MacroEdge 8/30 Redeye Report: A Pre-Flight Look at the August Labor Market Report (Labor Market in Stall Mode)

Our longer term view of the labor market remains unchanged - as it has since August of 2023. We discuss hiring trends, job openings, unemployment levels, and more.

Good holiday weekend to our readers and community,

As we head into the long weekend we wanted to leave you all with some charts and data into the weekend as ‘cycle exhaustion’ remains very high and things get busier post-Labor Day. Hopefully, you are reading this from a beach, or your couch, or somewhere unplugged from work - if not, I get that too…!

We’ll keep this one short since our next MacroEdge Ozone Weekly report for Monday evening will be very long and in-depth on the larger labor market trends, volatility trends, and final few weeks heading into the newest and ‘shiniest’ easing cycle which has hopes high for the mythical soft landing that has now been discussed for 24 months. Catch the latest update and more from our team in the coming days - particularly for our new real estate team being rolled out - with MacroEdge Ozone access for two weeks:

This evening we’ll skip past the ranting about ‘soft landing delusion’ and ‘why it’s not like 95’ and focus on the core areas of what will drive our employment forecast and employment outlook for August and beyond. Even in the face of falling unemployment last year (late Fall) we continued to hammer the point of ‘respecting the lag’ and waiting for monetary policy to transmit into the labor market - and monetary policy continues to do so. We anticipate the largest effects of monetary policy hitting the labor market once easing begins. Note: Payrolls do not need to contract for an economy to enter an official recession (see 1974 as an example) - but we are losing the tailwind of the huge migrant numbers + worsening job openings outlook that will result in the labor market weakening continuing for months to come.

Tonight we’ll focus on some of the key cyclical employment areas (trucking, construction, manufacturing, information, leisure/hospitality, real estate and retail)

& non - which have been the remaining drivers of employment growth through the summer (government, healthcare, social assistance).

The Overall Employment Picture

The overall employment picture is one of a cooling labor market nationally. Unemployment rose in 90% of MSAs y/y in July and in a majority of states. Total unemployment levels rose in July as well, with a larger jump than in previous months when the labor market was cooling more gradually. Job cuts were elevated - as measured by our gauge - >100,000 - indicating continued pressure with business closings and large companies laying off employees. In the broader picture of slowing growth for both the Household and Establishment survey, in the context of rising unemployment, we continue to believe that the Fed is behind on employment and in a bind on inflation (a two-tailed risk with inflation/deflation). While payrolls have remained positive, if we dig beyond the headlines (and the establishment survey) we can see that the labor market has been weakening since November 2023 more broadly, with cyclical sectors showing cracks even earlier than that. The fact that were on to more desperate narratives to shield the labor market from more obvious cooling data have been entertaining, to say the least. We’ve seen everything from the Sahm Rule doesn’t work with migration to a Category 1 Hurricane in rural Texas causing the 20bp jump in U3 and 40 in U6.

We think the tailwinds are leaving the sails from the non-cyclical sectors now too, which means slower payroll growth in the months to come (establishment headline), and a continued trend in the cooling of the numbers in the Household survey (which peaked in November 2023). We’ve already discussed our thoughts on the asinine 818,000 revision from the BLS (which they released late) and why that represents a larger issue for labor market data tracking in an era where the market reacts to the first headline and no one believes anything. The worst case scenario and largest scenario out of their control would be one where they lose control of both the labor market and financial markets - one that isn’t too far off where we are now. (As mentioned above, you don’t need contracting payrolls to be in a recession as evidenced in 1974). From the economic perspective - our base case remains a prolonged economic and labor cycle with the Fed having more limited firepower than in previous instances like 2020 due to recency concern about inflation and the risk of creating a ‘lost decade’ scenario in the context of a spiraling fiscal environment and global economic weakness.

Below, you will see the winds coming out of the sails of the labor markets, in a similar fashion to Summer 2007 and early 1991 - and very unlike 1995 (as we wrote in our ‘Why It’s Not 1995 note, a quarter ago).

Got record-long inversions in 95? Nope!

The Cyclical Sectors (trucking, construction, manufacturing, tech/information, leisure/hospitality, real estate, retail, airlines, banking):

