7/16 Weekly Report - An Insurance Crisis, "Ice Cream So Good", and Data Deep Dive

This weeks report features several of our great contributors diving into topics ranging from recessions never happening again - to the data that highlights where our economy is at. Enjoy!

If you haven’t yet joined the pre-access list for MacroEdge Ascend, coming late July, you can do so at MacroEdge.net .

Contributors:

@DonMiami3, @MarketMonkPicks, @TexasRunnerDFW, @TrishSunFL, @SixFinance

Weekly Macro Market Update

(@DonMiami3, Chief Economist)

Hope everyone had a great weekend and last week - been traveling and time zone hopping via the skyways and byways. Looking at the week ahead - there’s a few important items to come, notably, an important earnings week but pretty light week in terms of data releases. Standard data releases coming out of the Philly and NY Feds, respectively, as well as jobs data, and NAHB/MBA data). Overall, things continue to remain resilient in the economy, and the outlook remains unchanged from the MacroEdge team on continued further weakness into the 2H of the year with headwinds increasing to the markets and businesses, respectively.

Looking at a few data points put out by our friends at CalculatedRisk - here we have inbound/outbound containers from the Port of LA on a rolling 12-month average (Bill does this in order to eliminate volatility from your standard monthly reports which whipsaw back and forth). When rolled over the 12-month line you get a smoother report highlighting the substantial pullback we’ve seen on both the loaded-in/loaded-out activity in LA - highlighting both less imports and less exports. There’s undoubtedly some effect here from the onshoring of manufacturing - but imports dropping at the sharpest rate in 2007 could mean troubles ahead for things like retailers etc, come later in H2.

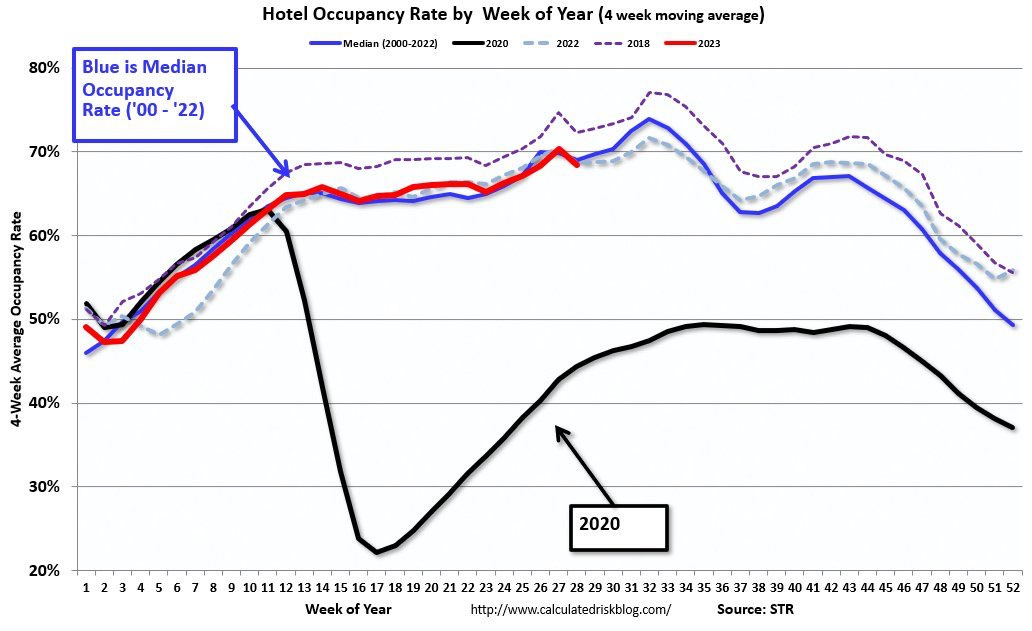

This second chart here from Bill highlights a year/year decrease in hotel occupancy rates - although we just saw a higher week/week increase in gas demand coming off the large print from the July 4th weekend.

