6/12 Special Monday Release: Real Estate Heroin and the Fed/Gov Enablers

A special Monday edition real estate update from California based real expert Vince Caviglia. Thank you Vince for the submission and enjoy the read all!

Thanks for reading MacroEdge! Subscribe to receive new posts and support our work.

Thank you to one of our core team members and real estate expert @CavigliaVince for the fantastic real estate writeup.

Everybody is looking for answers for what caused the low "on-market" inventory in housing. There is everything from Airbnb, build for rent, and Ibuyer. I bet you have heard there is no inventory, this is a facade. This is also a complex topic that we will simplify. Each of the above references are playing within the rules of the game and none of them set the rules. They can benefit from it though until the dealer takes their drugs away. The cause is government policy and the Fed manipulation. This was supercharged by the Fed merging with the Treasury so they could buy things previously illegal by their mandate. The Policy is always what surprises me and also why people end up with these off views.

Short Term Rentals

A simple google search will bring AirDna up as a tool people use to analyze what their Airbnb and VRBO would rent for before purchase. Airdna says 1.424M the bureau of labor statistics say there is 144M homes in the U.S. These numbers are rounded, but that is about 1% of market. This is not enough to topple the market. This is not enough to drive the market up either when you consider many were already owned. This was happening long before covid and some will go back to long-term rental. On the flip side, they are earning less and many will sell, but this is not enough to topple the market.

Blackstone popularized this in 2008 with Invitation Homes. It has been around longer so you find salacious headlines like they are going to own 40% of the market by 2030, or 59% of Single family homes built are build for rent. My favorite recently everybody is freaking out over 4000 homes bought by Petrium from DR Horton. The institutional ownership number is hard to find. In numbers by, the Department of Housing and Urban Development and U.S. Census Bureau, Rental Housing Finance, This is from December 2022. They state 121,000 single family owned by REIT's. I believe this is what most people are afraid of and that number barely registers. The way the government plays with numbers for fear and pass policy. They state 14.3% but this includes all real estate companies and LLC and a lot of other entities. It also includes Multifamily which is not the topic of this article. The LLC, LLP, and LP this could be mom-and-pop owner that owns one property in an LLC for liability protection and taxes. The 14.3% is only of the rental market, not the whole market.

The entity’s private funds do use these types of holding companies as well and can be large private funds. Let's give them a bone and say the whole 2,362,000 is institutional. Then add the REITs in there and they would own 1.7% of the housing market. This is still nothing to get excited about. This also has been going on for much longer than covid. They were not the majority buyer

Ibuyers

You can see here again the Ibuyers are not that big of a portion of the market. They all got crushed and already gave most of their inventory back. People accused them of setting prices, they do not own enough of the market to set a price. They do not have a monopoly on housing. The rates did that for them. All of these bring the macro to the micro. There might be one-off markets that were disproportionately affected. You should have a process for both. The macro moves are what people always call black swans when everybody can already see it is slowing.

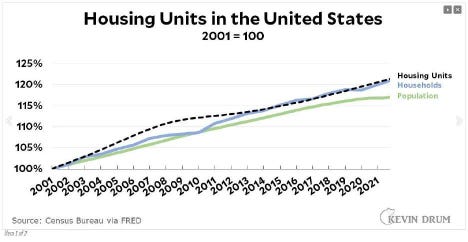

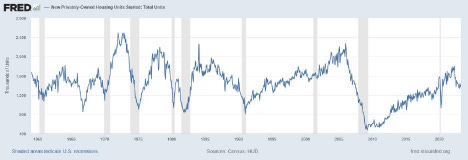

Real Inventory

Everybody said we underbuilt homes since 2008 but we have more homes per person. It is only the on-market inventory that is low. Let's take care of demographics and then revisit low-on-market inventory.

These trends don't have to be complicated when you do not listen to the narrative and put it together for yourself. You can see we did not need to build as much to keep up less population growth and household formation. The average age of marriage.

We have been in a home crisis for years making policy off it.

