6/25 Weekly Macro Report - HOPE, Fed Pause?, Canadian Housing, ROKU, and more...

A great lineup of contributors this week covering a broad array of topics from Canadian Housing to Michael Kantro's #HOPE framework. Respect the lag and have a great rest of your Sunday evening.

Thanks for reading MacroEdge! Subscribe for free to receive new posts and support our work.

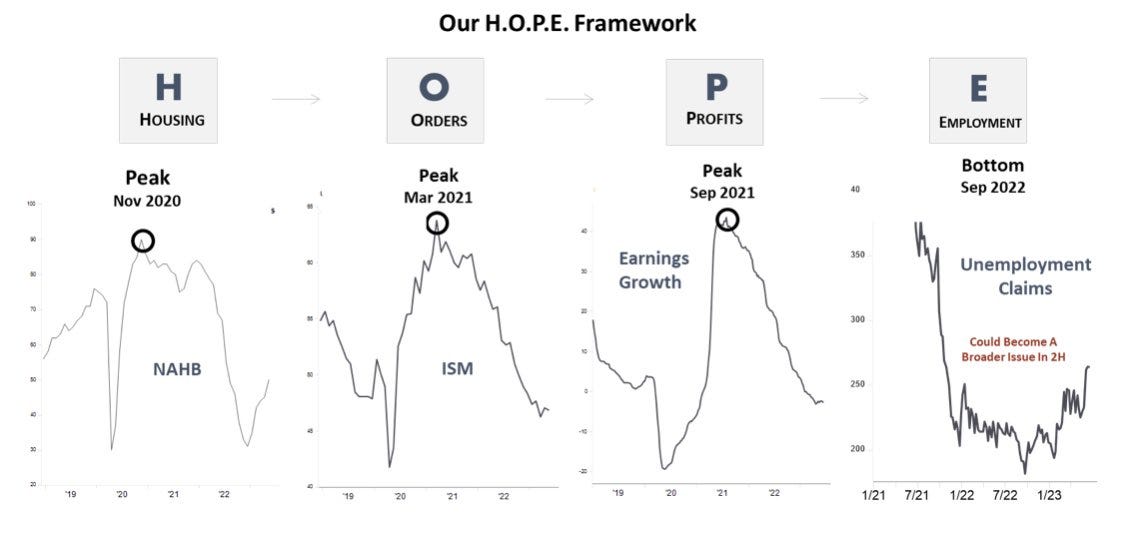

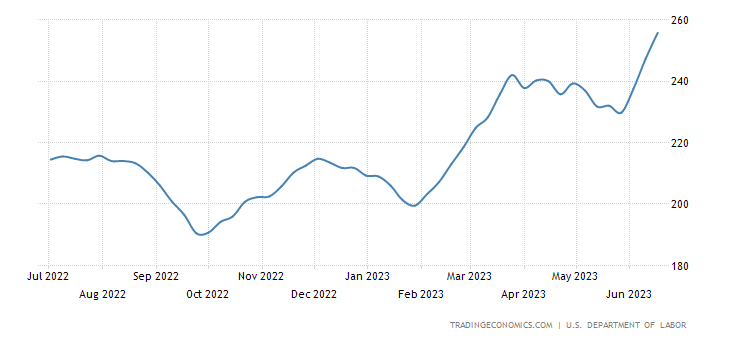

Hopefully everyone had a great weekend! Just providing a quick look at 3 different macro indicators for my short weekly writeup. First at the HOPE framework from Piper Sandler, secondly the 4 week average of jobless claims, and thirdly the S&P Manufacturing PMI.

Thanks for reading MacroEdge! Subscribe for free to receive new posts and support my work.

Michael Kantro's HOPE framework provides a concise assessment of key indicators suggesting an impending recession. Housing, a significant sector in the economy, appears to have reached a bottom, indicating limited room for further expansion. New orders, a crucial metric for economic activity, are weakening, signaling potential declines in business investment and consumer demand. Profits, a fundamental driver of economic growth, are declining, indicating reduced profitability and potential economic headwinds. Finally, the labor market is softening, implying a potential slowdown in job creation and consumer spending. Together, these indicators suggest a cautious outlook for the economy and raise concerns about the possibility of an approaching recession.

The latest data from the U.S. Department of Labor reveals that the 4-week moving average of jobless claims in the United States, a measure that smooths out week-to-week fluctuations, increased to 255.75 thousand in the week ending June 17th. This represents a rise from the revised figure of 247.25 thousand in the previous period, reaching its highest level since November 2021.

Analyzing this data through the lens of labor market dynamics, the upward trend in the 4-week moving average of jobless claims suggests a potential weakening in the labor market. When the number of jobless claims rises, it indicates an increase in the number of individuals filing for unemployment benefits due to job loss or reduced working hours. This trend could imply a higher level of job separations or reduced hiring activity by employers.

A sustained elevation in jobless claims can reflect labor market challenges, such as decreased job opportunities, economic uncertainty, or shifts in industry conditions. As the 4-week moving average accounts for short-term fluctuations, its rise indicates a more prolonged pattern rather than isolated weekly variations. The fact that it has reached the highest level since November 2021 further emphasizes the significance of this development.

