9/14 Weekly Report: FOMC Week - What's in Store in the US, BoJ Meeting, the 2007 Reminder

In this Weekly Macro Note - we dive in from everything to Sherwin-Williams 401(k) cuts, to the FOMC/BoJ week ahead, critical macro data we're watching, discuss 2007, and much more.

(@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers & Community,

This week, we have a significant set of events with the FOMC/BoJ meetings and rate decisions taking place, and we’ll provide coverage in our next Midweek Macro Note on Wednesday or Thursday. For those that have missed the latest update and some additional macro commentary on the employment market, metals, & more - make sure that you catch the last Redeye Macro Note below:

Did you catch our viral tweet of the week?

An exciting milestone on X reached as we surpassed 50K followers, and turned our attention to the next 450K.

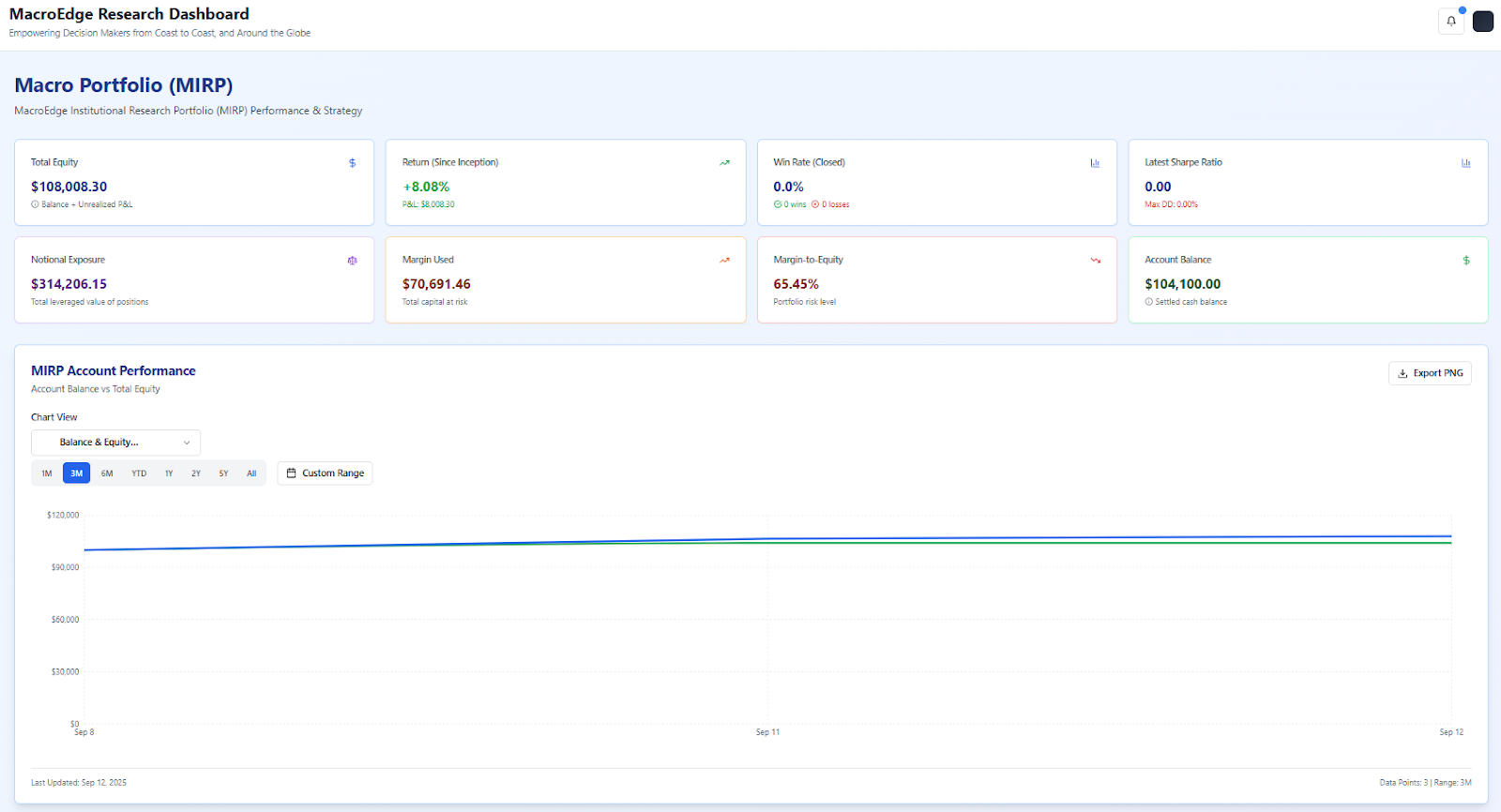

Institutional Research Development Continues

We continue to expedite development of MacroEdge Institutional Research - targeting our 10/1 launch with portfolio tracking, our new dashboard, reports, and more.

