Bourbon and Data with Don - A Red-eye Friday Evening MacroEdge Special

We discussed 'Red-eye' as a fun addition to our lineup- and it's especially enjoyable for me to write a lot while I am on the 'fly'. Let's get into the data and pour your favorite bourbon on ice.

Don Johnson (Chief Economist, MacroEdge)

- Wikipedia")

This week I found myself time zone hopping yet again - from time-zone to time-zone to time-zone - keeping the wheels turning on planes, trains, and automobiles… For “Red-eye” - and I am not sure how frequently we’ll be doing these, expect something a little more free-form in nature… Some data, ranting, thoughts, and a conversation between me and you, the reader… Thanks to the 50,000 or so of you who have tuned in to read us across our website and our Substack, here.

As I have the opportunity to travel fairly frequently, it provides a perspective that many either don’t have access to, don’t have the time for, or are not interested in… While I certainly am not one to fall into this modern-day Instagram camp of let’s take half-naked pictures of ourselves, pretend to be important, and simply visit places to put the picture up on the platform to make a few dollars - travel certainly can provide perspective, at the very least. For me - that perspective happens to be one of the economic nature of the different countries and locations that I am visiting - and what I see back home, particularly in the United States, is alarming. Many of us know that the United States (and many other Western nations) are run mostly by incredibly incompetent (I think in many cases it’s deliberate by whoever is bankrolling their campaign) moronic/narcissistic/sociopathic individuals who exist almost solely to get re-elected. This is why each cycle you and I hear the same talking points that have been surfacing every election cycle for the last 40 years.

The moral hazard in the United States has become unfathomably large between the elites, business owners, and their politicians who partake in the circus act. You could write Congressional spending bill-length stories alone on the current intertwining and relationships of those in the political or business classes at the top that pull the levers all of us play by. Platforms like X have done a great job exposing some of the insanity of Congresspeople who are essentially day trading with the information they are privy to with their positions in power…. This is also really no different from Fed officials selling the top of the markets before QT, buying assets when they restarted QE at the bottom, and eventually, we’re just heading towards the BoJ model of the Central Bank outright owning most of the assets and markets (something that may begin after the next cycle).

Moving onto the current economic times and a little discussion on data, I have no doubt that the Fed’s dual mandate will again be ruinous for the middle and lower classes (when the teeth of recession bite again in the near future). What will be even more insufferable for many of us is all of the ‘economists’ and ‘experts’ that will tell us that there was “no way to know what was coming!” and have had trombones to our ears for the last year declaring a soft landing, something they’ve botched time after time. What I am most concerned about from a longevity perspective are things like our middle class in America - which now holds fewer total assets than the 1 percent

(Data figure: Northman Trader, Wealth Inequality Visualized)- the disastrous debt pyramid that we continue to build higher while we dance around celebrating that we’re the reserve currency of the world - and our demographics. All three of these will get dramatically worse with another half-baked economic cycle that will likely require dramatic intervention by the Fed and fiscal policymakers. With the United States already running wartime deficits - one can only begin to imagine what things will be like if they devolve into a COVID-lockdown-style printing frenzy to keep things propped up once the snowball of a labor market downturn begins rolling. Another large dilemma that gets worse after each cycle is the overall apathy or lack of care among citizens about what is even going on. From the top down they will probably throw stimulus checks and debt cancellation offerings to those at the bottom (who will gladly be content thinking they’ve won the lottery with a $1,400 check), the middle will get hollowed out further, and the assets at the top will get propped up by every aggressive Fed and Fiscal policy tool imaginable. Some may think this is the cynical perspective on what will take place - but it’s merely based on our current trajectory and history going back decades.

