8/20 Midweek Macro Note: What the Zuck? AI Bubble Tremors, Jackson Hole, Jaws of Kyoto, & a September Rate Cut, AlphaSights Team Note

In this Midweek Macro Note - the team discusses the latest in AI bubble tremors with the Meta AI hiring announcement, out of control retail speculation & gambling, September rate cut odds, and more.

(@DonMiami3, MacroEdge Chief Economist)

Good Wednesday evening MacroEdge Readers and Community,

In this edition of the Midweek Macro Note we’ve got some interesting developments on the AI front again, with the new news dropping of Meta freezing hiring and inter-company transfers of AI resources. This adds to the laundry list of items over the last week that we can classify under the ‘AI Bubble Tremors’ label as the math continues to not pencil on data center infrastructure, and even more so on unprofitable LLMs that essentially utilize data centers as their landfills.

The whole thing right now seems a little too good to be true (it is), and unfortunately for those thinking AI & LLMs are going to mean UBI utopia a year or two for now, odds are given the labor market and employment conditions, one is better off honing their craft and focusing on getting better at what they’re good at - or exploring opportunities in other arenas. With over 500 AI unicorns with valuations of $1bn or more - that’s a whole lot of capital that needs to be churn and burned through from a liquidity standpoint for those painful red flags to start appearing… but the signals are certainly here, there, and everywhere.

We’ll also discuss Jackson Hole, the ‘Jaws of Kyoto’, a September rate cut and more below.

Don’t forget to find the latest on MacroEdge AlphaSights below, including in accessing the first report (AlphaSights #1 - August), and how AlphaSights is going to transform how institutional investors access and implement critical MacroEdge data and insights into their decision-making processes.

MacroEdge Ozone is leading the charge of intelligence investing and research in a complex world, at times rowing against the mainstream, we’re providing insights & financial research that matter around the clock. Access Ozone for 7 days below and experience why Ozone has joined the toolbelt of thousands of individuals and firms around the globe.

What the Zuck? Meta Slams the Brakes on AI Bubble Hiring

We broke the WSJ story this evening that Meta announced a full hiring freeze for its AI division - which was offering upwards of $250mm a year for particular resources and researchers. Three weeks ago they told Wall Street that 2026 expenses would surge because of technical talent and a full year of AI comp. Now the brakes are on. That is not choreography.

We have seen this before. The metaverse burned billions and delivered little leverage or value to the addictive social media platform enterprise. This time the bubble is bigger and wrapped in federal colors, with Washington elevating AI to national project status.

Should we take this as an instant catalyst for the bubble to start unwinding? Absolutely not. But it’s one signal of many that we should put in our notebook, and quickly.

AI Bubble Tremors: China, Meta, Altman, Stargate, and More

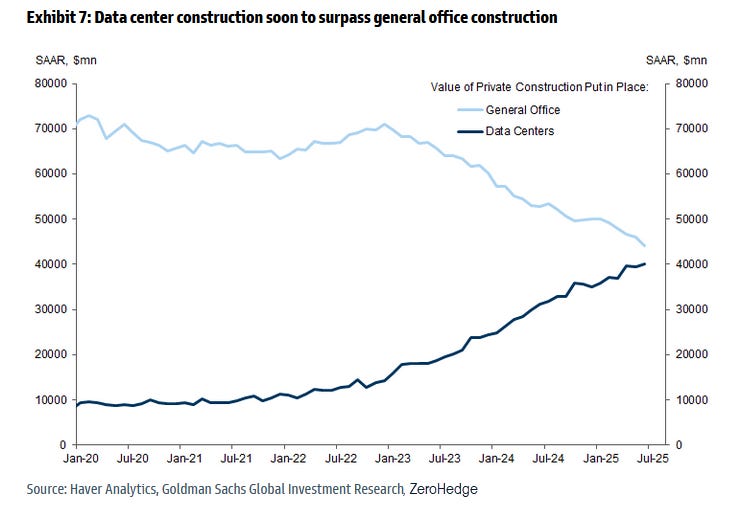

The AI bubble is seeing tremors, though we do note that this Administration - which has put its backing behind everything from an intervention standpoint - including attempting to nationalize minority ownership in private companies like Intel - will not back down easily from signs of trouble in their shiny object industries. The data center boom actually outweighed GDP contribution to consumer spending through the 1H of this year, and if it’s not near a peak (which we are increasingly thinking it’s moving towards peak levels,

Jaws of Kyoto

I’m getting some flashbacks to February with where we’re at with market concentration, retail optimism, valuation risks, internals weakening… and more - which is why our tone hasn’t shifted much even in the face of all this AI driven noise, now I present one of the most important charts from a technical standpoint, for the remainder of the year, and likely into 2026:

This Administration is likely to bring its biggest cannons to the table to defend the last 4 months of complete insanity - but without promises of YCC/NIRP/etc, for now - it’s likely that we need to work through some churn and burn through excess retail liquidity while distributive patterns take place. Risks are mounting, and rewards (the kind that we excel at) are appearing in the horizon, and that means opportunity is around the corner on the left tail side of the equation.

Notice that collapsing volume all the way up the ‘TACO’ rally? Yeah, us too. More to come on Friday evening as we likely see some wind in the sails briefly enter back into the frothy tech/high-beta names that we discuss so often.

McDonald’s Price Cuts

As it says, this was a very interesting piece of news that dropped today. Early signs of ‘high prices being the best cure for high prices’ coming true? Certainly for

September Rate Cut & Jackson Hole

The September rate cut question is one that is outstanding. In the Fed minutes today, respondents noted that inflation remains their top concern, and that risks for inflation are outweighing those presented by the labor market. Additionally, the Trump Administration is taking at aim at additional Fed members and the battle between the two entities continue to heat up. If the labor data comes in warmer than expected for August - I wouldn’t be surprised to see those September cut odds move back towards a coin toss

Powell is likely to stay hawkish at Jackson Hole because the inflation backdrop still has teeth. Food prices are grinding higher (though see signs of the ‘other way’ above with the McDonald’s example, core services remain sticky, and input costs are re-accelerating, which risks pass-through to consumers. Global food and commodity pressures are creeping back, keeping the risk of renewed inflation alive. Oil is the swing factor that can quickly shove headline inflation in the wrong direction. Expect guidance that keeps policy restrictive until disinflation is clear, broad, and durable.

We’re curious that come the Fall, if many people will likely look back at our early-2025 annual equity market forecasts and realize that we might not sound so crazy after all, even in the ‘crazy’ times we’re living in…

MacroEdge AlphaSights Team Note August 21, 2025 (@SixFinance, MacroEdge Head of Research)

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.