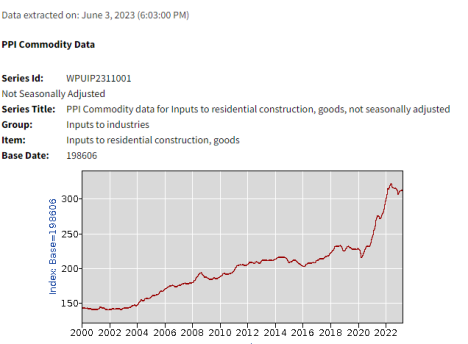

Residential PPI

You see it has not dipped much after 2008 then continued up. Then it skyrocketed. Let's use my market for a hypothetical. You build on the low end 600K house 1000 sqft. Your land cost 20% 100K. Your build cost is 400K or 400 a foot, throw in hold cost on private money take out financing, 6% for sales cost, taxes and insurance, development impact fees, and your building for free or upside down. Before all the additional fees it is about 16.6% difference from land and build to sale price. This is to simplify.

Then let's say for easy math 1 million dollar home. 200K for land cost, better finishes 450K build on the 1000 Sqft. Let's leave the additional fees out. Now you have a 35% spread to account for fees and profit. Yes people make careers off minimizing the cost to increase margins. Bezos famously said your margin is my opportunity. But this works even better at higher prices all a result of PPI and how they handled the last cycle.

This created the vast majority of development in the high end. Let's use my market above and below 1 million inventory. Below 1 million we had roughly 2.5 months of inventory the back half of the cycle. Above 1 million we had 6+ months of inventory. The affordability crisis is made. The only crisis is on the low end where we need it most.

I used my market for example but spoke to a land kicker that sold all of the Pacific Northwest and said it was happening all across the country. I first heard about this when Sam Zell said it about New York in 2015.

This is also why the high end is going up faster and down faster. More on this in a minute. But "they're not making any more land in California" yes that is when you build up. The city has increased density on everything.

Policy, backlogs, Inflation, and "On Market" Inventory a.k.a months supply

If it was not those things what was it. It is what it always is government and the FED. Policy first, let's not drive division on party this all happened under two opposite parties.

Covid happened and the next thing they did was lock everybody down. They shut companies down. We had an explosion of job loss and foreclosures. There were some industries still open this means orders were still coming in and backing up. This means a large demand that was being produced while the product was not.

The best illustration of this was lumber. They shut down Canadian logging, removing one of the biggest supplies of lumber. U.S. Lumber Reit’s soared. The reason the inflation was so bad is they created a supply-demand imbalance that allowed everybody to raise prices to meet the demand. Then the economy reopened and everybody had to race to get production back online and raise prices. They also printed a lot and gave the banks a huge way to monetize it into the economy.

The narratives discussed above may have added a little to the inventory, but it pales in comparison to government policy. The foreclosure immediately skyrocketed. It topped at 12%

within months we were at the highs seen in 2011. The government made it so banks could not foreclose, they put the properties in covid forbearance, people did not need to make payments, then they allowed banks to take the foreclosure completely off the books. This was an instantaneous removal of the forced sellers and 12% of the mortgage market.

It would take 10-12 years of new build inventory to replace that. This created another supply-demand imbalance.

The next thing you need to do to create an inventory problem and the fastest rising price ever is bring back the demand and add more fuel to the inflation fire. This comes to the FED and Treasury merging which allowed them to buy not only treasuries in their normal operation, but also buy MBS for the first time.

This dropped rates to the lowest in history compressing the MBS OAS and the 10-year. Paraphrasing, there is something called the one-factor model. It basically says that when rates move 2 standard deviations in either direction it becomes the only thing that matters in the context of affordability. It is the fastest-moving part of affordability compared to price and income I got this from Josh Stenier at Hedgeye. Hint income is the slowest. We saw the top side of the one-factor model, now we moved rates back up faster than anytime in history. This caused an explosion in demand while 12% of homes were sitting in Covid forbearance causing the first phase of the supply-demand imbalance. You can see below off the lows how fast that happened.

Now with rates so low it changed the affordability so drastically that it pushed the curve of buyers up in price right into the inventory of what people built this cycle. The buyers could afford the payments and their dream home. This made inventories match across the board. This is also why the high end went up faster than the low end in price. Simultaneously allowing them to not make car payments, credit card payments, student loans, pretty much all debt. Then you add PPP, ERC, and Stimulus checks. This directly dumping money in the economy. The banks were able to monetize the money off their books through real estate transactions.

Now the Covid Forbearance can be sold off slowly or the owners resumed payments as the economy got going. They potentially even refinanced into a lower rate that was affordable. The price increase brought them to a new level of wealth so they held on.

