MacroEdge 10/11 Redeye: Claims, Coal, Canes, and More

A midnight special from our Chief Economist covering coal (and inflation risks), the MacroEdge Job Cuts Tracker & Claims, why the economy hasn't landed, Nasdaq performance, and more. #MacroEdge

Good (very early) Saturday morning everyone,

I always enjoy these brief weekend Redeye notes, as we call them, since they provide everyone with some useful food for thought over the weekend. Hopefully, you find this one just as helpful. I started this edition of our notes when traveling extensively and writing from various planes and airports… how far we’ve come since then!

I won’t ramble or rant too much and we’ll stick to covering some data on coal/inflation, the evolving employment situation, and hurricanes. This note will be available to the entire community - so hopefully you enjoy the content and don’t forget to pass it along if you learn a thing or two - or see a visual that strikes you as useful. With much of the focus over the next 5 weeks going to be on the election - that will take the driver’s seat for most Americans (including likely markets for a short period). This was evidenced this week as markets ignored the bad data completely and continued their ascent through the close of the markets on Friday. Much of this continues to be the period in which the market hasn’t priced in either a hard or soft landing scenario (see more below) which will be determined by employment data.

Below you’ll see where we are planning to end the year - we’ll be changing a few things up as well go and also expanding MacroEdge TV with new content, interviews, and short-form ‘Reels’ for other platforms that readers have requested. Before the transition to a broader spectrum of offerings, access MacroEdge Ozone today (which currently includes Vision) for two weeks below:

Welcome to the future of financial and economic research.

This evening we’ll dive into a brief employment discussion - on Claims, Hurricanes, and the MacroEdge Job Cuts Tracker. We’ll also briefly touch on coal and the CPI risk. We’ll lastly touch on the continued Nasdaq outperformance, and the election boon (clownshow). Hopefully, if you are in the affected area from Milton on the West Coast of Florida you have power back now and our team’s prayers and well wishes go out to all of those who bore the brunt of not one - but two storms in a short period. Certainly not a fun thing to endure but Florida has a resilient populous.

Employment Discussion (Claims, Hurricanes, and the MacroEdge Job Cuts Tracker)

While the risk for commodities appears to be rearing its head in some ways (particularly on the energy side of things - which can significantly impact economic activity and consumer spending) - this section of my market note will discuss the employment situation. While the September labor market surprise is now in the rearview mirror - the market has reacted positively since then (and also ignored the Claims & hot CPI data this week). The election force as well as 50bp optimism, with organizations and business leaders declaring a soft landing, has resulted in new cash deployments into risk assets and equities - even though we’re still seeing substantial struggles in housing and employment.

