Labor Market Decelerates to Start the New Year, Economy Shows Signs of Resilience, The Gig is up, The Retail Sales Should Falter with Higher Inflation Fallacy

@DonMiami3, MacroEdge Chief Economist; @SquirtLagurtski, MacroEdge Contributor; @RealJohnGaltFla, MacroEdge Contributor

Labor Market Decelerates to Start the New Year, Economy Shows Signs of Resilience (@DonMiami3, MacroEdge Chief Economist)

Happy end of January everyone - welcome to another weekly report from the team. While the number of job cuts has increased this month, the overall economy continues to be quite resilient as we await the Fed’s first hint of interest rate cuts (likely to begin in March or April at the current pace).

The 10Y3M curve remains steeply inverted at -123bps and is on pace to be the second or third-longest inversion in history (since ‘69). In this weekly report I’ll cover the current inversion dynamics, our latest job cuts data, the latest Nevada labor market and casino data, and talk a bit about the latest Conference Board LEI update.

Current Inversion Dynamics

The 10-year 3-month spread remains at -123bps, one of the deepest and longest inversions on record. This continues to point towards a longer recession based on past history of this indicator (a recession >9 months). We are seeing rising unemployment in 49 of the 50 states now with Texas being the only exception to this. We’ll continue to watch this inversion dynamic as the Federal Reserve begins the pivots from the pause period to the rate cut period which should provide some normalization to the curve.