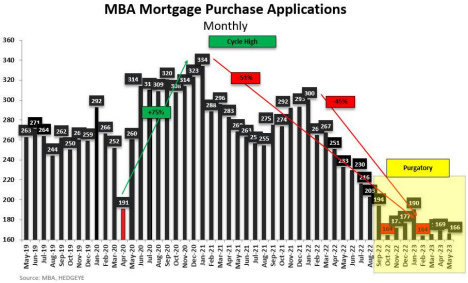

Refinance Applications

Let’s add back in the buyers from earlier IBuyer, Build for Rent, and Airbnb/STR buying 1% of market each in each year. These are a classic case of playing in the rules the FED and government created and chasing yield in an overvalued market.

We will move on to the exact reversal of this and the unwind in the current market. But first the backlogs discussed above this also applied to the city level. They let all the city go to remote work. It caused a backlog in permits that is still there today. I have spoken to developers across the country and this further limited the inventory. I experienced it first hand as well.

The Next Phase

When you say anything bad about the housing market or say prices are going down everybody jumps to, it is not 2008. It is not, they are all different with shades of the same. This is the everything bubble and there was a lot of money in the system. When people look back on those times they do not realize 2008 started in 2007. The Fear gripped the market with bank failures, this is the only part they remember. This is due to trauma. Then real estate nationally declined till 2012. It takes a long time to play out. Even in stocks 2000 started down in 2000 and went down till 2002. 2008 started in 2007 and did not bottom till the end of 2008. Nothing goes down in a straight line, the economy deteriorating on economic reports and better-than-expected earnings that are way off the highs is not the start of a new bull market.

The next phase was the FED saying it is transitory. We all know now it was not transitory, whether they were dumb or this was the plan is not for me to say. There were many that knew it was not transitory. I made this call on multiple podcasts and panels. I am an autodidact real estate developer. I do not have 400 PhD’s on staff like the Fed. What they did was paint themselves in a corner. They either have to raise to kill inflation or they go back to cutting and re-ignite the inflation which would be a much longer and harder road.

During the transitory talk, NAR does a home survey every year and the majority of people said it was a good time to sell. They said this but everybody was making so much on the fastest price rise in history that nobody was selling. You can look at household net worth.

The high demand above and the few people bringing their properties to market created the lowest on-market inventory(months of inventory) ever. Then you add the smaller catalyst, not the cause, the backlog in building and building supply, Ibuyers, Build for rent, and Airbnb/STR.

Then you get what you get at the end of every cycle, “nothing can happen because inventory is too low”. Both Commercial Real Estate and Residential started declining in June 2022. If the inventory is too low, why did the market decline in price as well as the inventory increase? Months supply is a reflection of the number of sellers and the number of buyers. It does not reflect true inventory.

Then you get people saying nothing can happen because nobody will sell a 3% rate. The FED said they want unemployment to rise. If you have no job and a payment, it does not matter what the payment is if you run out of money you cannot make the payment. My experience in the last cycle is that you need 14 days to stop foreclosure. People will wait till day 15 to ask for help. This gives this a long lead time.

The reason these drag down in the examples above of the previous cycle. The first phase all the economic indicators need to go down for people to realize. You print that much in combination with Covid handouts. Then let everybody stop payments on all debt. It is going to take a long time to suck all that cash out of the system.

First it was nobody will sell 3%, then everybody has cash, now it is low unemployment or foreclosure. They jump to the later and later cycle indicators. There is also a lot of noise with people quoting incorrect indicators.

What have we seen, credit card spending spike, savings tanked, retail sales dropping, PMI and ISM flirting with contractionary numbers. The Covid cash and credit cards are coming to the end of their spending.

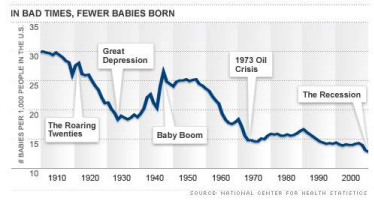

This is a good time to go back to demographics. Everybody takes the birth rate and projects forward. If you look at the average family that has no savings left and defaults on credit card debt. Unless it is an oopsie baby, I do not think people in that position are going to think it is a good time to bring a child into this world when they are having trouble taking care of themselves. This happens in every cycle. It gets more pronounced when people lose jobs which is what the FED wants.

It also happens in every cycle the family creation drops and the backlogs in development come out and it flips inventory. This cycle is more pronounced because of the problem covid caused at the city and the backlogs in building supply.

