MacroEdge Mid-Week Note: Yields, Technicals, and Employment Data

A quick midweek note on yields, technicals, and the latest employment data including job openings + Florida unemployment data.

Good Wednesday evening everyone,

We’re quickly getting through this short week at speed, so there’s more data and another nice weekend ahead of us. Hopefully you all had a great long weekend and are getting ready for the warm summer (at least here) that’s starting in just a few weeks.

We’ve got a lot of great things in store for MacroEdge in the upcoming months - MacroEdgeTV, our new multimedia outlet, will be available through YouTube in the coming days. Here will will host and upload our multimedia content, exclusive stories, interviews, and more for Ozone members and the public. Ozone members will get exclusive access to interviews with some of the best and brightest in the world of finance as well as coverage and stories from markets across the United States and globe.

MacroEdge One will be our new division covering data and research for Oceania and Asia and we anticipate that it’ll be ready by the end of July. To get all of the current Ozone research (which includes equity research from the Vision desk) - try Ozone for two weeks here:

In this midweek note we’ll highlight:

Yields

Technicals

Florida Employment Data

Yields:

The 10y3m (10 year minus 3-month) spread has uninverted a bit in recent days - which has spooked most equities:

This has largely been due to the movement in the 10-year yield (long end). Yields are approaching an inflection point with more data this week and higher inflation appearing again in places like Australia and New Zealand. We’re also staring down the potential of Europe cutting in the next two weeks and Canada potentially following suit after the ECB.

Take a look at the 10-year yield:

The move the last few days to the upside has spooked assets (as noted above), and continuation to the upside would like drive a ‘bear steepener’ effect that could be problematic with the weakening labor market. Hard to take a direction here but we will be monitoring where the 10Y, in particular, heads from here due to the ramifications included in either direction. If the 10Y went lower sharply, that would likely be due to weak economic data and cooling inflation expectations. So either scenario with very weak market internals/breadth could be problematic.

Let’s keep a close eye on it.

Technicals:

As discussed in our Sunday Weekly Ozone report (which you can get here):

The technicals were starting to look very extended again - particularly as the TRAN (transports) got disconnected from the Nasdaq rally. The Dow has been the laggard (with the Russell) and participation has been limited to Nvidia and not much else. The Dow has seen 5 red days in a row again so the next moves are likely to be determined by the data and 10Y.

The Dow monthly chart still has the potential for a ‘bearish divergence’ which would definitely be a major cause for ‘pause’ and a look at something more like an extended drawdown.

In the shorter-term, the Nasdaq got hyper-extended on the near-vertical move earlier this month and is breaking down from the highs:

The broader direction and potential shift will be data-dependent (and in particular: employment-dependent) so I wouldn’t get too hyped up either way at this point in time. Reiterating what Six said the other day in the Vision update - our overall view is that market fundamentals are extremely weak and we’re certainly concerned about some of the employment trends taking place (as you’ll see below). This scenario paints the potential for a larger downside situation that we have yet to see materialize, as we wait for things like Fed policy action, and higher unemployment. You can follow our updates on MacroEdge Vision for the latest on what our equity research desk sees on that side of things.

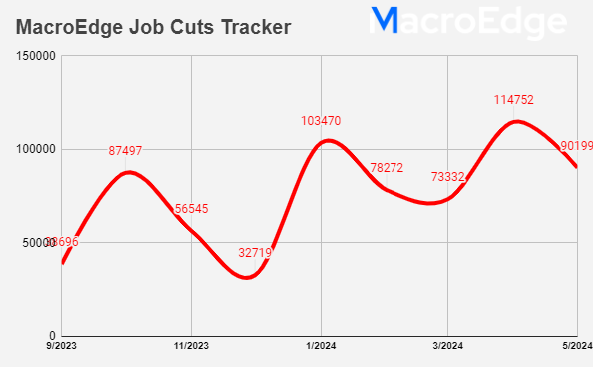

Employment Data:

On employment data - we continue to observe a labor market ‘cooling’ that has been moving gradually. Job cuts are again elevated this month:

Take a look at the latest Indeed Live Postings today, indicating a sharp drop in job postings:

We anticipate this labor market cooling to continue over the coming quarter and into the second half of the year.

The NFIB data continues to point towards slower payrolls ahead and a very interesting scenario would be one in which yields are rising and employment is weakening at a quicker pace… Let’s see what the rest of the week has in store and we’ll catch you Friday evening for more with MacroEdge Radio #9.

Stay tuned and have a great evening,

Don & MacroEdge Team