8/6 Weekly Report - Different This Time? Weekly Review, Canadian Housing, a Look at History, and More

Markets in Turmoil, a Look at the Current Cycle, Unemployment inHistory, and Canadian Real Estate Woes. Catch the data dive with insights from top our contributors this week. Is this time different?

8/6 MacroEdge Weekly Release

@DonMiami3, MacroEdge Chief Economist

@SixFinance, MacroEdge Head of Research

@ManyBeenRinsed, MacroEdge Contributor

@GooniStonks, MacroEdge Contributor

@RealJohnGaltFL, MacroEdge Contributor

Weekly Data Dive… Is this time different? (@DonMiami3, Chief Economist)

Super busy past week with the markets - things started to roll over on the equity front even with oil continuing to advance higher and put pressure on the disinflation narrative over the past few months. I still have a very difficult time seeing them no cap the run around $90 with a combination of political actions, SPR releases, or both - although if they do lose control that will likely push CME odds for the Fed to hike way higher than they currently are (odds currently favor this being the terminal rate through the remainder of the year). I personally wouldn’t be surprised if this is the terminal rate although the Fed speak has been purposefully confusing with each Fed member saying something different every day about the next steps for them.

I’m on the road again for a bit so going to keep today short and focus on a few updated index charts that include the new July data from the Fed - regarding employment, GDP growth, and a few others. These will be helpful for us to reference going forward in the future from here on out and these will be accessible on the MacroEdge Ascend website when the design team wraps up the work on that front. Tons of fantastic pieces from our team tonight so I hope you enjoy all of them - and as always, have a fantastic start to your week.

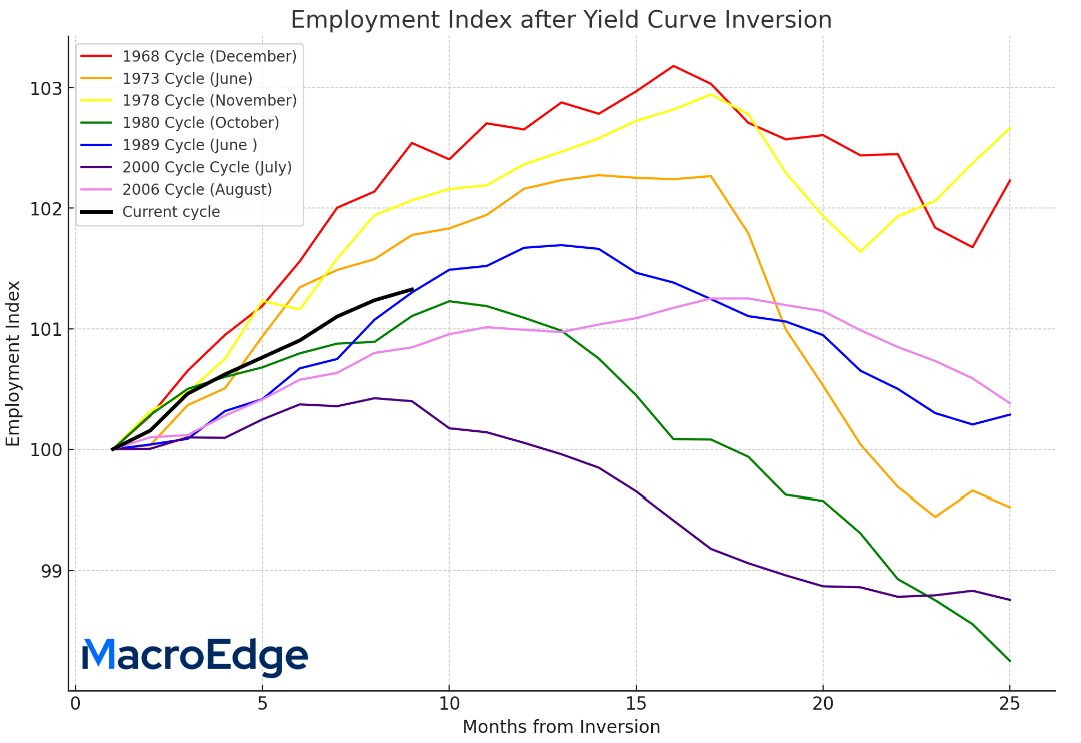

Here is our July update for the employment index - versus the average of all of the previous recession cycles (since 1969):

