9/17 Weekly Report - 'Labor Market Vacay', Considering California, a Freight Update, Inflation, and a Russian Punishment...

In this weekly MacroEdge Report - Don, CH, Squirt, Greg, and John take on everything from Nevada employment data, industrial production, California demographics, the freight market, and more...

9/17 MacroEdge Weekly Release

@DonMiami3, MacroEdge Chief Economist

@Econimica, MacroEdge Contributor

@SquirtLagurtski, MacroEdge Contributor

@GregCrennan, MacroEdge Contributor

@RealJohnGaltFla, MacroEdge Contributor

Weekly Data Dive and the Labor Market in ‘Vacay Mode’ (@DonMiami3, Chief Economist)

Hi all, glad to be back and just wrapped up a nice vacation myself from the 24/7 news updates of Bloomberg and X. Was very nice to escape from the hectic city life for a few days out in the flyover states and meet with/connect with some fantastic people over some great beer and great (sometimes mediocre) golf. In my short 38,000-foot update for this week - I wanted to provide you all with an update to the bellwether ‘bubble city’ labor market data and update some charts (particularly industrial production and capacity utilization) that can be used to assess how this economic cycle is progressing. Glad some of my charts on the California unemployment rate are being discussed - although some of the interpretations were wrong given that California’s unemployment has historically lagged

While we are entering Fall - a period marked by peak work hours to pay for those expensive Christmas gift tabs and Thanksgiving holidays ahead - and the summer ‘vacay’ peak travel season is now swiftly behind us - the labor market is entering its ‘vacay mode’ at this point in the economic cycle. Based on past historical patterns - the next 4-5 months are going to be crucial to watch to see if the Fed will manage a soft landing (not my opinion) or a hard landing (my opinion).

