9/1 Weekly Macro Note: September: Gold Marches On, Macro Week Ahead, Summer Wind Down

In this Weekly Macro Note - we discuss the continued rise of gold and silver prices, talk about the macro weak ahead, including the next NFP report, and the summer wind down. #MacroEdge

(@DonMiami3, MacroEdge Chief Economist)

Good Sunday evening MacroEdge Readers and Community,

As we wind down the long Labor Day weekend (hopefully you had an enjoyable one), we will keep things short tonight. We will cover what to be prepared for in the week ahead from a macro calendar standpoint, reflect on the summer wrap-up as we head into fall, and look ahead to the FOMC rate decision that is just a few weeks away. There is a lot to watch in the data, and we will outline the calendar for the week ahead and more.

On Wednesday we will have the Midweek Macro Note. Friday brings the Redeye Macro Note & Institutional Update. Saturday we will publish the next Institutional Report for September. There is much more in the pipeline. MacroEdge Radio will also resume on Friday, with Calvin joining us from logistics data firm Marhelm.

As Bessent ranted and raved today about everything from tariffs to his own success, we also got confirmation that we will be hearing from the President tomorrow at 2 p.m. EST. The announcement may focus on boosting housing affordability for Americans, with potential executive action noted today by both Pulte and Bessent, and hinted at by the President on Truth Social.

It should be a relatively quiet week until Friday, when we get the next nonfarm payrolls report. On Wednesday we will publish our NFP preview, and later that day recap the August employment data. Meanwhile, we are busy preparing the rollout of the Institutional Portal and Dashboard, another item to watch for Friday.

If you haven’t joined MacroEdge Ozone - you can experience all of our reports, data, dashboard and more for two weeks below:

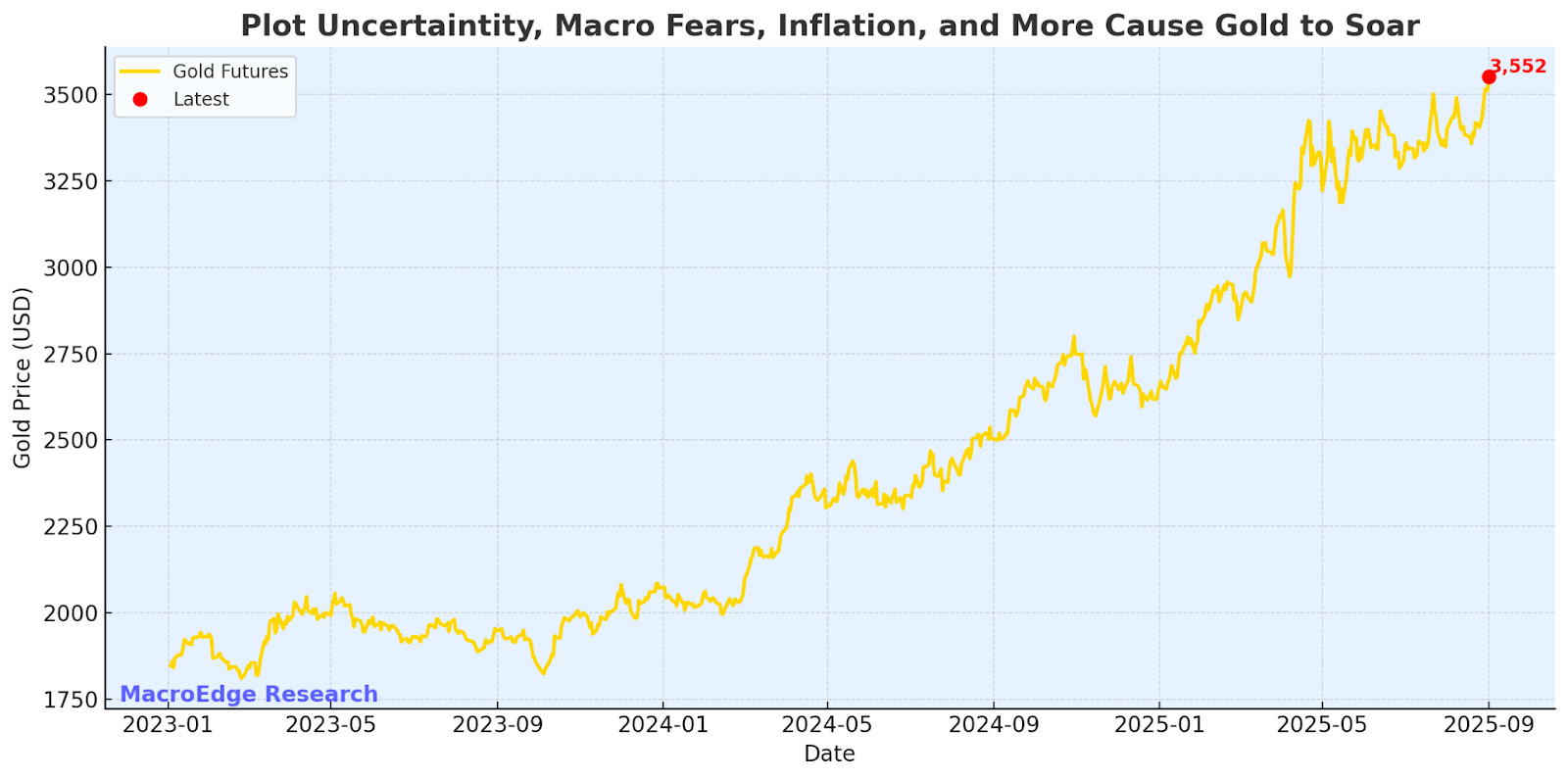

Gold Marches On

Gold continues its march toward the stars with continued inflation, uncertainty, and much more in everything that’s going on right now.

