9/24 Weekly Report - 'Keeping it Simple, a Paradigm Shift, Powell's Soft Landing Reversal, Alternative Energy Shifts, and '1987?''

In this weekly report - Don, Six, John, Greg, and Joe tackle everything from 'keeping it simple' with leading indicators, an abrupt FOMC paradigm shift, Powell's reversal, nuclear energy, and more.

9/24 MacroEdge Weekly Report

@DonMiami3, MacroEdge Chief Economist

@SixFinance, MacroEdge Head of Research

@GregCrennan, MacroEdge Contributor

@RealJohnGaltFla, MacroEdge Contributor

@SquirtLagurtski, MacroEdge Contributor

Weekly Data Update and ‘Keeping it Simple’ (@DonMiami3, Chief Economist)

Happy Sunday evening all - had the opportunity to get out there and play some tennis in the heat today which was a nice reminder of the ‘glory days’ on the court… (now I just am traveling, live on SAP/Python, and get out on the golf course for the most part). Always a big fan of taking care of the body in every way that I can so highly encourage everyone to give a shot on the court or even pick up pickleball and I promise you’ll have a great time.

Our data dashboard continues to progress and our new job cut tracker (not yet directly interactable, but it will be soon) is live on the website at MacroEdge.net. We’ve noted approx. 27,000 job cuts via public announcements this month, which is a slowdown from the previous month figure from Challenger, and explains why both initial and continuing claims have ticked down this month. Of note, September also sees seasonality working against the initial claims figure with a negative multiplier, and this effect will actually shift in October per our friend WARN TRACKER 2.0. He anticipates that we see both of these numbers rise by the end of October from their current places, and as we’ve discussed many times in this weekly report, anticipate the real shift to begin following month 15+ from 10y3m inversion.

I’ve booked some travel trips for the month of October to see how things are looking out in Nevada as well as some of the other ‘boomtowns’ - so I look forward to writing direct reports on location when I make it out to several different cities over the next month. Our restaurant expert DKB has been on location in the South seeing how things are looking and noted an interesting bifurcation between how busy things were in Austin (they were not) and how things are looking in Nashville (reportedly still insane). I find this quite interesting given that both of those cities have likely seen (or are near) their peak total nonfarm payrolls for this cycle. Nashville is looking like total jobs peaked in July and Austin metro appears to be seeing a slowdown in job growth as well.

Turning to my focus for the weekend - I’ll be ‘keeping it simple’ as the title states - looking at 4 different leading economic gauges: residential construction employment, total temporary help employees, technology inventories, and the Reno-Sparks MSA Unemployment Index… Reno is one of the cities I’ll be visiting on my October research trip so I am quite excited to get on the ground and see what things look like in one of the arguably largest boomtowns of the ‘20-’22 cycles. I think in this period of ‘soft landing fantasia it’s good to keep it simple on the data and follow the trends:

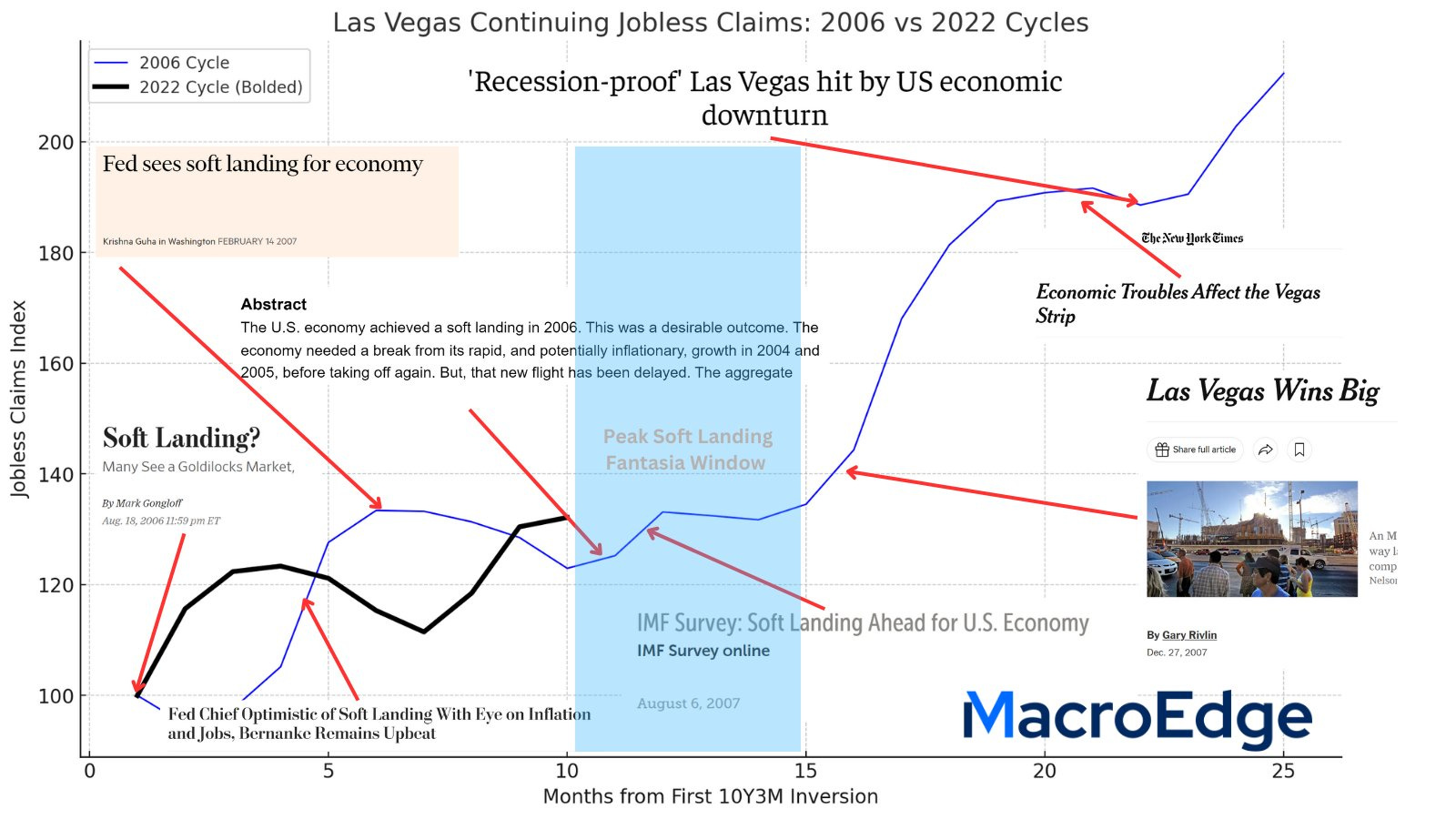

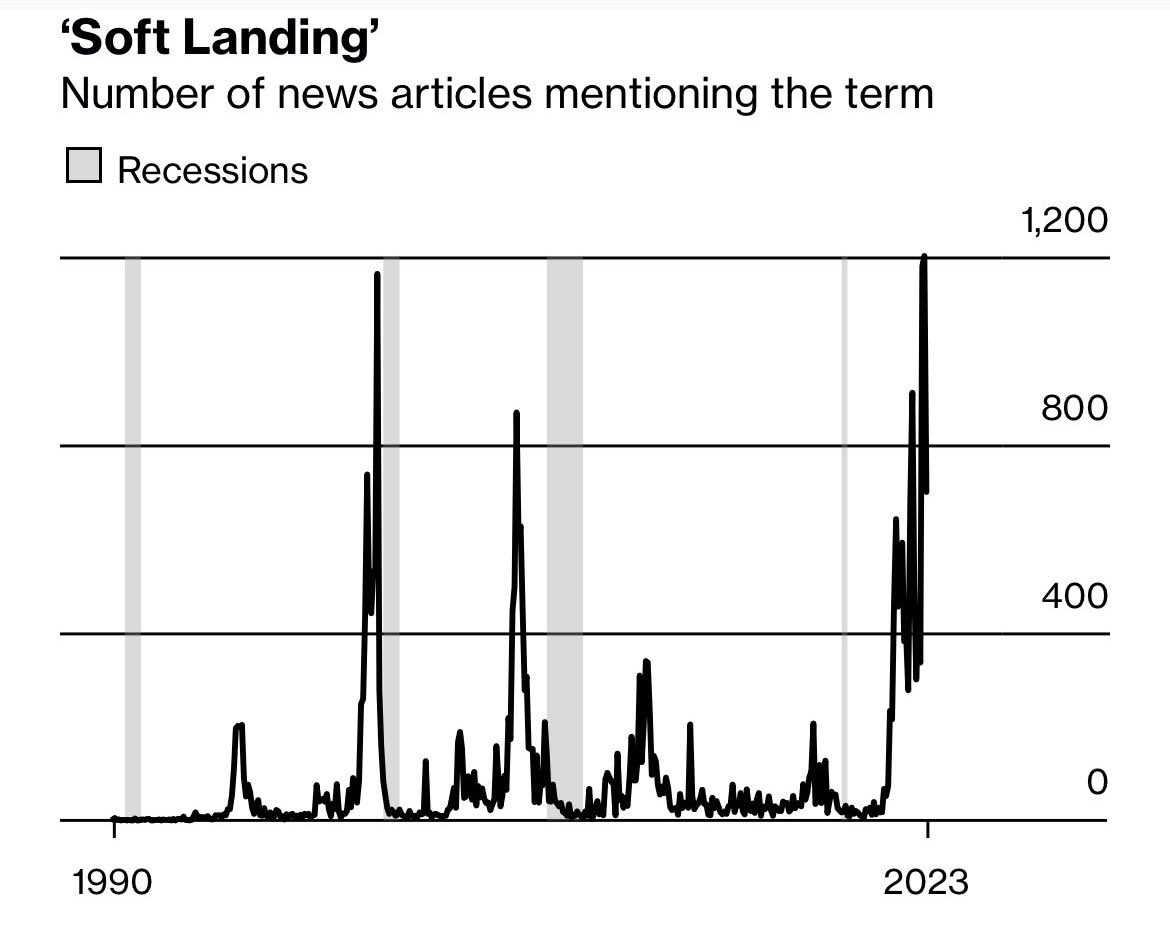

Of note above - the number of articles mentioning Soft Landing per week from Bloomberg (and the chart I created a few weeks ago notating the soft landing fantasia from 2006 to 2008 until things began to unravel in Q4 07/Q1 08.