With the downward revised jobs data again next month - we may be seeing slower job growth than the average of past recessionary cycles (or as I call, late stage cycles) - and employment is always very, very, slow to the party. If we compare our current Employment Index to all previous cycles - this is where we stand:

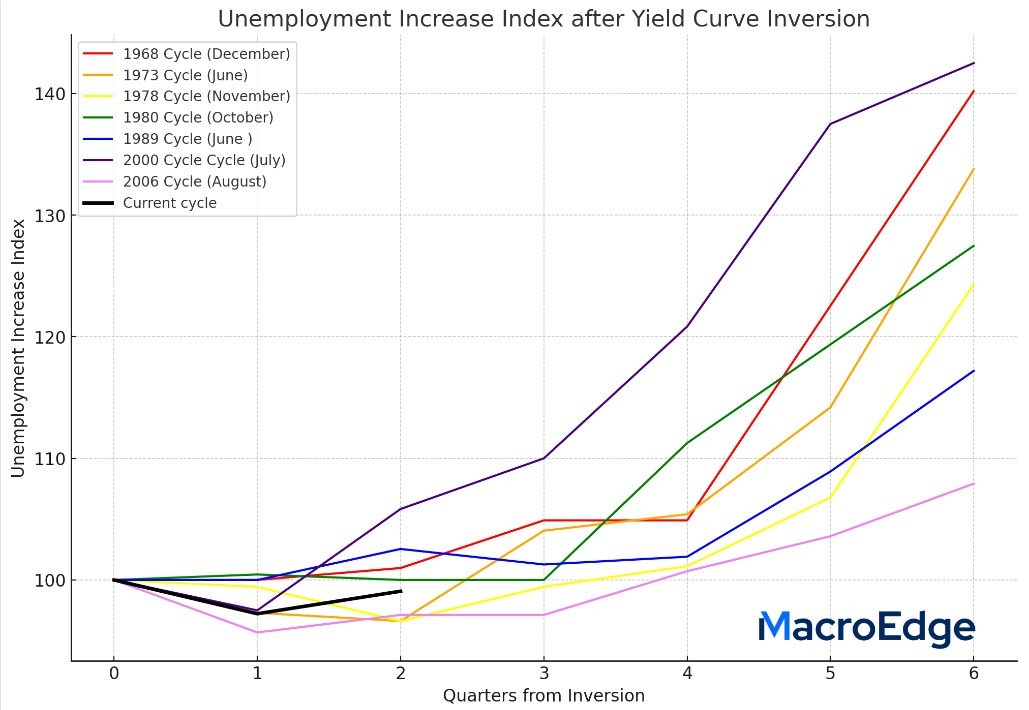

We should expect to begin seeing the unemployment rate tick up during some time during Q4 relative to the baseline unemployment rate established during month zero of inversion - which is something that has occurred in all cycles, including the very slow-moving 2006/07 cycle:

There hasn’t been a hard landing since 1968 that has seen unemployment lower a year (4 quarters) following inversion. 2006 and 1978 were two notable cycles that saw decreases in the baseline unemployment rate all the way until quarter 4 - when they ended up being higher than the baseline. This is something that I am watching carefully as Q3/4 progress.

On the real estate front - I will be focused closely on some of the data coming out this week about housing market activity - a further slowdown in inventory being added onto the market and a continued paralysis that has pushed home buying activity to 2007 levels in many markets.