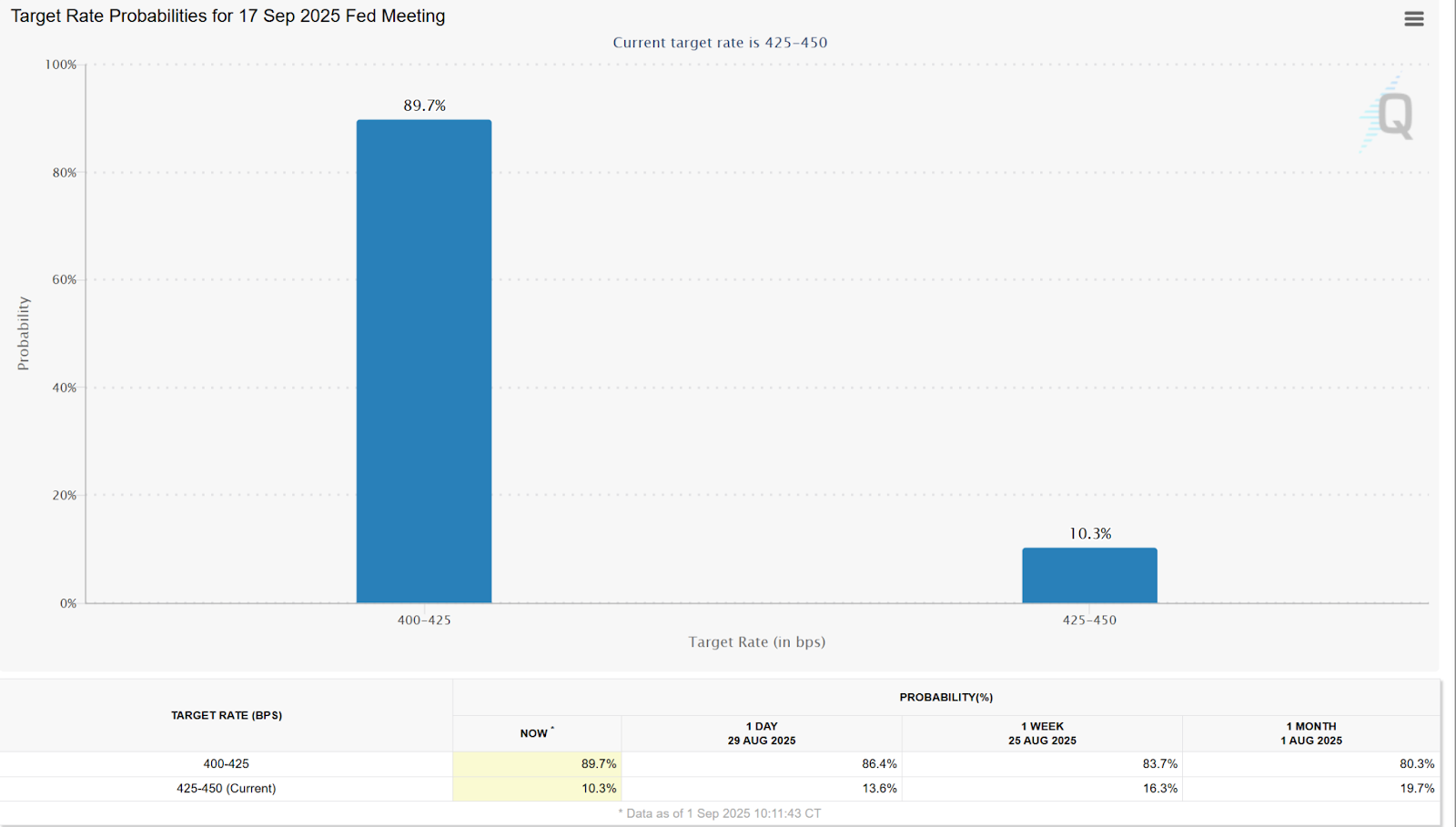

September Rate Cut an Almost Certain Outcome

The September cut is now an almost certain outcome - with odds pegging a 25bp cut near 90%.

Bessent came out today and backed up that idea further - with the possibility that CEA Miran joins the Fed fray through a confirmation before the next FOMC meeting.