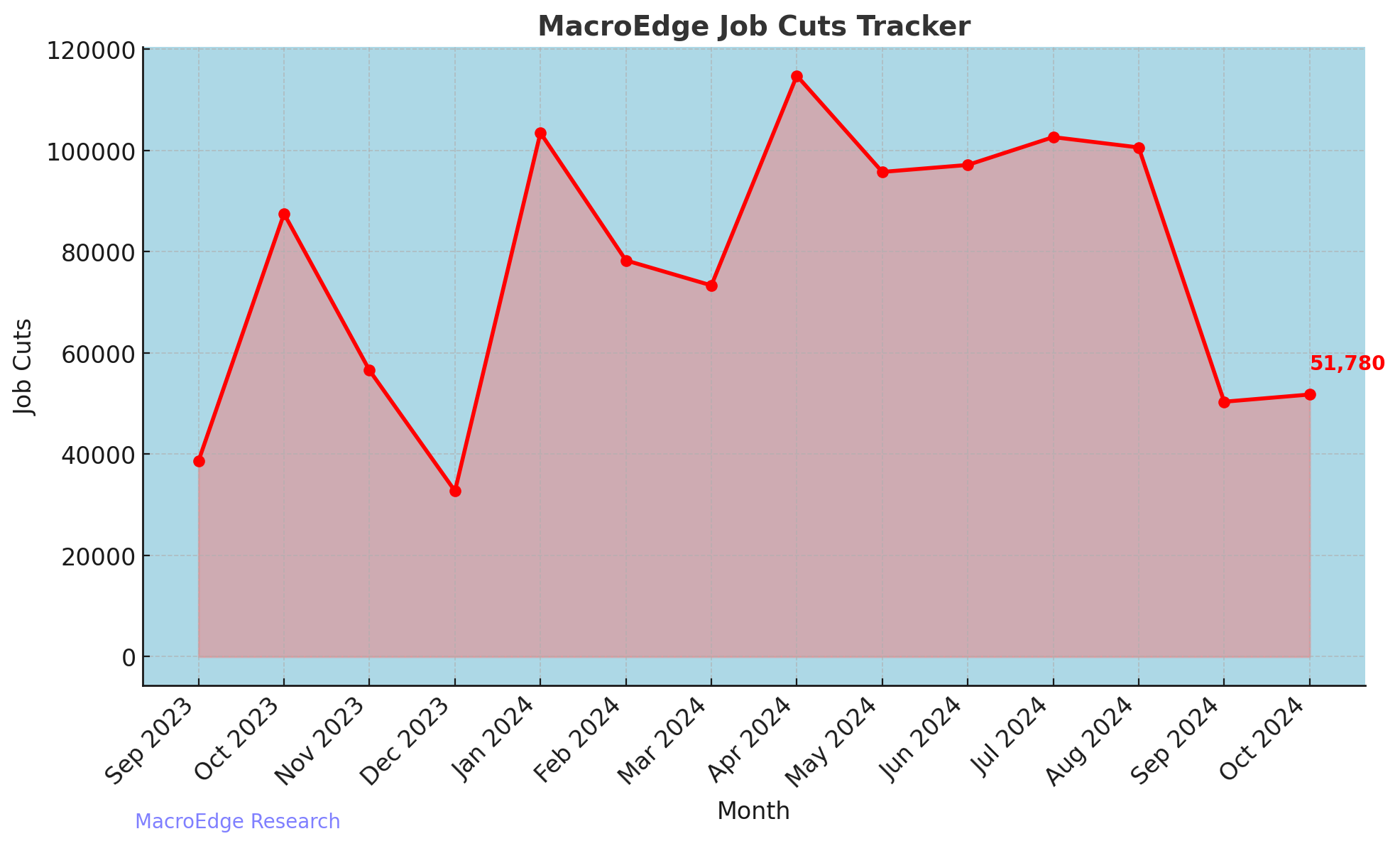

Job cuts this month - as measured by the MacroEdge Job Cuts tracker - are off to a hot start for October - particularly on the heels of a very large layoff at Boeing (~17,000) employees, another 1,100 at Stellantis, and ~2,500 at CDW just from today alone. Cabinetworks also contributed with another 400 - and also highlights the continued struggles in a very slow housing sector. We expected job cuts to jump this month given the seasonality of cuts within weaker employment markets historically - and we’re on pace to finish substantially higher than September given that it’s only the 11th of the month.