For now - the music continues to play, but see my comments below on my original recession forecast post for more thoughts as we approach the ‘hard landing window’ - where the probability of a hard landing starting will be highest based on historical data…

Weekly Market Report (@SixFinance, Head of Research)

Rates have exploded higher this week, causing a deep selloff in bonds. /UB futures lost 7 points between Monday and Friday. The 10-year treasury yield moved from just under 4% to 4.2% on Friday before retreating lower on weak USD following nonfarm payrolls. Mortgage rates saw a large increase with Mortgage News Daily reporting the 30-year fixed average at 7.2%. Yields going higher put pressure on every asset class, as 'safe' fixed income treasury assets look to be a safe haven in the intermediate term. The 10-year fell 14.7 basis points on Friday following the weak jobs report. Also, wage growth grew more than expected.

Amazon had an amazing quarter with shares exploding upward after hours, reaching a high of 143 on Friday. Meanwhile, AAPL's third consecutive sales decline has brought its PE multiple into question, sending shares down around 5%. AAPL, known as a leader of equities, gives pause to the near-term market direction. With 3 consecutive quarters of sales declines, AAPL's 30 PE multiple is worth a second look by market participants.

Semiconductor stocks fell flat on their face with QCOM and AMD after experiencing weak earnings given their valuation multiples. The enormous hype around AI fails to materialize into tangible sales outperformance. AMD gained back much of its losses on Friday, however.

Russia's attack on Ukraine's main inland port across the Danube River from Romania on Wednesday sent global food prices higher, ramping up its use of force to prevent Ukraine from exporting grain - Reuters. Not only has Russia withdrawn from the grain deal, but they are also actively suppressing Ukraine's ability to export grains. This could cause increased pressure on food inflation as grain shipments from the 'breadbasket of Europe' become extremely volatile. India also announced considering cutting or abolishing their 40% tax on wheat imports, which led to a 3.5% surge in wheat futures.

Insider selling is starting to increase, with many instances of insiders selling company stock in large chunks. Notably, ABNB founder selling a large portion of his holdings in the company he founded. Whether this trend is merely profit-taking after a terrific performance in the first half of the year by the overall market or indicative of a larger underlying concern regarding future performance remains to be seen. I suspect it is the latter.

US crude stocks fell by 17 million barrels in the week, the largest drop in US crude inventories since 1982, according to the Energy Information Administration on Wednesday. Global oil demand reached a record high in July. Oil prices increasing remain a key risk to the FED's fight against inflation. Oil producers maintain their production cuts, and OPEC+ announced Friday that they would extend production cuts. Crude futures closed out the week at 82.64, a 308 basis point gain across the past 5 days. A Ukrainian drone strike hit a Russian tanker filled with fuel for the second time in 24 hours late Friday night, adding to global fuel risk.

JP Morgan has pivoted on their recession call, with now all of the large banks predicting no recession. We think that is very premature given the Probit model giving a greater than 80% chance we see a recession by May 2024. Our internal models (more on this from Don) suggest the recession chance to be even higher looking ahead the next few quarters.

NVDA will report its earnings on August 22nd with an expected EPS of 2.07. The way the market digests Nvidia earnings will be very telling about the near and medium-term equities forecast, in my opinion. As previously touched on, NVDA ignited the torch of AI that spurred much of this YTD rally in equities. (NVDA -442 bps past 5 days)

SPX gained early Friday only to give back all its gains and then some, declining roughly 62 points in the final 3 hours of trading. SPX declined over 100 points from the start of the week and closed right around the lows. This does not look like a dip I would personally buy, especially with AAPL weakness. However, if the 10-year yield can retreat below 4%, that would change my viewpoint. I do not believe it is time for the long bonds trade yet, other than potentially a short-term mean reversion to the upside, until unemployment rates begin to meaningfully increase.

The percentage of workers leaving their employer in the United States fell to 2.4% in July from 2.6% in the previous month, the Bureau of Labor Statistics said on Aug. 1. The so-called quit rate in the finance and insurance sector dropped to 1.1%, well below a peak of 2.4% in April 2022 - Reuters. We see that what has been called 'The Great Resignation' has begun to move the other way, with increasing instances of employee attrition decreasing. Wells Fargo and State Street have both reported slower-than-expected attrition, perhaps signaling increased employee hesitance in joining the job market. This has caused increased severance costs between the two firms, a trend that could become prevalent on a larger scale in the job market.

