MacroEdge Mid-Week Market Note: 'Where in the Cycle?', Welcome to Summer Mania

My focus remains on the weakening labor market, an update to 'where in the cycle' as equities don't care, and a quick welcome to summer note.

Good Wednesday evening all,

If you had the day off - I hope it was well, and if you didn’t - I hope it was still swell. We’re at an interesting historical point for markets, politics, and the economy. While individually I have my concerns about the long term feasibility of the current trajectory of debt growth in the United States, our trends in birthrates, reliance on short-term policy boosters like mass immigration to boost economic output and job growth, expanding wealth inequality, cost of living, and more - my goal with MacroEdge is for our team to remain as objective and data-driven as possible in our shorter-term view world. In this mid-week discussion note/rant/free-form article (which I like to do about once a quarter) - we’ll hit on a lot of topics all at once about ‘where in the cycle’ we really are.

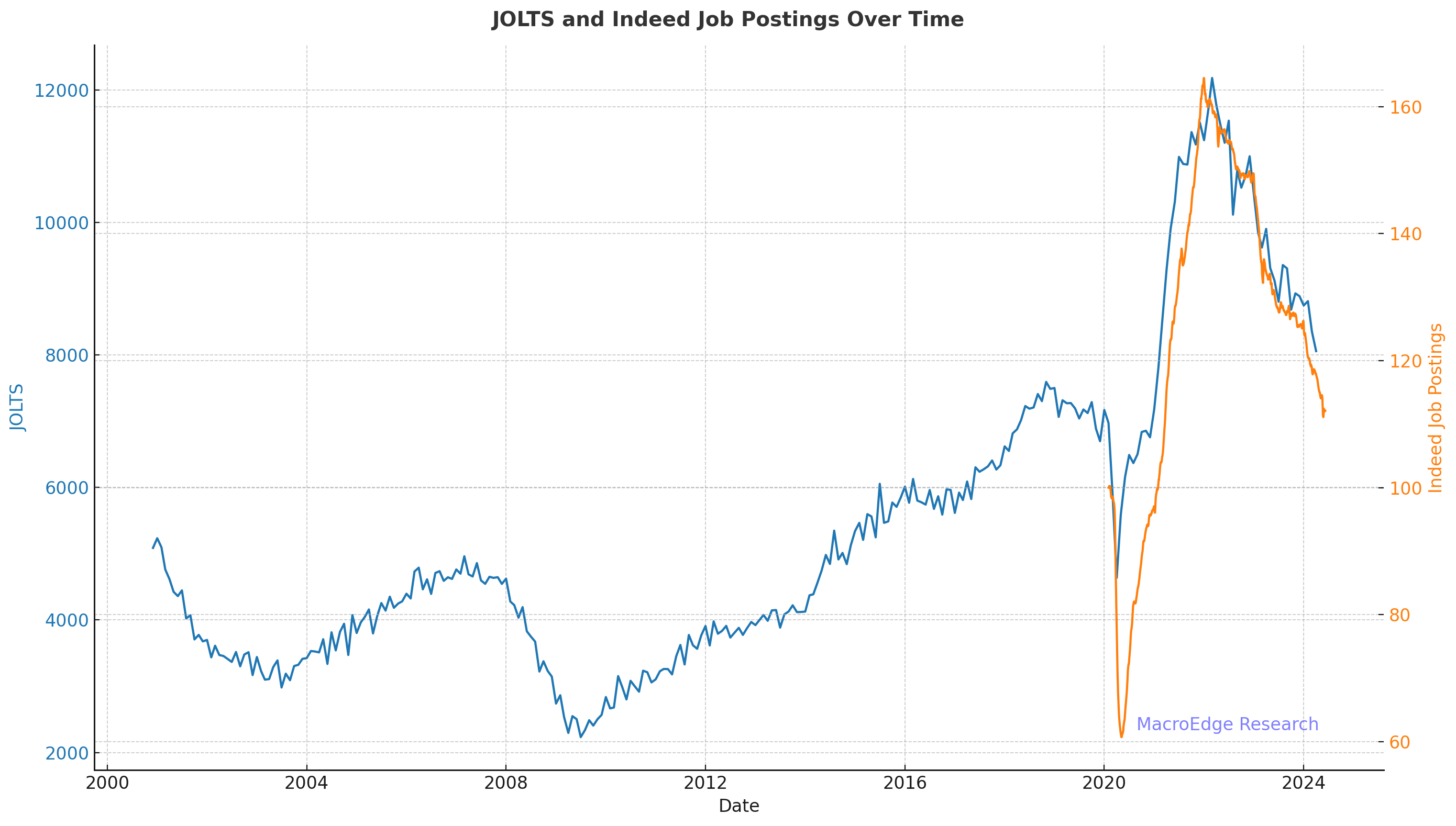

I started to grow weary of the labor market strength (now 20 months ago) when the 10-year / 3-month yield curve inverted - our historically reliable early warning signal for economic problems ahead - and my outlook on the labor market given current underlying trends remains unchanged. When we first began discussing ‘employment/employment/employment’ going back to April 2023 when our first posts were released, unemployment and the number of total unemployed people were both at cycle lows. We’ve seen a lot of labor market weakening from then to now - and the underlying trends remain in place for further weakening. Our five primary measures of a weakening labor market (unemployment - U6, total unemployed Americans, the Kansas City Fed LMCI, claims, and total job postings/openings) have all continued to weaken which is why I’ll be a lone ranger on labor market worry isle if I have to be the only one. We’re now at the point (price does in fact drive sentiment) where people who I respect will look at the employment data like I am crazy if I suggest that there are larger issues ahead for the labor market. Many are claiming this new regime of $7.3 trillion a year in Federal spending has brought about this ‘new regime’ of a Caracas-style equity market seeing double-digit gains with labor market perfection. While the labor market will have structural issues shortly due to demographics that may contribute to lower headline unemployment (like we see in the Japanese data) - this certainly isn’t the case this cycle. The uniqueness of this cycle’s ‘gig economy’ added into the labor market mix of millions of Americans turning on their phone to 1099-NEC their way into making minimum payments on their credit cards has also likely masked weak labor data - making it harder to gauge the overall health of the labor market. Here’s a look at the latest data for these 5 measures:

(KC Fed LMCI - small increase in May on lower job cuts)

(Job Postings and Openings) - larger trend remains intact, 5+ million less jobs than when the Fed began tightening