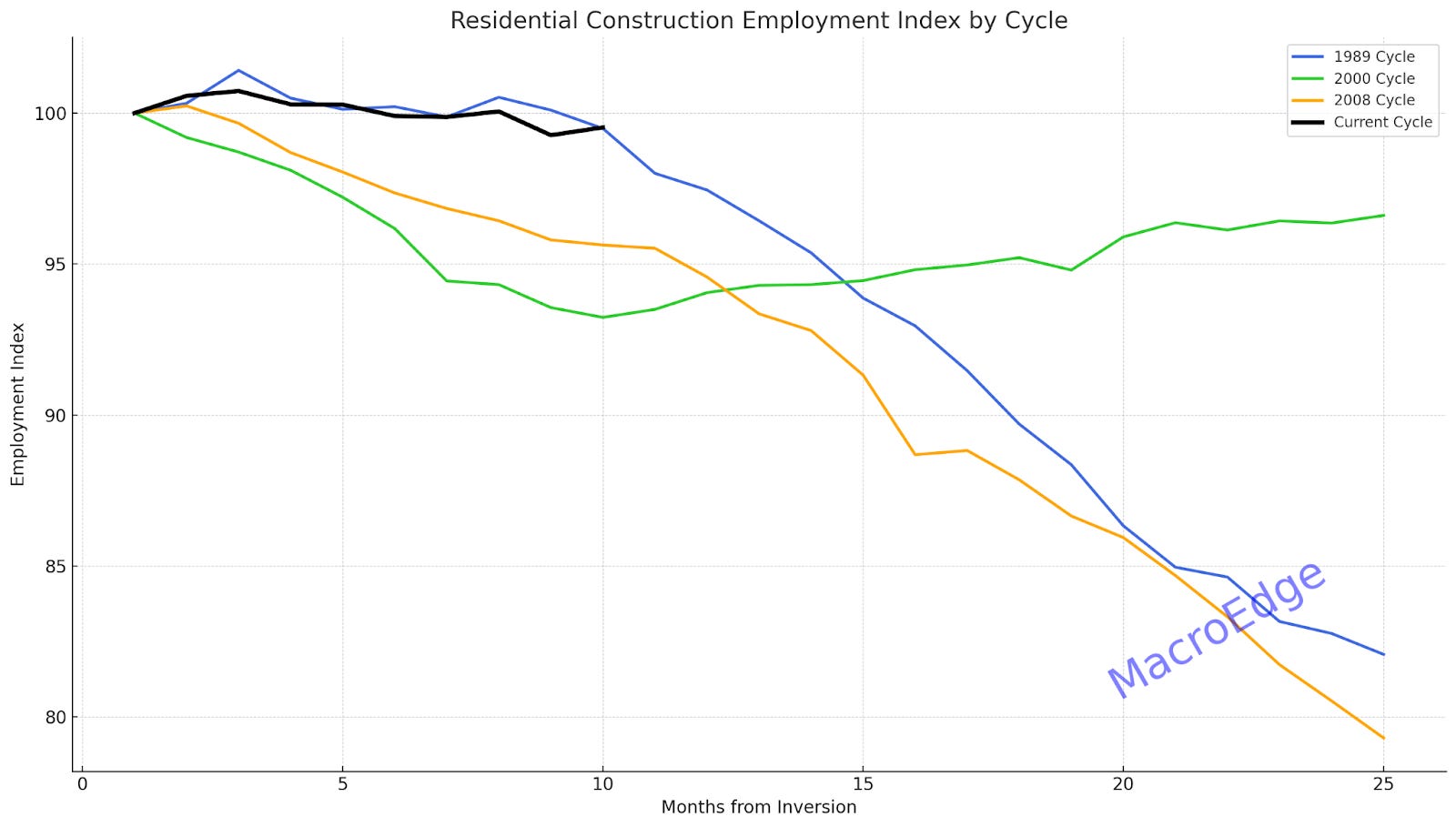

On the residential construction employment front - one of the more cyclical gauges of the economy - I think this gives us a great idea of the ‘type’ of recession we may get this cycle. While in 2000, the residential sector wasn’t affected to a great degree - it most certainly has this cycle with home sales falling to their lowest levels in 3 decades, the NAHB index again contracting, and new home construction beginning to roll over. The residential construction employment figure tracts closely to total units under construction so we should begin to see the index roll over now:

It’s been a more resilient employment cycle for the homebuilders this cycle, but I anticipate a lot of that has to do with backlog from 21/22 building and not from the actual hiking cycle still potentially taking a place. Definitely a notable lag this time around on this front, we’ll keep an eye out on weakening over the next 5 months.

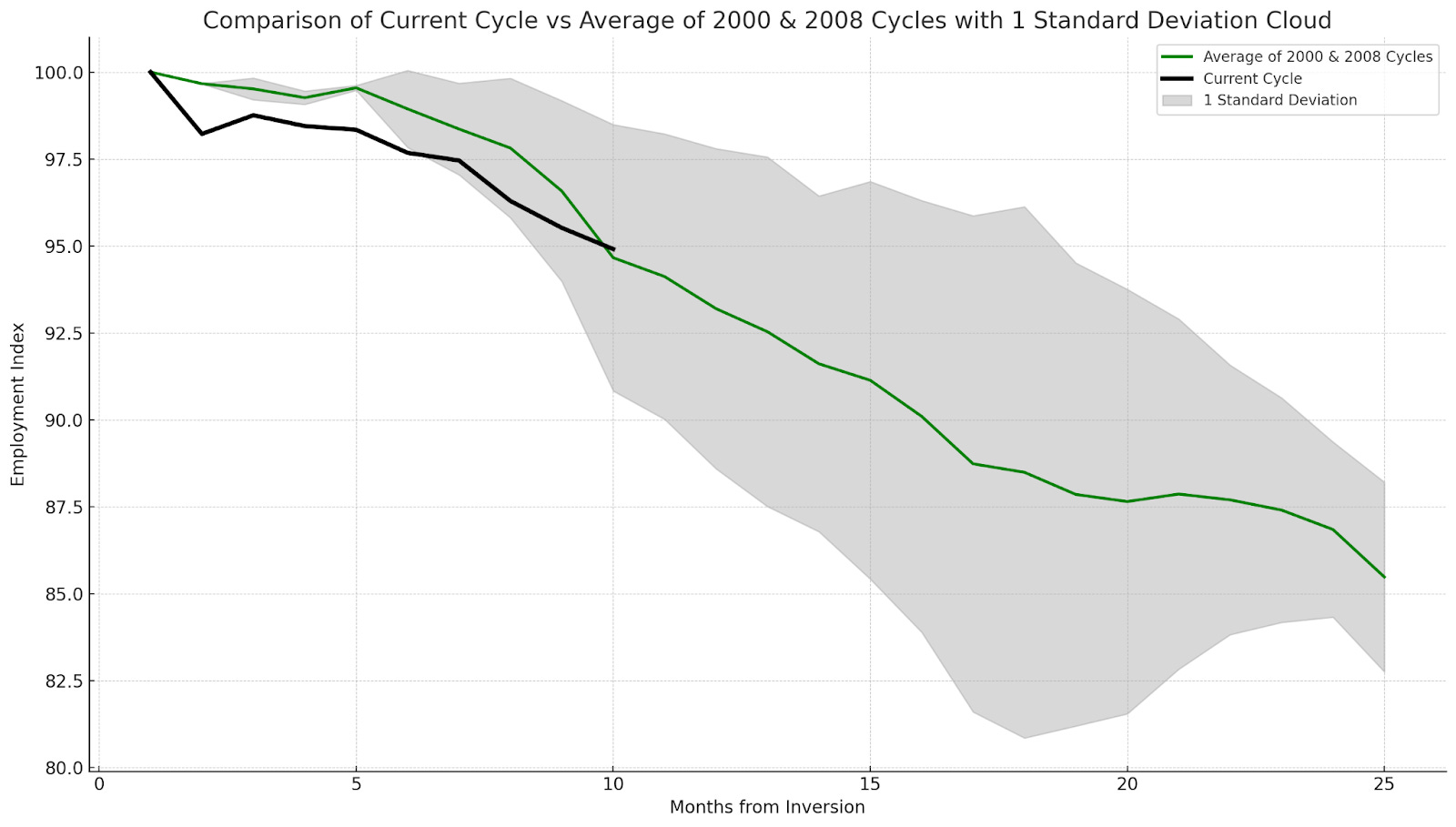

Turning our attention to the total temporary help employment index - this measures total # of temporary employees working within companies. During periods of growth, companies bring in temporary help to assist with operations and during times of capex shrinkage, the opposite occurs. This index has had a historically reliable lead time to actual recession, and you can see how we are fairing versus previous cycles here:

We are very closely tracking the 2000/07 cycles on the temporary hire front, and I expect this decline rapidly into the coming months (along with job openings).