Lastly, FED speakers this week by and large inadvertently signaled that a FED pause was likely in the cards going forward, with the final FED hike already having taken place. Oil and Commodities remain a must-watch for me moving forward to determine if the tightening cycle in Fed Funds has already reached its zenith.

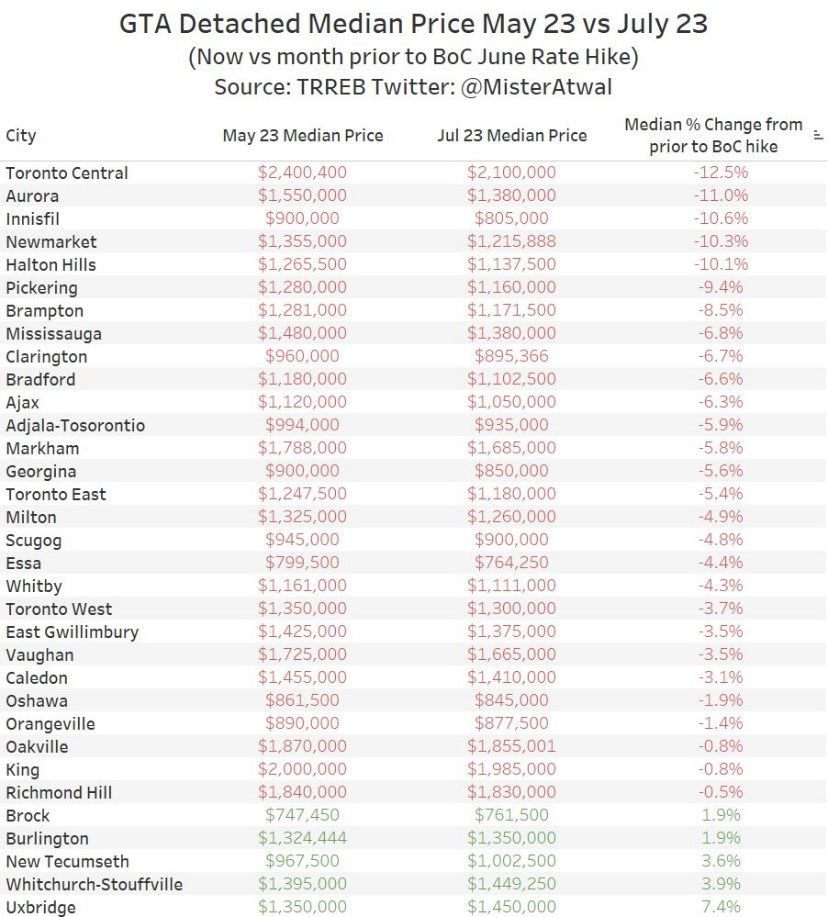

Canadian Real Estate: Dead Cat Bounce? (@ManyBeenRinsed, MacroEdge Contributor)

Canadian real estate has been an enigma for the last 18 months or so.

Canada experienced a dead cat bounce in housing prices in the first half of 2023. Many believed it was the bottom due to the real estate industry's messaging. See attached chart.

Within the last 60 days, many places erased all gains from H1 2023. Bidding wars and open house line-ups have disappeared, creating a stark contrast from earlier this year. An interesting winter awaits.

*GTA means Greater Toronto Area

Housing ministers across Canada are trying to restrict Air BnB and short-term rentals, citing supply issues and the need to control immigration. Some still believe there's no ceiling to rental prices in the country. Hoarding properties for financial gain will likely face government intervention. B.C. housing minister states, "There's too much of our housing stock being used as short-term rentals, instead of supporting residents of B.C." Nova Scotia's housing minister points out "130K vacant bedrooms across the province that could be used on a short-term basis for people looking for a place to live."

The housing crisis in Canada is not solely due to mass immigration, but a culmination of factors, including investors holding onto multiple properties and squeezing people financially.