As the Fed remains in its restrictive stance through what will likely be the late summer, the odds for our ‘Summer of Policy Error’ rise sharply. Even with lower job cuts this month, a single month in the larger trend is something we aren’t using to confirm a reversal in the trend (especially until the Fed begins to lower rates!).

(Initial claims, above) are not high enough, but lag rate cuts (as does unemployment). The current trajectory and global cutting cycle underway puts us on a timeline for September cuts and based on the labor data for June - I don’t anticipate July. The current order will see England, Australia, New Zealand, and then the United States begin to lower rates. The 10y/3m remains inverted at -118bps and will not resolve until the Fed begins to drop rates (barring a ‘wave 2’ of inflation). Inversion remains a positive tailwind for equities and it remains to be seen if cuts are the same (they have not been in Canada/Europe, so far)…

The coming ‘resolution’ to our where in the cycle narrative will be a critical inflection point for what our economy looks like for a long time. The US as it currently stands is now running a $2 trillion deficit (and adding $1 trillion) to the national debt roughly every quarter. While the typical person will look at this and say things like ‘whatever’, America #1, financial engineering/MMT are undefeated - the problems, societally, are much more structural. We’re seeing the overall decay impacting (in particular) males under 30 in the United States, our birthrate - dramatically, and things like the % of wealth held by the top .01% now >15% of all outstanding wealth in the United States. The reality and real key takeaway to grasp on this point is we’re now adding $2 trillion to the debt every, single, quarter for slightly over 1% GDP growth.

The odds are the debt increase will continue to be exponential and other larger issues contributing to the above will expand, too. Reminder that wealth inequality (even in the most unstable countries) - takes similar form:

Currency debasement, unbelievably accommodative fiscal/monetary outlets, and a reckless entrenched political establishment will have their date with destiny, but this is a much longer-term discussion. Luke Gromen, who I follow on X, writes frequent fascinating posts on the subject - particularly in the context of other historical superpowers that have made the same follies that the United States is currently making. It’s difficult to discuss these issues in an apathetic world where frankly, nobody cares that much, and in a political system where we will see nothing get done.

With all of that being said, our primary focus (on the research and macro side of things) will be the employment picture as it continues to evolve. Because all else equal - employment matters the most for the economy. Six will continue to guide the way forward for our equity research desk as I take a more employment/macro-oriented focus for the second-half of the year (which begins in just 2 weeks!).

Have a great evening and start to your summer.

Don