Shifting our focus to the manufacturing front - I want to focus particularly on manufacturing inventories, and I will have a graph for you all next week. Inventories continue to decline slowly from their peak and this has been another leading indicator that can be followed to track the health of the broader manufacturing sector. Next week I will take a closer look into IT inventories with all the hype around ‘AI/tech’ manufacturing being ‘onshored’ back into the United States… something I think has been overhyped in the shorter term timeframe.

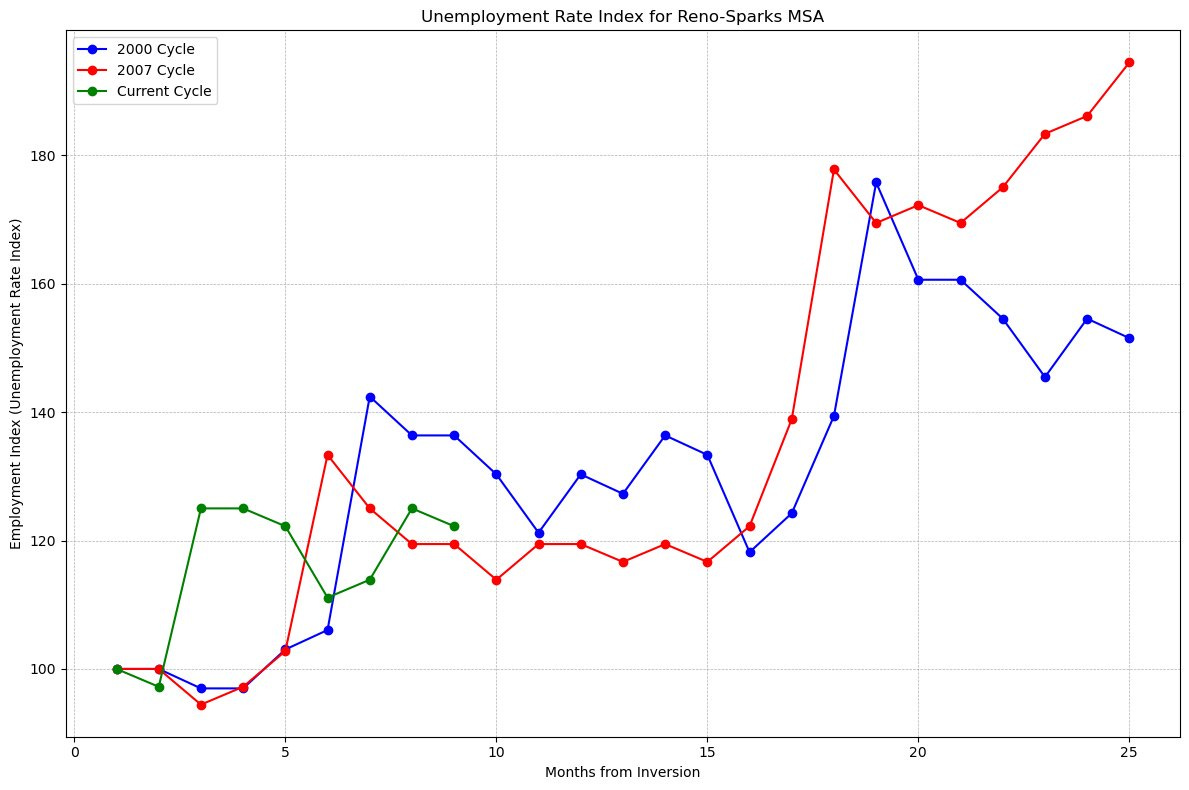

Lastly so we can get this piece out on time for you all - I wanted to document Reno-Spark MSA’s current unemployment index versus 00/07, and it is smack in the middle of those two cycles. Reno has seen unemployment rise a ways from the bottom set all the way back in November 2022 and has continued to drift higher from that point. I expect that Reno may be a city hit quite hard in a downturn and we might see something that looks like a mixture between Dotcom and 07 for the city on the employment front… but that remains to be seen.

Notice how Reno follows the same Nevada trend of month 15 marking the end of the ‘fantasia’ period as unemployment rises sharply from month 16 following inversion in previous highlighted cycles. This data is a bit dated, so I will make sure to update this for months 10-11 when the data is released.

For now, have a great evening and start to your week, and I’ll see you around.

Don

Paradigm Shift (@SixFinance, MacroEdge Head of Research)