Interesting data from FT out of Spain:

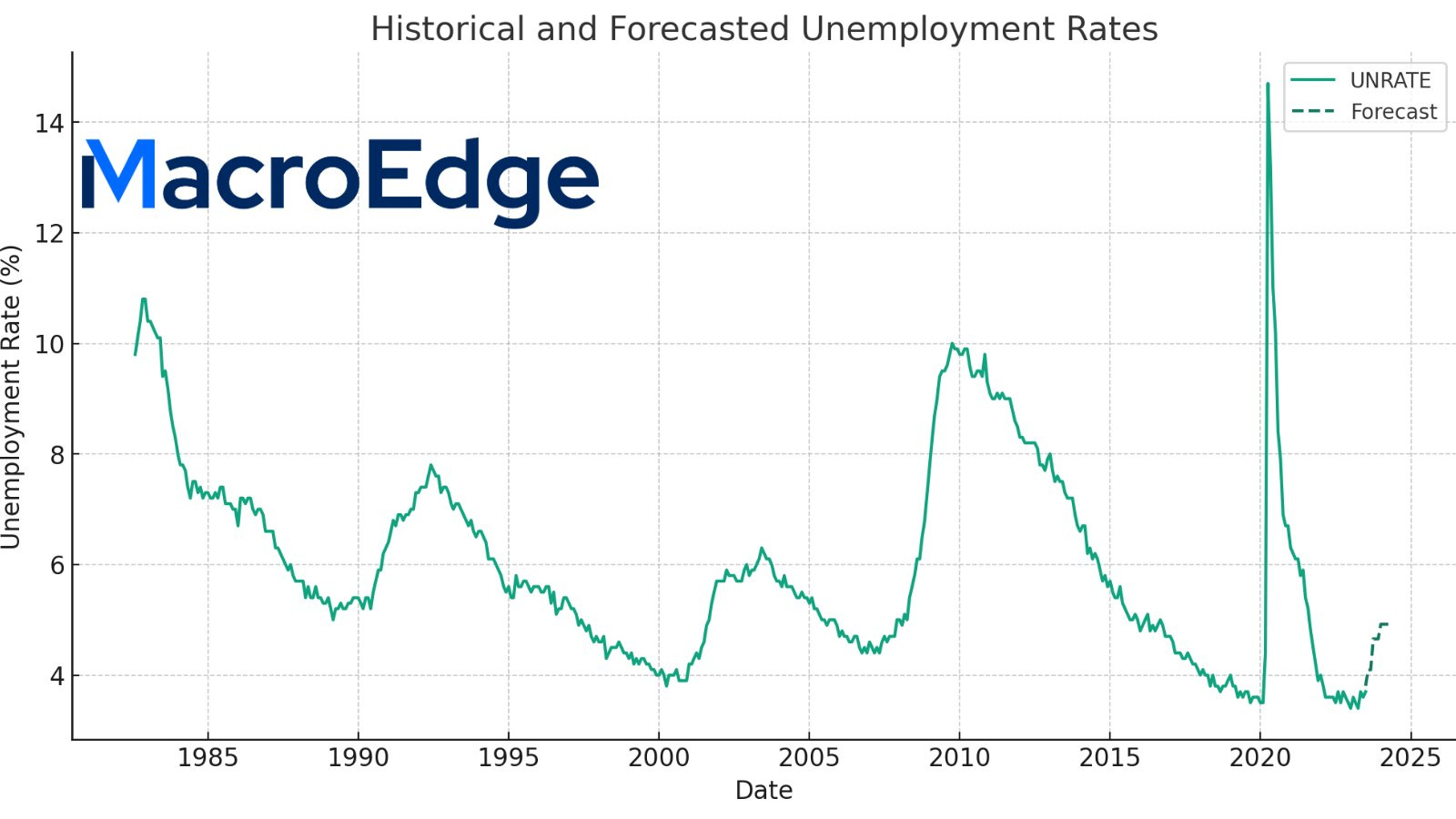

The MacroEdge UNRATE forecast thorough June of 2024 highlights a sharply increasing unemployment rate from current levels up to almost 5% at the end of the second half of next year, highlighting headwinds ahead in the labor markets that are in line with things like sharply decreasing job openings and the Fed continuing its goal of tightening up the labor market dramatically (still their endgame, in our opinion).