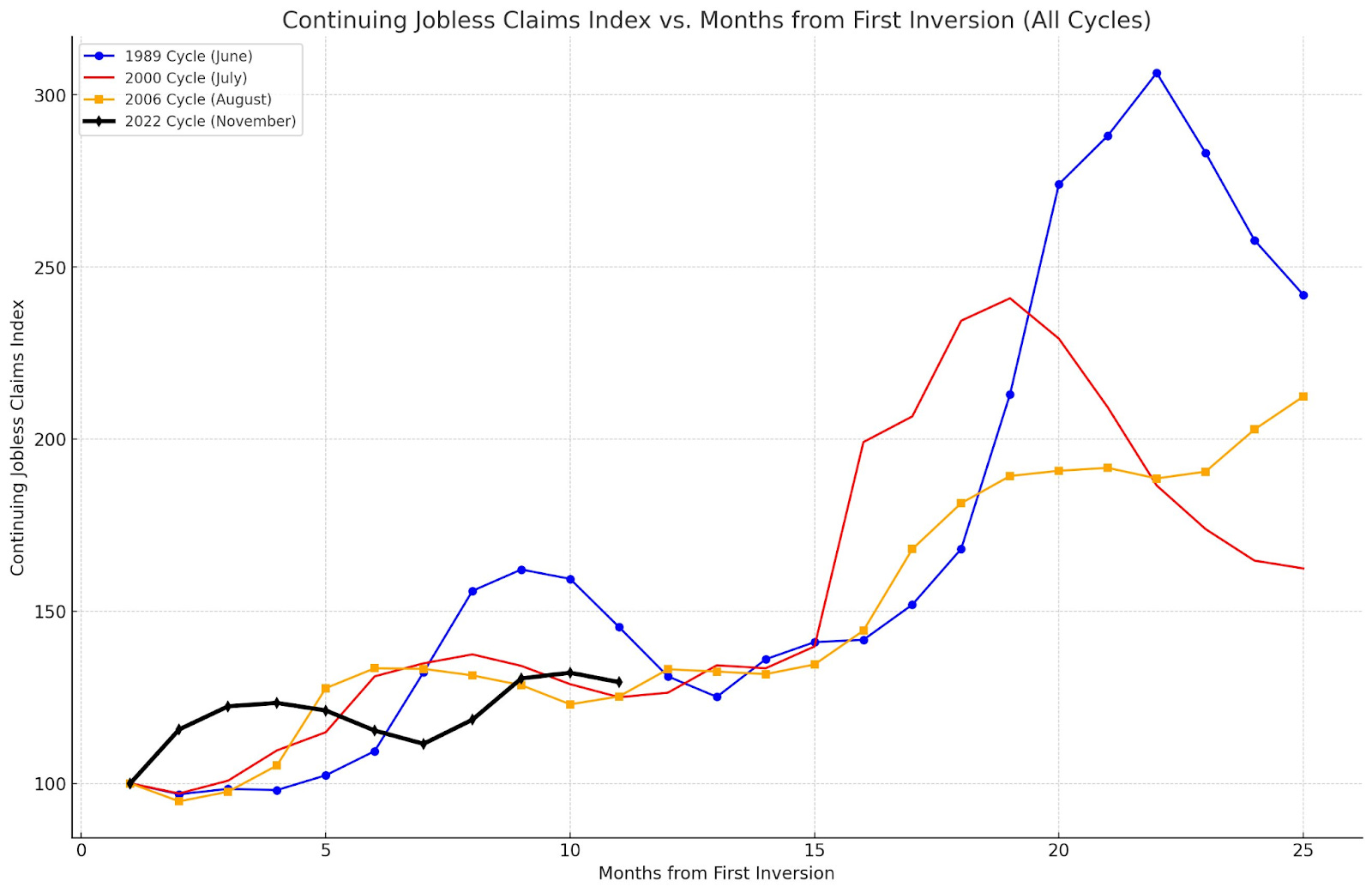

This chart for the Nevada job market includes the latest September continuing claims data as the marker for month 11 (first week of September, so still a bit behind), and you can see how tight the next 4 months gets here:

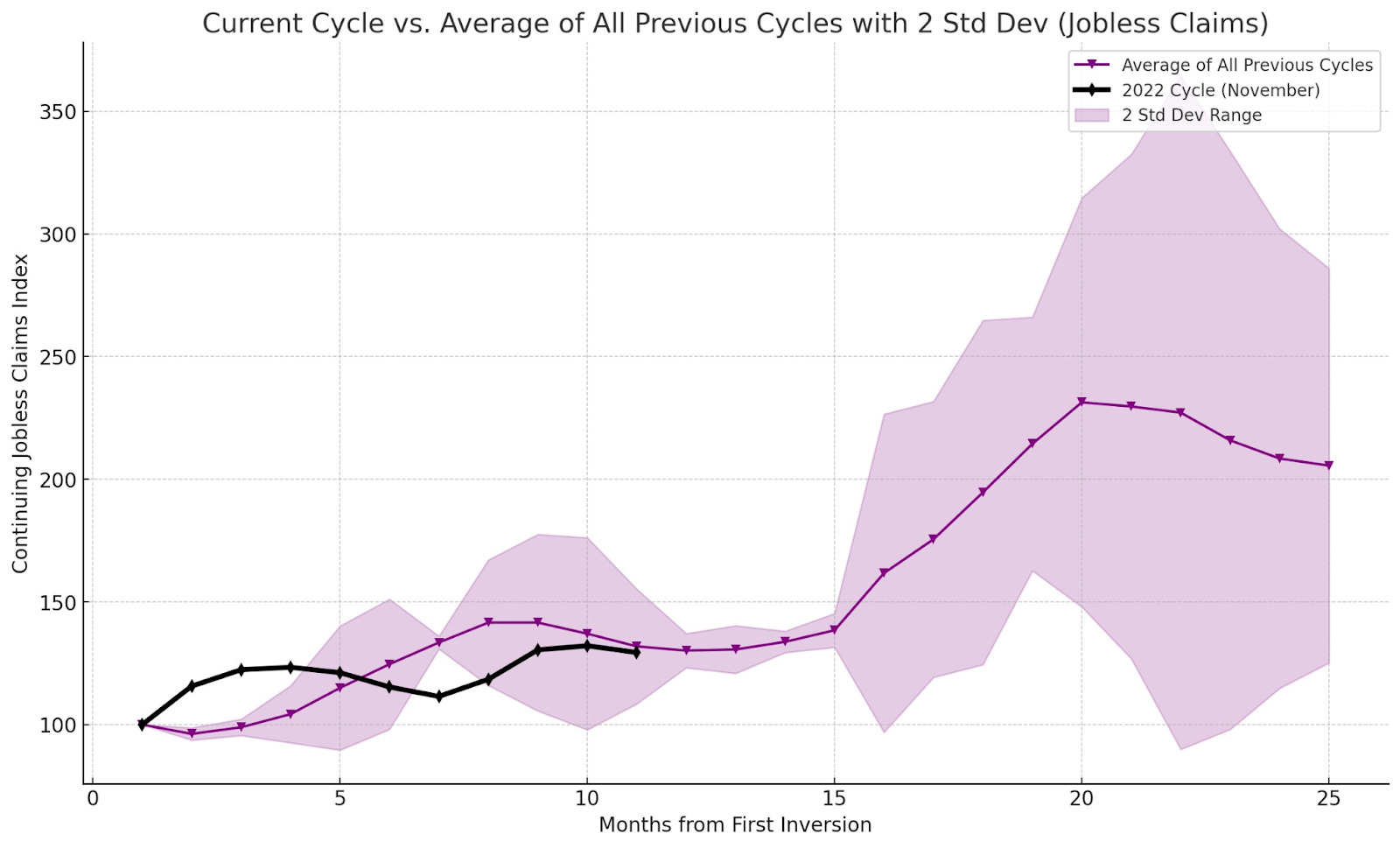

The standard deviation window across previous cycles narrows to the very tight range up until month 15 (which would be Q1 of next year) - so we may be entering a winter lull for the labor market now assuming that this cycle isn’t moving faster than previous cycles for the Silver state. I may be taking a trip around the country in a few weeks time to gauge how various markets are performing (looking at things like restaurants, hotels, tourist traffic and more) so that could be further insight into how things are looking under the hood.

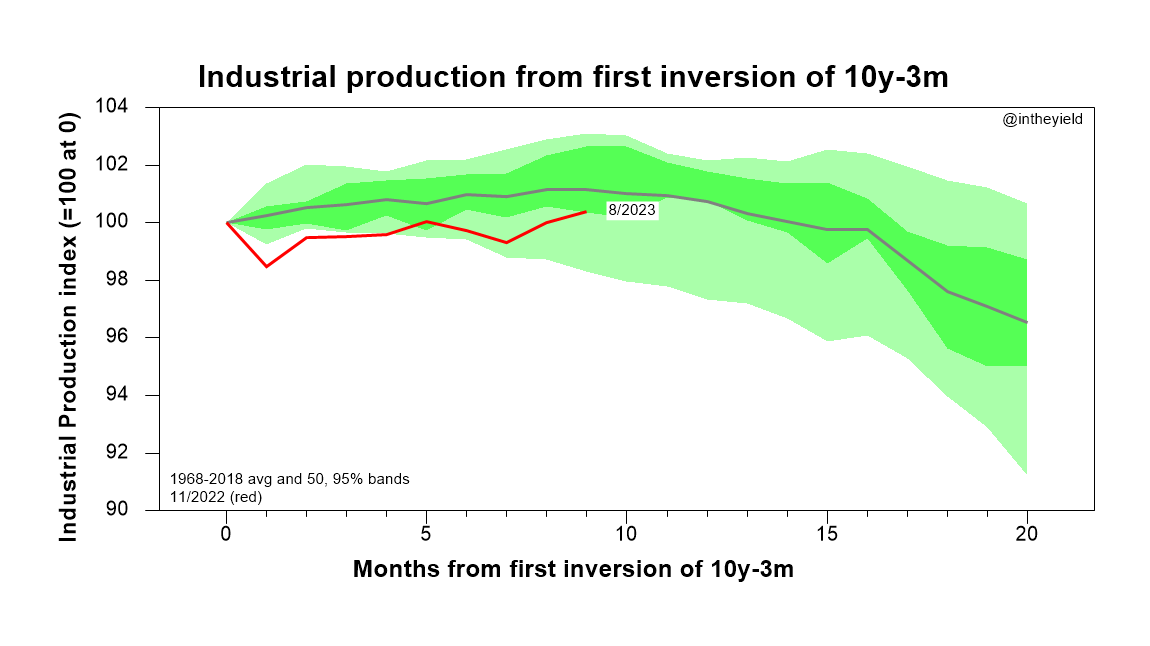

Lastly looking at industrial production and capacity utilization - industrial production is working on reclaiming its September high from last year - so not yet pointing towards recession, while remains a ways off the high. Industrial production tends to lead the labor market (charted above) following inversion… so if we’re following the average, we should begin to see this trend down or stay in the range over the next many months.

I will keep you all posted on the progress of our data dashboard and other news relating to MacroEdge as things continue to progress. Kept tonight short given how in depth some of our contributor pieces are - so hope you enjoy and have a great week…

Don

Considering California… A Deep Demographic Dive of the ‘Once’ Golden State (@Econimica, MacroEdge Contributor)

Demographics is usually kind of like watching grass grow...but when something somewhat shocking is taking place, and nobody seems to be talking about it...well it deserves a spotlight.

I think it's fair to say, so goes California, so goes the US...

So here goes a quick article on California annual births versus California home prices...let's dig in.

