A California ‘Cooling’, The Business Cycle Tightrope, An Early Spring?, Powell’s Big Pivot, Canada's Economic Rollercoaster, and The Data Mirage from the BLS Continues

@DonMiami3, MacroEdge Chief Economist; @SixFinance, MacroEdge Head of Research; and @SquirtLagurtski, @TexasrunnerDFW, @ManyBeenRinsed, & @RealJohnGaltFla, MacroEdge Contributors

A California ‘Cooling’: California Labor Market Weakness Continues (@DonMiami3, MacroEdge Chief Economist)

Hi all - another weekend of all-time highs in equities on a foundation of AI and sand masks some weakness in the economy elsewhere. In California - our pioneer tech state - things are not looking as grand as they were 2 years ago for the tech sector. The state is running a massive deficit for FY24-25 ($68bn) so it’ll be interesting to see where things head throughout 2024.

Looking forward to our MacroEdge 2025 Vision that is underway with our social club, new features coming soon, new website overhaul, and more. You can get on a trial for our legacy platform, Ozone, here: https://macroedge.substack.com/subscribe

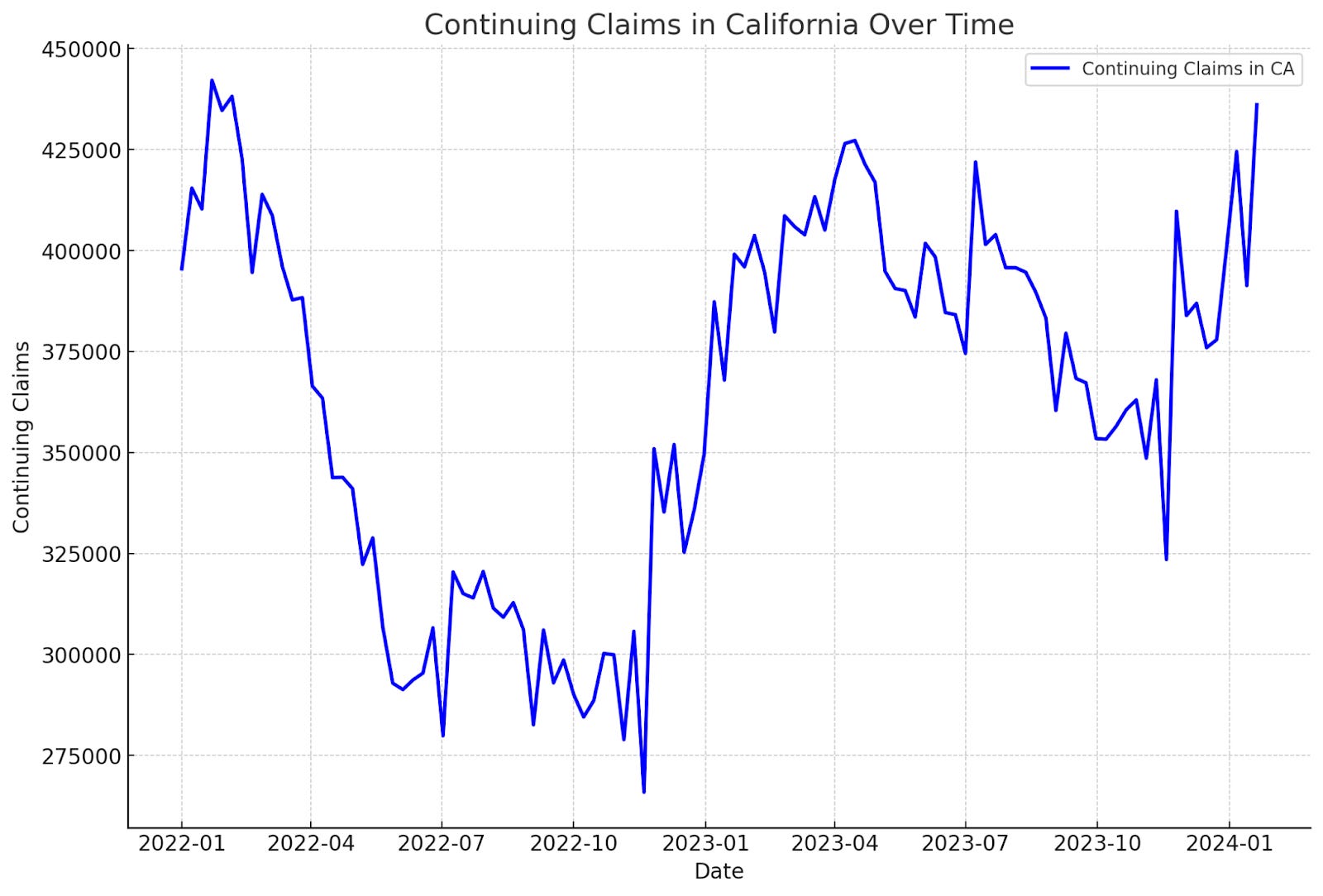

The California labor market continues to look the weakest in the country (by both scale and downturn). Unemployment and claims are elevated, and core cyclical sectors like tech have been leading the drag in the state.

Continuing claims are the highest since January 2022 at >430,000 and made a higher high this year even with all of the tech layoffs California experienced in 2023.

Unemployment stands at 5.1% in the state and has been increasing…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

The Business Cycle Tightrope: Navigating Peaks, Pitfalls, and Predicting the Perils of Commercial Real Estate in 2024 (@SixFinance, MacroEdge Head of Research)

The purpose of tracking the business cycle is to have an awareness of the point we stand to at the very least not get blindsided by a weakening of economic conditions, and at best capitalize on it and come out the other side stronger than before.

While the stock market hits all time highs on the back of AI euphoria and scorching hot NFP payrolls data, things seem very rosy on the surface. Although exciting, this is typical of financial markets right as they are peaking. Markets hit all time highs while at peak interest rates nearly every cycle, and while the market always recovers over the long term, investing at peak interest rates is a dangerous endeavor, with generally subpar results…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