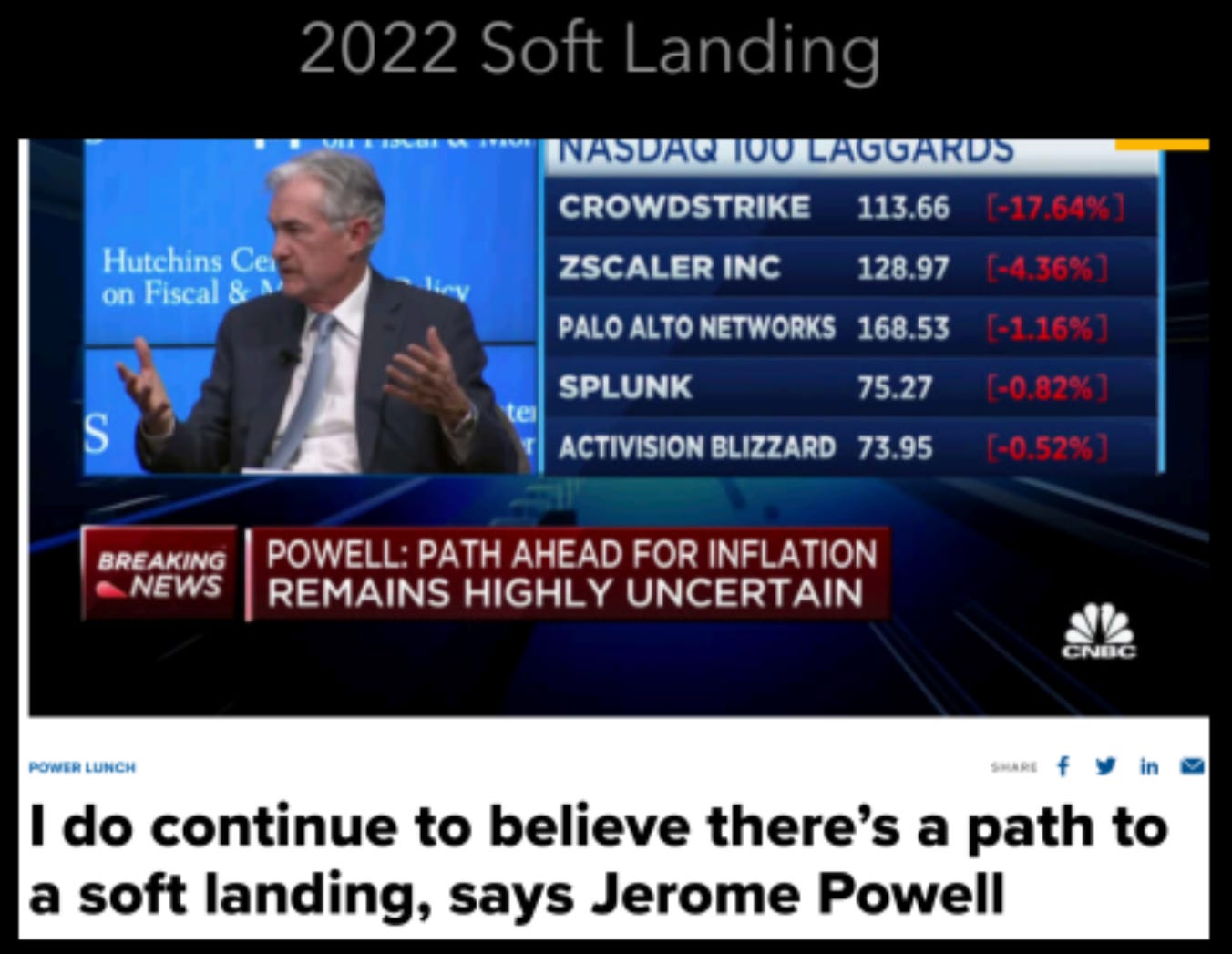

“Higher rates not just for longer, but maybe forever” was the title of FED mouthpiece Nick Timiraos’ article following the hawkish pause issued by the FED this week. FED did not choose to raise the federal funds rate this week but they left future increases on the table, along with a very important revision in the FED dot plot of only 50 basis points of rate cuts penciled in for next year.