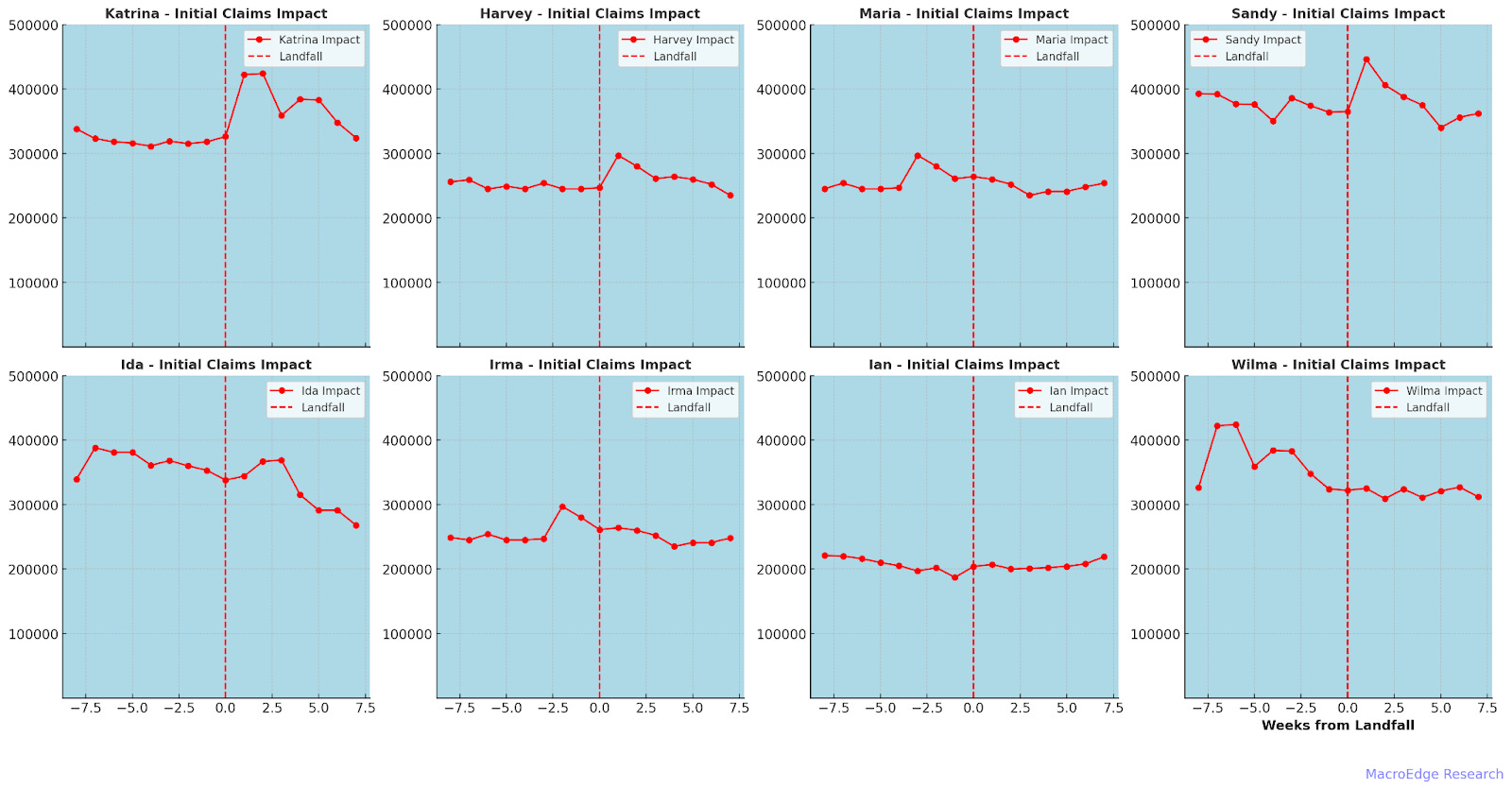

We’ll continue to update the labor market situation as the month evolves. Notably (and as predicted on Wednesday in our Midweek Report) - we saw a substantial increase in both Initial and Continuing Jobless Claims. While some of this jump can be attributed to the hurricane, that is not the full story here.

Large jumps in claims were seen in states outside of the hurricane-impacted states (NC hit the worst in the Claims state-level data), highlighting continued labor market weakness. We may also get some residual from Hurricane Milton stacking on here over the next two weeks as well:

Both Continuing and Initial Jobless Claims are moving as seasonally expected now, bottoming in late September and advancing higher - and if layoffs continue at the current clip I expect that we will see over 2 million continuing jobless claims come winter-time.

Job cuts usually lag claims by ~3 months.

The market shrugged off the fact that Initial Claims hit its highest level in a year, while Continuing Claims surged back to the highs:

I am not going to put the cart ahead of the wagon here, which is why we should take into account the slow nature of monetary lag impacts for past cycles as well (especially as the curves continue to remain broken), so read below and see the below visual.

