MacroEdge Institutional Report 02: Launching Institutional Research, MIRP, Value, and the Left Tail Playbook

In the second edition of the MacroEdge Institutional Report - we talk about the coming launch of our new offering line (10/1/25) - dive into everything from macro to the left tail. and so much more.

Critical Points Discussed

The Launch Moment: October 1 is when MacroEdge Institutional Research goes live. MIRP is the operating system for conviction, transparent and rules driven, built for allocators who cannot afford noise. The Roundtable this week sets the tone.

The Macro Reality Check: Markets are priced for perfection, credit spreads are compressed, and inflation is alive where it matters in services, insurance, utilities, and healthcare. Rate cut euphoria looks stretched and CPI and PPI will test the narrative.

The Risk Playbook: Left tail stress is cheap, correlations break when they should not, and regional banks show the cracks first. The focus is on convexity, credit signals, and sector fragility while defensives prove their worth when confidence runs too hot.

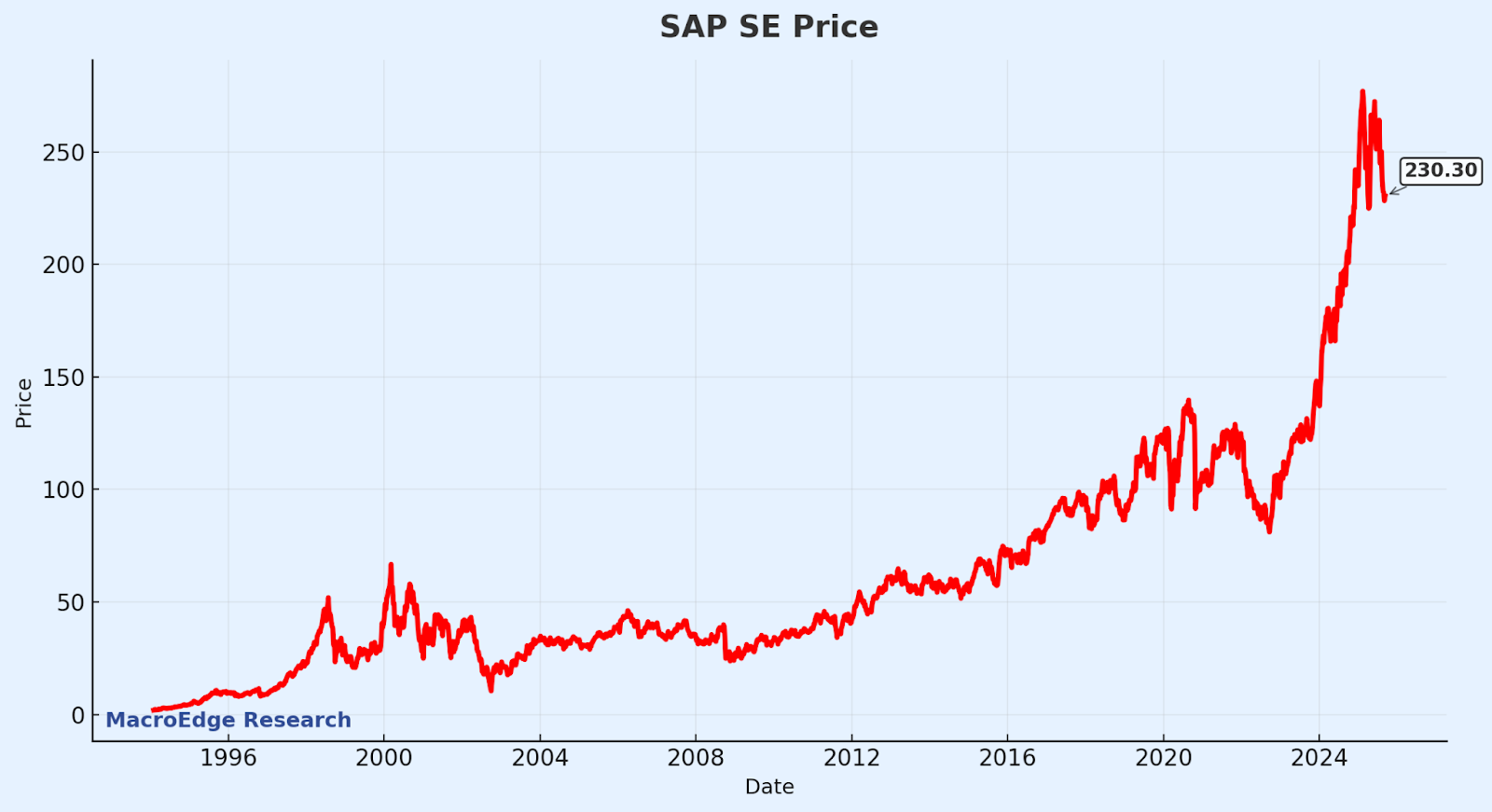

The Structural Truth: Enterprise systems are not just software, they are infrastructure. Oracle, SAP, and the integrators control workflows, compliance rails, and backlogs that make switching nearly impossible. Multiples may cool but durability does not.

Good Tuesday evening MacroEdge Readers,

This evening we’re going to dive into the second edition of our MacroEdge Institutional Report series, focusing on everything that we seek to do and deliver through the newest division of MacroEdge.

While Ozone will continue to deliver cutting-edge insights, data, and our thoughts to our more than 8,000 Substack readers & across our audience - Institutional Research is where we’re really going to press into the underlying answers to the deeper questions on our minds in the macro sphere. From positioning to ideation, data & more, we’re putting it all under the Institutional Research umbrella. For those with a discerning eye for opportunity, or those with a desire to utilize our cutting-edge employment data to make your next business decision - whether it be portfolio strategy, or labor strategy - Institutional Research is designed for you.

I am very pleased with the team that we’ve assembled to make Institutional Research a reality, building upon the foundation that is Ozone - and we’re going to keep making MacroEdge better for you, every single day. A missing element from Ozone - the personalized customer experience - is coming into play with Institutional Research, and we’re really going to enhance the MacroEdge experience with the addition of direct relationship-building tools with you, each and every one of our Institutional Research readers and members.

Institutional Research is all about connecting you with opportunity, and our team is here to do just that. We’re excited for the liftoff of Institutional Research, and look forward to the 10/1 launch - when we will make registration available, for those who want to experience the full Institutional Research experience for 4-weeks.

MacroEdge Institutional Research Arrives Soon

MacroEdge Institutional Research is built for allocators, portfolio managers, and family offices that move real capital and do not tolerate noise. Critical macro indicators, valuation signals, and decisive guidance live in one interface so you move from signal to sizing in one click. Speed is not a feature. It is the strategy.

At the center is the MacroEdge Institutional Research Portfolio (MIRP) Index. It is a performance-driven portfolio framework that hunts asymmetric opportunity and enforces discipline when markets get loud. No mystique. No hero trades. The MIRP Index tells you what changed, why it matters, and how to position. When to scale. When to defend. When to stand down. It is an operating system for conviction.

Subscribers receive MIRP Insights and Research with monthly and intramonth updates covering signals, adjustments, and forward-looking risk and reward. You also receive the MacroEdge Institutional Report once a month with hard analysis of market structure, macro conditions, and the evolving opportunity set. On top of that, you get Actionable Institutional Intelligence, including valuation frameworks, macro dashboards, and targeted signals for decision-makers who cannot miss the window.

Availability and Access

First access trial accounts open October 1, 2025, alongside the official release of the MIRP Index. To request access or learn more, visit macroedge.net/institutional.

The MacroEdge Institutional Research Portfolio – Performance Tracking

MIRP is the rules-driven portfolio core of MacroEdge Institutional Research. It converts macro signals into disciplined positioning, targeting asymmetric opportunities across global markets with clear rules, tight risk, and transparent accountability.

Asymmetry engine: portfolios designed to cap downside and compound upside across cycles.

Cross-asset scope: equities, rates, FX, commodities, and volatility signals in one framework.

Update cadence: monthly and intramonth MIRP Insights with signal changes and forward risk/reward.

Transparency: live model weights, trade log, and post-trade attribution for every adjustment.

Implementation ready: index-aligned model that maps cleanly to futures, ETFs, or managed accounts.

A Macro Roundtable: Thursday Evening

On Thursday evening, we’re tying something new with a Macro Roundtable. This will take place on Thursday at 9pm EST, and we’ll be sending out the direct link to those that fill out the link below. This will be a nice way to start building out our community through different channels, and we will restrict the space for Q/A and audio to around 30 people. With members of the MacroEdge team participating, we expect that we go about 45 minutes to an hour and it should be a blast. No official format yet, but RSVP below and we’ll make sure to send you an invite 24-hours before.