Last year, Canadian banks extended amortizations for many, resulting in interest-only mortgage payments without reducing the principal. It's a recipe for disaster. The "renewal crisis" has been a concern since last year, with everyday renewals at higher rates. I spoke to someone who renewed from 1.9% to 6.1% on an 850K mortgage. Do the math; it's not pretty.

Unemployment in Canada is increasing, with 69K jobs lost last month. Bell and Telus, major telecom companies in Canada, have been laying off thousands of staff, including in the banking sector, throughout the year.

Heading directly into a recession seems undeniable. IT contractors struggle to get renewals, and hundreds of international students are seeking jobs nationwide to support high living costs. It's a recipe for disaster.

See: Large Job Line for McDonald’s Jobs as Immigrants Face Potential Job Shortage

Seems like everyone is now on the bandwagon that oil prices will surge, and inflation will come roaring back, aligning with my thesis since late 2022. I believe the next few CPI prints will be inflated, leading to potential BoC and FED hikes in September.

Data is king. Let's see how it goes.

The Market Pause… Charts and More (@GooniStonks, MacroEdge Contributor)

With a well-defined market pause over the last several weeks, we are left wondering what else is in store heading into the more seasonally weak periods of the year. Sectors like semiconductors tracked by the $SMH have found some resistance back at their 2021 highs. Here we see a potential double top in price and momentum around this $160 level. Semis have been riding the AI wave in 2023 and have been almost immune to market weakness until the last several weeks. But their relative underperformance in the last few months has been noted.

The $SMH relative to the $SPY, ALSO has made a double top dating all the way back to the Dot Com bubble. This alongside a roll over in strength could show a sign investor are cautious on the more outperformance of the $SMH, which has already doubled from the October 2022 lows.

The Average Stock

Relative stock performance is a significant indicator of market and economic strength. If the average stock is making new lows while a handful of large stocks continue large gains, you could infer that the biggest and largest stocks are thriving while the rest of the economy is struggling to keep up.

This is tracked in indexes like the Russell 2000, or more reflectively, in the $RSP. The $RSP is an index tracking S&P 500 stocks, as if they all have the exact same weighting. The $RSP peaked at the beginning of February, while the $SPX has made new YTD highs in the last few weeks.

It’s possible we are in some type of consolidation period like 2019, where the average stock underperformed the heaviest-weighted large-cap stocks for over a year. After the March 2020 crash, we quickly found ourselves right back in the consolidation zone before breaking out of the 2-year range at the end of 2020 and the real market gains took place.

With the YTD gains being so heavily influenced by the largest stocks, it would be great to see outperformance in the average stock relative to the heaviest-weighted stocks in the back half of the year indicating more broadening out-of-market performance.

*Any analysis/research is not financial or investment advice.

The Pre-Recession Unemployment Myth (@RealJohnGaltFL, MacroEdge Contributor)

The usual suspects are out touting their book as the “there can not be a recession when the economy is this strong” parade continues on the various Bubblevision programs.

Everyone who is considered by the used car sales stock media as a “serious economist” would never say that unemployment is about to super spike to massively higher levels as the US economy implodes into a recession. The reality is that every time the US has had a major recession, and we’ll leave the pandemic out of this discussion, unemployment spikes rapidly just before or after the recession has already started.

Let’s start this discussion with a review of the last three “big ones” after 1987 and how the unemployment data, not including the more accurate U-6 really panned out.