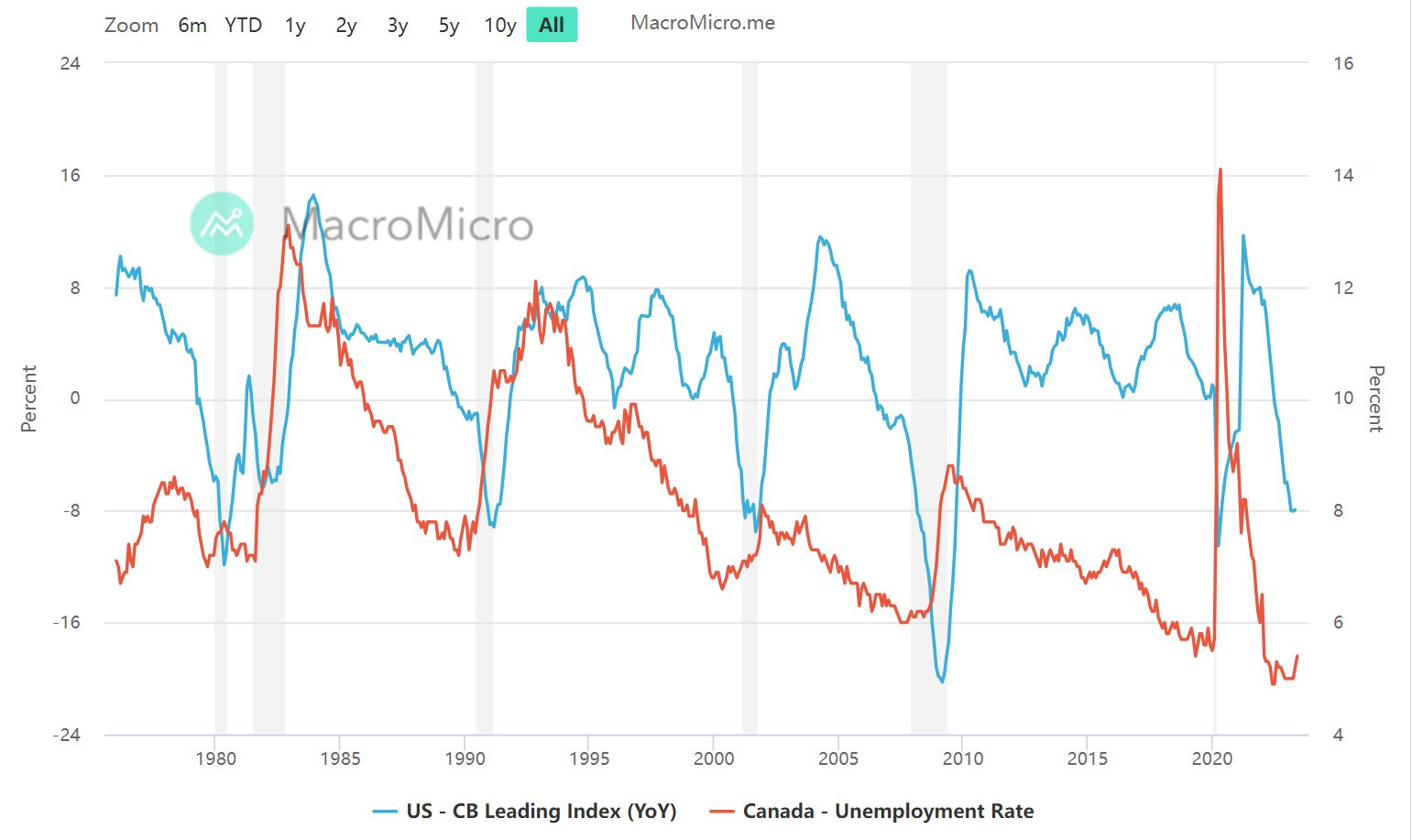

Canada is facing headwinds as well (above) and has seen a larger increase in their unemployment rate already than we’ve seen in the United States. Notice that every time that we see a greater than 8% decrease y/y in the leading index, unemployment rises sharply in Canada - with the smallest example being the increase seen after the tech bubble collapse in the states in 01.