The Left Tail is About as Cheap as It Gets

With sentiment being completely off the rails again, especially among retail investors. The age old post-08 bailout-era that we find ourself still in begs the obvious question, is there zero risk in equities?

X-user ‘Red2011’ notes his thoughts:

If you read my feed, well, you’ve probably come to understand that I have my own thoughts too.

Some of my different thoughts on the left-tail here, as we find ourselves in a risk-free environment.

Index crash convexity (VIX verticals / SPX put spreads)

Purpose: clean left-tail exposure when correlation moves toward 1.

Structure: 3–6M VIX 20/30 or 22/32 call spreads; SPX 5–10% OTM put spreads staggered across expiries; total premium at risk per sleeve ≤ 0.50–0.75% of portfolio.

Quant tells: VIX 1M–3M term structure in contango ≥ +2 vol pts; implied minus realized 1M ≤ +3 vol pts; 25Δ put skew in the 20–40th percentile; VVIX sub-100 with realized correlation rising.

Risk rails: if VIX < 13 for two consecutive weeks and 1M realized < 10, reduce or roll down premium; if sustained backwardation, monetize.

High-yield credit stress (CDX HY or HYG/JNK put spreads)

Purpose: credit usually reprices before equities when funding tightens.

Structure: 6–12M HY index protection or ETF put spreads 5–15% OTM; sleeve risk ≤ 0.50–0.75%.

Quant tells: HY OAS in bottom quartile of 10-yr history (roughly < ~3%); CCC–BB spread compression at extremes; downgrades/upgrades < 1.0; coverage ratios slipping; 12-month default rate trending up; hot HY primary while loan officer surveys tighten.

Risk rails: if HY OAS tightens ~50 bps from entry alongside improving macro breadth, collapse to tail optionality; re-engage on re-tightening or issuance spikes.

Regional-bank credit shock proxy (KRE downside structures)

Purpose: if credit wobbles, regionals wear it via funding costs, deposit mix, CRE marks, and capital talk.

Structure: 3–9M KRE put spreads or flies; optional money-center hedge vs KRE to neutralize broad financials beta; sleeve risk ≤ 0.50–0.75%.

Quant tells: 1M KRE implied-vol percentile < 40th with 25Δ put skew steepening; short-interest days-to-cover > 3 and rising; H.8 small-bank deposits flat to down and 3-month C&I/CRE lending contracting; office/retail delinquency rates rising; criticized-loan ratios edging higher; KRE vs BKX relative strength breaking down; tighter correlation with HY spreads.

Risk rails: two weekly closes of KRE outperforming BKX with deposit stabilization and slower reserve builds — collapse to tail flies only.

Having left-tail exposure doesn’t mean getting into a kayak and going head-on into the rapids, names like Oracle today, a business backed by a machine and brilliance, highlight continued value and upside opportunity, even in an environment of low-priced risk and extreme valuations.

Outlining the Defensives

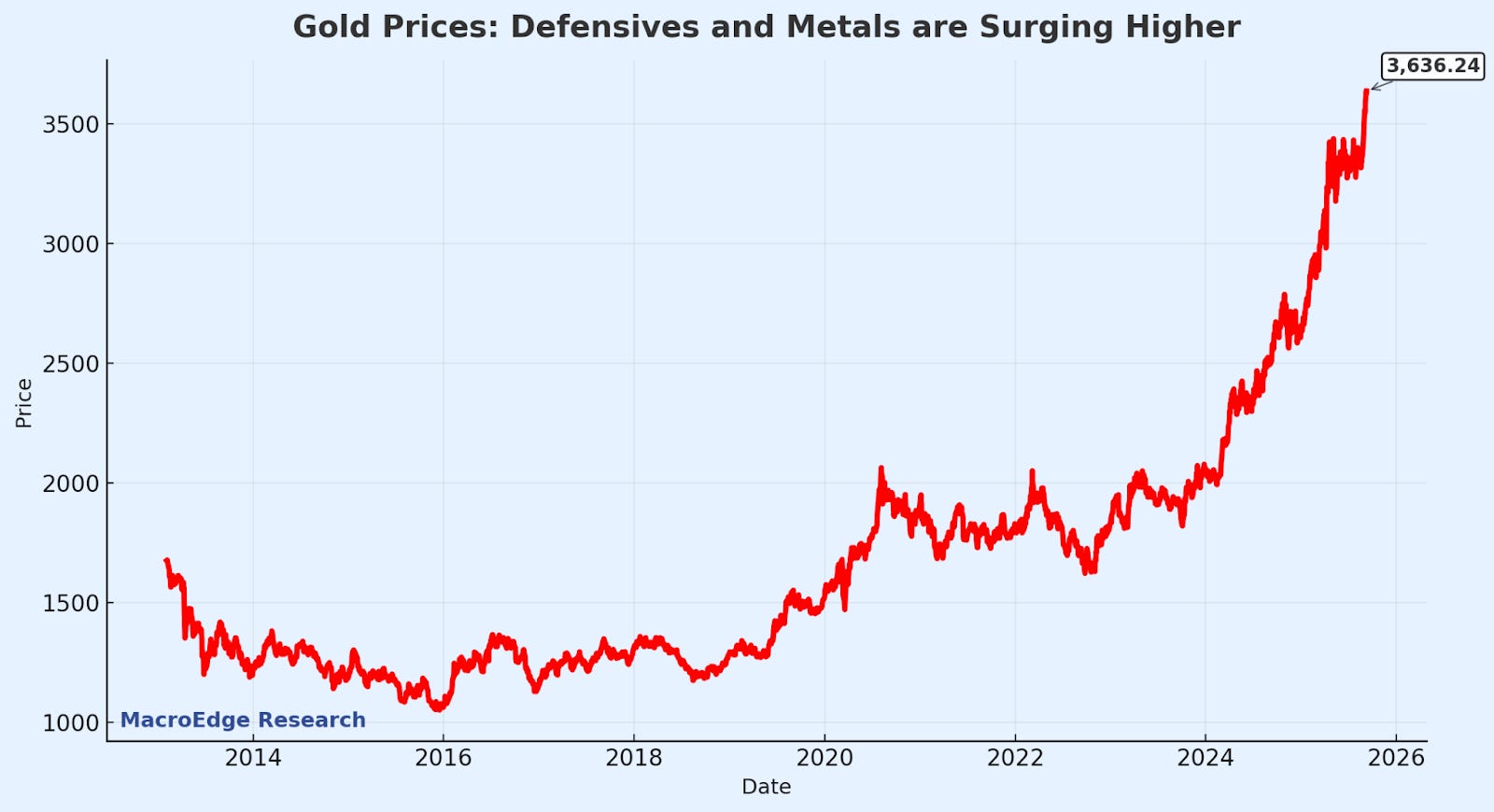

Central banks are stuffing reserves with bullion, and the bid is relentless. Retail keeps chasing on every dip, ETFs are rebuilding inventory, and the futures curve says the market is willing to pay up for immediacy. Everyone from sovereigns to private wealth is getting the goldfinger right now because policy credibility is thin, real rates are chopping around, and gold is the one defensive that keeps working when everything else gets marked down.