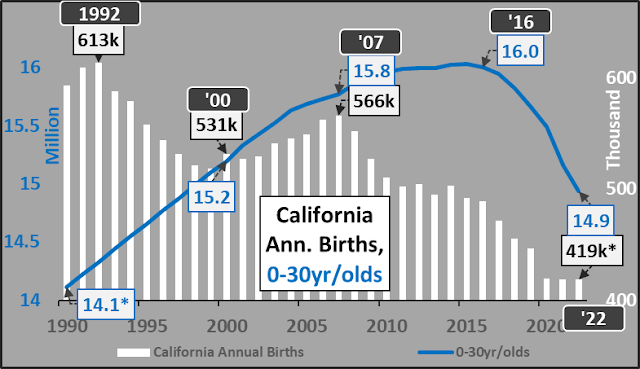

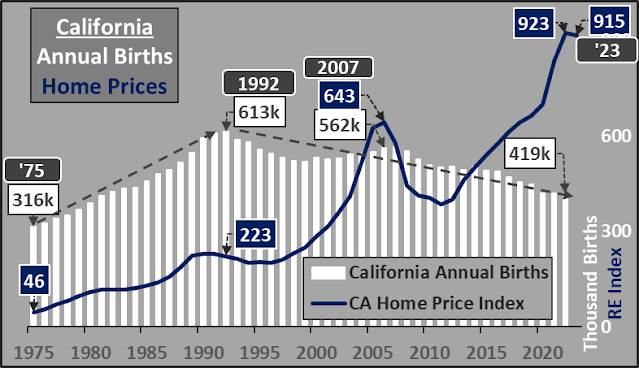

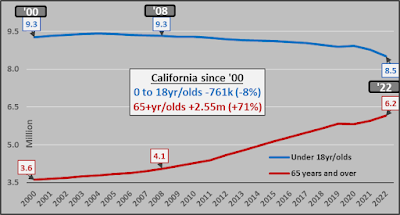

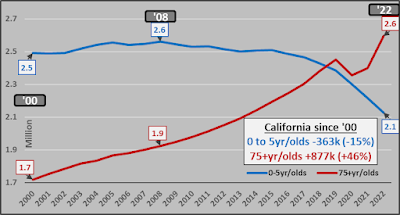

1- After rising for a century+, births in California peaked in 1992 and have been falling precipitously since. Annual births have now declined by nearly 200 thousand or -32% amid the largest childbearing population in US history. The decline in births (inclusive of ALL births, regardless parents' legal status) has been going on for so long that now the under 30-year-old population has begun the follow through of that birth decline. A like 30% (and growing) decline is to be expected eventually for the entire population of the state, working its way from youngest to eldest population segments.

Soaring housing prices amid declining annual births would seem logical as young adults are most likely to be negatively impacted by the rising costs of living...and choosing to forego marriage, children as a result.

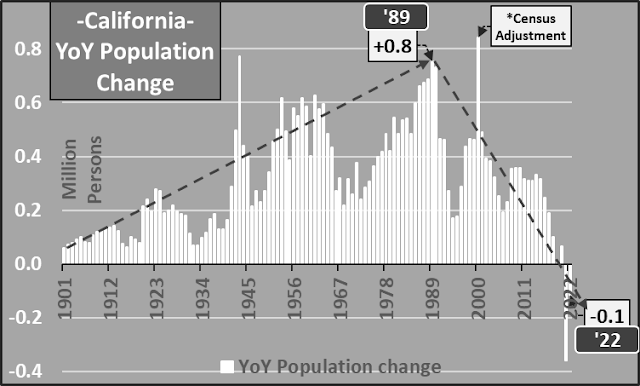

Unsurprisingly, California's annual population growth accelerated, then peaked in 1989, and was decelerating until 2019...then outright declining since. Many assume it's the state's politics, or tax policies, homeless, or unaffordability driving a temporary decline...but in truth, California's decline is coming from bottom-up negative demographics...only worsened by the sudden exodus.

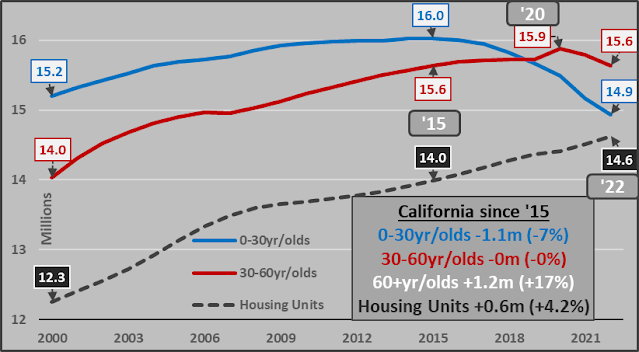

A perusal of California's population by age groups (0-30yr/olds, 30-60yr/olds, 60yr/olds vs total housing units) highlights that the youngest segment began its demographic driven secular decline in 2015 (following the declining birth trends) and the 30 to 60yr/old segment began its decline in 2020. The 30 to 60 year-old cohort began falling earlier than it was going to demographically...primarily due to a slew of political, business, tax, and lifestyle issues in California. However, housing unit creation continues unabated.

