9/7 Weekly Macro Note: Employment Snapshot, James Bonds, Inflation Data Week, Rate Cut Excitement, Gold, and More

In this Weekly Macro Note we discuss everything from the cooling employment picture, bonds, rate cut odds for the upcoming FOMC meeting, inflation data ahead this week, and more.

(@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers and Community,

I’m still somewhat discombobulated from a very exotic day yesterday - we’ll call it a ‘day trip’ - so we’re back in the office getting things spooled up this evening for another busy week.

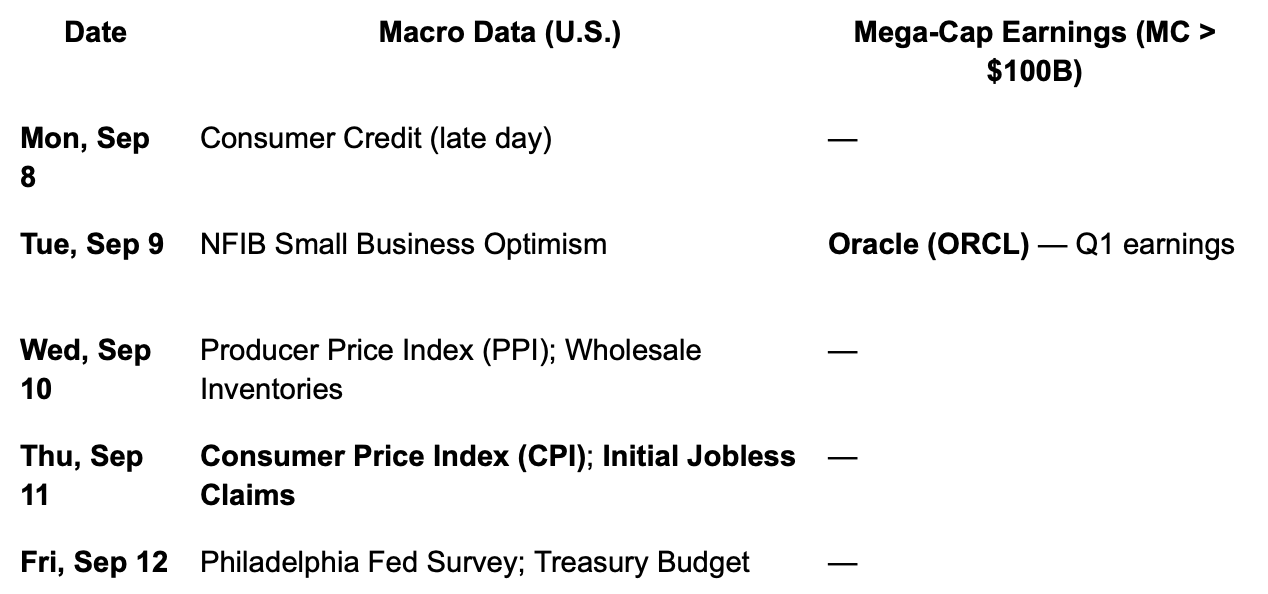

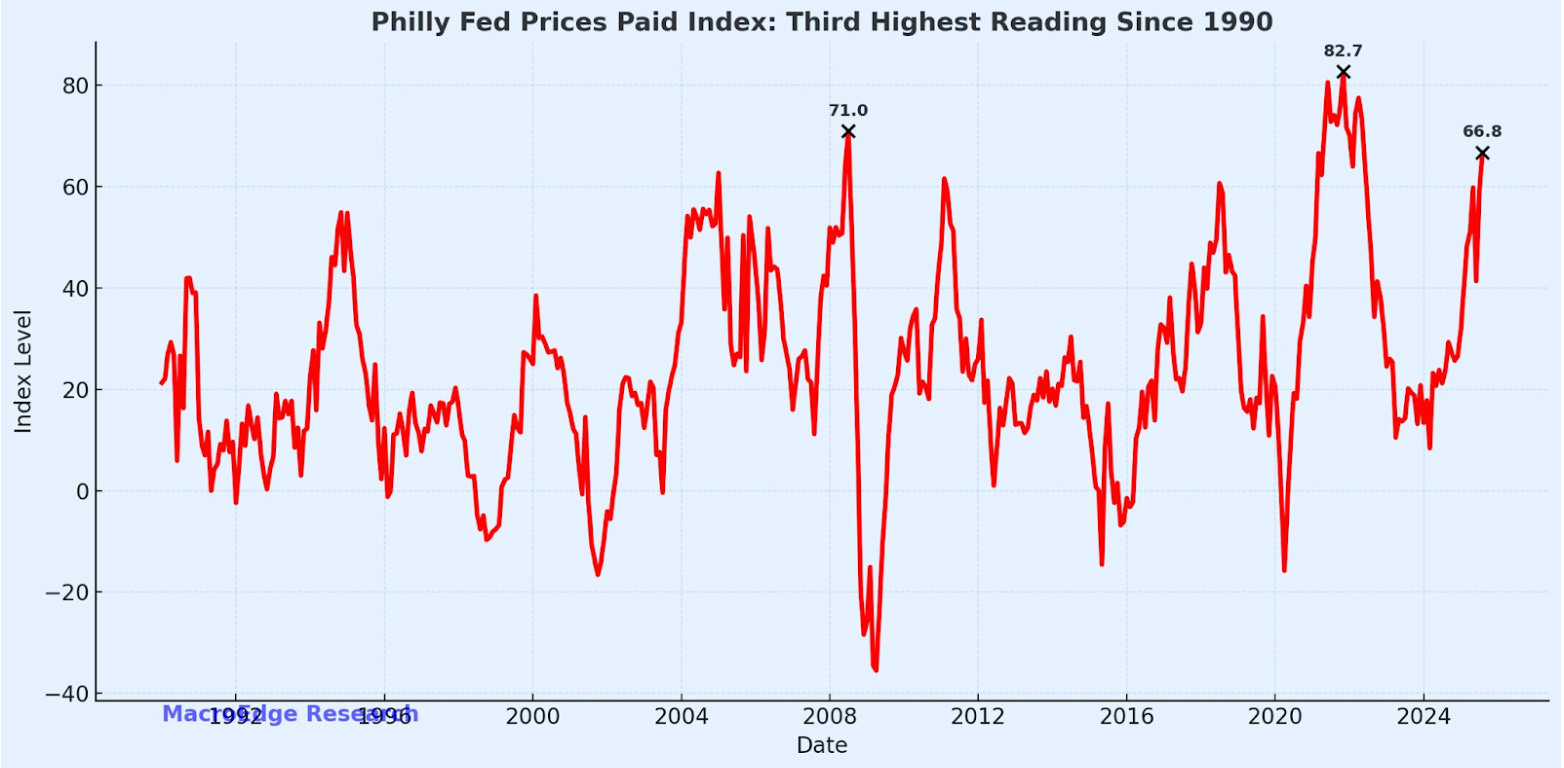

This week puts the inflation focus back into view with CPI/PPI and the Philly Fed Prices Paid Index. Only Oracle this week from a megacap standpoint.

In global news - Prime Minister Ishiba of Japan is stepping down after a largely disastrous tenure - marked by bond yields on the long-end hitting record levels, a tepid tariff response, and multi-decade high inflation in the east Asian nation. This announcement has pushed the Yen down and bonds up, though Japanese traders are undoubtedly waiting to see a) who the replacement is and b) if the BoJ is going to pursue one more rate hike due to rising yields (note that this is what Bessent wants, too).... (Bessent also thinks the stock market is the economy - which it is now as the K-shape continues to expand further and further apart). GDP came in at 2.2% annualized, showing a strong rebound, which will likely offset some of the decline in yields.

Don’t have MacroEdge Ozone? Get a week of access below and transform your data and insights from our industry-leading team:

In the Upcoming Institutional Research Report

The second edition of the Institutional Research Reports will be available on Tuesday - we’ll be discussing everything from tariff price pressures, opportunities in defensives, currency markets, so much more from myself & @SixFinance. We will be releasing MacroEdge Institutional Research on 10/1 - for those that would like 4-week access to the new line of research, data, our dashboard, and access to our team, you can fill out a request for the August report below:

(the first press release will be out mid-week, and the Institutional Research report will also be distributed to our entire audience on Tuesday - for a final time).