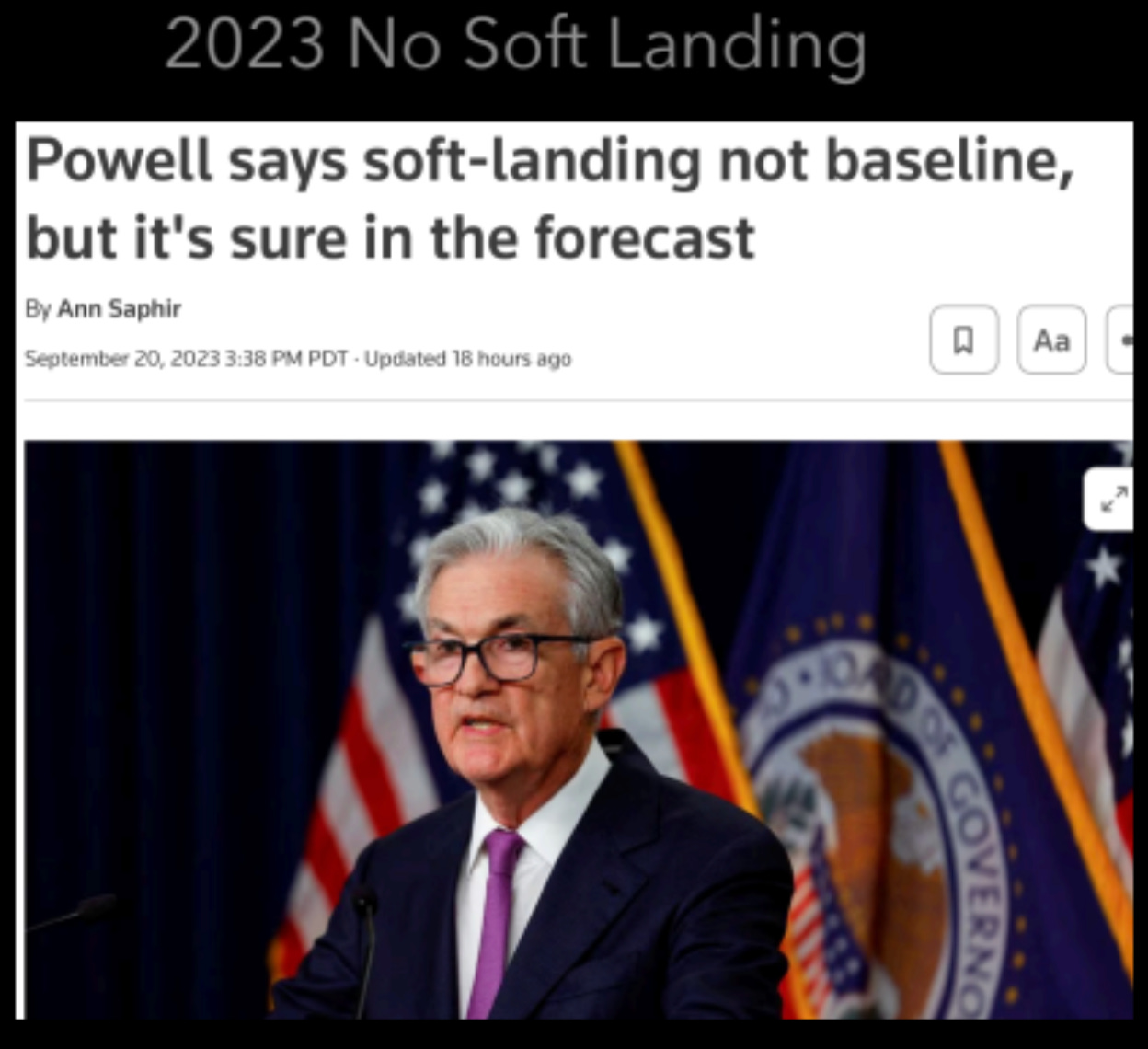

The most notable to me part of was when Jerome Powell said “I would not call Soft Landing a Baseline Expectation”. This was noted but glossed over and is a very important piece of FED rhetoric. That is the chairman of the Federal Reserve telling you to buckle up.

Risk assets dropped substantially this week with the S&P500 dropping over a hundred points in the days following FOMC, with each day closing on lows. Big MOC imbalance orders to sell were the theme of the week with billions of MOC to sell orders popping up. Nvidia, a great benefactor and the golden boy for AI hype now currently sits at nearly 20% drawdown from peak. We have covered NVDA in depth here so I won’t beat a dead horse although I do expect its’ drawdown to continue.

The ten year yield hit 4.5% briefly, a marked and important number following the FED as the fixed income benchmark yield soared late in the week.

Market repricing of risk and forward growth possibilities has been notable this week. A “paradigm shift” of what is to come has been shown by the FED.

Oil remains on a tear despite a small correction to end the week, hot on the heels of 3 figure oil price target estimates by bank analysts. As usual, when the banks all get bullish on something after it has already ran significantly it may be smart to start locking in some of those gains if bullish. To frame world governments oil price opinion with one anecdote: today French President Macron said “France asks oil industry to sell fuels at cost”.

Regional banks balance sheets continue to get hammered as all of their low yielding debt holdings accumulated during ZIRP get clobbered as yields rise substantially. The 10yr yield remains about 50 basis points higher than when several large banks collapsed already this year from bank runs due to solvency risks briefly shocked markets until the FED instituted emergency Bank Term Funding Program (BTFP). Without this program it’s highly likely we would’ve seen a cascading domino effect throughout the regional bank space. Steve Eisman of big short fame last week called banks currently “uninvestable). Due to the rise in yields, regional bank balance sheets and their equity positions are likely being crushed with the BTFP keeping depositor liquidity available. To compound issues for regional bank stocks, they’re now paying FFR +10bps to access liquidity. *disclaimer- short regional banks KRE remains one of my largest positions*

Early on in the week ahead we may see a bounce to punish late shorts, but I expect more selling as valuations continue to compress as reality sets in for risk.

FDIC insured Certificates of Deposit at global systemic important banks and Tbills remain a great position for the intelligent investor at this stage of the cycle especially with current yields.

Under the Radar (@SquirtLagurtski, MacroEdge Contributor )

In 2020, the Covid-19 pandemic took center stage and has been rippling through the economy ever since. Economic events have become front and center in mainstream media, and on social platforms alike. Between a pandemic, an election, insurrection, riots, wars, and most importantly, a recession, hysteria has dominated airways and social threads. The American consumer now juggles hybrid working schedules, higher costs, an increasingly tight budget, and evolving macro events that require at least passive attention. There's growing speculation behind government spending.

I choose to dig where the headlines aren’t. Looking around hysterical headlines and political fanatics has always been my approach. While I don’t view them as coordinated attempts to distract us, I always try to remember that a good scandal never goes to waste in Washington or Wall Street. Such environments can be beneficial for advancing other narratives, like renewable energy, for instance.

Since 2020, there have been major moves in the advancement of the alternative energy space. In March 2020, for instance, the US Nuclear Regulatory Commission reviewed a license application for an Advanced Fission Power System. Oklo Inc. had been developing its plans for the plants in Piketon, Ohio since 2016, and it now produces 1.5MW of clean power.

Note: Piketon, Ohio, is also where Centrus Energy Corp will begin producing HALEU (High Assay Low Enriched Uranium) nuclear fuel in October 2023. It's the only US facility licensed to enrich Uranium up to 20%.

This Ohio facility is a fission power system that generates 1.5MW of clean power. What's remarkable is its capability to use nuclear waste as fuel, rendering it completely carbon neutral. It produces both electricity and heat.

In May 2020, the Department of Energy initiated the Advanced Reactor Demonstration Program (ADRP). This program's aim is to bolster the deployment of advanced nuclear reactors to fortify energy security. With a funding aim of $3.2Bn over seven years, the ADRP seeks to establish partnerships between private and public entities. The goal is to get these reactors operational within 5-7 years. This signals a profound commitment to the nuclear energy industry in the US and the establishment of a global supply chain to support the industry. A notable observation is how a small number of both private and public companies progress alongside one another. This is with growing interest from the US government/military, which, for the last decade, has been promoting energy-dense technologies such as wind/solar. These technologies, although promising, have proven to be cost-intensive and inconsistent, with unforeseen negative environmental impacts. For instance, wind farms have reportedly been confusing whales during mating seasons, leading to disruptions in their feeding, migration patterns, and even causing beachings in ocean-based setups. Solar energy, on the other hand, lacks consistent stability in their generation, especially during seasonal shifts, peak demand times, and extreme weather events. This is especially notable when juxtaposed with the potential nuclear energy offers.

In August 2023, Nuscale Power (SMR) received a groundbreaking approval for their Small Modular Reactor design. Dubbed the VOYGR-6, this design boasts a 77MWe capacity, enough to power 60,000 homes. It can support a vast range of private and industrial applications.

Note: President Biden has allocated $14Mn to assist Romania in acquiring a VOYGR-6 plant as part of a global push to expand clean energy. Additionally, Chubu Electric in Japan has taken an undisclosed equity position in Nuscale Power.