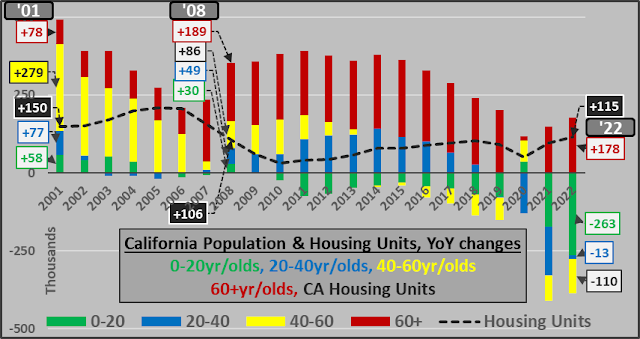

Below, California's year over year changes in population, by 20-year age groups, set against annual growth in housing units. The demographic deterioration is easy to see. All segments are now in decline except the ongoing growth of elderly...demographically, these trends are likely to not only continue but accelerate.

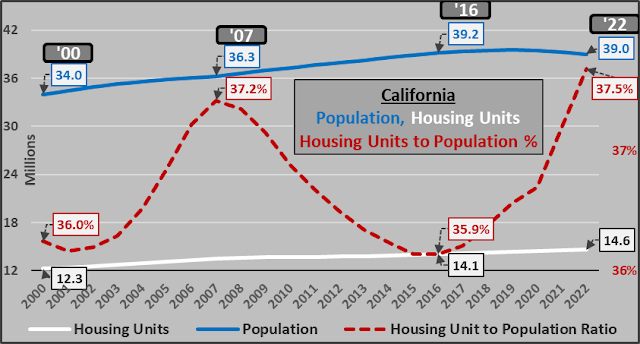

Putting California's declining population into perspective against its rising housing units...take note of the red line, detailing housing units per capita in California at a new all-time high, surpassing the previous peak set in 2007. This is just to suggest that there isn't a housing shortage, rather a housing affordability crisis which isn't borne of inadequate housing...but inappropriate Federal Reserve set interest rates and asset purchasing, federal government debt creation, and state/local tax/regulations (ie, Proposition 13 (1978) limiting the property tax rate to one percent of the property’s assessed value plus the rate necessary to fund local voter-approved debt. It also limits increases on assessed values to two percent per year on properties with no change of ownership or no new construction).

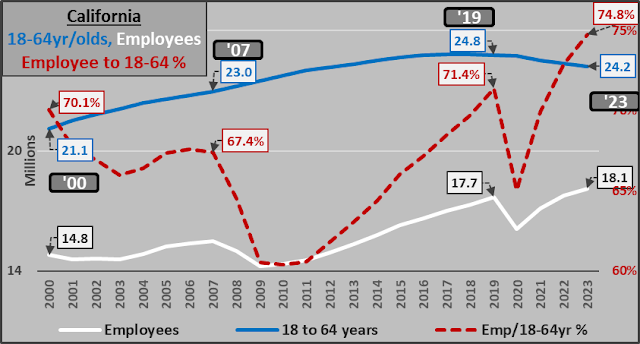

I suggest a crisis is imminent in California as a shrinking working age population is at record high total number of employees (and likewise record employment %)...suggesting there is little to no further fuel for employment growth available. The demand pushing that record employment was short-term interest rate driven deficit spending, stimulus, PPP (much of it straight fraud), etc. etc. As the Federal Reserve is "normalizing", demand and resultant employment will likely fall precipitously.

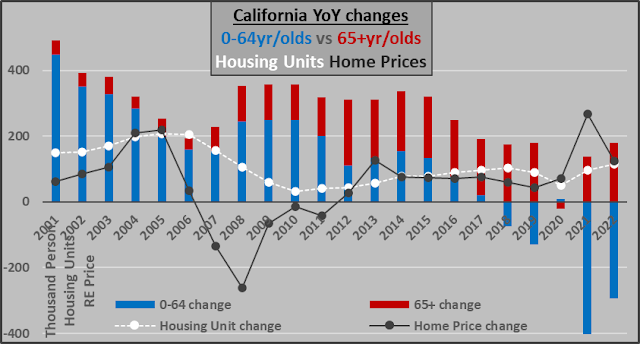

Below is annual California population change (divided between under 65yr/olds vs 65+yr/olds), annual change in net housing units, and resultant change in home prices. Given the declining under 65 year-old population makes up essentially 100% of the 1st time home buyers, 90%+ of the states employees...the imbalance of inverting demographics, record high home prices, record housing units per capita, at record high short-term debt fueled employment rates, amid significant ongoing housing unit creation could/should give one pause?!?