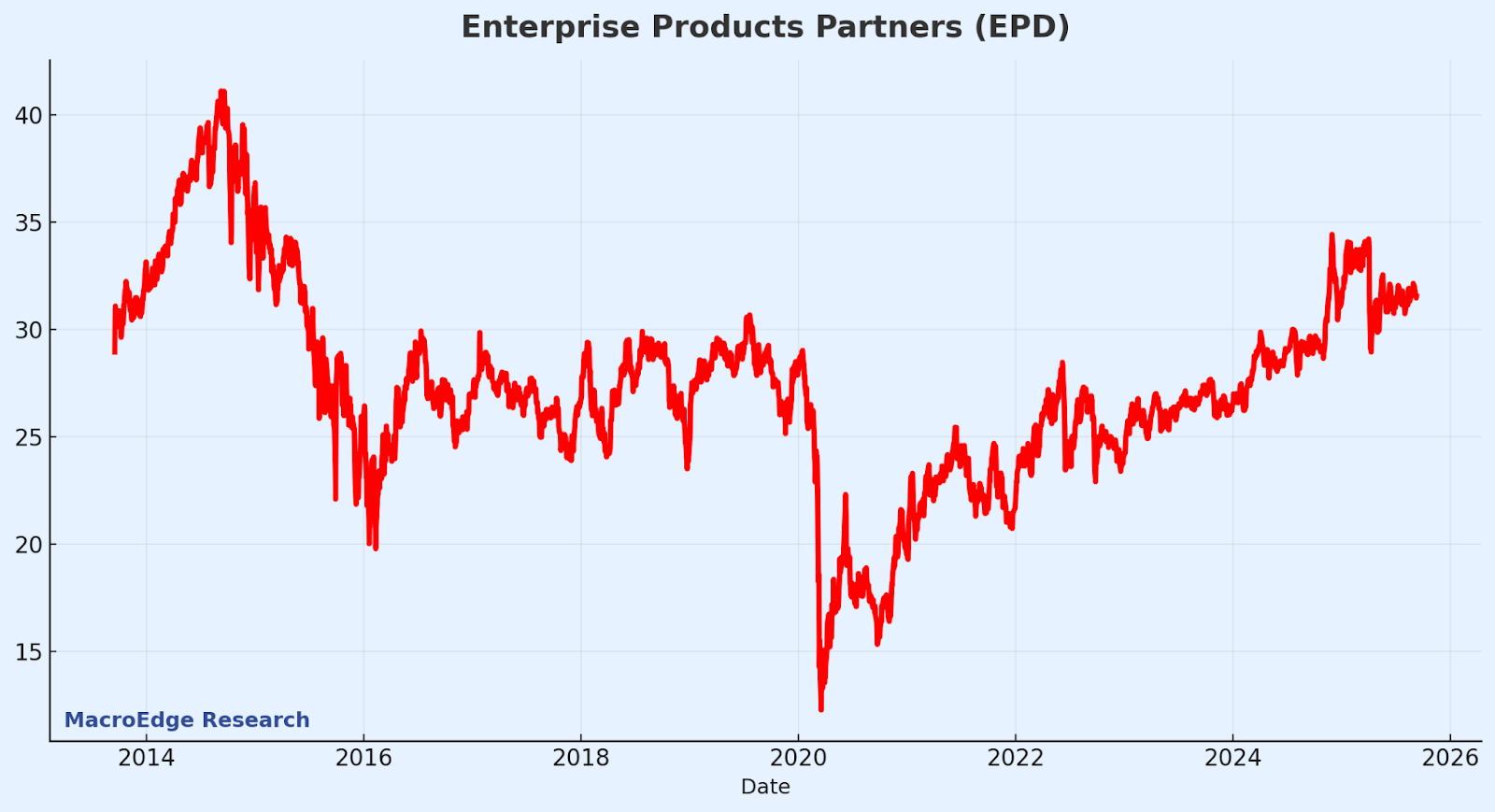

EPD is the classic defensive in a stagflation tape because cash flows are largely fee based, volumes are sticky, and many tariffs have CPI-linked escalators. The balance sheet is clean, distribution coverage is healthy, and free cash flow funds both distributions and buybacks. You get inflation pass-through, durable contracts, and a valuation that still sits below what you would expect for this quality and predictability.

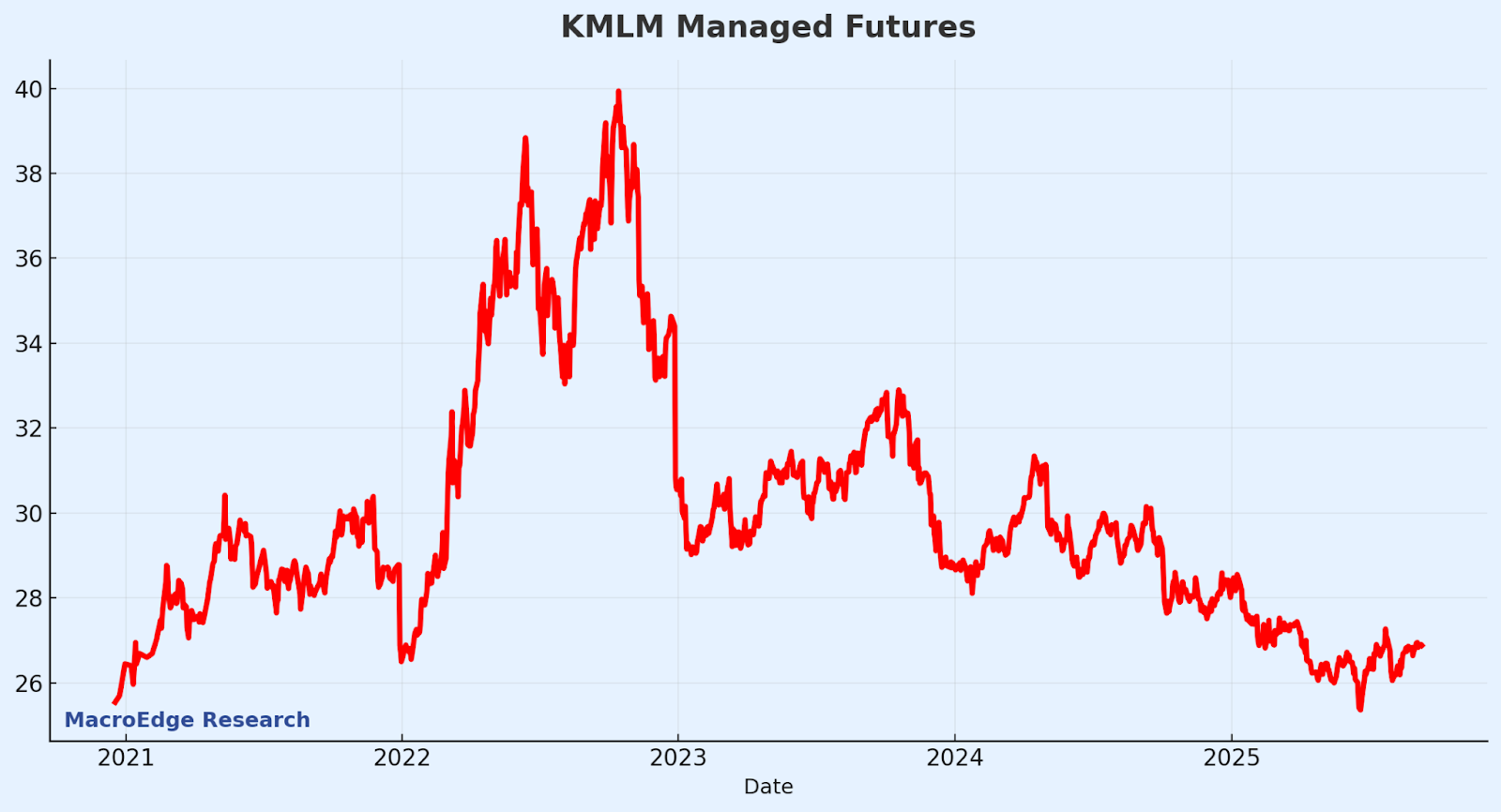

KMLM is a clean, liquid way to hold trend exposure across commodities, rates, and FX, which is exactly the kind of diversification that works when inflation is sticky and growth keeps wobbling. It is rules-based, capital-efficient, and historically low correlation to stocks and bonds helps stabilize portfolio volatility while giving you upside if stagflation drives persistent moves.

Is the Ghost of CPI Really Dead?

With this week being a PPI x CPI week - we’ll have more objective company commentary in the Redeye Macro Note, or the Weekly Macro Note, about the true state and trends with inflation.

Is the Ghost of CPI Really Dead? Not even close. Headline prints have cooled, but the spine of inflation is still services, insurance, utilities, and medical care, and those are not melting on schedule. Our read is simple: until 3-month core services, median CPI, trimmed-mean, and the insurance and healthcare components roll convincingly, the CPI ghost keeps rattling the house.

Rising Unemployment and CPI

One of the plausible, more ‘surprise’ scenarios seems to be a situation of rising unemployment and rising CPI, in the mind of the institutional investor of late. People have a hard time envisioning a scenario where the 10Y can continue to rise, alongside rising unemployment, but I wouldn’t call that an outlier scenario anymore.