A weakening labor market can have broader implications for the overall economy, including reduced consumer spending, lower business confidence, and potentially slower economic growth. Policymakers, economists, and market participants closely monitor jobless claims data as an important indicator of labor market health and economic vitality.

The S&P Global US Manufacturing PMI for June 2023 registered a decline to 46.3, indicating the most significant contraction in the manufacturing sector since December. This figure contrasts with May's reading of 48.4 and fell short of the forecasted 48.5, as per preliminary estimates from Markit Economics. New orders experienced the most substantial decline since December, driven by weak demand resulting from muted customer confidence, while foreign demand remained subdued. Furthermore, input buying contracted at the sharpest rate since January, and both pre- and post-production inventories saw sharp declines. Regarding prices, cost pressures continued to diminish, as suppliers aimed to bolster sales by offering reduced prices. Input prices recorded the most significant decline since May 2020, and selling price inflation was the slowest in the current inflation sequence. Meanwhile, improved success in finding suitable candidates enabled firms to expand their workforce. Overall, the level of optimism was the weakest observed in 2023 thus far, primarily influenced by customer hesitancy and concerns over inflation.

Why did the Fed Pause? (@TexasRunnerDFW)

Jerome Powell spoke this past week and unequivocally signaled further rate hikes this year. The economic data hasn’t changed much since the June FOMC meeting, so it begs the question, why did the Fed pause? This has been the fastest, steepest rate hike cycle in US history. Powell, it would seem, has been on a hell-bent mission to slay inflation, bringing it back down to his oft-repeated 2% target.

But is that really his primary objective?

Because if it is—why pause when inflation is still clearly running above that 2% target and signal intent to hike again in the future? At the June FOMC press conference, his answer to a similar question posed by Nick Timiraos of The Wall Street Journal was ambiguous at best. Powell opened with a Freudian slip, using the word, “skip” and quickly walked it back.

We all heard it. This was an intentional skip, but the Fed clearly doesn’t want it to look like one. They want it to look like they’re taking things in stride and strictly going off the economic data. I think I have an idea as to why.

Inflation is a huge problem that the Federal Reserve has been tasked with tackling. But (and Powell alluded to this) Central Banks don’t have sole control over inflationary pressures. Congress and the Treasury Secretary are partners in this inflationary dance, and they haven’t exactly been following Powell’s lead. In other words, in the face of unchecked spending and debt ceiling policy by the government, there’s only so much the Federal Reserve can do to combat inflation.

So, what else can the Fed do? In addition to fighting inflation, the Fed needs to look out for its own best interests. And as of mid-2022, it had two major

problems beyond inflation:

1. A credibility problem

2. An impotent tool (QE)

The latter is the Fed’s biggest problem, and one Michael Burry highlighted in a now-deleted tweet from April 2022. Given our massive unsustainable debt burden, the absolute worst-case scenario for the Federal Reserve would be to find ourselves in a new financial crisis (war, systemic bank failures, another pandemic…etc) while

we’re already at zero rates. Effectively, it renders them helpless to respond.

This is why Powell hiked so swiftly and aggressively. It was imperative for him to get the Fed Funds rate above 5% as fast as possible, BEFORE SOMETHING COULD BREAK. Because the Fed needs to have a funds rate that is high enough to cut from should they need to (and we all know that they will).

Luck, it seems, was in the Fed’s corner for once. Powell has been threading the needle like a master seamstress, rapidly bringing the Fed Funds rate above 5% with only minor breakage in the system (regional bank failures, some distress in CRE). This gives him an opportunity to tackle the other major problem facing the Fed: Credibility.

Frankly, the markets completely ignore forward guidance. They’ve been catered to before and now, their current valuations dependent on QE and ZIRP, expect a pivot. To the markets, a pause means a pivot. What better way to break the market’s entitled expectation of this than to skip a rate hike? The market will run bullish off the skip, interpreting the pause as the end of the hike cycle. But if the Fed comes in and hikes again in July, the Fed throws the market off balance and claims some of its power back.

This, I believe, is why the Fed paused, then immediately turned around and signaled more hikes. There is a power game between the markets and the Fed, and Powell is tired of losing. If nothing breaks first, I expect the Fed to hike again in July. Powell knows that the markets don’t believe him. And really, after 2018, why should they? What better way for the Fed Chair who cried Wolf to restore credibility than to

Canadian Housing Update (@ManyBeenRinsed)

Seems like the recent bounce in Canadian housing has reached its end. There are no longer long queues at open houses or stories of offers well above asking price. The recent 25bps rate increase by the Bank of Canada has significantly cooled the market. Another rate hike is expected on July 12th, making this summer an interesting one for the country.

To provide some context on the situation in Canada, consider an example: A $1M house with an $800K mortgage, a $200K down payment, and a 30-year amortization. The monthly payment amounts to nearly $6K. Over the course of 5 years, the mortgage interest accumulates to $250K, with $50K going towards the principal.