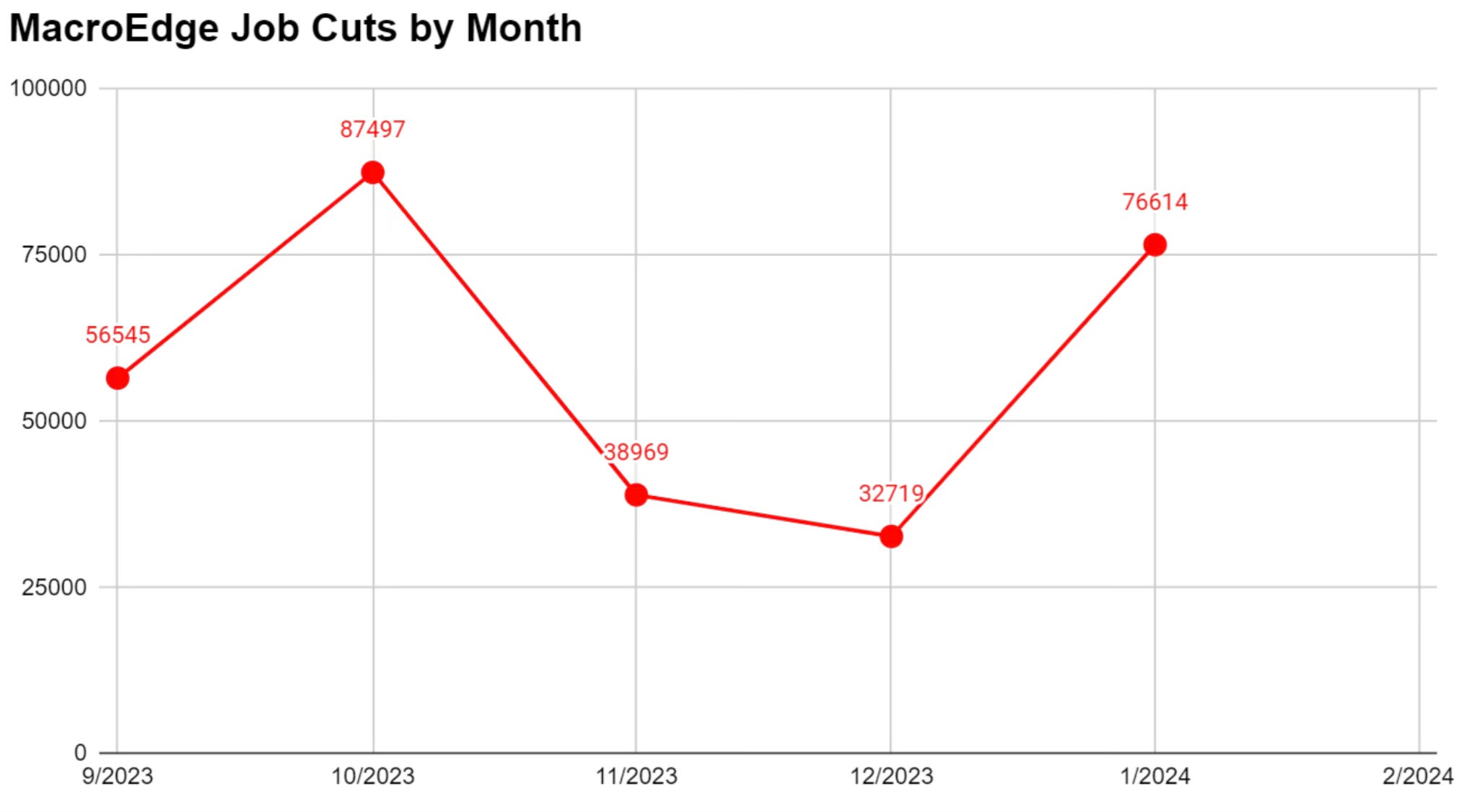

Total job cuts are up sharply month over month (32,719 in December to 76,614 this month) but are still lower than January 2023. The concentration of job cuts continues to be in the technology sector…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

The Gig is up (@SquirtLagurtski, MacroEdge Contributor)

Since 2022 the unemployment rate in the U.S has been hovering near or at record lows of ~3.7% leading to speculation from economists and analysts seeking interpretations of historical trends as it relates to the potential for a recession following record stimulus as a response to the Covid-19 pandemic, and the ripple effects seen in the collapse of three major banks. Can the U.S avoid a recession, will unemployment increase sharply as seen in past experiences, can a recession occur while unemployment remains stable at the lows, all questions that have been included in some form during the discussions between media, the Fed, economists alike. Or is there some other explanation that may lead to a change in the way unemployment data and the greater workforce activity since the pandemic (and arguably before) is used to gauge the health of the overall economy and its many parts.

Recently, talk of the “gig” economy has been the focus of attention due to the substantial growth in gig work (Uber, Lyft, Door Dash, Shipt, and even Airbnb) which has analysts searching for the mechanics which effect the labor force and may be changing how trends develop in the historically niche group. The gig economy has grown substantially

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

The Retail Sales Should Falter with Higher Inflation Fallacy (@RealJohnGaltFla, MacroEdge Contributor)

The financial media has decided long ago that the indicator of strong consumers and retail sales will always serve as validation for the most abhorrent of policies be they inflationary or worse, destructive to the ability of the middle and lower classes to subsist on existing wages and salaries.

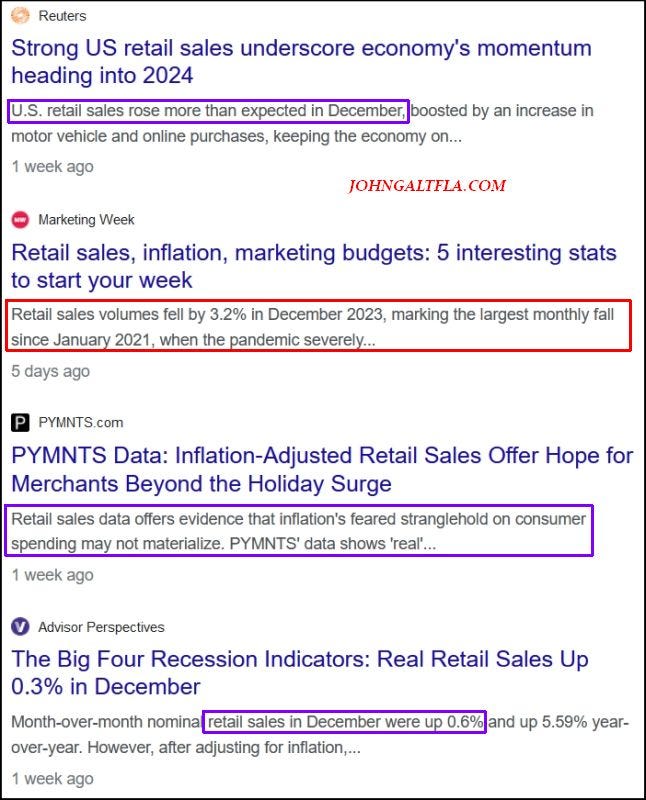

The headlines after last week’s report on retail sales, America’s propaganda based financial media did not fail to disappoint.