What Value Remains on a 3-12 Month Horizon

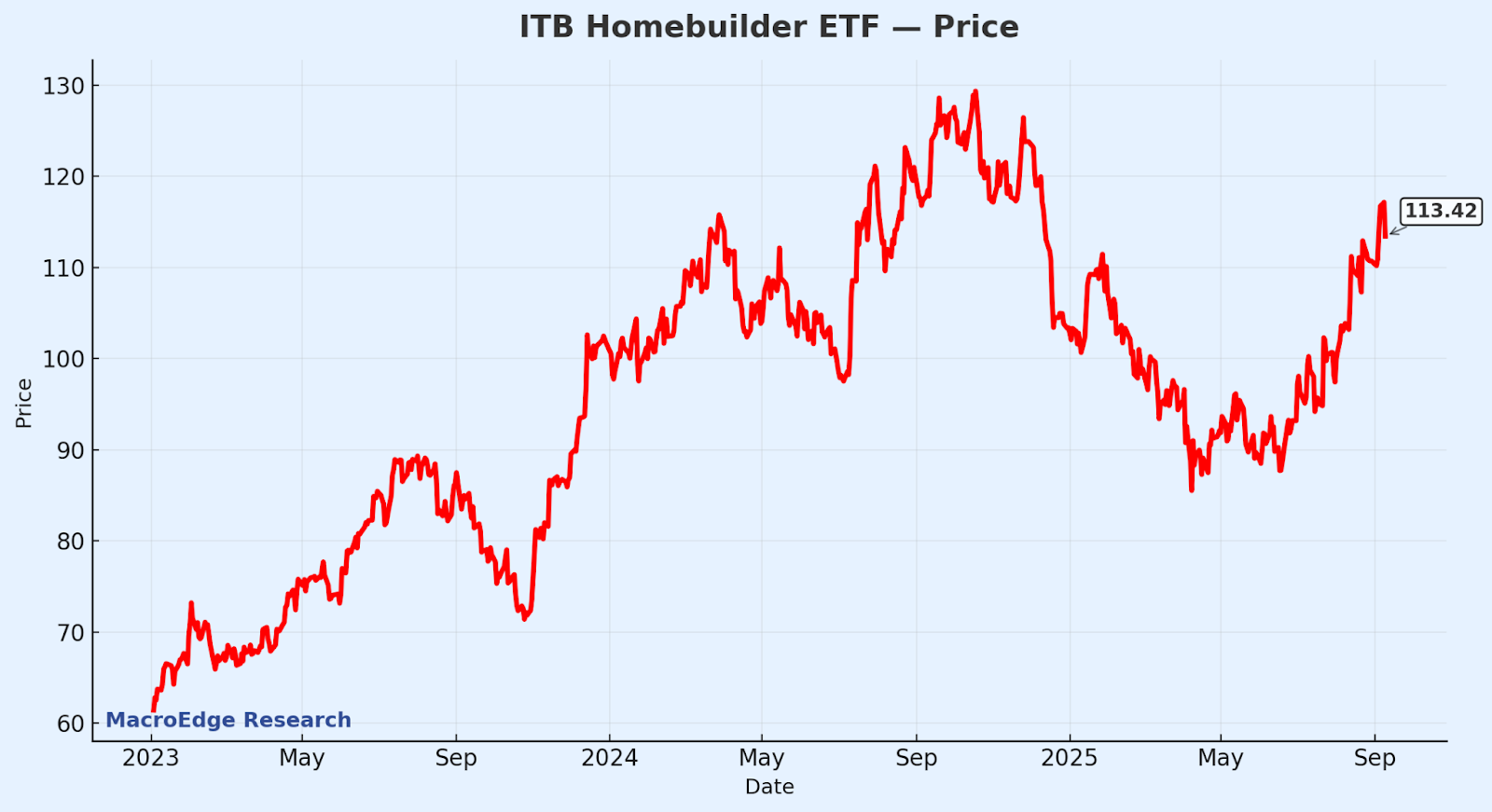

From a value standpoint, Six is taking the deep dive away below on unique individual and thematic opportunities, and there’s a lot to bite on. I’ve taken particular interest in the airlines, regional banks, and new home construction companies as targets in my crosshairs if the broader global macro picture continues to slow down.

While equities are near record-expensive levels, valuations are stretched, and sentiment is too - there’s still opportunity out there for those of us seeking it out.

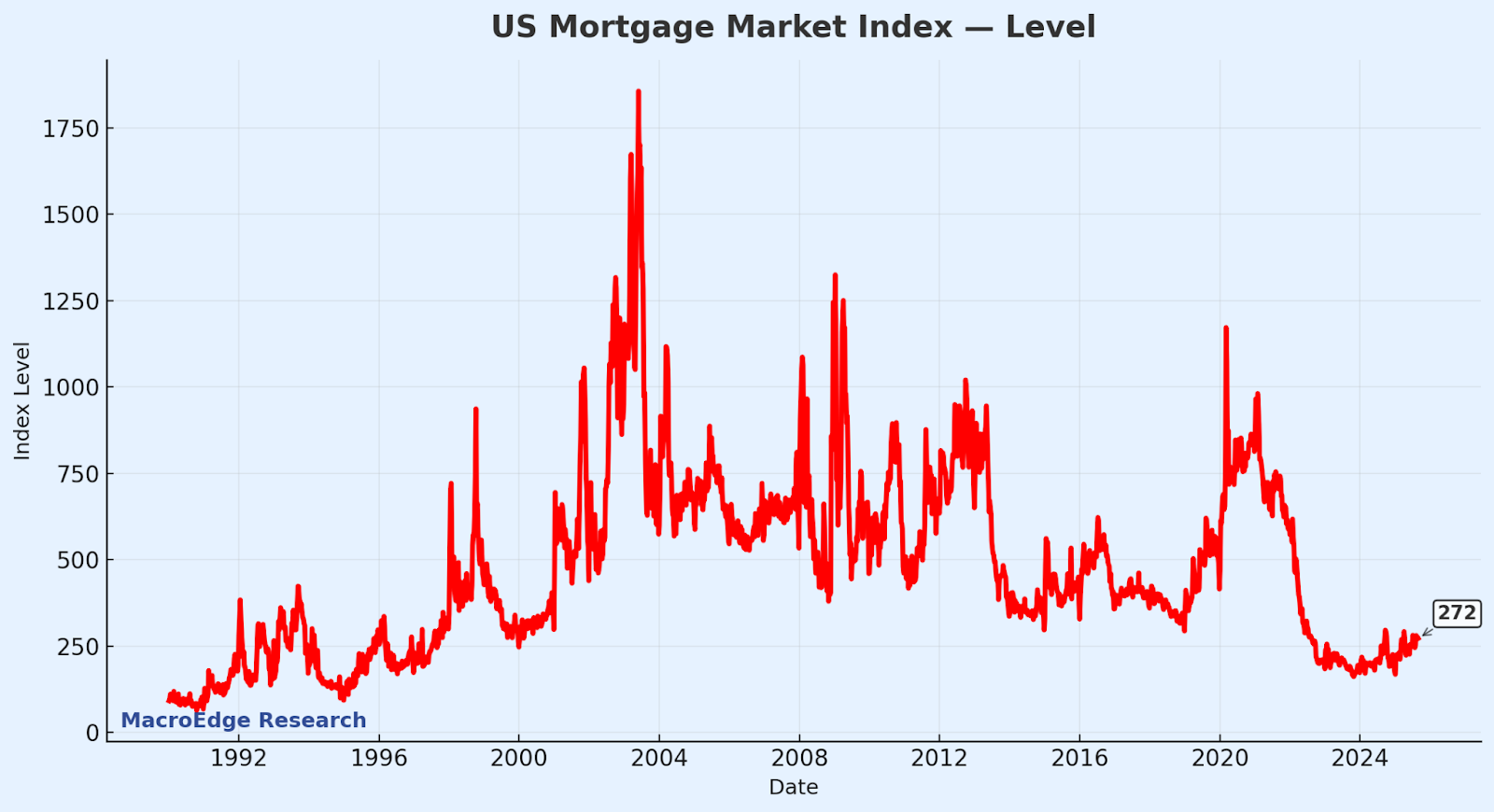

New home construction companies have rallied sharply off of the April low, on the excitement about rate cuts.

Note (US Mortgage Market Index - below) has barely moved following the 100bps of easing that had everyone thrilled last year for rate cuts:

Continued risks in the mortgage market include…

Mortgage demand inertia: last summer’s rate cut excitement did almost nothing for purchase or refi applications. Primary–secondary spreads and tighter underwriting muted transmission, so small rate moves will not save orders.

Affordability + rate volatility: payment shock remains high and every 50–75 bp wobble hits traffic and forces incentives.

Demand rollover / cancellations: rising unemployment and softer household cash flow lift cancels and erode backlog quality.

Credit tightening: AD&C and mortgage credit can tighten quickly as regional banks retrench, raising funding costs and slowing starts.