In Canada, some single mothers who earn six figures have faced challenges obtaining mortgages and have been forced to refinance with their ex-husbands. The situation is dire, and many are hopeful for rate cuts, which has been the prevailing sentiment over the past year. The housing market is on the verge of a potential collapse.

Cities like Vancouver have proposed 9% annual property tax increases for the next 5 years, while Toronto has promised tax hikes. Areas around Toronto, such as Mississauga, have already reported property tax increases of $500+ annually. Certain areas are experiencing a surge in inventory, leading to longer market durations. The 5-year Canadian bond yield has risen significantly in recent weeks, resulting in mortgage rates exceeding 6%.

All these factors are aligning for a memorable Canadian summer in the housing market.

Roku and the Prospects for Recovery (@MarketMonkPicks)

With $QQQ and $SPY trading within 10-15% of all-time highs, much has been written about market breadth. Seven major tech stocks, dubbed “the Magnificent Seven” by Bank of America have driven the majority of the S&P 500’s gains this year: $AAPL, $MSFT, $GOOG, $META, $AMZN, $TSLA, and $NVDA. This is a well known market narrative and I won’t rehearse it here (see Baccardax, 2023). While catchy, I do wonder if the person who coined the name realizes the implications of that film reference. In the film, a Mexican village is being terrorized by the bandit and his gang. In desperation, several of the villagers travel to a Texas border town in hopes of hiring gunslingers to rid them of Calvera. Unable to offer much money, they hire a motley team of seven gunfighters, only three of which survive the final battle (Pfeiffer, 2023).

I am sure plenty of people on twitter can offer you perspective on which stocks will live and die to close the year, but that’s not my objective here. I’m more interested in the minor characters. Much of the historic Covid rally was driven by high P/E growth communication stocks that retraced sharply to the downside for over a year. $ROKU stands out in that story. Always more of a little brother in the streaming space, it took the fall with $NFLX without seeing as much of the recovery. Roku also makes hardware, which has weighed them down significantly at times. $ROKU hit an ATH of $490.76 in July 2021 before a steep and steady drop under $40 to close 2022. Currently trading at 62.57, $ROKU has rallied impressively on the year up over 50% YTD.

Insiders, Institutions and fundamentals

When assessing a stock, I primarily assess technical analysis at what I see as some key levels on the chart and options activity. Other areas to consider are insider and institutional ownership, along with their fundamentals. Insider ownership pains a bleak picture. No one is buying: “Since 2020, insiders have not purchased shares of Roku. In fact, from Q2 2020, insiders have sold about $977 million worth of stock, with the vast majority of sales occurring during 202” (MarketBeat, 2023). Institutions, however, are more promising. Institutional ownership is currently over 66%, and “over the last 12 months, institutional inflows have amounted to $1.42 billion, compared to $907 million in outflows” (MarketBeat, 2023). The average of analyst PTs on the stock is 71.04, which would not offer much upside from here.

Fundamentals are fairly ugly, and as they do not stack up against the competition in net income or P/E ratio, which look scarier than any horror movie you could stream on your Roku television.

Roku’s last earnings were mixed. Net losses were 194 million, up sharply from 26 million the previous quarter. Platform revenue dropped by 1% but was offset by an 18% increase in device revenue. One positive area was user growth, with their base growing by 17% (Roku, 2023).

TA, options, and some sunshine pumping

The picture I paint above shows room for caution. If you believe that market breadth will narrow in the near future because the magnificent seven will pull back, a stock like $ROKU is likely to catch some stray bullets and would have trouble standing on its own with major tech pulling back. However, the recent pullback near 60 dollars is worth watching for signs of support, particularly among day and swing traders. $ROKU has seen strong intraday and weekly rallies this year and pulled back enough to potentially charge up for another round.

Options volume has been steady throughout the recent pullback, with some interesting buyers at 7/21 and 9/15 75C. I would not call the picture in options definitive but there is no significant push in puts under 60 as of yet.

ROKU 7 day options volume (Unusual Whales, 2023)

In closing, I’m not an analyst, I’m a trader. I look for stocks that have been here before at a level of support, a reasonably favorable sector environment, and supportive flows in options. $ROKU has some major issues ahead to achieve growth, become consistently profitable and compete in a difficult space in streaming and hardware. In the short term, a recovery to recent highs at 75 is plausible.

References

Baccardax, M. (2023). Apple, Nvidia, Meta, Lead Market Rally (Why That's Not Good). The Street

Pfeiffer, Lee. (2023). The magnificent seven. Encyclopædia Britannica. https://www.britannica.com/topic/The-Magnificent-Seven

MarketBeat. (2023, June 20). Roku’s recent gains bring hope amidst slump in streaming giant. TradingView. https://www.tradingview.com/news/marketbeat:234ba5356094b:0-roku-s-recent-gains-bring-hope-amidst-slump-in-streaming-giant/

Roku. (2023). Roku Quarterly Results . https://www.roku.com/investor/quarterly-results

MacroEdge contributors may or may not have a position in any mentioned ticker. MacroEdge does not endorse any ticker mentioned in contributor pieces and no direct MacroEdge representative holds any position in tickers mentioned above.

Thanks for reading MacroEdge! Subscribe for free to receive new posts and support our work.