October 2020 saw the Department of Energy awarding $80M each to Terra Power and X-Energy to construct advanced reactors, funded by the ADRP. Terra Power, initiated by Bill Gates, has been forging partnerships for its Natrium project in Wyoming. This project, in collaboration with BWXT Technologies (BWXT) and GE Hitachi, is touted to produce 345MWe through a sodium-cooled fast reactor equipped with a salt-based energy storage system.

Note: Terra Power has awarded contracts for the project to both BWXT for design/engineering of the heat exchanger. BWXT also partners with Nuscale for engineering SMR technologies. GE Hitachi collaborates with Terra Power to design and implement a 500MWE energy storage system. This system will boost the Natrium facility's performance and stabilize energy during peak demand.

The Natrium project, located near a PacifCorp coal plant in Kemmerer, Wyoming, is a testament to the numerous commitments by private, public, and governmental entities. Billions are being invested in long-term funding to rapidly revamp the US energy infrastructure. Notable names in this initiative include Westinghouse, BWXT, NuScale Power, Centrus Energy, and mining firms like Cameco (which owns 49% of Westinghouse) and NexGen Ltd. All these entities are actively expanding to support a burgeoning alternative energy supply chain.

I will be actively following these developments to relay information that seems obscured from the public view.

The Federal Reserve, What are they good for? (@GregCrennan, MacroEdge Contributor)

The Federal Reserve, often referred to as the "Fed," has a dual mandate: maintaining stable prices with a 2% annual inflation target and ensuring low unemployment. However, recent decisions and statements by Fed Chair Jerome Powell have raised questions among many Americans about whether the central bank is effectively fulfilling its role in controlling inflation and supporting the economy.

At the latest Federal Open Market Committee (FOMC) meeting, the Fed faced a crucial decision. Despite unemployment being currently considered low but slowly rising, one might expect the Fed to raise interest rates to combat soaring inflation. After all, inflation has been averaging around 4.5% for nearly four years, well above the Fed's mandated 2% price stability target set by Congress. Yet, despite indicating last year that raising interest rates was their primary tool to tackle inflation, the Fed opted not to increase rates at this meeting, leaving many wondering about their effectiveness.

This move has prompted many to question the Fed's commitment to its price stability mandate. Gas prices, in particular,have surged, nearing record highs and experiencing almost a 100%increase since January 2021 and 30% in 2023. When asked about this significant increase, Jerome Powell responded, "The Fed tends to look through energy moves that we see as short-term volatility." This response has raised concerns about the Fed's apparent indifference to the rapid rise in energy prices, even as OPEC and Russia reduce supply, and the Strategic Petroleum Reserve (SPR) is being tapped into to limit the short-term price increase in gas, increasing the risk of even higher energy costs in the near future.

The disconnect between the Fed's actions and its mandate is becoming more pronounced. During the press conference, Powell's stance on a "soft landing" for the US economy seemed to waver. While he initially expressed confidence in this scenario earlier in the year, he later admitted, "No, No, I would not do that...I thought there was a path to a soft landing, but there are factors out of our control...and we will restore price stability." This sudden shift in tone raises questions about what Powell may know that the public does not and why he isn't more transparent about it.

Furthermore, concerns over a potential credit debt bubble and widespread public dissatisfaction with the economy were addressed indirectly. Powell acknowledged that people "hate inflation, hate it," and this contributes to negative perceptions of the economy. However, he failed to fully address the underlying issues causing discontent among Americans.

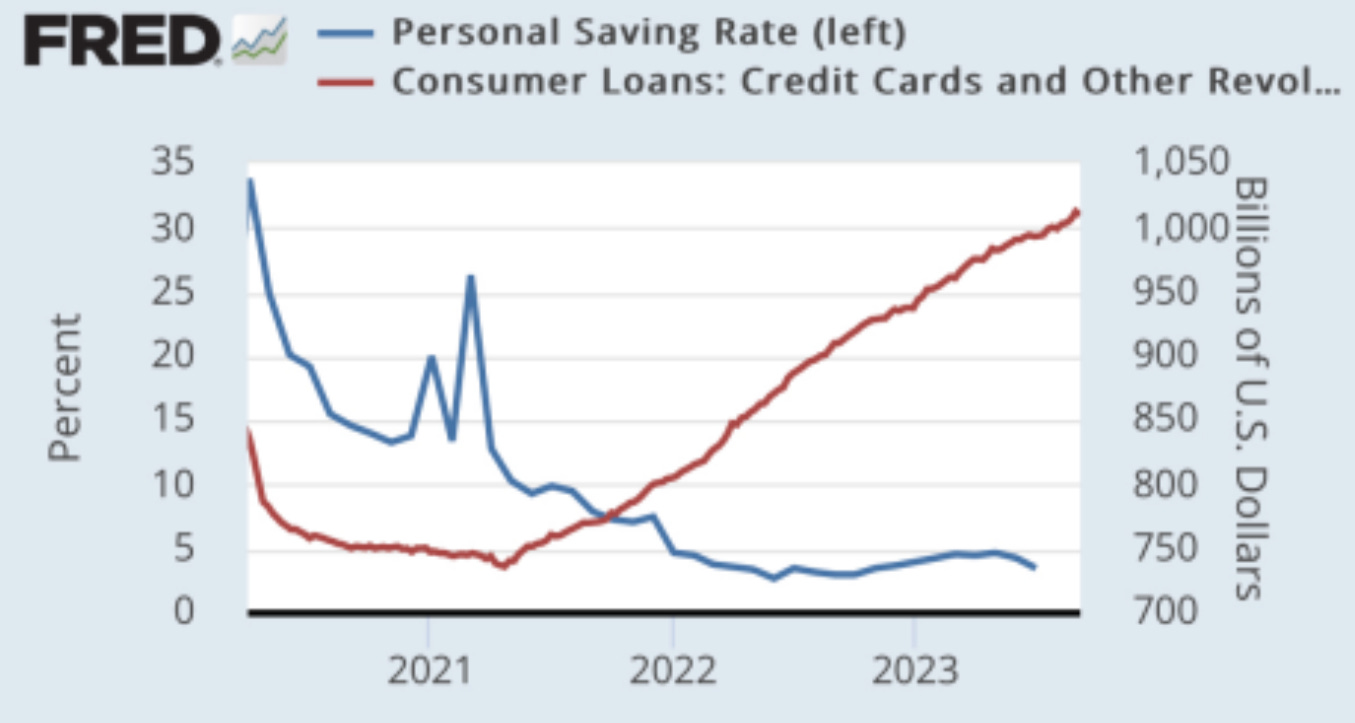

The reality is that many Americans are feeling the strain of massive inflation since January 2021, depleting their personal savings, as real wage increases have not kept pace with rising prices. The gap between reported inflation with the CPI and PCE indexes and the actual cost of goods creates a stark disconnect between what people read or hear in the news and their everyday experiences. This gap has led to increased credit card debt, which recently hit a record $1 trillion, as people struggle to maintain