Existing-home supply normalization: resale inventory returning pressures pricing power and compresses margins on community openings.

Cost and insurance pressure: labor, lots, materials in pockets, plus insurance availability and premiums in FL/CA/TX squeeze gross margins.

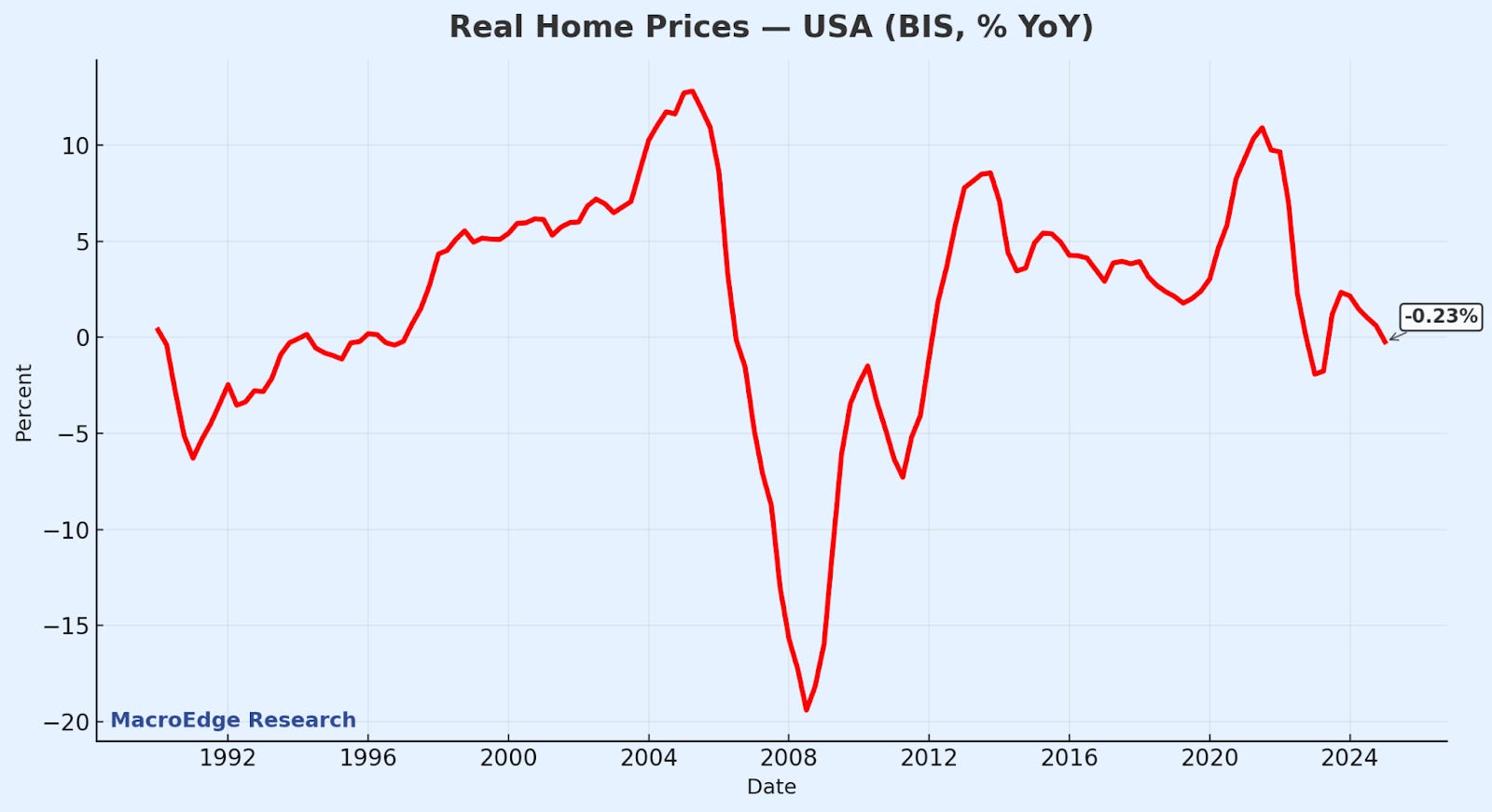

It’s important to also point out that home prices are not participating in the equity price rally, falling in many markets on a nominal basis, and nationwide on a real basis.

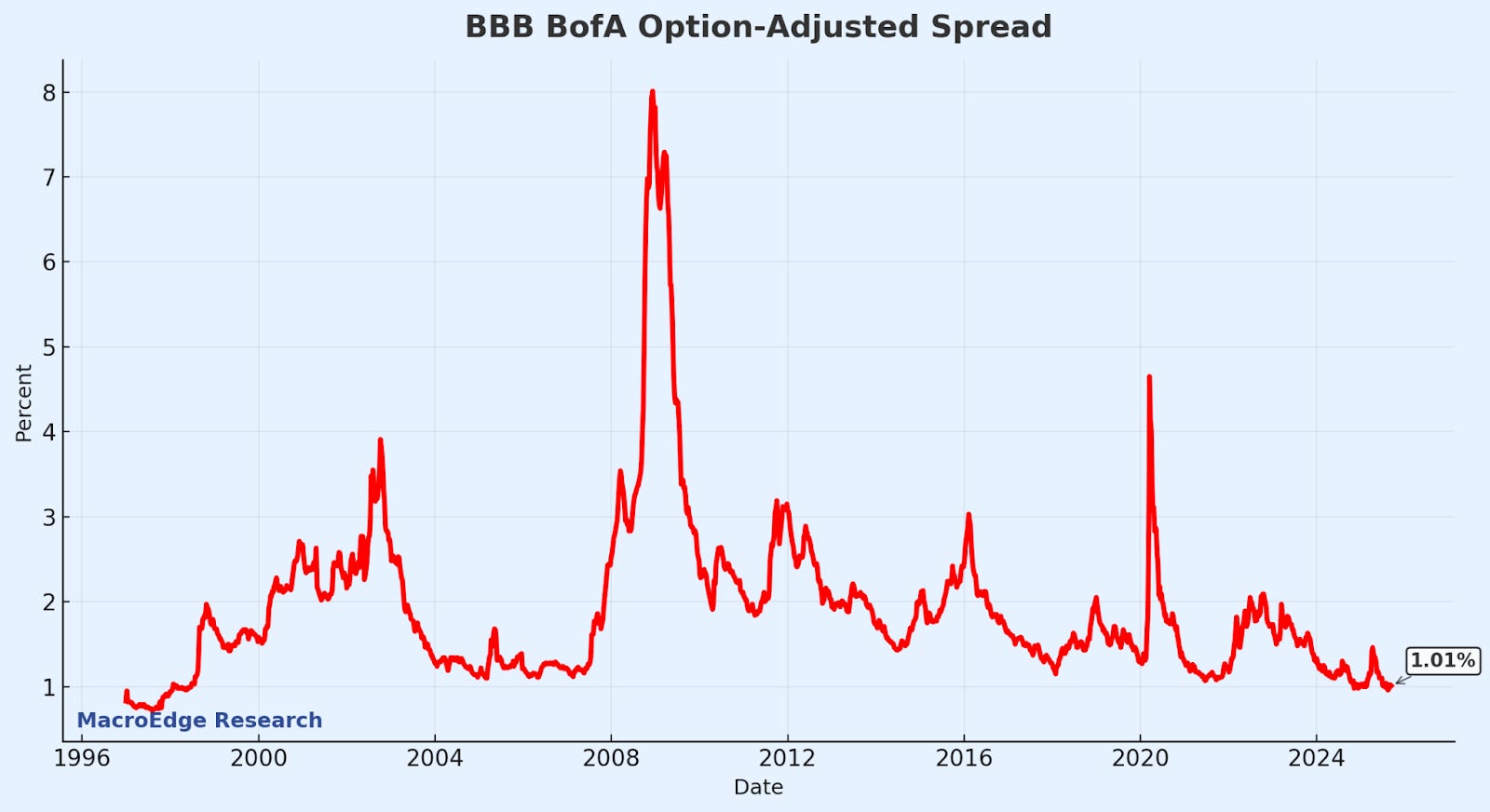

Credit Spreads Reflect a Complete Pricing out of Risk

When spreads are this low, it tends to be before bad things occur - there is less risk priced into credit markets now then prior to the GFC, and we’re on par with the pre-Dotcom spread days.