Inflation Data Week… & More

Employment Snapshot

A soft jobs print as expected. My forecasted -10K wasn’t far off from the final print. The employment situation continues to cool gradually, and notably, Trump mentioned that we should expect the real data - about 12-months from last months’ print (also said similar about GDP growth). If rate cuts continue to impact the major cyclicals - such as residential real estate construction employment - things are going to get more interesting and complicated for policymakers into the winter.

Overall Total Unemployment Level

There are more unemployed Americans than there are job openings, for the first time since right after the lockdowns –

Long-Term Unemployed

Slow moving impact to unemployment this time, but still seeing a 10y3m normalization in the next 12 months and the youth are getting hit hard this cycle.

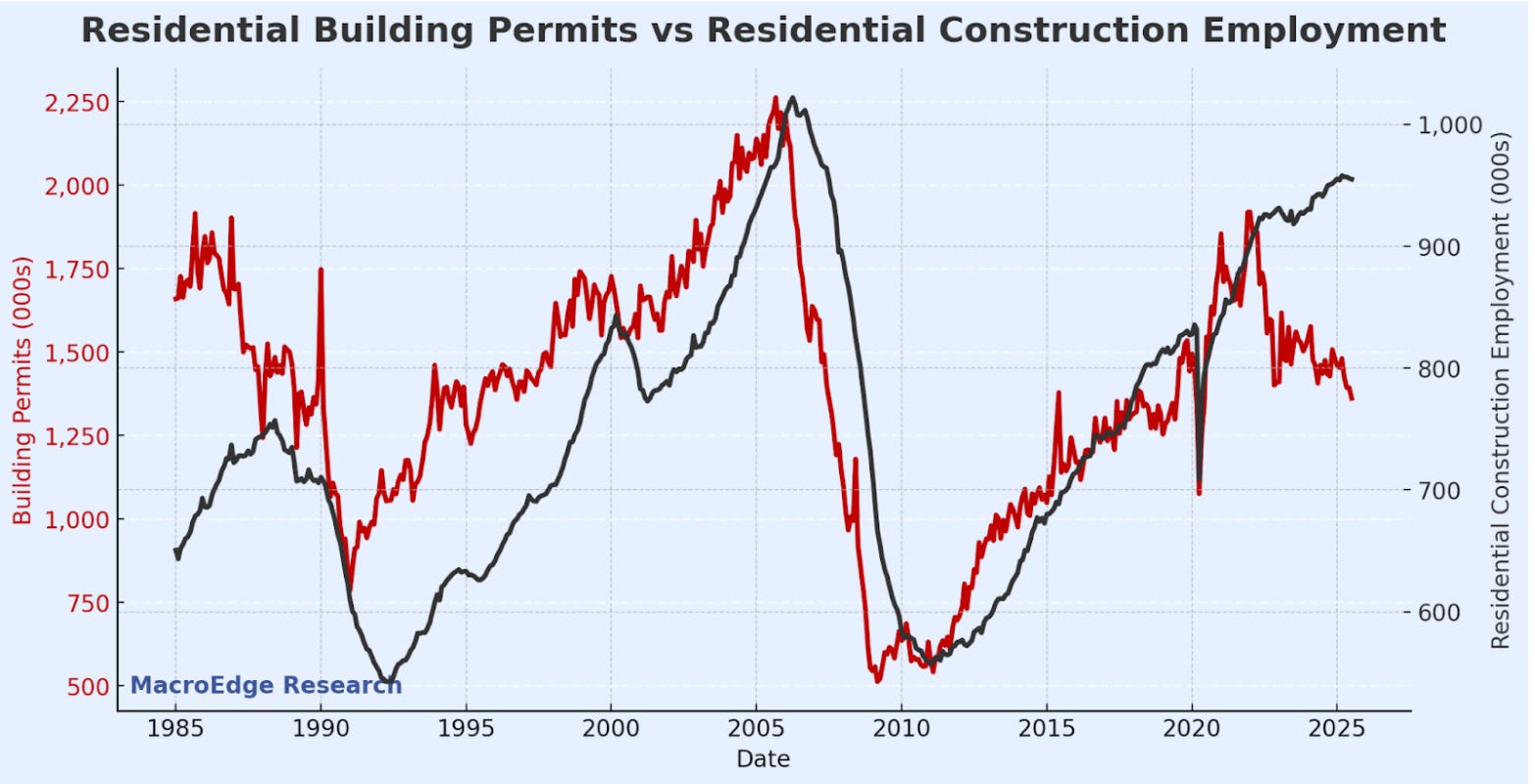

Residential Real Estate Construction Employment follows Permits

Future direction here is pretty clear - a slow motion train running in reverse

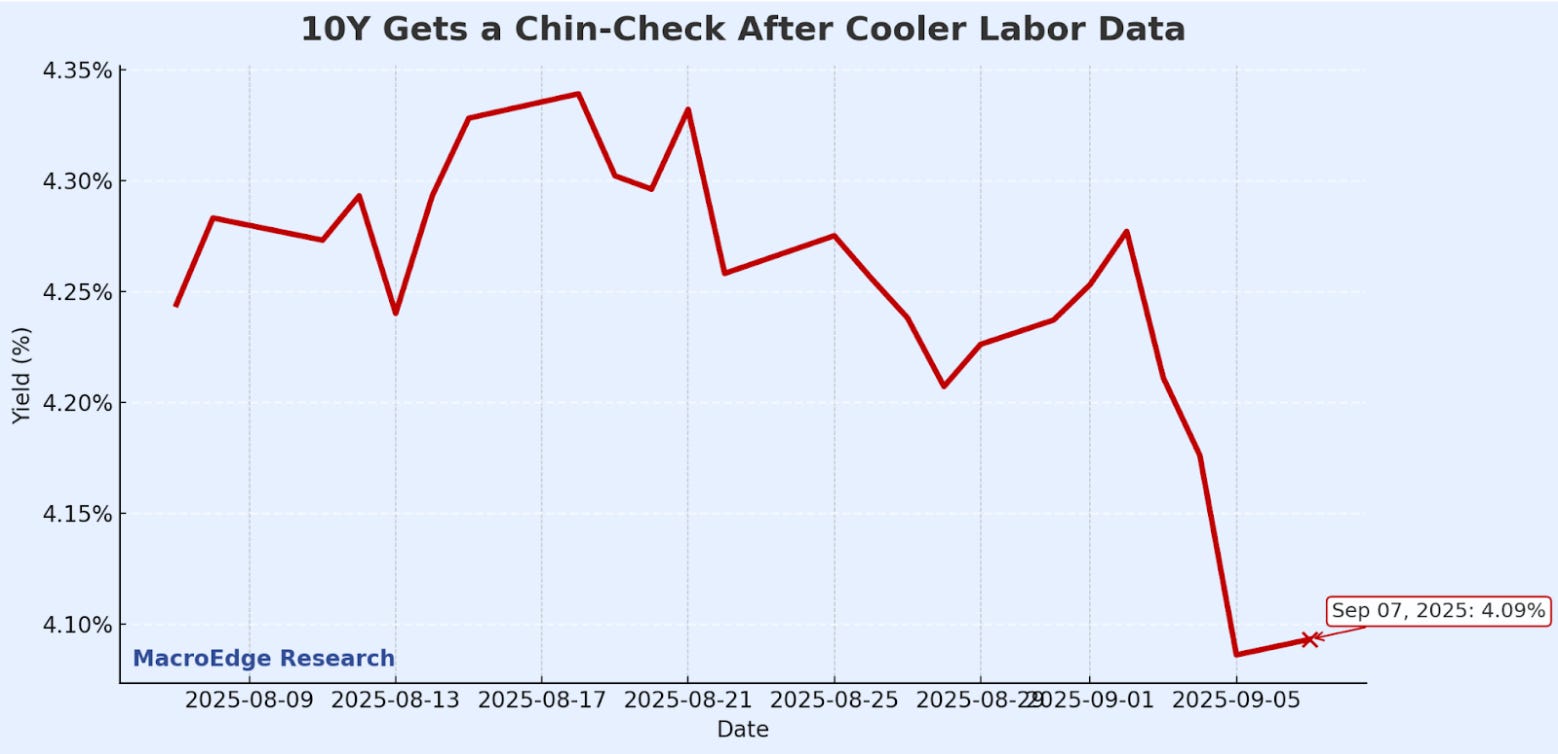

James Bonds & Rate Cut Excitement

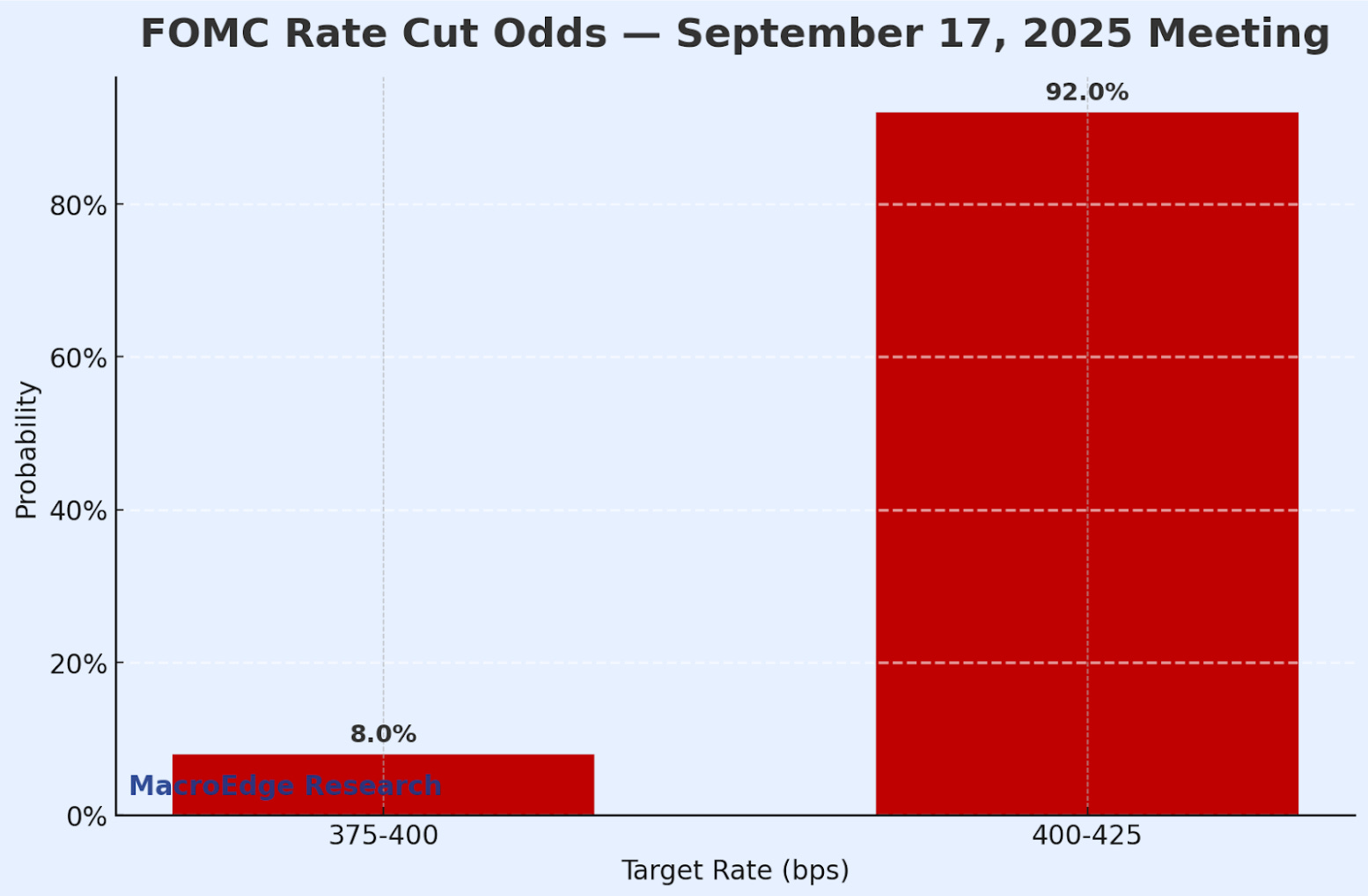

The weak employment report got everyone very excited about the decline in the 10Y and odds of rate cuts spiking sharply (to almost 100%).