their standard of living in the face of skyrocketing costs, including gas prices approaching $4 per gallon nationwide, with some areas exceeding $7, as seen in California.

One telling statistic is the decline in US retail sales after adjusting for inflation, marking the longest consecutive year-on- year decline since 2009. Americans are now paying more for fewer goods, and this trend is reflected in rising sales at gas stations while non essential purchases like iPhones are suffering.

In conclusion, as the Federal Reserve grapples with rising inflation and its mandate for price stability, questions about its effectiveness and its impact on the middle class are rising just like inflation. The Fed's mixed messages and apparent reluctance to take decisive action on inflation like Paul Volcker did, have left many wondering: What is the Fed good for, if not to help the middle class weather the storm of rising prices and economic uncertainty?

A Dark Reminder For the Stock Market From 1987 (@RealJohnGaltFla, MacroEdge Contributor)

I have been known to be a bear. Hell, I’ve also been known to preach some doom, gloom, death, destruction, and the end of civilization.

Based on current events, that would seem to be a sound analysis of everything that is happening in our world today.

My preference though, is to analyze history and look at things from a different perspective from everyone else and see if patterns emerge that replicate other troubled times in history. On FinTwit (Financial Twitter) and among some friends I have been publishing a chart which should be a dark reminder to those ignorant of history.

In 1987, the US 10 year Treasury had yields shoot up as there was fear of the economy overheating and a new untested Federal Reserve Chair was facing the potential of a revival of inflation, the destructive economic consequence of the 1970’s and weak Fed leadership.

Unfortunately for the new Fed Chair, he would face a crucible by fire just two months after assuming the office on August 11, 1987.

That’s right boys and girls, the one and only Alan Greenspan.

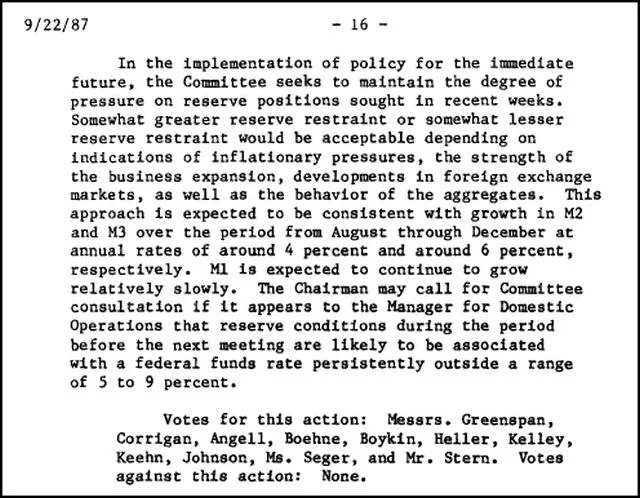

On September 22, 1987 in one of his early FOMC meetings, the following excerpt from the Fed Policy Statement stated the following:

Throughout the statement, Greenbook, Bluebook and other Fed publications and public pronouncements there was no indication of a pending panic, no excitement over an economic event, some concern about potential inflation, and very little worry that economic growth along with monetary expansion would create a problem for the economy.

The market, however, had already taken over the policy decision from the retiring Volcker and incoming Chair Greenspan by starting a rocket ship in the 10 Year US Treasury Yield starting in the spring of 1987:

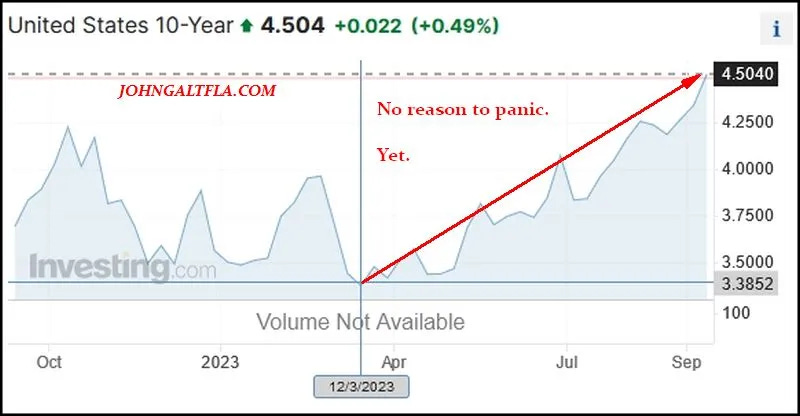

Thus this author’s reference about the whining on business television, radio, and FinTwit today about a 4.50% 10 year yield almost, I repeat almost seems laughable.

The past year has had some interesting price action in the 10 year yield also:

There are key differences between that era and this one. The entire “safety” trade was based on the newfangled (technician term) Portfolio Insurance which was engineered to prevent cascading sales and crash events. That did not work. Thankfully we have 0DTE options and ETF’s for everything imaginable which are much, uh, safer alternatives. We hope. And no, I’m not being serious with that statement, it’s a Ford Pinto with Firestone 500 tires wrapped in a flaming Tesla doused in gasoline.

Thus should the 10 year suddenly pierce the 5% yield by early to mid-October not only will my alarm increase on these pages but my mattress might get fatter after I tap my bank for every note they have in circulation. Because this time if we have a 22.6% crash, I fear this country may not return back to normal as we once knew it.

Got gold?

Great coverage!! Very insightful. Thank you.