As someone who is greatly excited by left-tail trading and profiting at the expense of the risk-free behavior of modern market participants. In this zero-sum game and with current behaviors, we’re at peak insanity, a place that precedes opportunity for the people like me and you to make money on their stupidity. If we end up in a ‘new-era’ of risk free markets, yet again, such as in the 04-07 period - then earnings will need to continue to expand, and we’ll need to see breadth broaden out further.

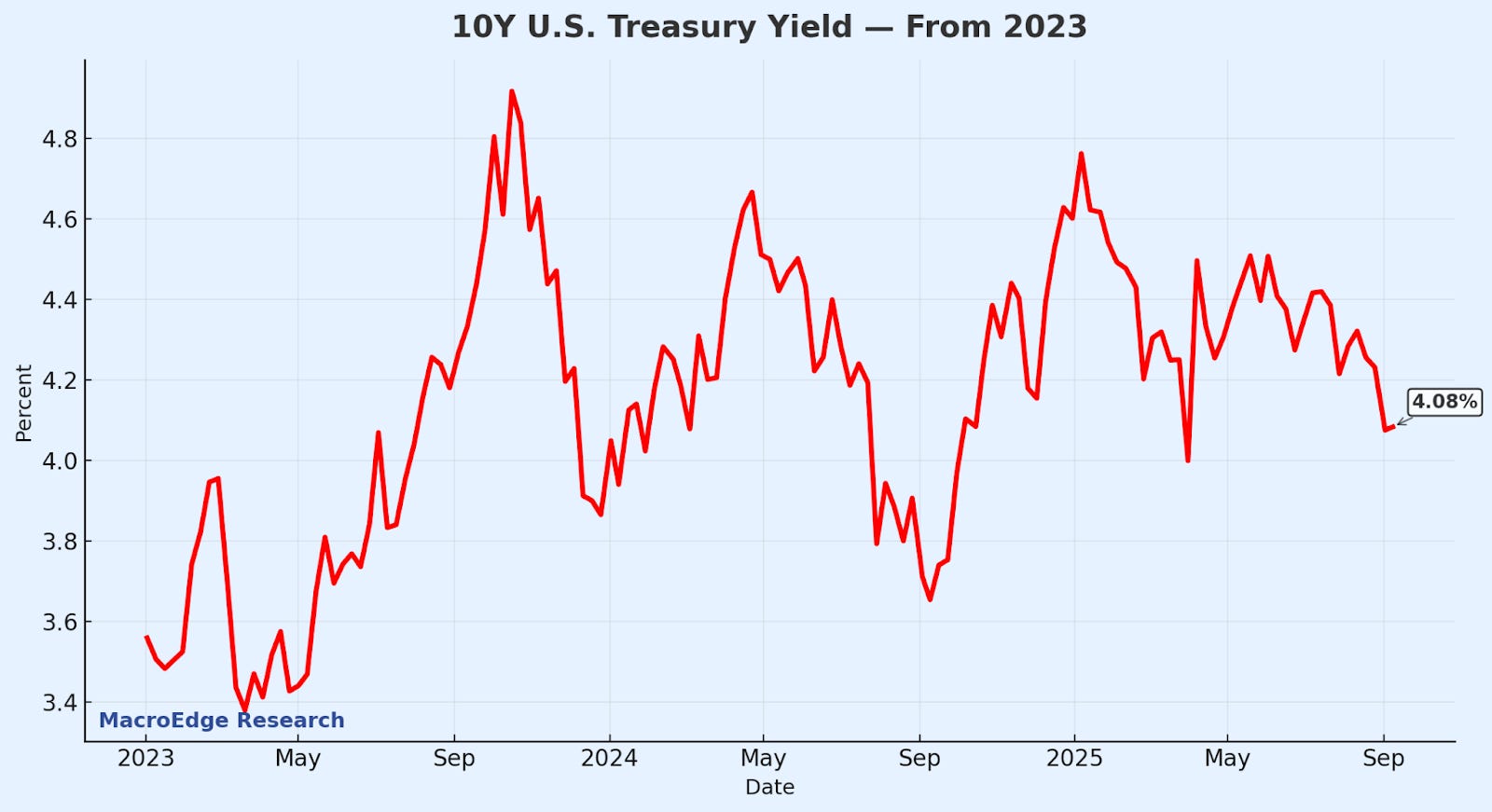

Market is Over Its Skis on Rate Cut Bets

One of the most common ‘rinse and repeat’ trades of the last almost 3 years has been the markets incessant excitement each time we got rate cuts.

The 10Y (above) again reflects some of that excitement, which seems a little odd, because it was lower earlier in the year. For now, if the PPI and CPI come in hot this week and inflation expectations rise, with asset prices continuing to melt up, it could very likely be another intermediate low in the 10Y. If things continue to run hot, the cuts (mentioned and discussed above) will again need to be priced out. The impacts of the inflation wave of 2021-present are now quite clear on the consumer, and if one subscribes to the more traditional view of inflation, eventually it results in demand destruction, and we’re seeing some of that now in limited areas of the macro-landscape.

The Asymmetric Macro & the ERP Trade

While MacroEdge is in the business of ERP integrations (through Transform) - we aren’t public, so I can’t tell you to find us on the public market. The recent strength in Oracle and execution momentum at integrators like Huron is the tell: mission-critical ERP keeps compounding its moat. Switching costs, embedded workflows, compliance, and multi-year migration backlogs lock in durability, while AI copilots and cloud upgrades expand wallet share rather than dilute it. That flywheel benefits SAP and the broader ERP ecosystem because platform demand and implementation capacity reinforce each other, platforms monetize product, integrators monetize time, and both deepen stickiness.

Markets are so expensive right now that we’re patient. If multiples cool, the window opens to accumulate quality at a discount. What we’ll watch in the next few reports: backlog growth and conversion, renewal and attach rates, operating margin progression on cloud ERP, and integrator book-to-bill and utilization. If those stay firm while price compresses, that’s our signal to lean into the platforms and the integrators that make them unavoidable.

To Conclude

MacroEdge is launching Institutional Research to deliver a tighter, professional-grade workflow for allocators, portfolio managers, and family offices. The centerpiece is the MacroEdge Institutional Research Portfolio (MIRP) Index: a rules-driven, cross-asset framework that turns macro signals into disciplined positioning with clear risk bands, live model weights, and monthly plus intramonth updates. First-access trial accounts open October 1, 2025 for a 4-week experience. A new Macro Roundtable is set for Thursday at 9 pm ET with limited Q&A slots by RSVP.

Markets remain expensive, so the playbook emphasizes asymmetry and defensives. Left-tail sleeves prioritized: index crash convexity (VIX verticals or SPX put spreads), high-yield credit stress structures, and regional-bank downside via KRE. Defensives with real upside: gold on persistent central-bank and retail demand, Enterprise Products Partners for CPI-linked midstream cash flows, and KMLM for systematic trend exposure across commodities, rates, and FX.

Inflation’s core drivers are sticky. Services, insurance, utilities, and medical care keep the CPI risk alive; until 3-month core services, median CPI, trimmed-mean, and key subcomponents roll convincingly, inflation risk persists. Housing is a pressure point: mortgage activity barely responded to last year’s easing, affordability is tight, and real home prices are slipping even as homebuilder equities rallied. Credit spreads are near cycle tights, implying very little risk is priced. Rate-cut enthusiasm looks overextended and could be repriced if PPI and CPI run hot.

ERP remains a structural moat. Strength at Oracle and execution from integrators like Huron reinforce platform stickiness and backlog visibility, which also supports SAP. If multiples cool, the window opens to accumulate quality. Watch in upcoming reports: backlog growth and conversion, renewal and attach rates, cloud ERP margin progression, and integrator book-to-bill and utilization.

MacroEdge Institutional Research Portfolio (MIRP): Global Macro Strategy & September Positioning (@SixFinance, Head of Research)

About:

The MacroEdge Institutional Research Portfolio (MIRP) is an unconstrained global macro model portfolio that may invest in any publicly traded security. The portfolio employs the use of leverage and concentration, occasionally to a high degree. The portfolio is absolute return seeking in nature, and will encompass bonds, commodities, currencies, equities, and their derivatives. The portfolio will aim to identify and capitalize on asymmetric opportunities, and become more aggressive as profits accrue. It will look to capitalize wherever possible on securities experiencing substantial inflection points.

The current positions as well as real time execution and trading logs will be available on the dashboard. First positioning executions will be done Monday, building on the below.