US import and export prices are collapsing which present disinflationary headwinds:

(Export prices)

(Import prices)

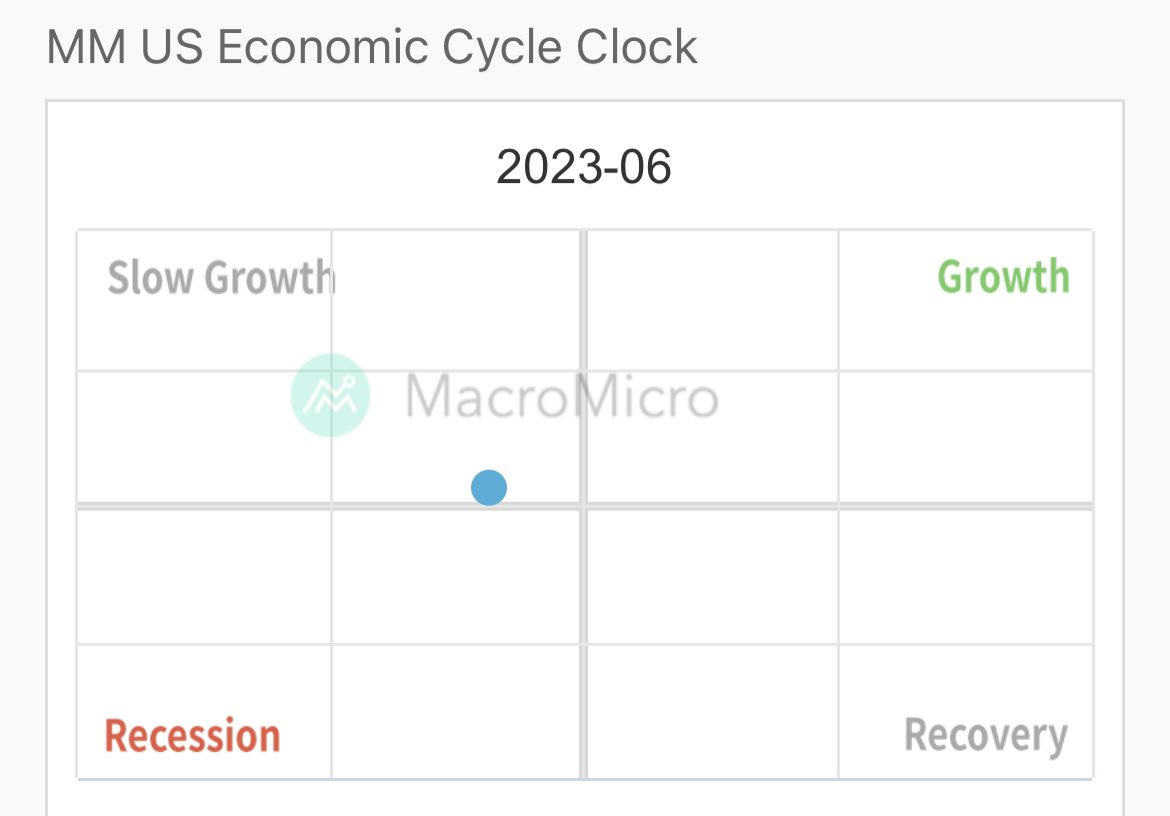

Our partners at MacroMicro’s MM US Economic Cycle Clock continue to move towards “recession” territory with stalling growth and headwinds present in the economy.

In more positive news for the economy - UMich sentiment did bounce quite sharply on lower inflation expectations - although I am expecting this to roll over into 2H as there are two headwinds to have this: #1 inflation comes back or #2 recession risk presents itself sooner then consensus expectations.