Over the next two weeks, we’ll be making all the datasets available in dashboard form, testing the portfolio trackers, and reports will become viewable and sent out through the new interface. Our goal is to design a tool that doesn’t require going anywhere else to view everything you need - from live financial market movement, to our reports, macro data, critical updates, and so much more.

If you missed the September Institutional Report, you can read it below:

And another dashboard preview before we shift into the report…

Weekly Macro Calendar

For earnings - it’s a pretty quiet week, Lennar and Fedex report. Costco is the next megacap on 9/25. For macro - it’s a very busy week.

Not a MacroEdge Ozone member? Get Ozone below with two-week access:

FOMC Meeting - Why it Matters

This week the Fed will decide on a 25 or 50bp cut. While we’re going to treat this like another Superbowl and everyone is going to get so, so excited about whatever happens there’s no signal factor in being part of that crowd. Long story short - if the economy is the strongest it’s ever been - why on earth is the entire fiscal policymaking machine calling for 50bp rate cuts (and on)... the answers are quite obvious, ranging from debt servicing costs on our nearly $40 trillion debt load to the economy is not at all strong, even with continued record deficit spending, the people in Washington have zero plan to get out us out of the situation.

I will note that - and we’ve had this discussion at length in the MacroEdge group internally - that I do think if the 10Y and 30Y begin to advance higher - we start to hear calls for things like YCC and other instruments will be adopted on the monetary side that move us in a more ‘Japan’ style direction as we’ve discussed for the last year.

There has undoubtedly been a cooling employment market but it hasn’t cooled enough to actually take CPI down to the Fed-mandated 2% level which is problematic. With U3 not at 4.5% yet, though it may hit that by spring, this policy action seems rather preemptive, and bond traders may punish us for it. More obvious signals might also be what Powell is paying attention to…

Attempting to print the debt away and tax us through currency devaluation will continue to have long-term implications that we’ll have to assess the size, scale, and magnitude of. Just look at the price of gold, as one example. The whole thing is one giant house of cards, a ponzi scheme per se, waiting for its next can kick until the can eventually finds itself headed over the next cliff before intervention levers are pulled.

BoJ Meeting - Troubles in Japan

If you recall last July - Japan started a global equity and bond market terror that lasted all of about a week before the BoJ stepped in and guaranteed support and liquidity for its markets. Since then, things are a lot different for the Nikkei (which suffered its largest single drop on record that day) though things are also different for the bond market, which has seen yields continue to rise sharply, especially on the long end. Given the comments from Bessent and potential that the tariffs unwind, it begs the question - is there a chance that the BoJ hikes again to attempt to slow inflation? Japan’s fiscal situation is dire, and they can’t really afford to hike, but we’re pegging the odds between 12-15%:

Highlighted the Nikkei bubble in the Friday evening report if you caught that in the Redeye Macro Note. It’s really a global phenomenon, with similar price action in everything from the DAX to the TSX, Nasdaq, and more…

The Jaws of Kyoto Remain Name of the Game

Protection is dirt cheap right now, and we don’t need to overthink the current market structure:

Liquidity is as thin as it gets, and we keep getting bid higher into the stratosphere on expectations that we’re all going to live to 150 and AI is going to work 5 jobs on our behalf while we collect UBI checks (just ask Vlad Tenev - he thinks we’ll all just day trade):

As mentioned previously - if we break to the upside here, I’d imagine it’s going to be coupled with a substantial resurgence in price pressures, though for now, seeing things slowdown and labor continue to cool is the more likely outcome for the time being. We may not see a meaningful downside or a correction until the second cut of this sequence (or if they pause cutting due to inflation concerns after a 50bp cut this week).

Florida Home Price Correction Continues

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.