Intro:

As tariff legality is sent to the Supreme Court for review, the next leg of the business cycle hangs in the balance. Within the larger context of the fiscal dominance regime, the two components with the largest potential energy for markets remain tariff revenues and interest rates. As the tariffs are estimated to bring in $3 trillion+ over the next 10 years and interest costs now north of $1 trillion annually, a reversal of tariffs would likely also present a stronger economic backdrop leading to higher terminal rates.

Should tariffs be ruled legal by the Supreme Court, we can expect to see a large net fiscal tightening in the form of lower deficit spending by the Federal government via tariff revenues, and less demand destruction leading to the government being unable to bring interest payments substantially lower, leading to higher deficit spending via interest payments.

For risk, momentum is heavily on its’ side. Rising global yields, particularly on the long end of the curve, present a cautionary view, as mortgage rates and corporate financing costs are broadly rising. Global growth continues to be driven primarily via fiscal expansion, despite tepid Real

GDP growth rates, leading to rising global yields and driving financing costs. UK GILT yields are now higher than when Liz Truss was ejected from her role as PM of the UK by the bond market.

Rightly or wrongly, risk assets are near the top of their valuation bands, with broad US equity valuations extremely stretched, global equities rallying in lockstep, and credit spreads compressed to secular lows.

TRUMP ON GDP: BIG YEAR WILL BE YEAR AFTER NEXT:

If we continue to attempt to extract signal factor from the White House’s rhetoric, this can be taken as given as continued validation of previous clues from this administration of orchestrating a slowdown that will allow for refinancing of the Federal debt burden, with OBBBA deregulatory tailwinds and lower interest rates being the rising tide that later lifts all boats.

While the headline rhetoric from the administration remains risk asset positive, the tariffs clearly remain the key lever in accomplishing this financial alchemy and refinancing the Federal debt.

The pricing impacts previously delayed by inventory front-loading are set to materialize with unprecedented force over the next 12 weeks, fundamentally altering the investment landscape for the remainder of 2025.

September 2025 marks the beginning of the pre-tariff inventory cliff as retailers exhaust stockpiles accumulated before tariff implementation. Import volumes are already collapsing, down 19.5% year-over-year as companies shift from pre-tariff goods to tariff-affected inventory. The National Retail Federation confirms that inventory depletion will cause a downturn in trade volumes by late September as holiday season inventories are already in hand.

US Import Volumes

Walmart CEO Doug McMillon recently warned "As we replenish inventory at post-tariff price levels, we've continued to see our costs increase each week, which we expect will continue into the third and fourth quarters". With Walmart's 15 day inventory cycle, the company faces immediate price pressure by September’s end.

As US retailers are broadly forced to re-up on inventory at current tariff levies, price increases will filter through to the consumer, hitting demand in a material way. This is what makes the tariff ruling so important, and also why the economy has appeared to be so resilient in the face of tariffs up to this point. There is little slack left in inventories, and the effects of tariffs are likely to be much more pronounced over the next few quarters should the Supreme Court neglect to strike them down.

Bonds:

Traders piled into US bond shorts this week only to get smoked by a slew of poor labor market data. Traders may be attempting to frontrun and replay the scene from last year when the Fed cut 50 and yields soared. Following this week’s events, US directional bond positions do not appear to present overwhelmingly clear value in either direction. On one hand, there is negative momentum building in the labor market, on the other, a lack of further weakening may lead to a resumption of bear steepening in the curve.

Global yields are moving higher, with Japanese and UK 30 year yields showing interesting dynamics. The Japanese yield curve continues to bear steepen following decades of ultra low interest rates. UK GILTs are now meaningfully elevated at ~5.5%, at the same time as the UK posted a surprise decline in home prices this week. A fiscal left tail still exists for GILTs(price), although this appears to be a reasonable enough spot to start a position in UK duration.

Commodities:

Gold has experienced a continued institutional bid and has broken out of its consolidation to the upside, despite weak participation from retail, evidenced in weak premiums to spot in the physical market. A similar situation is ongoing in silver. These markets have moved so much higher over the last year that chasing the price up here doesn’t appear to be an optimal use of capital, while at the same time the strong institutional bid along with the recent breakout does not present a high conviction short.

Oil has been rangebound in the 60s, and domestic capacity is increasing. This is another market where clear directional value is difficult to find. The administration was quick to react to rising oil prices during the Israel-Iran conflict, and have been vocal about getting oil prices down. This implies a lower ceiling for oil prices in the medium term, absent a larger geopolitical shock that the administration is unable to contain.

Currencies:

USDJPY presents one of the most interesting pairs at present. The Japanese yield curve continues to bear steepen, while the US readies for a renewed rate cutting cycle. Japan has exited decades of deflation and with its interest rate differential with the United States set to narrow, Yen longs present both a quality standalone bet, as well as being a haven and hedge should risk off conditions reemerge.

Equities:

The artificial intelligence boom continues to power the equity rally. Capex remains high and the AI summit showed no signs of weakness in guidance. Technology multiples are now reaching

very frothy levels just as earnings growth is decelerating. Continued capital expenditures will continue to power infrastructure providers so long as capital expenditures remain robust. Rate cut expectations have sent the largest banks into premium valuation territory as the market attempts to frontrun a steeper curve and higher net interest margins. US equities continue to embody remarkable resilience, while AI continues to exhibit bubble characteristics.

Emerging market equities have surged, outperforming developed markets. The earnings growth differential between emerging and developed markets is widening. A fall in the dollar has also bolstered EM dynamics.

Equity volatility remains at relatively low levels as global fiscal spending has improved the broader liquidity regime.

-Office REITs

The commercial real estate office sector has seen huge losses, with delinquencies reaching all time highs, and properties regularly selling for a fraction of their peak valuations. Low rates following COVID drove cap rates to unsustainable levels and years of higher rates have been a tremendous burden on the sector. POTUS has now made clear through his rhetoric that he wants rates down to support the real estate sector, and in August bought $100m in office bonds specifically. Mortgage rates posted their largest one day drop in months following the weak Nonfarm Payrolls numbers. With the White House striking an implied fiscal put under CRE, it appears office REITs are in play.

-PSKY

The merger of Paramount and Skydance has led to the Ellison family gaining majority control over the business. Larry Ellison’s son David has been instilled as CEO, with the two of them controlling majority voting control. The newly merged company has signed a 7 year exclusive deal with the UFC starting in 2026, which can be expected to bolster subscriber count. This newly formed entity and new leadership appears to be a large inflection point in the business, with the potential equity upside being huge should they be successful.