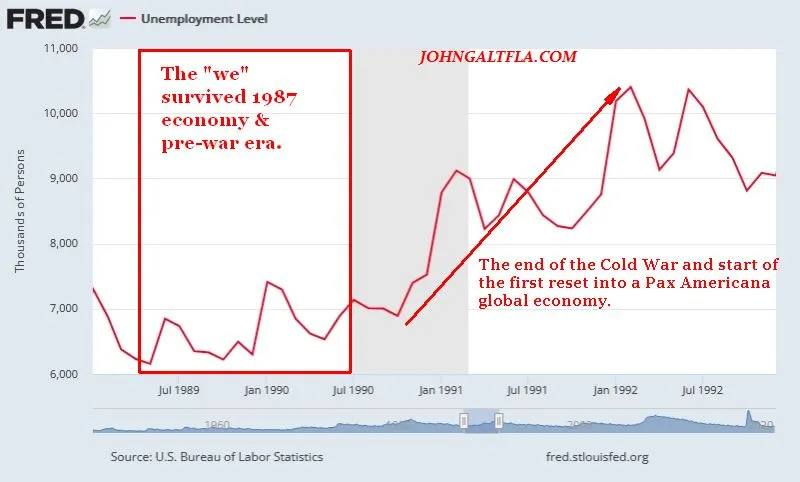

First in 1989, the post-crash economy which stumbled after the October 87′ debacle grew as Reagan’s policies were continued under President George H.W. Bush. The Cold War was ending and the future never looked brighter until the Iraqis decided to invade Kuwait creating a situation that caused a short-term spike in economic activity followed by the inevitable recession.

The U-3 unemployment rate followed in lockstep.

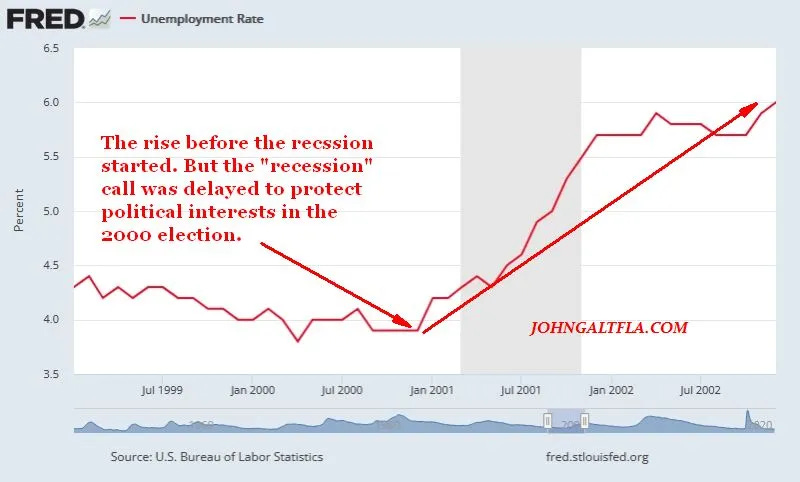

In 1999-2002, the recession was postponed due to political reasons. This time the BEA didn’t want to make the hard call in mid-2000 so as not to influence the Presidential election. In reality, the US economy had contracted severely in every metric except employment levels by June of 2000 and that data was suspect considering how ruthless the Clinton regime was regarding protecting its perfect economic record since 1992.

The shadow recession almost got Al Gore elected. Thankfully it did not. Unfortunately, the GOP alternative was not much better and unemployment spiked with the blame put on 9/11 even though the acceleration in layoffs started long before the attack.

Lastly the “Great Recession” which was an actual depression for 20-30% of the American population. The devastation wrought by years of Federal Reserve mismanagement and lack of oversight along with political incompetence lead to one of the most fearsome crashes in American history. Unemployment started to rise rapidly, especially for the much larger contractor grouping working within the “new” economy, in early 2007. The hard layoffs hit towards Christmas of that year causing massive concern despite denials by many on television and the political world.

The real unemployment rate, as measured using 1980’s comparable metrics was closer to 17-19% at the peak, if not worse as the BLS continued to churn absurd revisions out on a monthly basis. For this current era, keep in mind that inflation is not over, the recession may be starting any week now, and the layoffs reported thus far are just the tip of the iceberg. This could be the big, nasty reset in American financial markets which has been postponed twice in the last twenty years or just another excuse for government largess to pacify the masses. Regardless, by the time unemployment levels and rates catch up to economic reality, the markets will be the last entity to recognize the problem and set pricing accordingly; especially during an election year.