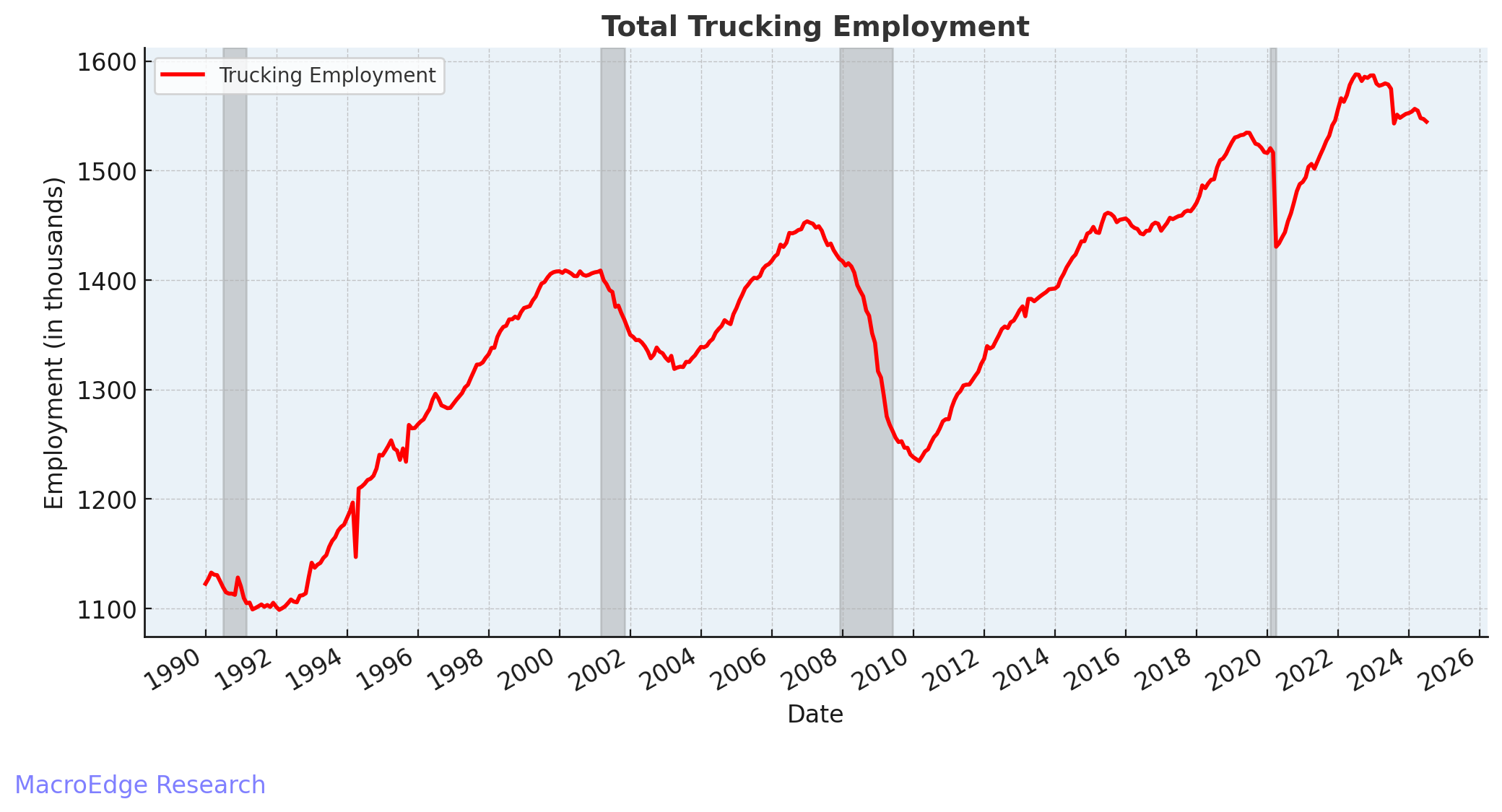

Total Trucking Employment:

On a year/year growth basis view:

Total Construction Employment:

On a year/year growth basis view:

Manufacturing:

On a year/year growth basis view:

Technology/Information:

On a year/year growth basis view:

Leisure and Hospitality:

On a year/year growth basis view:

Real Estate:

On a year/year growth basis view:

Retail:

On a year/year growth basis view:

Airlines:

On a year/year growth basis view:

Financial Activities:

On a year/year growth basis view:

The Non-Cyclical Sectors (Government/Healthcare, Assistance)

Government:

Healthcare/Assistance:

May marked an inflection point across both cyclical and non (private and non as well) and the trends are starting to roll down the same track. I’ll have more on this in our in-depth deep-dive in the weekly report, but we still have some numbers and data to work through.

We’ll dive in deeper in the Monday night weekly Ozone research report, but until then, respect the lag and have a great Labor Day holiday weekend. You should get a clear idea of the trend from the above. We’re at maximum employment with a market that wants to make new highs on any positive data point to confirm what pundits are pushing at the banks and over the airwaves, and a similar repeat of past cycles could see new highs materialize through an employment shock delivering a blow to markets. Until then, we’ll continue to navigate the complicated data landscape and Six will have a great update on Vision on Monday.

See you in the Ozone for much more on our August outlook and market thoughts, and until then… the stars appear for further labor market cooling into the winter months.

— Don

Chief Economist, MacroEdge (Don@MacroEdge.net)

The future of finance and economics is here. Welcome to our #UrbanEconomics vision.

Great stuff as always Don. Appreciate the breakdown of the various labor components 🤝