The idea is to keep this article short...so I will not detail the interest rate and asset purchase manipulations that resulted in a housing price surge amid decelerating/declining quantities of potential housing occupants. But just understand as long-term organic demand moved lower (left to right), short-term synthetic demand moved upward (left to right). If those short-term manipulations are not maintained &/or increased...a likely housing price decline or collapse would be the most likely end-result.

*Demographic and housing unit data thanks to US Census, Home price index thanks to US FHFA.

PS - how this started, where it's going...

Extra credit charts...since I made 'em, think they're interesting, might as well post 'em.

A Freight Update and Greener Pastures (@SquirtLagurtski, MacroEdge Contributor)

Truckload carriers are seen cutting capacity with equipment returns, and an increase in qualified drivers. Renewals have also been on a decline as small carriers grapple with everything from high diesel prices to higher cost inflation, and high interest rates. Spot rates have been in decline for over a year and spent much of the summer season bobbling near lows as the Covid boom during the pandemic is well past and smaller carriers have burned through raised capital. That doesn’t, however, seem to have industry leaders too worried.

“It’s still too early to forecast what might happen on contract rate renewals next year, but a decline is unlikely,” Jim Filter, Schneider’s group president of transportation and logistics.

The freight market has been searching for a balance for the better part of two years now as U.S consumers battle sustained higher inflationary pressure and uncertainty in multiple layers of their everyday lives. With summer winding down and peak season past, companies have reported a mixture of restocking, though Schnieder is looking at the next three months to have steady seasonal activity with expectations reigned in as consumers pull back from spending. Back to school shopping brought some demand improvement along with Halloween seasonal items doing a little better than expected. But the effect of those categories is not expected to change the outlook for the rest of 2023. Instead, companies are looking into 2024 for material improvements and further rebalancing of inventories.

Companies across the country attempt to equalize their inventories to a changing demand picture the flat spot rate market emphasizes the shifts occurring within the economy and how consumers are spending their cash. Student Loan payments are set to start in October, credit debt is still rising, and delinquencies are starting to get attention, the strength of consumer going into holiday shopping season is a big question mark. Schneider National lowered its 2023 earnings guidance in an August earnings report. Currently the Panama Canal has been backlogged since spring from a drought, current conditions are persistent and leading to the Canal Authority to release stating transits may be further reduced, and GXO Logistics reported intent to lay off 92 workers in a Texas distribution center due to losing a customer. Earlier this year GXO laid off 286 workers at several locations in the US, one of them also in Texas in Fort Worth. GXO Currently employs 130,000 people globally in 27 countries and has nearly a thousand warehouses.

Over the past decade the idea of consistent renewable energy always seemed unreachable, unaffordable, unsustainable, and expensive. However as the climate change narrative from the early 2000’s brought us steel and paper straws, it would accelerate during mid 2010’s into outright activism, but when the pandemic struck us in 2020 and an election scandal would sort of blur the vision we had around its progress, its cost, but more shocking to me personally its effects on.. The environment. It worsened. There has been no admission of naivety to the growing number of events currently playing out in the US, There’s certainly enough to track but the solution we were told would replace our outdated infrastructure hasn’t materialized for the majority of US tax payers just yet and in fact, the farmland I see now littered with solar panels and overgrown grass doesn’t make me feel as if renewable futures are too bright here in southwest MI. Reports on the east coast of whales beaching, getting confused while searching for food from the wind farms humming along, entire habitats being substantially effected doesn’t seem very environmentally friendly.

Nuclear energy has always been the dirty adversary to renewable ideologies due to its shady past in wars and accidents alike. However, it seems to still be lucrative for some. While researching into Uranium mines and their potential in Virgina I came across Small Modular Reactors being sought by the US Miltary to power remote and hard to access areas which could be used as self-sustaining powered defense sites or any other number of possibilities.

Terra Energy is excitingly investing in Kemmerer Wyoming. Their Natrium Project has been underway since September of 2020 and is a partnership between Bill Gates’ own Terra Power, and GE Hitachi, Terra recently awarded BWXT Technologies a contract to “explore the feasibility of introducing small-scale nuclear reactors within the state of Wyoming”. The role of GE Hitachi is the addition of capacity to the site and its overall running output of 345MWe, boosted by 500MWe during higher usage times and under certain gaps in consistency or interruption of other renewable sources. And improve overall sustainability and consistency in general.