If you haven’t joined the pre-access list for MacroEdge Ascend which will be rolled out gradually toward the end of the month by our team - you can go join at the bottom of our new site:

https://www.macroedge.net/

Other than that - Threads usage has already plummeted as expected, and there’s a lot of data and news to go around.

Have a fantastic Sunday evening.

A World Without Recessions “Ice Cream So Good”

(@SixFinance, MacroEdge Head of Research)

This week we saw CPI come in under expectations at a print of 3.0% YoY. Naturally, markets loved the news and a Goldilocks scenario was a foregone conclusion in many market participants' forward projections. The dollar index shown below printed multiple gravestone doji candles on the daily and showed an all-but free fall. Rate cuts are already being priced in, and many expect that July will be the last rate hike, soon to be followed by cuts, and a soft landing/no landing. While CPI headline inflation is in free fall, it is important to know that this inflation number is showing a YoY comparison to the cyclic high of inflation in June 2022. We could very easily see CPI YoY prints creep up again next month and the following month due to the base effect.

Nvidia had a breakout week, exiting the range it had been consolidating in. I believe it important to note that a lot of the explosive movement in equities to the upside has been rooted in NVDA AI craze. We saw NVDA expand by 2 years of revenues on thursday, and then again on friday, before posting a massive intraday reversal to close red. NVDA price action is something to keep a close eye on going forward when monitoring the equities rally.

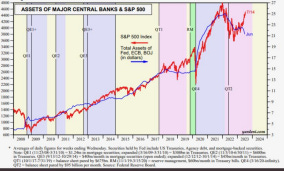

Central bank liquidity and equities are closely linked and this is a widely known phenomenon. What we are seeing today, is central bank liquidity and SPX diverging substantially. This is something that is unlikely to persist, as monetary supply and asset demand cannot diverge markedly for very long.

US Redbook’s sales weighted YoY same store growth posted its’ first YoY decline of this cycle, signifying that we are not out of the woods yet.

Bridgewater co-CIO Bob Prince has said “We’re likely to be stuck around this level of inflation. The big risk right now is that you get a bounce in energy prices when wages are still strong.” This was shown this week as crude oil futures posted large gains before cooling off on friday. With the Strategic Petroleum Reserve over half emptied by the Biden admin and likely no more SPR drain, we could see increasing upside momentum in oil pricing in the near term absent a recession, causing inflation to creep up, providing OPEC production cuts remain in place.

After this recent rally, with projected 2023 SPX operating earnings annual growth forecasted at a consensus -0.1%, I don’t see very much reason to be buying equities at the same valuation we

saw during monstrous QE and abundant liquidity, as well as ZIRP. YoY earnings down as well. With Tech booming, we need to start getting realistic about mania vs reality.

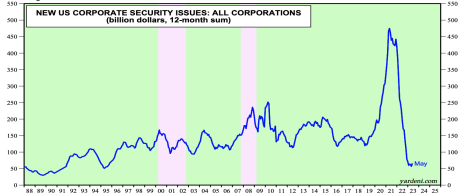

The IPO boom is clearly on pause, absent a few success stories recently. New securities issuance is as the lowest level in decades.

Remember when looking at the dot plot, the FED will not bring down rates significantly unless we have a recession, which will certainly knock equities off their high horse. I would be extremely cautious buying valuation multiples here with macro where it is.

A World Without Recessions “Ice Cream So Good”

(@TexasRunnerDFW, MacroEdge Contributor)

Recently, an academic on Twitter posited, "Recessions are policy errors." In theory, should central bankers and elected officials not be capable of engineering a growing economy with cycles of expansion and contraction, without ever needing to dip into a recession? If only perfect policy were executed, could we live in this recession-free utopia? Yes, in theory. But we don't live in theory. We live in reality. And in our reality, we know with certainty that we don't have a government that always executes good policy, let alone the perfect policy required to achieve such a feat. If erroneous policy is already in place to trigger a boom/bust cycle, then calling for additional policy to avert the bust portion of a cycle isn't preventing a recession; it's suppressing one. Why does this matter?