An Early Spring? (@SquirtLagurtski, MacroEdge Contributor)

This week brought a mixture of emotions for the market as Fed chair Jerome Powell tamped out embers of growing calls for rate cuts, saying a soft landing has not been achieved and they have much more work to do in their quest to return inflation to a 2% target. From the beginning Powell has remained consistent in his narrative, reinforcing yet again his intentions to remain vigilant and respond to the economic data as it comes.

There has been no shortage of speculation from market participants, all seeking to find the edge of Powell’s intentions as higher for longer has begun to root itself firmly into the base case outlook. Arguably, following data can have desired effects while it generally lags current conditions but the crystal ball in Powell’s office accounts for the lags it seems so for now all is on schedule although when asked about timelines, he stopped short of predictions, perhaps the crystal ball does have limits. To that end there were notable earnings within logistics as well as some data releases which can offer a glimpse into the drivetrain of the economy, which is seemingly just, getting by. Consumers are feeling more optimistic as reported in the consumer confidence index released on Monday, hitting a two-year high and printing its third consecutive increase, however…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

Powell’s Big Pivot: I Don’t Have the Right Tools Housing Market FOMC Language Changes (@TexasrunnerDFW, MacroEdge Contributor)

In June 2022, as the Federal Reserve began hiking interest rates off the historic post-Covid lows,Powell made this statement to reporters during an FOMC press conference about the US housing market,

“I’d say if you are a homebuyer or a young person looking to buy a home, you need a bit of a reset. We need to get back to a place where supply and demand are back together and where inflation is down low again.”

In September of 2022, Powell was asked to clarify these prior comments about a reset. He said,

“When I say ‘reset’, I’m not looking at a particular set of data…we probably have to go through a correction to get back to a balanced housing market.”

Then, nearly a year later, in June 2023, Powell noted at another FOMC meeting,

“We now see housing putting in a bottom, and maybe moving up a bit. We’re watching the situation carefully.”