Rate cut odds spiked to 100% - with the odds of a 50bp cut increasing to a meaningful 1/10 shot:

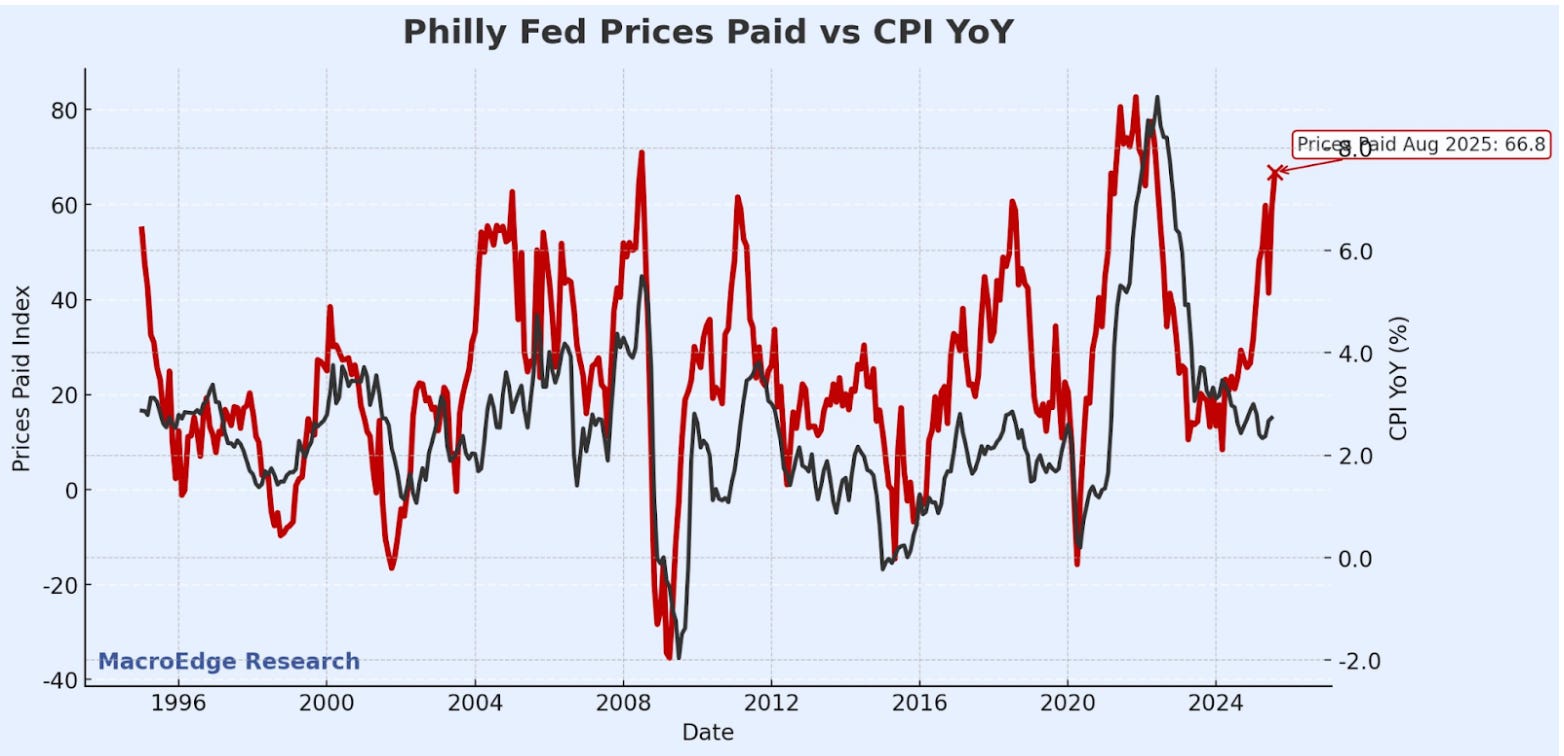

Stagflation Still Seems Plausible

One thing that I note in the upcoming second edition of our MacroEdge Institutional Report is that we cannot rule out the ‘stagflation scenario’... We still aren’t of the woods yet from the tariff impacts:

The next update for the Prices Paid Index will be on Friday:

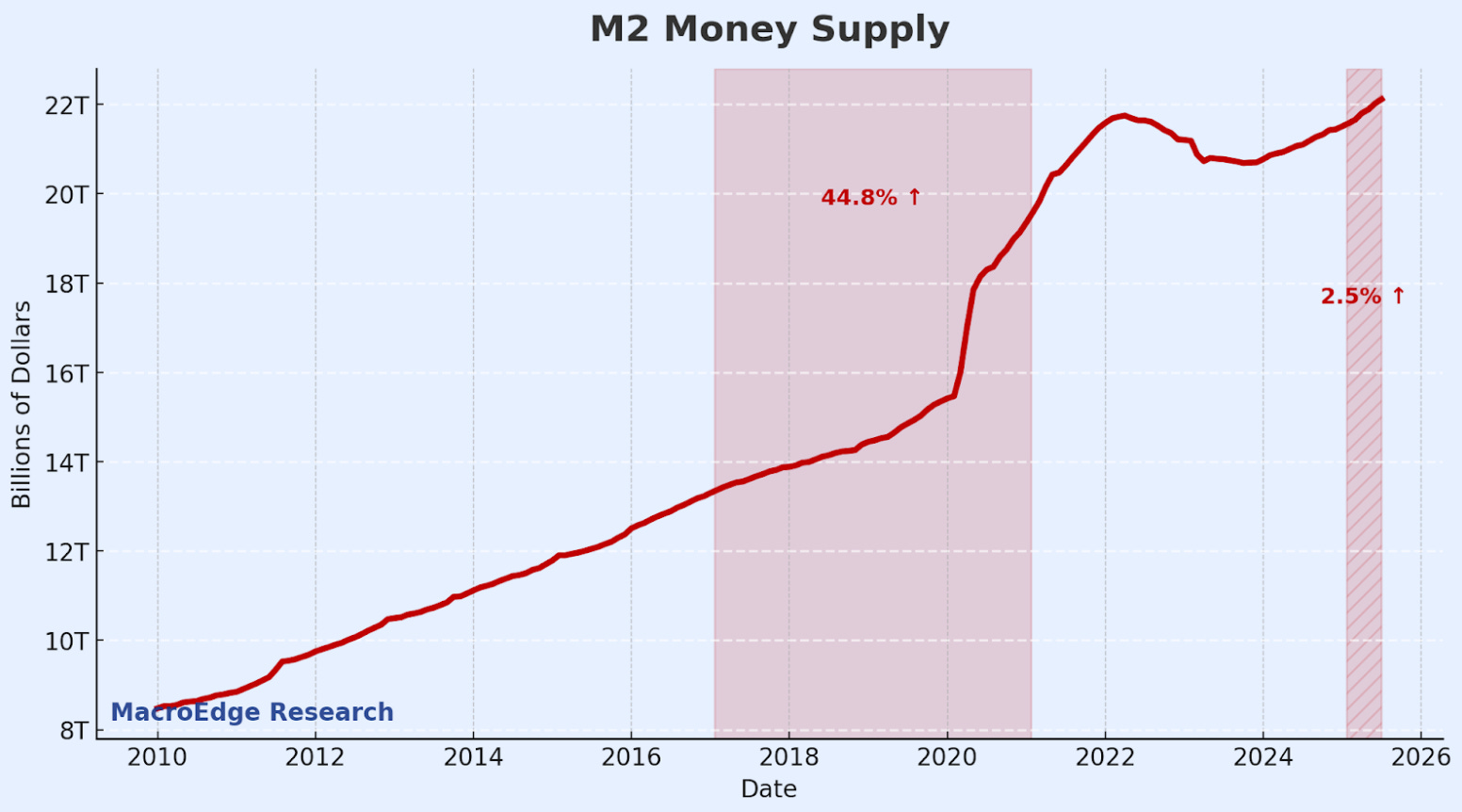

This government (and this Administration) absolutely love the ‘Big Print’ tool - and they’ve shown no signs of slowing down, even with all the phony beginnings of things like DOGE:

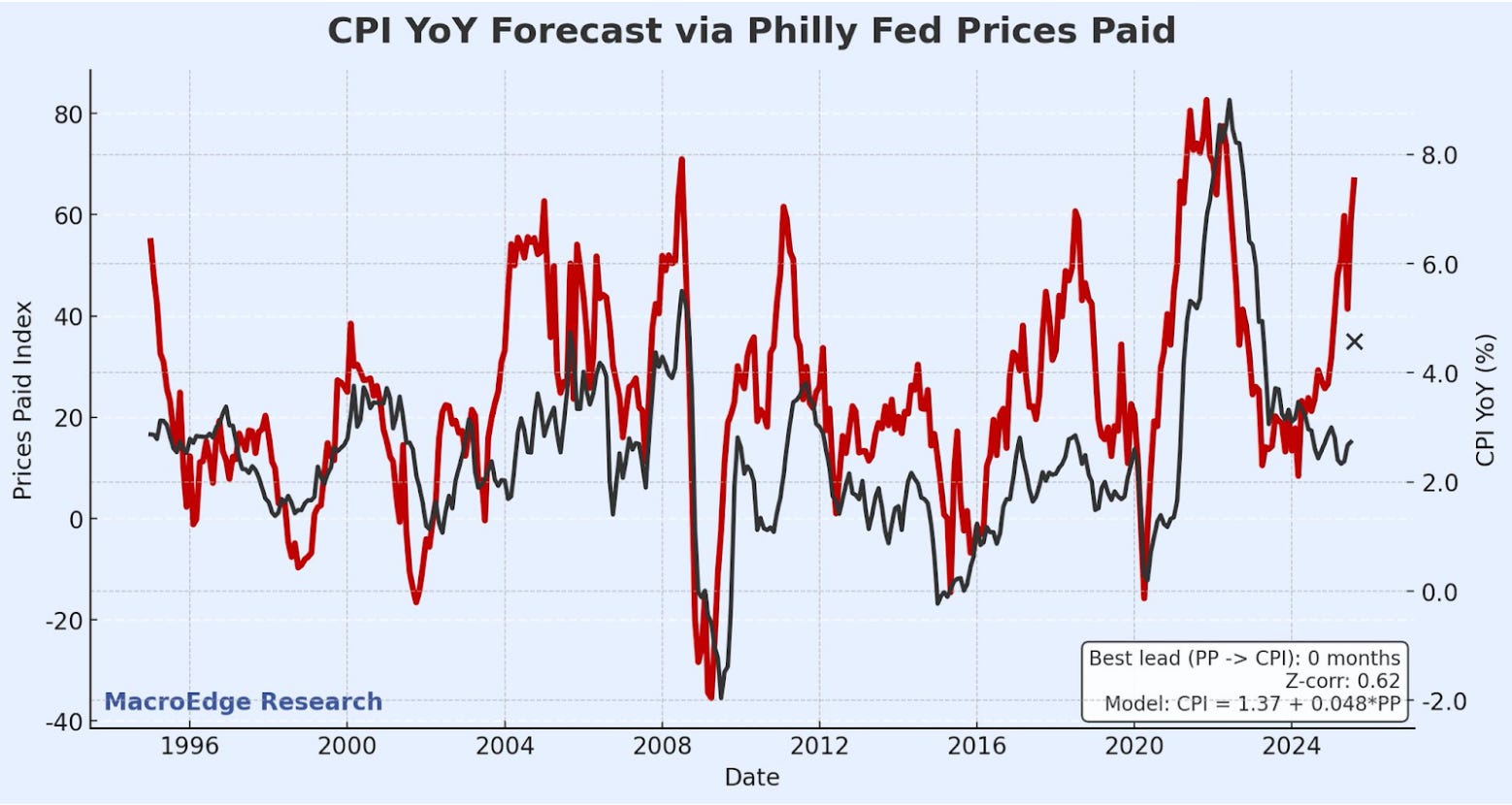

The imputed impact on a potential rise in CPI from Prices Paid can be seen in one model I created -

Job Cuts Have Likely Bottomed Until December

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.