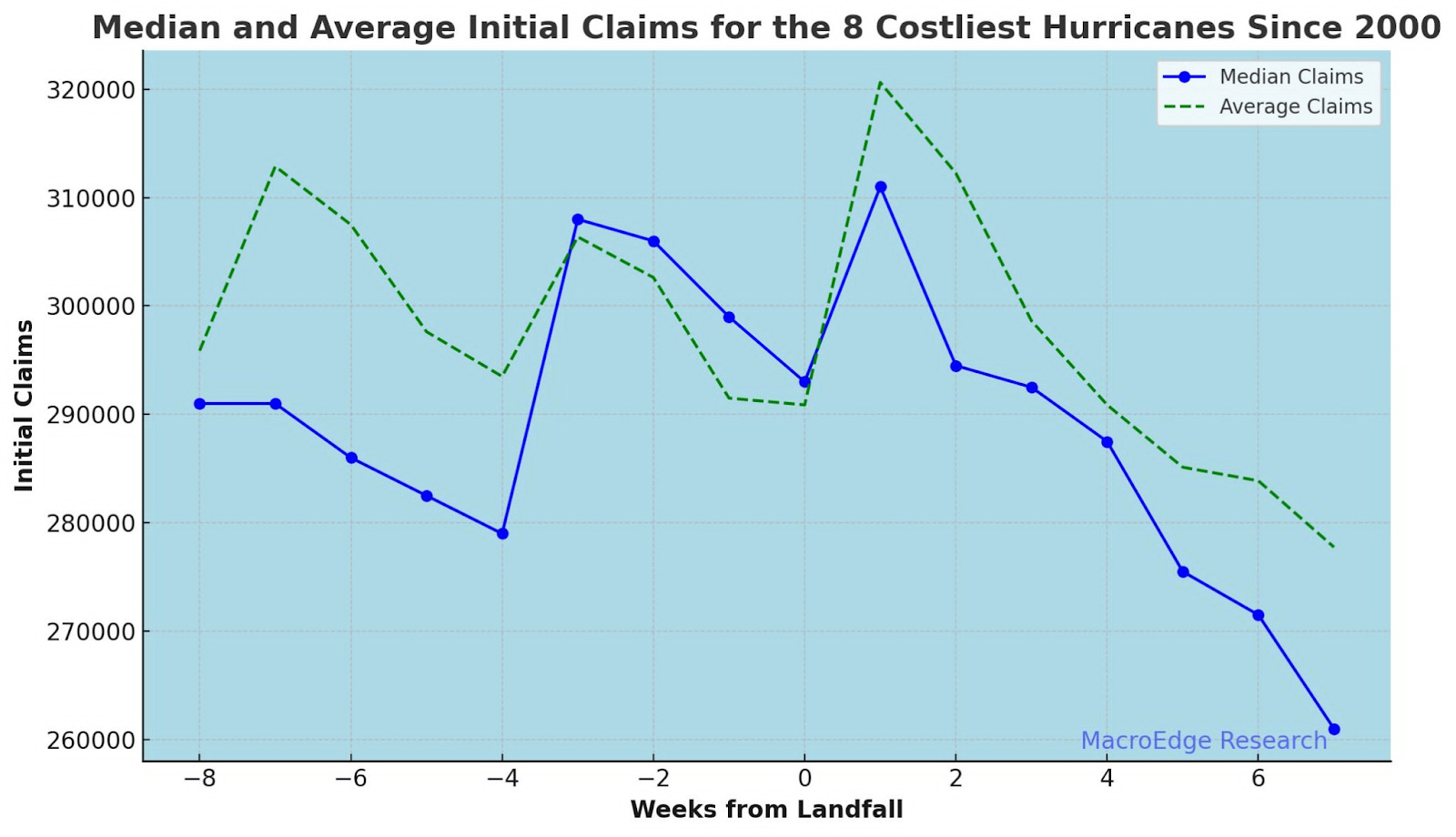

We’ve also maintained that we should continue to be patient and wary of early landing conclusions - as claims tends to be a post-rate cut story - something that just began ~3 weeks ago. We can now add the current cycle to our graph view (which you can find at MacroEdge.net/data):

Claims rise in hard landings, and stay largely sideways in soft landings - that’s where Continuing Claims (as well as U3/U6) come into play:

Oh, and job postings are seeing little sign of relief (recall that monetary easing takes a long time to get in motion as it pertains to labor and attributing the fall in unemployment in September to easing, is simply false):

Job postings look similar to the H2 2022 period, but we’ll keep a close eye on them through winter. It certainly is not an advantageous environment for those in the labor market - especially in white collar, and will remain a difficult market for some time, especially with AI and outsourcing effects.

Coal & Inflation (Continued from Wednesday)

Some inflation risks appear to be rearing their head again - particularly on the energy side - which matters most for the economy. Something I am keeping an eye on - along with oil and natural gas.

MacroEdge Vision’s update on Wednesday provided an update to several new positions here related to coal.

Nasdaq 50bp Kick Continues

As anticipated back in our early September releases and notes - the 50bp optimism (and euphoria) continue to drive much of the optimism behind the rally that we’re witnessing:

Notice how the market prices in concerns around 2-3 months after it sees labor market woes - historically (of course noting that the sample size of hard landings is small). In soft/no landings - markets tend to rally and end a 12-month ahead around 25% higher than first cut.

While the rally and excitement continue and election distractions are dead ahead - the direction of the landing will be priced in when the market has deciphered where Claims will go. This is usually a few months after the first cut in modern cycles (in both hard and no-landing instances)

Hurricanes have no direct impact on financial markets (while having huge regional and national economic implications), which you can view in our Wednesday note.

We’ll have so much more to cover on Sunday with real estate, rising yields, inflation risks, and more - hope to see you there. If you missed MacroEdge Radio #23 - you can find it on our YouTube channel next Wednesday morning & every Wednesday morning. For now - it’s still too early to determine the landing in all of the fog, just my two data-driven cents.

Have a great weekend,

Don - MacroEdge Chief Economist