This was followed by a remark on the impact of mortgage rates in the November 2023 FOMC meeting,

“8% mortgage rates could be quite significant for the housing market.”

Powell’s comments at the latest FOMC this week represented…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

Canada's Economic Rollercoaster: The Rise and Fall in 2024 (@ManyBeenRinsed, MacroEdge Contributor)

Canada's in a real mess right now. Bankruptcies are soaring, houses aren't moving, and inflation is tearing through everything from groceries to, well, you name it. And our government? They keep singing the tune that we're still the G'est in the G7. It's like we're all being led to the slaughter, and so many folks are just blind to it, like they've been for the past two years.

Let's talk about 2023. The housing market kicked off with a bang, but by early summer, the Bank of Canada dropped two rate hikes, and things went south. Houses that made a quick 300K gain in the first half of 2023? Yeah, they lost all of that by the end of the year. Imagine thinking you're buying the dip, only to have your feet clipped out from under you. I spoke to a guy who bought into the "dip" story in May 2023, told by his realtor that rate hikes were over and it was just a healthy housing "pullback." Now he's down a whopping 300K, and the realtor? Poof! Gone, not even in the game anymore. Back in 2022, I warned everyone to stop snatching up condos and pre-construction homes because the storm clouds were gathering. Lo and behold, we've got a load of people stuck…

Full article included in this week’s MacroEdge Weekly Report only available at MacroEdge.net.

The Data Mirage from the BLS Continues (@RealJohnGaltFla, MacroEdge Contributor)

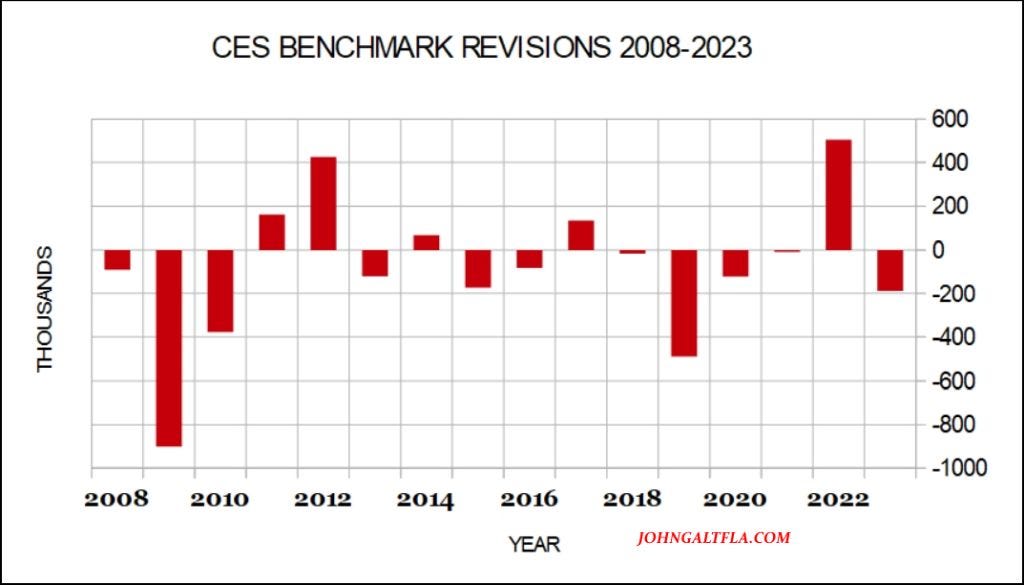

Over the past few decades, these pages and in some of the commentary I have offered elsewhere has been somewhat harsh analyzing the data emanating from the Bureau of Labor Statistics (BLS) and the various bits of information they release each month.

This past Friday the Employment Situation Summary from the BLS was released with a strong headline number indicated 353,000 jobs were created in January. This despite reports indicating massive layoffs in January in the service, technology, and manufacturing sectors as reported in the pages of MacroEdge on a daily basis.