Other than Marketing Week, and after all who needs marketing in retail, the headlines outlined in purple indicated that the pump was fine and the American consumer has no problems with inflation, right?

Even the local news media is carrying the water as this story apparently promoted by the National Retail Federation illustrates via WGEM in Quincy, Illinois:

The reality is that retail sales since forever has always been announced by total dollars, not via volume, or net sales per unit. The truth about inflation however is that it aids in the net total or perceived “wellness” of the economy by pumping up the total volume of retail sales in gross dollars.

For example, reviewing the damaging Fed inflation of the 1970’s versus retail sales indicates that even during the numerous recessionary and near recession periods of contracting economic expansion, retail sales for the year increased on a year over year basis. But why?

The answer is simple.

While gross retail sales are up, non-discretionary items (food, fuel, housing, insurance, etc.) are included also in the total. This distorts the reality of the real reason for the increase but why report facts when one can impose emotion on hard numbers if the government tells a reporter to do so? If “sales” continue to rise at a faster rate than the “official” CPI, then of course retail sales will expand because obviously one dozen eggs at $1.99 per dozen is an increase over $0.99 per dozen one year before. The bottom line is still basic math, regardless of the various statistical gymnastics performed by the US government.

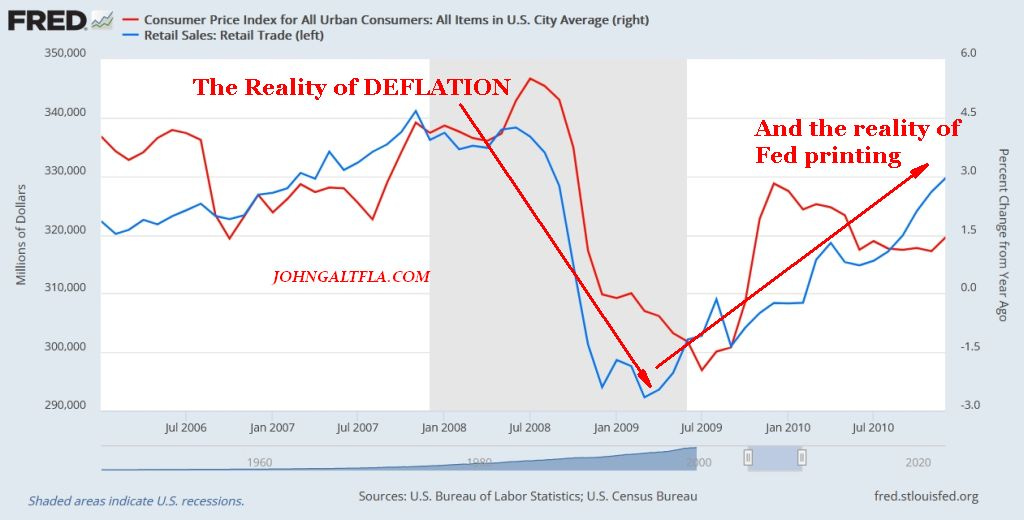

A better example of how real contractions work, where recessionary collapses impose real deflation and reductions in credit availability, and indicate the over dependence on the gullibility of the American consumer was in the 2006-2010 time period.

Note in the graph above that one gets to see what happens when the Federal Reserve loses control, aka, deflation, and then overwhelms the system with a monetary category five hurricane of printing. If the reality of the BEA was to do their jobs honestly and not politically, that shaded area could easily be expanded to Q3 of 2010 when the CPI finally started to increase exponentially again after a full year of monetary insanity.

What it required for consumers however, was an increase in confidence and the belief that their credit lines along with future employment would no longer be threatened before beginning to spend like drunken sailors again.

As the realization that banks and major American corporations would be bailed out by the Fed and government began to hit Main Street, the average consumer rationalized that same extended benefit would apply to them.

Fourteen years after the destruction of capitalism to save capitalism it would appear that the American consumer believes that this backstop will remain true. This is for good reason as the US government, due to political not economic considerations, is looking to backstop bad student loans, home loans, and probably soon consumer credit mistakes.

All in the name to keep the current administration in power and reassuring the ignorant American voter that there never will be a day of reckoning for the banks or themselves in the name of “justice.”

After all, if the hedge funds and banksters do not believe they will ever have to pay everything back, then why should the average consumer believe that either?