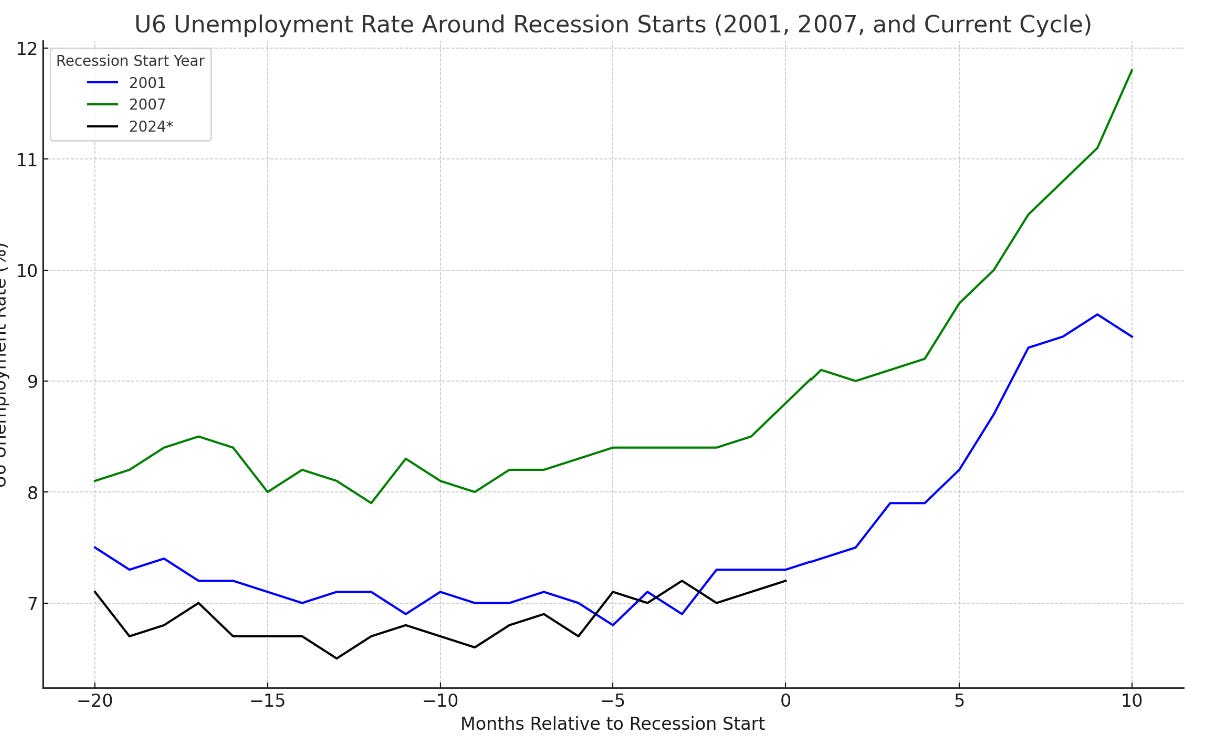

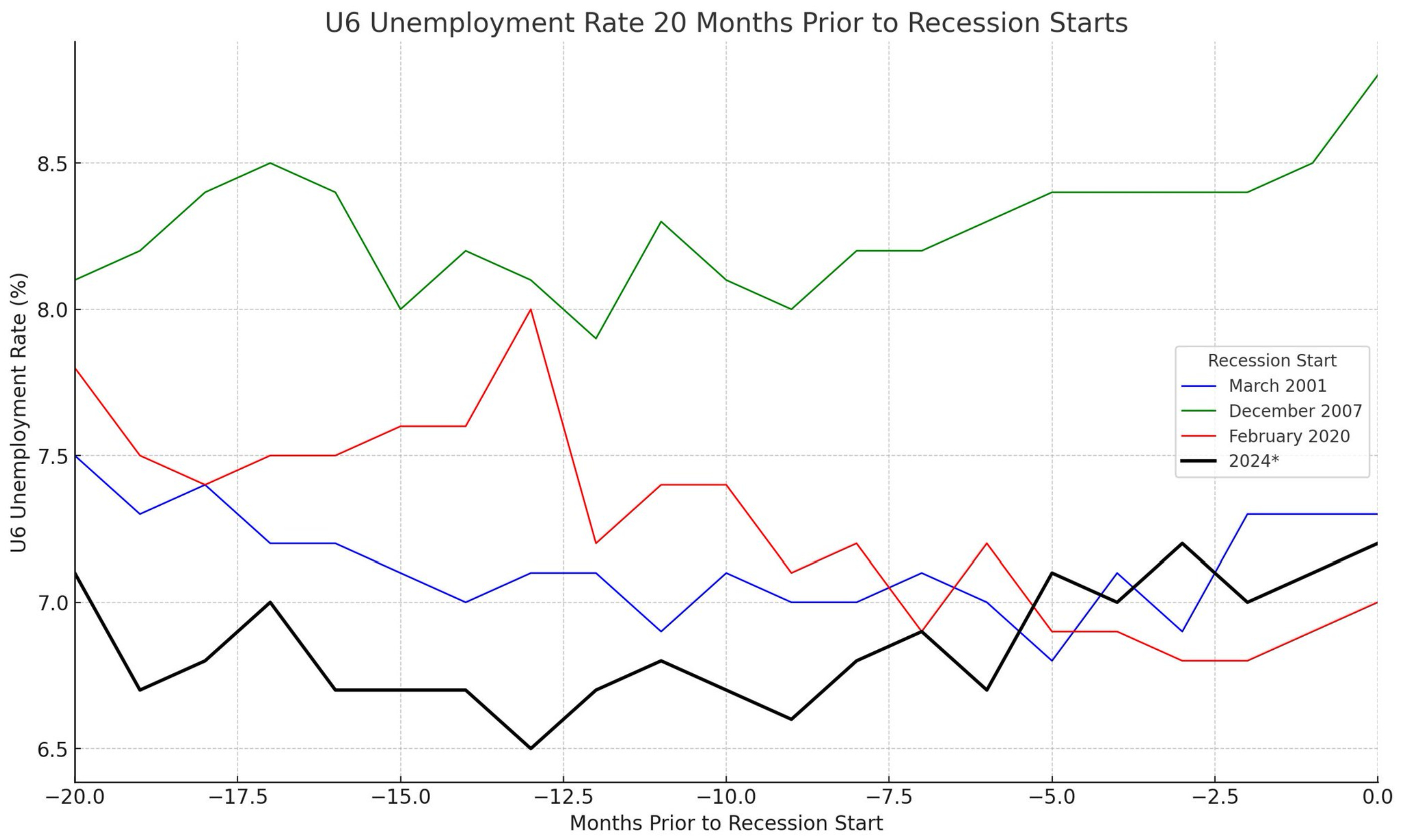

So that I don’t put you asleep with this being the first time I’ve done a longer form post again in a while here - and I know there’s a lot to read in our Sunday weekly report (which you can get access to by subscribing to Ozone here or at MacroEdge.net) - let’s focus on my favorite topic: the actual data. In over a dozen states coincident economic growth has turned negative and labor market indicators are flashing red in states across the board from (Montana, California, Washington, and more) which I make sure and hit on at least every other week. In doing a bit of a data dive this evening I wanted to map out the path of prior U6 unemployment rate’s for the last 2 cycles that we have data for (01/08) to see where things stood with the current cycle. I set the baseline at 20 months prior to the actual start of the NBER recession and the result is pretty clear:

We are tracking very similarly to both pre-Dotcom days and pre-GFC days (although I anticipate this trend would be fairly similar across cycles) if we had the available data, and with the period prior to the COVID lockdowns included, the output is this:

This would align fairly similar to my original mentions of the recession window going all the way through April utilizing past 10 year - 3 month curve inversions (we are now in the second longest inversion dating to 1969). Unless something dramatically breaks and causes a more sudden pivot, then the pause will continue doing its work to slow down the economy (decimating sectors like CRE, currently) and the lag effects usually arrive like a freight train. Following something more like the 2000/01 path would give us 6 or so more months of solid but weakening U6 figures as the state-by-state and sector-by-sector story continues to play out. Job cuts remain very elevated as well - especially going into March, and continuing claims are nowhere near being close to declaring a ‘soft landing’ or out-of-the-woods type scenario for the labor market.

The risks in 2024 for the economy are large - and the next saga will take months and years to play out - just has the inversion has taken months and (now a year+) to play out. I have a feeling that SuperMicro Computer or NVIDIA haven’t invented a server, AI chip, or SaaS to save us from this so-called saga… but what do we know?

Welcome to the next saga of labor market dynamics… one filled with demographic questions, a gradually increasing unemployment rate, unemployment ceiling constraint questions, millions of multiple-job holders, and more

Cheers and here’s to a Red-eye glass to us both…

Don

(PS) Oh, and I think the South Africation we’ve been waiting for is a little more aligned to where we’re headed for the next saga. Hope you have a seatbelt.