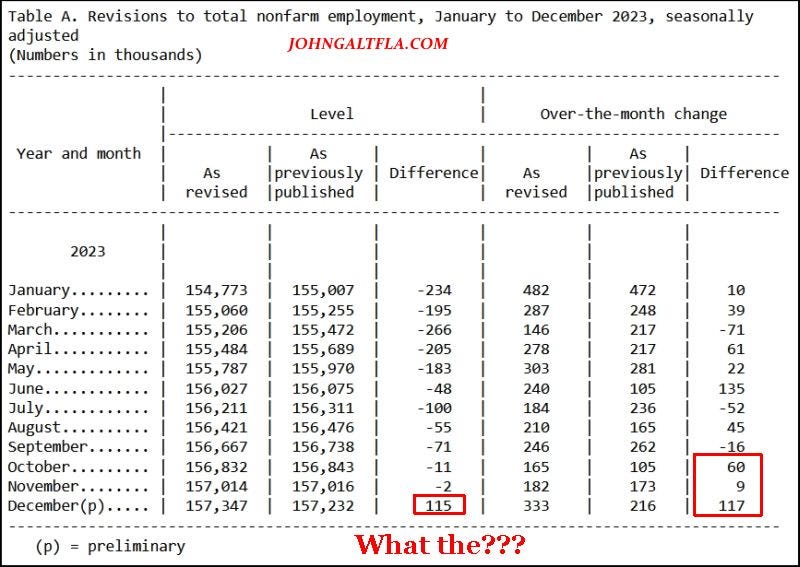

The requirement to suspend belief is buried within the methodology and reality. For example, revisions to the 2023 headline reports was proudly touted in the ESS this past week as demonstrated within this chart below:

If anyone truly believes that over 100,000 people were added to the workforce in December of 2023 per the revisions published by the BLS in the chart above, one must ask themselves the following questions:

December is basically a two business week month for employers. Thus any hiring would be for only necessary replacement personnel and not a net gain.

Decembers in general are year end periods where bonus calculations are made and adding additional headcount is frowned upon in almost all businesses heading into the new year.

Due to the three major holidays, Hanukah, Christmas, and New Years, most employers are winding down HR activity as there usually is a lack of personnel to provide training, orientation, etc.

Yet the BLS would have everyone believe that in the first two weeks of the month over 100 thousand jobs were added due to their statistical calculations? Hardly.

Next up with this current report is another anomaly which stands out like a sore thumb. The BLS insists that the Business Birth/Death model is a reliable statistical indicator for measuring employment activity. Thus when this author reviewed the following, let’s just say I had some questions:

So if we added 115,000 new jobs over the original published numbers but the Birth Death model indicated a loss of 86,000 jobs, then this means that the real number of “new” jobs created was over 200,000 jobs. Which makes the numbers in December 2023 and January 2024 even more unbelievable.

To understand why there should be some doubts in the data being produced by the US government one has to review the methodology. The Current Employment Situation (CES) report relies on 629-666,000 employers answering a survey. Of that the average returned completed surveys averages around 129,000; roughly a 20% return rate. This means that hundreds of billions of dollars on “jobs day” are wagered on 20% of the employers honestly filing and returning these surveys.

Good luck with that.

Add in some historical perspective and one has to start asking even more questions about the viability of the jobs report as a measure of America’s economic health.

For example, from the 2016 CES National Benchmark Article, the following footnote (2) appears:

“A review of industries for the possible presence of noncovered employment in benchmark 2011 yielded 13 additional industries. As a result of including these industries, employment for total nonfarm was 95,000 more than the originally published March 2011 estimate level. The difference between the benchmarked and published March 2011 estimate level was 162,000. For this table, the 95,000 amount was added to the original published total nonfarm and total private March 2011 estimates before calculating the percent and level differences. Similarly, for the financial activities and education and health services supersectors, this table displays March 2011 data after incorporating the employment from the additional industries.”