Friday NFP Day

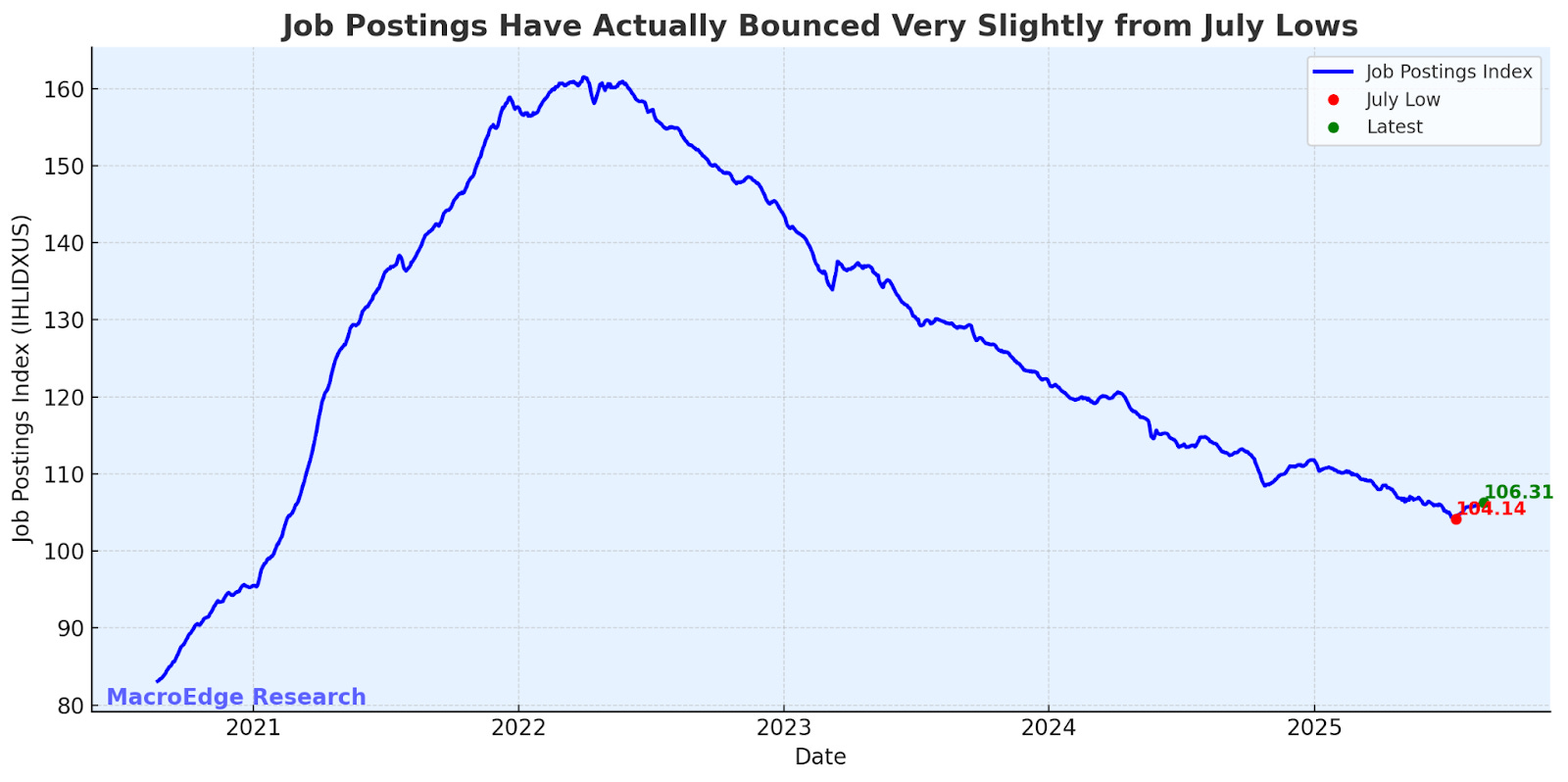

On Friday, we’ll get the first rendition of the August employment data - and we’re heading into another major revision in just a week that may give us an ever broader scope into what the current labor situation really is. The real estate component remains the most important key to any sort of broader slowdown in employment - and we haven’t yet seen that materialize.

Job Postings have rebounded from their July low, per Indeed:

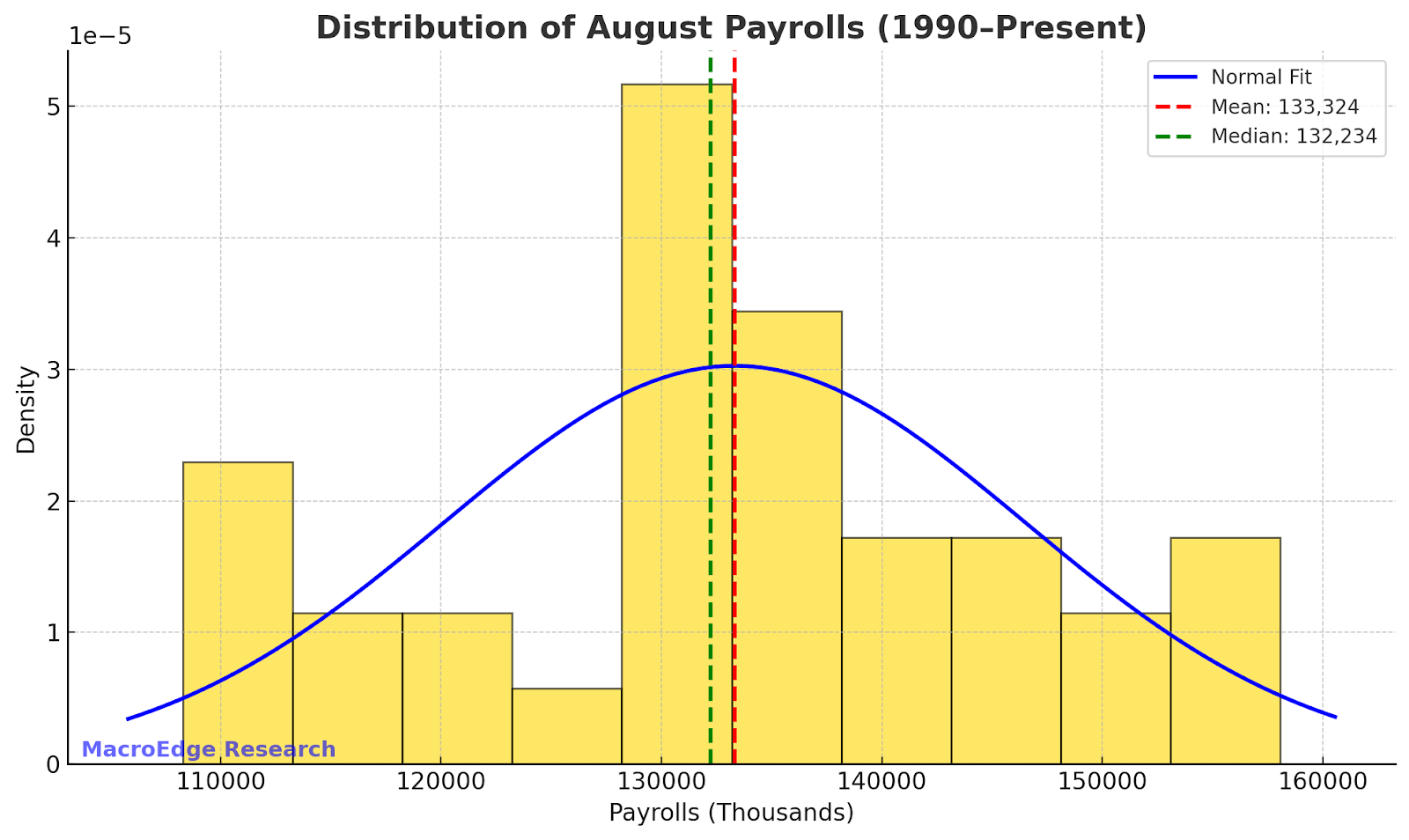

August is usually a month with more tepid job gains:

… although expect the data quality to continue to be complete garbage (will be interesting to see how Antoni alters things going into September)...

