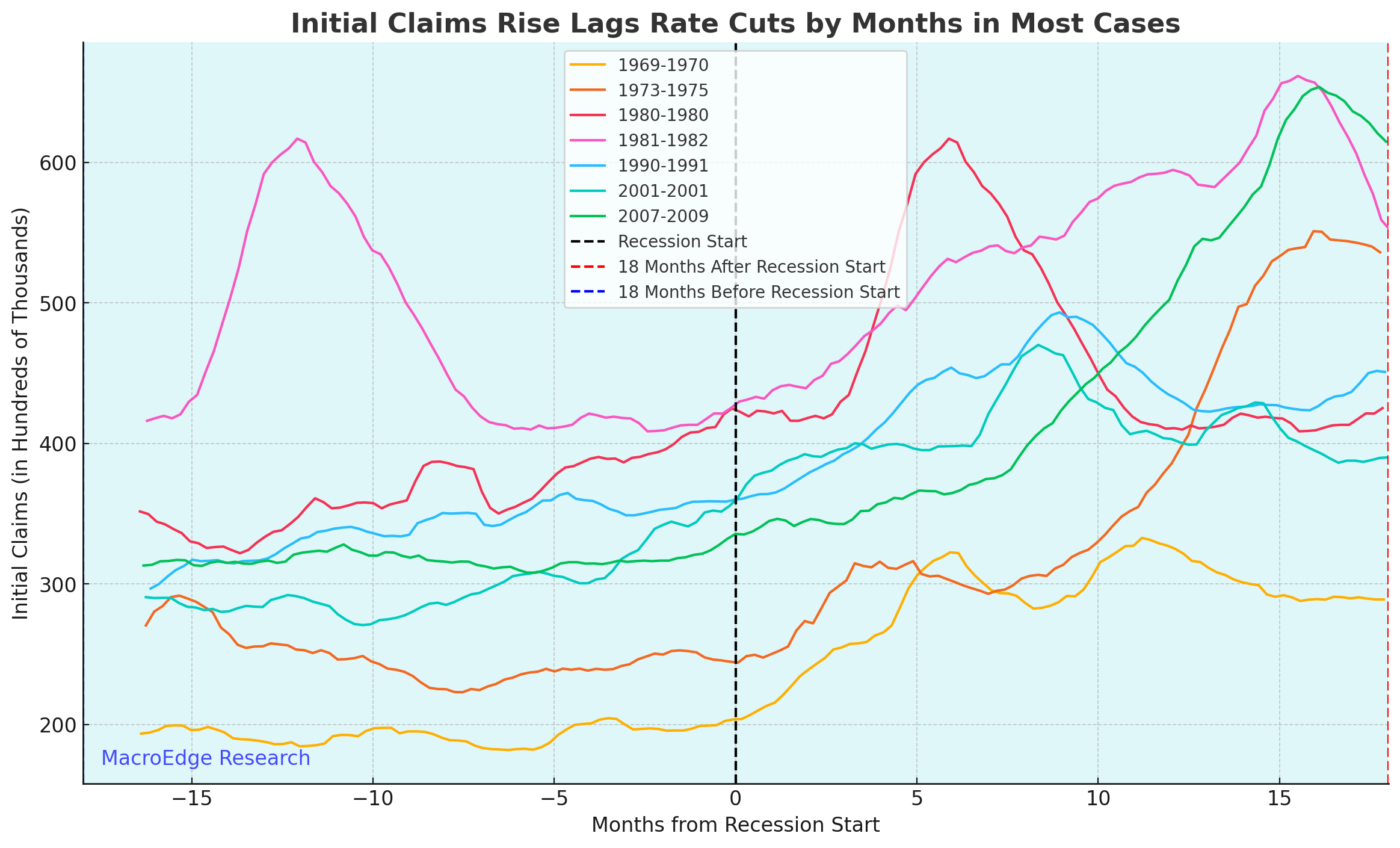

Initial Claims are a Very Lagging Indicator:

Historically, initial claims (which excited markets this week as we are back in a good-is-good and bad-is-bad regime) are a very lagging indicator. The data outliers here are the back-to-back 1980-1982 recessions which you can see in the data with the large spike in 1980 also being seen in the start of the 1981-1982 cycle.

We’ve also had a lot of discussion around the validity of claims as an economic indicator anymore given how low states pay out in unemployment insurance (recall that COVID payments were a one-time deal). Unemployment claims in Florida, for example, pay around $250/week for an unemployed person - they can likely make far more in the gig 1099-NEC economy - versus going through the hassle of filing a claim. Secondly to that point - if you’re in a city like Miami - you aren’t even making a rent payment on $250/week.

Road to Rate Cuts Volatility:

With the ‘Road to Rate Cuts’ being the road we’re now on - we anticipate that the Fed starts the easing cycle next month with a 50bp rate cut.

While the short-term carry trade blowup and employment fears saw markets sell hard over the 2H of July into early August - our focus remains on what happens post-cuts now and the MacroEdge Vision desk is in the process of identifying opportunities through our research work.

Until then, we continue to respect the lag, monitor the data, and watch for signs of further labor market weakening (earnings & employment)…

Don’t forget about CPI this coming week too…

Have a great weekend everyone and we’ll see you all for the Sunday report.

Don & MacroEdge Team