To me that reads as if the super expensive renewable energy still costing tax payers is already needing to be assisted by the very source of energy our government and activists fought to keep out of the spotlight, while some even actively pushed other sources onto consumers while they invest and gain from it. Small Modular Reactors are part of a growing branch in the nuclear energy space for good reason. Boasting a 30-80 year lifespan multiple governments and private companies have been collaborating on their design. These systems are much simpler and easier to manage than your conventional reactor systems and have the potential for commercial, industrial, residential, and military applications. The Department of Energy is working with multiple companies to subsidize their inception and acceptance. Nuscale Power has the first fully approved design from the Nuclear Regulatory Commission, and has multiple other variations of their VOYGR-6 project in Idaho. Which just received approval its standard design approval. VOYGR-6 is part of a multi-year project to construct and expand a 463MW carbon free energy source that has been under construction since 2018 and has been progressing regularly.

I will add that costs relating to the project have been rising since beginning via cost target from $58/MWh in 2021 to now $89/MWh in 2023, reasoning for the increase has been explained as interest rate increases from the financing, as well as a substantial rise in materials costs for construction. The Department of Defense funding absorbed a large portion of those burdens however costs are still rising, bringing into question the projects future IF the conditions do not level out. Japan has a current 8.5% equity position for its own projects in the planning stages currently and is advancing them, so I would say there’s sustained interest in their capabilities as of right now.

Fueling these sites is a growing industry in multiple countries from India (which recently discovered more lithium), and Canada, Australia, and Asia with financing readily available and expansion underway currently from governments and private interest. NexGen Energy has been expanding their mining operations in their Rook I mine steadily and recently received $110M from Queens Road Capital ($70M+Shares as collateral for loan). The shares total a premium value of ~$743M themselves. Partnered with an Australian firm. A previous debenture from 2020 in the amount of $30M is already in place. NexGen leadership has well established history with mining and materials in the Australian and Asian region. Cameco Energy recently cut its production forecast which will likely raise the price of Uranium during a time which I believe it will also see consistent and growing need with such projects expanding. Of course, researching further is what I plan to do and if you’re looking for a more sustainable and growing energy play it’s worth looking into.

Weekly Data Dive and the Labor Market in ‘Vacay Mode’ (@GregCrennan, MacroEdge Contributor)

This week's inflation report has sent shockwaves across America. It marks one of the most significant increases in inflation since last year, leaving Americans deeply concerned as gas prices at the pump are approaching record highs again. Many of us this weekend are left pondering, “Why,” like in the song by Jadakiss, "Why do we have inflation? Why is inflation considered good by some? Why do we continue to repeat the mistakes of history?” Why can’t we solve this?

Why Do We Have Inflation?

Inflation, in contemporary terms, refers to the steady increase in the prices of goods and services over time. However, the original definition of inflation centered on the expansion of the money supply. But why does it happen? The primary reason is the government's ability to increase the money supply. But how does this occur? Government programs are funded through taxation, programs we voted for. When politicians promise new programs without raising taxes to cover the costs, the government resorts to printing money to bridge the financial gap such as this year where the deficit will be just shy of $2 trillion. This injection of additional currency into the economy, without a corresponding increase in goods and services, inevitably leads to rising prices as the market seeks a new Equilibrium.

So, why do governments follow this practice? One major reason is that politicians have learned that directly raising taxes on individuals can lead to electoral defeat. Since most people don't fully understand this inflationary process, governments often shift blame to external factors such as corporate greed, a strong economy, or geopolitical issues. This allows them to continue printing money, as we witnessed this year. An interesting side note: the last U.S. president to directly raise taxes on the population, George H.W. Bush, who lost his reelection bid in 1992.

Why Are We Told That Inflation Is Good?

Is inflation ever a good thing? Some argue that low inflation is favorable, but the truth is that no inflation at all is the ideal scenario. While some believe that inflation encourages consumer spending and business investments, it's worth noting that major shopping events like Black Friday, the biggest shopping day of the year, feature falling prices, not rising ones. This challenges the notion that inflation necessarily drives consumer spending.

Why Don't We Learn from the Past?

History provides a sobering lesson about the destructive potential of unchecked inflation. From the Romans debasing their currency by diluting silver content to the Weimar Republic's hyperinflation in the 1920s when money became so worthless that people carted it around in wheelbarrows, the consequences of runaway inflation are dire. Recent examples from Turkey, Zimbabwe, and Venezuela remind us of the tragic repercussions: soaring prices, vanishing savings, and social upheaval. So why do we repeatedly ignore these historical warnings?

Why Do Keynesian Economists Support Inflation?

Keynesian economists often advocate for policies involving a controlled level of inflation. They argue that moderate inflation can stimulate economic growth and reduce unemployment. They fail to mention other issues of having constant inflation like major boom and bust that the US economy has experienced since 1913.