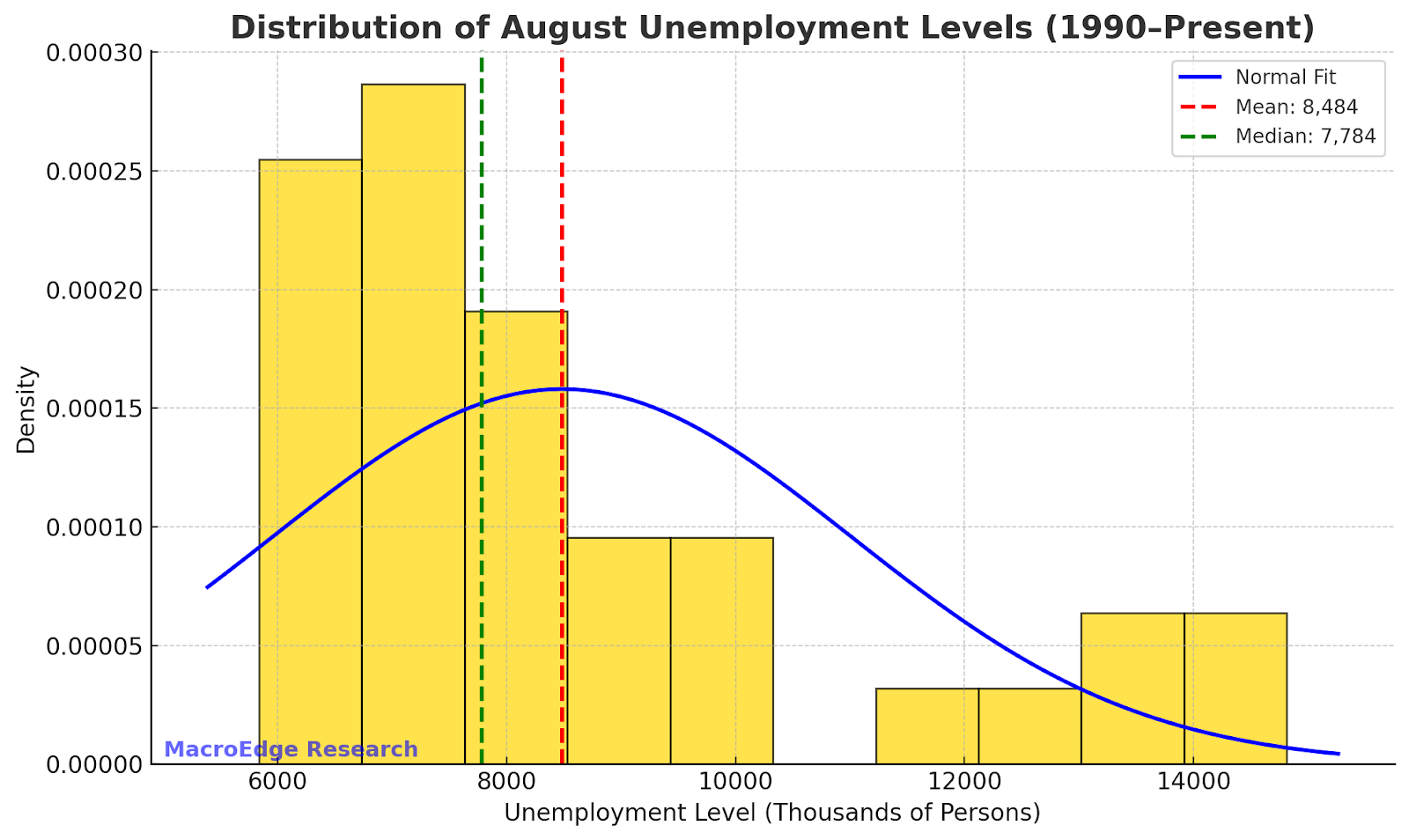

The unemployment level is sitting near a cycle high and likely continues to tick higher:

August unemployment levels since 1990:

Are both inflation and employment becoming problematic? The Fed seems to think so, but places assets and employment first… We’ll have more on Wednesday evening. With delinquency data for consumers near its worst readings ever and things continuing to look soft, it remains a challenging macro picture with a lot of crosscurrents. We’ll discuss more on equity markets on Wednesday… don’t miss it.

Summer is Over, Here Comes the FALL (@RealJohnGaltFla, MacroEdge Contributor)

Traditionally, Labor Day marks the end of the summer for the American public and the beginning of full time work and school for families all across the land. In the worlds of the stock market and economics, it also begins the greatest seasonal period for problems despite those talking heads that believe there will never be another bear market or recession in their lifetimes.

This belief that a “new” way economically has been the hope of every economist and stock market huckster since the inception of the Federal Reserve in 1913 and played upon the emotions of investors every since. In 1964, the New York Times published an article titled (yes, in all caps) “ARE RECESSIONS A THING OF THE PAST?” The money phrase from the story was the opening paragraph where it was stated:

Are recessions necessary?

This question, almost unthinkable five or ten years ago, has become a topic of serious conversation among economists and others as the American economy sets a record with every succeeding month for the duration of a period of peacetime business expansion—with no end in sight.

Emphasis is my own of course because where have we heard that before? The Reagan boom, the 1990’s through the .com bust, the Greenspan Bubble started with the great reflation in 2003, and of course this era where artificial intelligence is going to cure all of mankind’s woes.

Naturally what everyone forgets, as bad memories are something we can not allow during euphoric bull market periods, is that after that June 6, 1964 article, President Johnson bullied the Federal Reserve and then Nixon took over in 1969 to preside over the eventual easy money inflationary period that lasted a decade. That of course stuck President Nixon with a tumultuous economy where equities were in a cyclical bear market from November of 1968 that did not really end until August of 1982.

The 1929 Warning

“Nowadays people know the price of everything, and the value of nothing”

–Oscar Wilde, The Picture of Dorian Gray

In 1929 the market could only go up. The new modern technologies of the era promised a revolution that would forever end the concept of depressions and recessions as the young Federal Reserve and modern economic technocracy envisioned by Hoover and his supporters would never allow such an event to occur again. This author’s favorite stock chart from the era tells the tale of the tape for that time period, RCA:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.