If one thinks this is unusual, think again. The BLS and politicians know that nobody reads the footnotes. Period. End of conversation. “New industries” and classifications are created adding employment to the total then revised away years later as “better” methodologies are developed. It’s the nature of statistics, but in reality, it also provides a wee bit of political insight into how the data is manipulated.

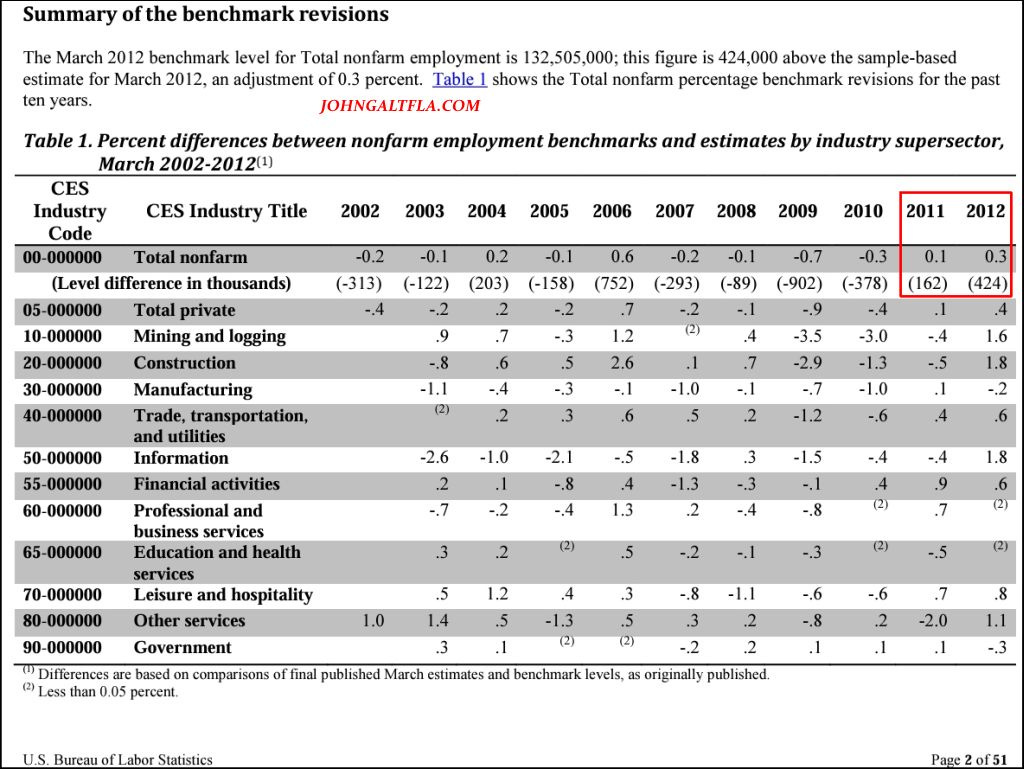

For example, let’s look at the chart from the 2012 CES National Benchmark Article:

Why would this author think that highlighting the two years in particular is important?

1. The Obama administration needed to show positive employment growth after two tough years of recovery from the GFC. The race against the Republicans was going to be a tough one and the Democrats truly feared losing total control of all the Executive and Legislative branches of government.

2. The Bureau of Economic Analysis (BEA) conveniently created new measures of GDP which resulted in outsized, okay, outright fictitious indicators of a budding economic expansion as soon as 2010 that moved even faster thanks to Obamanomics.

Every politician since that era, yes that includes Trump, has learned to overwhelm the masses with headline data, revise it closer to reality in the future, then blame the bureaucracy if something breaks.

The charts do not lie, as I demonstrate in this review of benchmark revisions below.

With an initial downward revision for 2023, the sudden surge for this past month’s report makes no sense. Until one reviews a calendar and understands that this is an election year.

Hence if one is making investment decisions for their own accounts based on government data, be it employment, inflation, national debt, or even trade, I wish them the best of luck. Everything eventually will be revised away and vanish from the headlines; just like the stock certificate at the top of this article.