In conclusion, the question of "Why?" concerning inflation is not just about why it's bad or why the government creates it; it's also about understanding the impact on our lives. At the Federal Reserve's target inflation rate of 2%, your dollars today lose 50% of their purchasing power in 36 years. Sadly, since we abandoned the gold standard in 1971, average inflation has been 4%, meaning your dollars lose 50% of their purchasing power every 18 years. This continuous erosion of wealth, especially for the middle class, has far-reaching consequences, including a decline in middle-class status.

As Jadakiss says, "All that I've been given is this pain that I've been living. They got me in the system. Why they gotta do me like that?" -Let's continue to explore these questions together, seeking a better understanding of the complex world of inflation and its effects on our lives.

Russia Decides to Bring the Petro-Punishment of the West (@RealJohnGaltFla, MacroEdge Contributor)

The current state of oil prices should be enough to catch everyone’s attention in Europe and the United States, but unfortunately, the traders still do not think the OPEC+Russia cartel is serious about restraining supply to maintain higher price levels.

The charts however say otherwise:

Chart courtesy of Investing.com

If one reviews the chart above, the last time oil broke out like this was into the top of the summer 2022 inflationary rage. Now the media, especially the financial aspects of it, want to create the illusion that this is a regional issue and nothing for the West to worry about.

They should be freaking out however.

After over a year of constant conflict in Ukraine, sanctions against Moscow, and seizure of Russian assets on a global scale, there is still little recognition of the shift happening in global political alignments. The “South” shall rise again is not just an expression from the American civil war, but apparently a reflection of the second and third world nations being held hostage by financiers and political fiefdoms in Europe and North America finally saying enough.

In the past year the world has witnessed the rejection of Francophone colonialism, US hegemony in the Middle East, and skepticism about the actual function of NATO throughout the globe. Now the world is reacting adversely and doing so via the only vessels they have, China, India, and Russia.

The news breaking today from Russia via their national news service TASS is the opening shot:

Oil export duty in Russia to rise by $2.5 starting October 1 to $23.9 per ton

MOSCOW, September 15. /TASS/. Export duty on Russia’s oil will go up by $2.5 to $23.9 per ton starting October 1, 2023, the Finance Ministry reported on Friday. “According to the Russian Finance Ministry’s calculations, export duty on the Russian oil will rise by $2.5 to $23.9 per ton starting October 1, 2023,” according to the ministry’s statement. Currently, the export duty on oil reaches $21.4. The average price of the Urals crude oil amounted to $77.03 per barrel, or $562.3 per ton, in the monitoring period from August 15 to September 14, 2023, according to the ministry. At the same time, the price of North Sea Dated oil for this period was $88.61. Thus by slightly increasing the prices to their favorite customers, which does not include China or India by the way as they have already locked in long term contracts, the inflationary impacts on those European nations still buying Russian products will be felt immediately. The Russo-Ukraine War however provides another indication however that harsher economic measures might be approaching this autumn and winter. From OilPrice.com: Russia is again reviving the possibility that it could ban all crude oil product exports in order to stabilize volatile fuel prices in the country, according to Russia’s TASS new agency said on Friday. Alternatively, Russia could increase its oil product exports duty to $250 per tonne. This duty will be refunded for those companies that meet their quota for supplying fuel to Russia’s domestic market.

A ban on product exports out of Russia—although temporary—would squeeze Europe’s diesel supplies even more. While Europe has banned the importation of Russian-sourced refined products as of February, it merely shifted trade patterns, with Russia increasing its refined products exports by 50% year over year as of the first quarter by increasing shipments to Africa. The news comes even as Gazprom’s Astrakhan gas processing plant resumed gasoline output after maintenance work. Russian Energy Minister Nikolai Shulginov said earlier this week that there were a number of oil refineries that were due to be brought back online after maintenance work—Astrakhan being just one. The end of maintenance work on the refineries could go a long way in easing Russia’s domestic fuel crunch, and could negate the need for a ban on the country’s exports. Russia has been considering a fuel export ban since May in an effort to avert domestic fuel shortages and rein in prices after announcing a halving of subsidies to oil refiners that will start this month in order to keep more money in government coffers to fund its military operation in Ukraine.

The results of such a ban on top of increased duties means that the inflationary tidal wave washing ashore in Europe, Japan, and the United States is not about to abate. Russia and Saudi Arabia are aware of this and will tolerate stagflation in the West as long as capital flows with Asia remain unimpeded by American and British threats of action which will never happen. With this in mind, inflation is about take a leg back up into the higher range that the Fed failed to account for as Brent Crude will remain in a $95-$120 range throughout the winter months. God help everyone however if it breaks out above $120-$125 and heads up towards $150 per bbl as none of the central banks are prepared for this type of economic debacle in the West.

Great perspectives!!

Nice read. Lows not in but I still fuck with it