MacroEdge Espresso Hour: Labor Data Continues to Frost Over as Summer Approaches, Equities Love It, The K-Shaped Economic Dynamic

Don and John dive head first into the cooling employment data, why equities are loving it, and John discusses the k-shaped economic dynamic shaping up in the United States, this cycle. #TeamMacroEdge

MacroEdge Update, Labor Data Continues to Frost Over/Equity Love Session (Don @DonMiami3)

Happy Saturday afternoon everyone -

We’re calling this quick update the ‘espresso hour’ since it’s the perfect time of day for it and there’s some important labor market data from the past week that we haven’t yet covered.

I can also give you the latest updates on MacroEdge… The latest Ozone data dashboard updates have been made - and the dash now includes the KC Fed Employment indexes and international unemployment data from other countries facing similar labor market woes (like Canada and New Zealand). When you load this in your account page for the first time - it may take about a minute to load in the new iFrames - so patience is appreciated as we continue to expand our data coverage. The MacroEdge Radio page is now live on the MacroEdge site and MacroEdge TV will be coming for all Ozone members in the coming months (our own in-house production team talking all things economic and financial data). We have discussed making a shift away from X Spaces given all of the technical issues on the X-end lately, but haven’t decided on a substitute so we’re leaving things be for the time being. It also makes sense with our largest audience being there to keep things put until a better platform alternative for audio is found.

If you haven’t joined us on MacroEdge Ozone yet - join us for two weeks at:

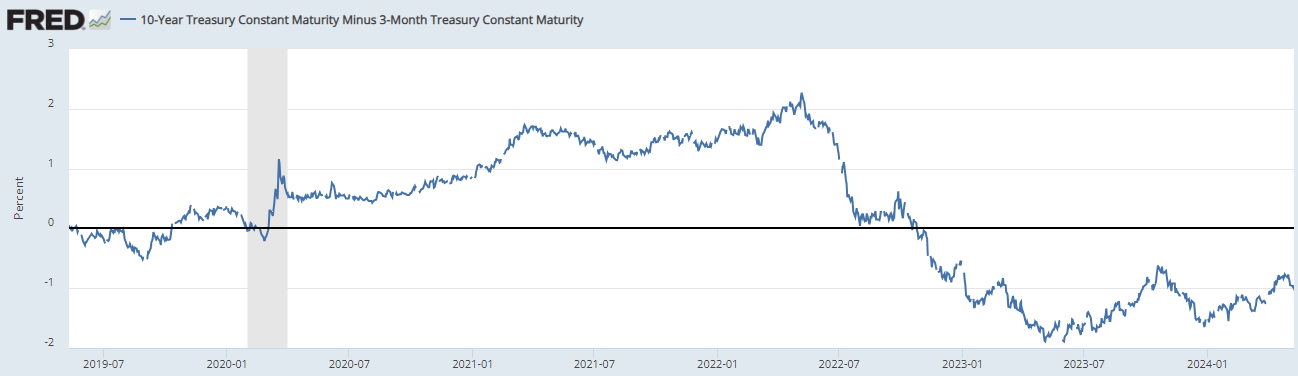

Today we’ll focus on the 10y3m curve, the latest employment data, and a short bit on the equity rally.

The elusive ‘un-inversion’ of the 10y3m curve remains nowhere to be found:

This will either occur when the long end (10Y) blows out or the short end falls on rate cut expectations (3M). For now: policy will remain in its restrictive stance as the curve signals. Of course, with most focusing on equities as their sole gauge of economic health and reason to ignore broader data (like the employment data below), this doesn’t mean the cycle isn’t playing out in a variety of data outside of markets. We’re seeing softer data in real estate - particularly on the construction front, in all leading employment indicators, with the one exception being the KC Fed Momentum Index (which rose on lower Challenger Job Cuts in April - as they vastly undercounted retail job cuts). The more likely scenario here continues to look like Fed cuts - over hikes - given the employment data. Global CBs will likely start cutting next month, as well, with the ECB leading the way based on their policy talk in the last 2 months (and cooler inflation/employment data).

Consumer Confidence (measured by UMich) dropped sharply on employment fears and rising inflation concerns among those surveyed:

As John highlights below in his piece - a vast majority of Americans clearly aren’t feeling optimistic about the ‘equity rally’ or ‘incredible economic growth’ that consensus economists and media firms continue to parrot. The drop recorded from March to April was one of the largest on record on a month/month basis (a 7-sigma event as highlighted by Theya Advisors).

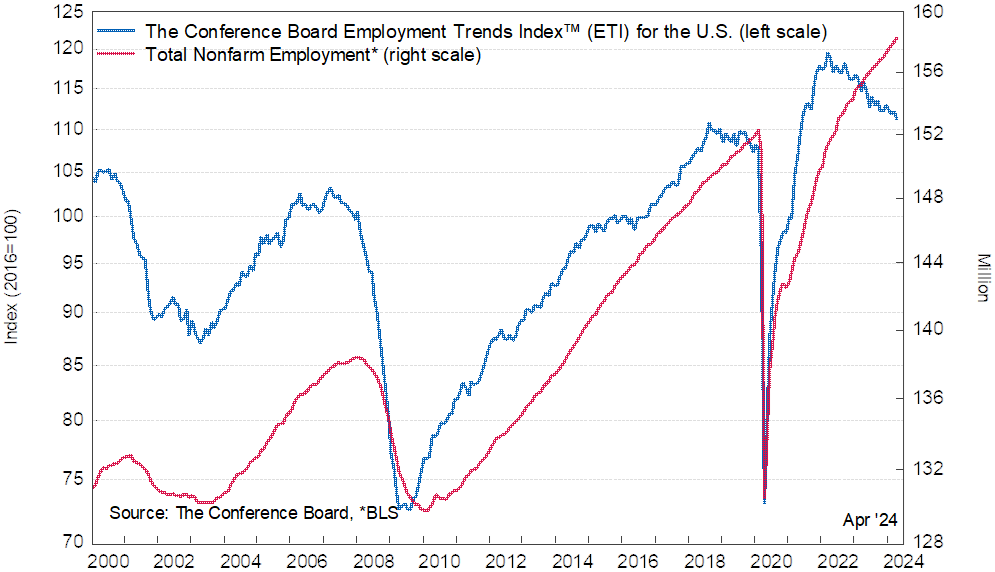

Conference Board Leading Employment Trends Index and KC Fed LMCI below, highlighting the same trends of underlying cyclical labor deterioration:

KC Fed LMCI 3MMA by MacroEdge:

On the labor front - we continue to wait for a Fed cut/cuts as the signal of acknowledgment on weaker labor market data. This will, of course, occur after we see the weaker labor data since the Fed is no more forward-looking on employment data than we are. The worst labor deterioration follows Fed cuts on a 1.5-2.5 year timeline. The unprecedented modern inversion also signals a substantially longer than average period of employment market woes (based on the historical data) - the big question mark this cycle is how the Fed/Congress responds to weaker employment data…

With the April correction having been mainly wiped out by the low-volume rally of the last week, I thought Six - our head of research - summed up the equity market dynamics nicely on MacroEdge Radio #7. Looking underneath highlights continued weakness (particularly in software and semiconductors) and the recent Dow rally has been driven in large part by XLU (utilities). Precious metals continue to rally and the RINF inflation ETF is well elevated from the Fed pivot (still!), even with oil having pulled back sharply. The VIX has been smashed back into the ground and with rising employment risks - the markets face continued risks ahead. The overall markets will respond positively to bad data until the bad data becomes too bad to ignore (as seen with the latest initial claims print)…

… and equities don’t mind this. (Initial Claims < 300,000 even in the gig era, also continues to be one that we’re watching closely with the MacroEdge Job Cuts Tracker advancing to new data series highs). Highest Initial Claims (SA) print in 8-months:

Let’s see when sentiment sours (which should align with equities rolling over), and assess the Fed/Congress response as these things continue to evolve (as they may impact CPI, DXY, the 10Y etc on a longer run basis):

Hope you all have a great Saturday afternoon and make sure to thank your mothers tomorrow,

Don

If You See Kay: The K-Shaped Economy (@RealJohnGalt)

There is nothing better than finally finding a way to tie an April Wine song into modern monetary theory and the state of the economy in the United States this year.

As wildly immature as it might sound now, that song was considered offensive in 1982 and collegiate professors wanted it banned on the college radio station. Needless to say, there were lot’s of requests for it during finals.

Now that I’ve bored my readers with old boomer music memories, just how does a semi-hard rock band from the 1980’s relate to the recession this author thinks our nation is now mired in?

If you see:

It has been a day or two since the financial used car sell you a quality equity media used the “K shaped” recovery term, but at this moment in time, it is totally appropriate.

The upper 25% of the population is getting by fine or thriving.

The lower 75% of the population is living paycheck to paycheck, missing house, car, medical, insurance, and probably credit card payments also.

All one has to do is review the headlines or read quarterly reports from banks and credit card companies:

Gen Z lean on credit more than millennials did and racking up more debt

Credit card debt: Renters and poor people are falling behind

Auto loan delinquencies keep going up: What to do if you can’t make car payments

Auto lenders see consumer loan challenges in 2024

Medical industry increasingly refusing to perform surgery until full payment. What can patients do?

Their first baby came with medical debt. These Illinois parents won’t have another

15 million Americans still have medical bills on credit reports

‘Buy Now, Pay Later’ Has Americans Racking Up Phantom Debt

A payment method that some call ‘phantom debt’ just hit a new record

Those stories are indicative of just how bad the situation truly is for the lower and middle class and now it is getting worse. Inflation is hitting affordability for everything from car insurance, homeowner’s insurance, medical treatments and even buying food for the dinner table.

Concerns Grow Over Food Affordability Amid Biden’s Economic Optimism

Food Affordability Crisis Looms as Farm Bill Debate Heats Up: Millions at Risk of Hunger

‘We’re barely able to keep enough food on the shelves’: Food banks brace for summer

West Texas Food Bank sees longest line for food since pandemic

Inflation cuts donations to CT food banks, while pantry lines grow

I do realize that “list” articles are boring but so are some of my geeky chart articles. But those stories are the right side of the “K’ to the downside. The destruction wrought by 24 years of absurd economic policies and abstract theories being applied to save the politicians and financial elites is now coming home to roost again; just like the 2008 crash.

Meanwhile for just a small sampling the stories reflecting the upward side of the “K”, please, enjoy. And try not to shed too many tears for people enduring problems like this in their lives, money is stressful.

Bark Air promises a first-class ride for your pet — for a hefty fee

They Love Their $14.95 Million Hamptons House. The Problem? Their Dog Hates It

Woman seeks help after cleaner used bleach on her gold toilet bowl and left unremovable white stains

That’s a tough one there, can’t help ya babe.

Then there is this classic from Don at the Miami F1 race this past weekend:

Without going on and on about yacht prices, expensive car issues, and how people are bitching about first-class being removed from most domestic flights (that one sucks btw), I think our readers get the idea.

The majority of people are crashing and burning and if their 401Ks do also, the upper 25% do not care.

America is about to endure another recession after these mini-three to four month ones, so get prepared for the worst as the financial institutions and government’s ability to fund itself are going down with everything else also.