Well, suppression has consequences. We've seen these consequences repeatedly in the decade since the Great Financial Crisis. Quantitative Easing saved us from a collapse in our banking system and a global pandemic but catapulted us into an era of extreme wealth inequality, unrelenting greed, a rise in populism, and mounting debt. Every day, we discover new permutations of the societal consequences Greenspan's monetary policy experiment has brought upon us. And every day, they get weirder and weirder. Look no further than social media.

But first, let's step back in history for a moment. In ancient Rome, crowds gathered to watch Gladiators battle to death in an arena. At first, the Gladiators were slaves, given no option but to fight. But as time wore on, Roman citizens (usually very poor or outcast from society) volunteered to train and go into battle for the chance to win riches, fame, and glory. This bread and circus spectacle grew in popularity under the reign of Julius Caesar, arguably as a means of distracting the masses from recognizing their diminished autonomy under imperial rule. Perhaps Silicon Valley elites, fueled by ever-cheaper capital, have constructed a modern-day Colosseum in social media. Our modern-day gladiators don't sacrifice their lives for riches, fame, and glory. Instead, they sacrifice their souls.

Boomers argue about politics in a blind rage on Facebook. Women sell their bodies on OnlyFans. Men livestream video games and crash planes on YouTube for likes, clicks, and cash. Over time, the crowds grow numb and restless, looking for a bigger dopamine hit. The gladiators grow more desperate and audacious.

A viral video of a woman on TikTok robotically pretending to be an NPC (non-player character in a video game) is the latest, most disturbing iteration. She immediately followed it up with another video, admonishing her haters. "I'm here in the arena, making money. What are YOU doing?"

We're watching, shaking our heads, wondering what kind of world we're living in. This is a world without recessions. Are you not entertained?

Florida Insurance Crisis - Climate Risk or a Business Cycle Indicator?

(@TrishSunFL, MacroEdge Contributor)

With an increasing number of insurers pulling out of Florida, the crisis that’s unfolding is gaining more attention. And while a shift in narrative attributing the calamity to climate change appears to be taking place due to the impact of one of the most destructive storms in recent years hitting our shorelines, is the real story beginning to be buried under the climate change narrative?

Many articles have been published recently in particular due to the recent announcement of Farmers Insurance and AAA announcing their intent to not renew policies in Florida. In the past year, four insurers have announced their intentions to pull business. According to the Insurance Information Institute, a 40% increase in property insurance rates is expected this year after a 33% increase in 2022. According to Mark Friedlander, the Director of Communications for the Institute, the average Florida homeowner is paying $4,231 for property insurance; nearly triple the national rate of $1,544.

“Floridians pay the highest homeowners insurance premiums in the nation for reasons having little to do with their exposure to hurricanes,” said Sean Kevelighan, CEO, Triple-I. “Floridians are seeing homeowners insurance become costlier and scarcer because for years the state has been the home of too much litigation and too many fraudulent roof replacement schemes. These two factors contributed enormously to the net underwriting losses Florida’s homeowners’ insurers cumulatively incurred between 2016 and 2021.”

According to Friedlander, Florida had 79% of homeowners’ insurance lawsuits while only having 9% of homeowners’ claims indicating legislation, including one-way attorney fees, has been the primary culprit.

In recent years, insurers have been plagued by roofing scams that have been exploited due to loopholes in state law and court decisions that allowed them to proliferate into a cottage industry of door-knockers offering free roof inspections and promises of roof replacements covered by insurance. Homeowners are persuaded to sign an Assignment of Benefits to contractors that then file fraudulent or inflated damage claims. Contractors sue forcing insurers into settlements many times over the original claim, most of which goes to the attorneys in the form of a “contingency fee multiplier.”

And compounding the issue has been rising replacement costs. According to Zillow data, the average home price in Florida in June 2023 is $390,856, up 70% in five years from $229,897 in 2018. Most of the gains occurred between 2020 and 2022, rising 50% from $256,067 in June 2020 to $384,798 leaving many policyholders underinsured and insurers collecting premiums that undervalues the risk of the coverage.