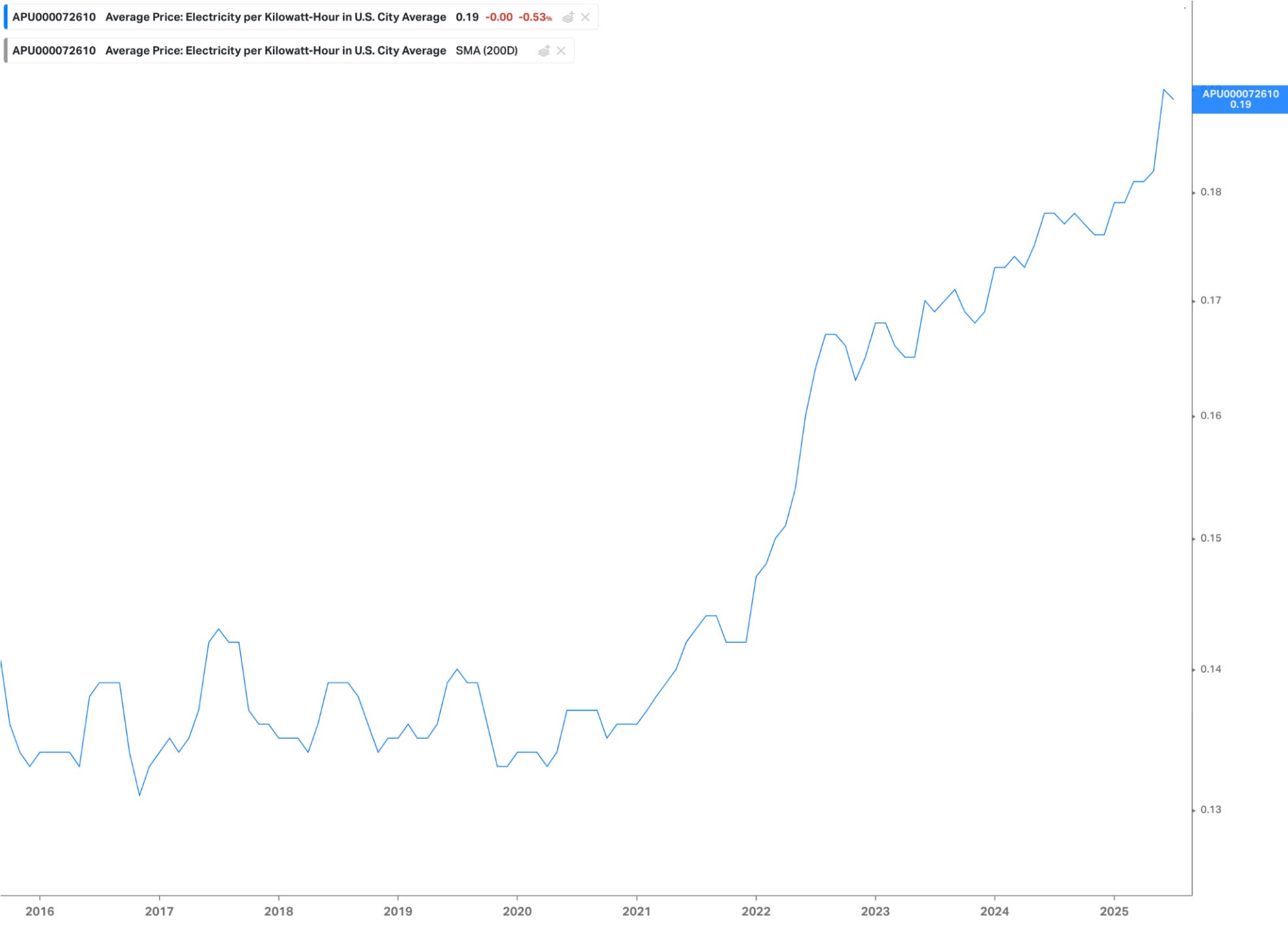

-Solar

As electricity costs surge, solar has put in at least a local bottom following a deep drawdown from post COVID highs. Major concerns in the sector have eased, including the continuation of tax credits, and domestic manufacturing incentives. This is a major inflection point in the sector, and these stocks that are deep in the hole have begun to reprice higher, buoyed by the tailwind of higher electricity prices. Elon Musk is a constant proponent of solar, which all things equal should further help lift the sector out of its trough of disillusionment.

Technically, TAN (Solar ETF) looks about as bullish as can be, and still far off its highs.

(Electricity per Kilowatt-Hour in US City Average)

Long Only Wealth Management Positioning

Within the framework of wealth management style and positioning, and a long only mandate, current valuation metrics present a challenging environment for asset allocation. Equity valuations are in their top decile, statistically shown to have low forward returns. It is quite possible that the technology bubble that is present in artificial intelligence will continue to power equities higher, but should that come in the form of more multiple expansion we would look to continue to reduce equity exposure on the way up. The aim here is simple, to generate high single digit, low double digit returns while smoothing volatility through diversification at the strategic level, as we wait for a fatter pitch in equities to size back into the stock market.

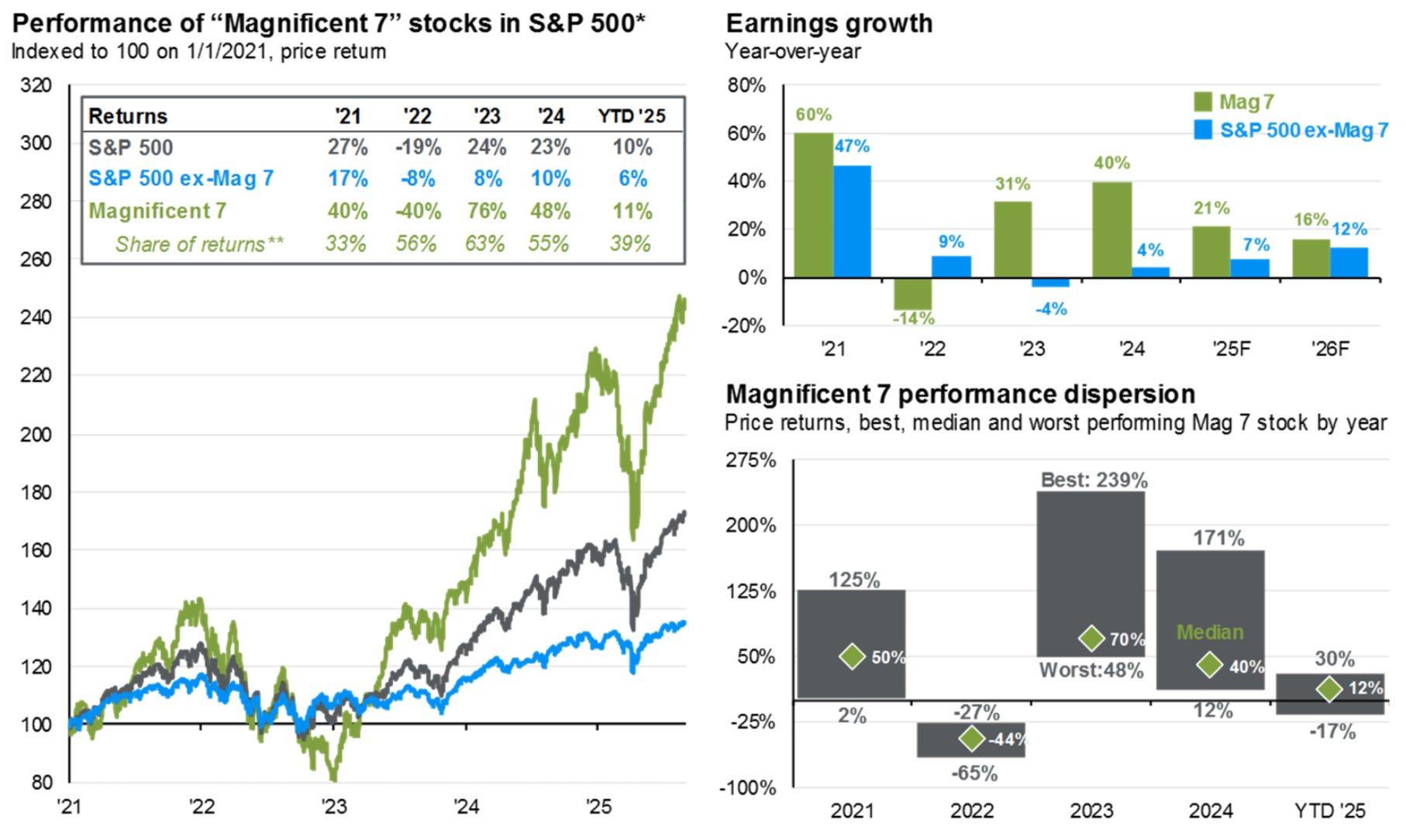

Magnificent 7 earnings growth is decelerating, and these stocks that make up an ever growing share of the index are becoming highly stretched. This warrants much more selective positioning when managing for the medium to long term.

Under these equity market preconditions, a larger fixed income position would historically be warranted. However, the secularly tight credit spreads today do not adequately compensate for the credit risk taken, which also leads to a credit underweight.

In light of these factors, the current long only portfolio, which uses solely ETFs and Mutual Funds, looks as follows.

40% Equities

20% Fixed Income

40% Liquid Alternatives

The equity composition is heavily tilted towards lower valuation metrics, with the equity anchor fund being Oakmark, with a track record of beating the SPX since inception in 1991, and a sub-13 PE ratio across its holdings. HAWX is currency hedged international exposure, which neutralizes foreign exchange fluctuations and isolates the performance of the equity holdings. This is useful during the current period of deglobalization and heightened uncertainties around the path of currency pairs.

OAYMX 20%

RDVY 10%

HAWX 10%

The fixed income component is a composition of senior loans with higher seniority in the debt stack, and a top rated high yield fund.

SHOYX 10%

SRLN 10%

The liquid alternatives side of the portfolio is intended to provide exposure to alternative strategies that have very low correlation to the business cycle. QDSIX is a collection of hedge fund strategies that have shown equity-like returns since inception with low correlation to SPX. BDMIX is market neutral long/short exposure and leveraged. CBYYX is a catastrophe bond fund, whose category has outperformed high yield over the last decade, yet is correlated with the natural disaster cycle, not the business cycle, while yielding more than junk bonds currently, further diversifying the exposures across the portfolio.

QDSIX 20%

BDMIX 10%

CBYYX 10%

This portfolio will be rebalanced by us typically monthly, but if no changes are warranted it will not be rebalanced. By the same token, should conditions warrant a change, an intra-month rebalance is possible.