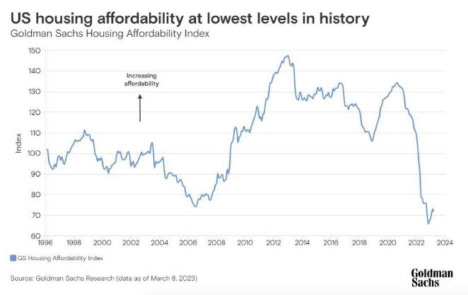

If you couple this with now we have the least affordable market ever. The rates made it affordable now the FED says no soup for you. The 3% rates and the declining home value has created home prisons. People do not want to lose money so they are holding on. 1.4M homes are underwater. It is a small amount but it is a start. 62% of people that bought in 2022-2023 can not make payments.

People are hanging on because of the narratives they see and thinking the FED will cut. They had a long wick discussed above. The FED only cuts when things break. Even after a FED pause the unemployment spikes historically.

Foreclosures I see people showing the lagged data charts from the St Louis FED and quoting a research company that does not have loan-level data. They say there is low foreclosure. Even in my market if you look at the governing body's research it says 100 foreclosures this year. You look at Tax Docs and it says 718 this is down from 1602 earlier this year. People can still do a notice of default equity sale till the rest of the cycle plays through. Black Knight had the total delinquency rate in February was 3.45%. Q4 2007 was 3.1% and Q1 2009 was 8%. I am still not saying this is 2008. I am giving context. These can continue NOD equity sales till some of the other factors above play out, especially unemployment. The banks taking too big of a hit to tier 1 core capital will force them to be more aggressive as well. The cherry on top is personal bankruptcies are rising.

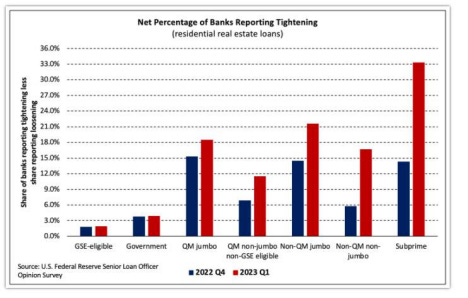

If we tie some of this together. We have the lowest mortgage purchase apps ever, the lowest sales volume, and very low on-market inventory. Unemployment makes forced sellers. This changes the inventory. The bleak personal finance picture the buyers will not rush back in at the end, liquidity in the market and tightening credit standards ensures this. We are just seeing the beginnings of liquidity and tightening credit. You can call all non-qm subprime it is the same under a different name. It is a loan to a non-prime borrower that has something wrong with it. I have seen things like less than 1% debt service coverage ratio loans with 10% rates. This means on a rental house the owner still has a payment. Yes, they are being sold into the MBS market. I have also seen people use non-qm for house flips. It is different like all cycles but the risk is still there. Subprime did not cause the last cycle, the Fed raising rates 17 times in the last cycle and Clinton wanting to increase housing ownership did.

I will wrap it up with this. Since the 1980’s they dropped rates every time to get us out of a recession. 2008 they ran out of cuts so they did QE on top of cuts. 2020 they cut then merged the treasury and FED so the FED could buy the whole bond market previously illegal by their mandate. 2008 we had bailouts, TARP, HAMP, HARP, and FDIC Loss share. 2020 They allowed banks to take distressed assets completely off book. We also had the supplemental

reserve ratio. They stopped all payments on everything: credit cards, student debt, rent, home mortgage, etc… They also did bailouts, the one that comes to mind is airlines which did 48 billion in buy backs then got 50 billion in bailouts and it saved no jobs.

Every time we do this the policy gets more extreme, puts the next generation more in debt, and steals opportunity from the people. This is why the wealth gap keeps getting bigger. This is also why all the narratives above exist like Real Estate only goes up. It has been trained for 40 years. Ray Dalio in his book has a whole chapter on a beautiful deleveraging, then one sentence on how it widens the wealth gap. Well, we have more debt on everything. “Debt cuts both ways” and “debt is the brother of volatility”

I cannot tell you the crazy policy that will come out this round. I can guess what is going on around the country. They will claim civil unrest to use emergency powers to do whatever they want. Claim something like, they need to stabilize the markets because people are looting in SF and firing guns in the streets of Chicago. But they need you to keep blaming the greedy corporations and have fear as cover. Ibuyers, Build for Rent, and Airbnb. This paragraph is an educated guess.

I told people in 2008, 2018, 2020, and now what always happens is I lay out my thoughts then people forget. Then when I am not participating people accuse me of liking to see people in pain. I am just a player in the madness of crowds so take from this what you will.

Thanks for reading MacroEdge! Subscribe for free to receive new posts and support my work.