But the problems haven’t been limited to just homeowners. Commercial properties are experiencing the same rate increases including government buildings and schools which results in increased costs which are passed on to property owners via property taxes. The school district of Charlotte County, where the eye of hurricane Ian came in on the mainland, reports their insurance policy rates are increasing by 75%. And while property owners have some protection in the form of increase caps on assessed values, these caps are not on the actual taxes charged leaving the possibility of increased millage rates.

A recent article in the New York Times quotes Trevor Chapman, a spokesperson for Farmers Insurance saying, “This business decision was necessary to effectively manage risk exposure.” Also, it clarifies that Farmers isn’t totally pulling out from Florida but ending its home, auto, and umbrella policy coverage under the Farmers brand.

Despite multiple pieces of legislation being passed since 2021 to combat excessive legislation, insurers are still pulling business which leads to the question, is the litigation costs and climate risk the only reason for these insurers to walk away?

With our memories being short these days, it seems forgotten that Florida went through a similar crisis in the mid-2000s after a similar surge in property values and a series of storms.

According to a New York Times article in June of 2006, Farmers Insurance was asking the Florida Office of Insurance Regulation to increase its homeowners' insurance rates 74 percent on average. The headline from that article read, “Rising Insurance Rates Push Florida Homeowners to Brink.”

In a recent article written in the NY Times, a spokeswoman for the Florida Department of Insurance Regulation was quoted as saying the department received from Farmers was marked as a “trade secret” which should prompt questions as to what was contained in the letter. Was there data or reasons cited that are not being publicly disclosed?

Given the nature of the insurance industry, in which data is collected, analyzed, and future risk is assessed based on actuarial analysis, should we wonder if there is data the private insurers are contemplating may pose an added risk?

With that question in mind and knowing the similar crisis we faced nearly 20 years ago, I looked into insurance issues that plagued the market following the Great Financial Crisis.

In 2010, the Florida Department of Financial Services released a report titled, ‘What is the IMPACT of the Economy on Insurance Fraud and Arson in Florida?’

The report was prepared in response to the National Insurance Crime Bureau reporting an increase in questionable claims that determined their cause was attributed to the economic downturn. The NICB report stated a rise of 27% in suspicious car fires, 77% increase in commercial slip and falls, and a 407% increase in hail damage-related claims.

The NICB was cited as saying, “the poor economy may be driving normally good people to do bad things…” and that, “Hardcore criminals also have more opportunity to entice normally honest people into their fraudulent schemes.”

The Florida report cited Realty Trac ranking Florida second in the nation in the number of foreclosures behind California, another state seeing insurers pulling business. According to the report, foreclosure rates greatly increased the exposure of homeowners’ insurance to fraud. An analysis conducted by the Florida Department of Law Enforcement’s Division of Insurance Fraud stated homeowner claim fraud

referrals (including fictitious claims or damage, fictitious liability claims, and inflated claims) increased 41% between the fiscal year 2008/2009 and fiscal year – 2009/2010.

The Coalition Against Insurance Fraud estimates that on average, fraud occurs in approximately 10% of property and casualty claims. So with talk of a pending recession and the existing risks insurers take given the high rates of property & casualty litigation Florida has already been experiencing, it shouldn’t be unreasonable to question if we may be at a point in the business cycle where insurers are concerned about significant risks far beyond those already known due to hurricanes and are proactively taking measures to reduce those risks.

https://www.iii.org/press-release/triple-i-extreme-fraud-and-litigation-causing-floridas-homeowners insurance-markets-demise-062322

https://www.cbsnews.com/news/aaa-insurance-florida-crisis-farmers/

https://www.nytimes.com/2006/06/29/us/29florida.html

https://www.nytimes.com/2023/07/14/business/farmers-homeowners-insurance-florida.html https://insurancefraud.org/fraud-stats/

https://www.nbcnews.com/news/us-news/roofing-scams-florida-property-insurance-hurricane rcna29649

https://www.myfloridacfo.com/docs-sf/investigative-and-forensic-services-libraries/difs documents/economicimpactreport_3rd_quarter_fy09-10.pdf?sfvrsn=c90dbc23_2