A New FOMC - What's the 'Real'ity?

In this Wednesday note - we cover the FOMC decision from today, discuss the implications of a Warsh Fed, and highlight oil inventories sitting at their lowest levels in decades...

Don Johnson (@DonMiami3), Chief Economist

Good Wednesday evening MacroEdge Readers & Community,

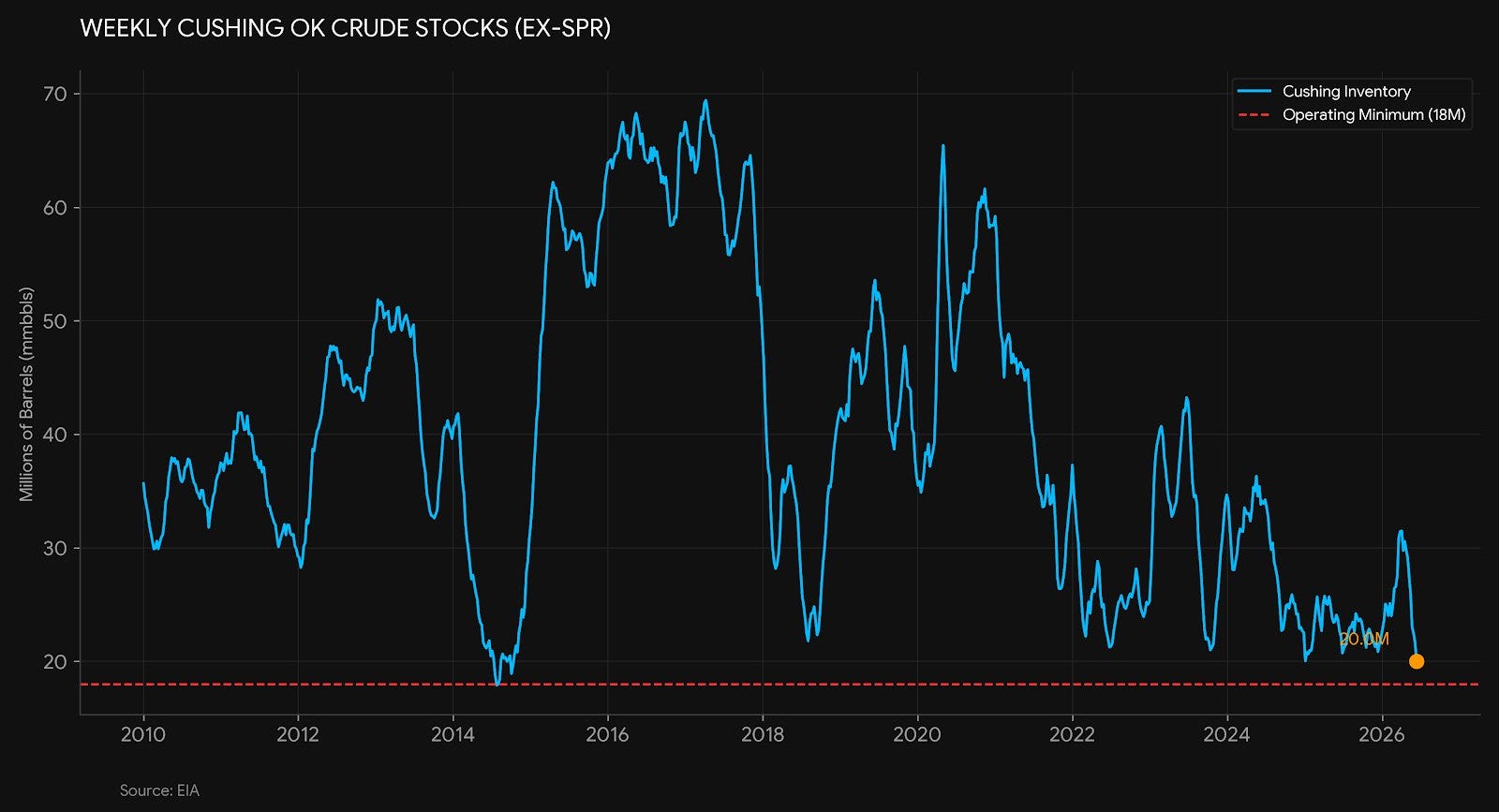

We’re navigating what could be finality to the US-Iran conflict with the digital signing of an MoU today between the two countries - and I will be covering more on that tomorrow. Tomorrow’s Midweek Macro Note will focus on the centralization of markets, an update to our Global Bubble Index, and we’ll take a look at the MoU details in better detail to understand the impact - particularly on energy markets. While organizations and analysts are now massively net short oil and related equities - it appears that additional opportunities will emerge and the drawdowns are going to continue with haste through the summer:

It is going to take significant time for boats leaving Hormuz to actually get underway, and traffic will remain suppressed below pre-war levels until at least August, by our estimations. Given that China also kept a lid on purchasing Iranian crude, this should be another tailwind for prices to attempt to find a higher base. If we see broader macro pressures build, and equities fall (which are now much of the economy) - then we may see the dip expand further than what we’ve seen.

This evening, John & Six will deliver a separate update - covering the FOMC meeting outcomes from today, the press conference, and much more - and Six will provide a portfolio strategy update…

Not yet a MacroEdge Ozone subscriber? Upgrade to Ozone below and get all of our research, data, portfolio strategy, and more below. We have exciting news about Portfolio Strategy on the way - so stay tuned in the coming weeks for what we’ve got in store as we continue to evolve in the second half of 2026.

The Fed is Fighting the Last War (@SixFinance, Head of Research)

The Dot Plot is Already Stale and the Curve is a Gift

The new regime unveiled today of a shortened statement and a near-total elimination of forward guidance (ex-dot plot), was a welcome change. Since the Bernanke era, the Fed has fed, coddled, and tucked-in markets cozy in their pajamas by giving so much insight that the outcome of nearly every Fed meeting was already nearly totally priced into the interest rate curve, and the only thing to trade was the new forward guidance issued at said meeting.

That era appears to be coming to an end. Warsh explicitly discussed markets taking a more active role in adjusting positioning based on public and private data, encouraging participants to react to market developments, not to how they believe that the Fed will react to those developments.

Today’s split Fed on what Warsh called “low conviction” has scared the market, with December SOFR futures fully pricing in 2 rate hikes. This comes following other central bank hikes in response to inflation from the Iran war. The icing on the cake was the steadfast final wording in the statement “The Committee will deliver price stability”.

The market has reacted aggressively, with nearly a full rate hike priced in today alone between now and the end of year. This is where I am buying hand over fist.

Why this is all backward looking:

The Fed dot plot is responding to May CPI at 4.2% YoY. Producer prices near four-year highs. A wartime energy shock that caused oil prices to double.

Continued below: ‘The Fed is Fighting the Last War, I Smell a Rate Cut, Today’s Equity Warsh Out - John Galt)