5/15 Report - Recession Indicators, Canadian Housing Update, Airbnb Update, and More

Recession Indicators from @DonMiami3

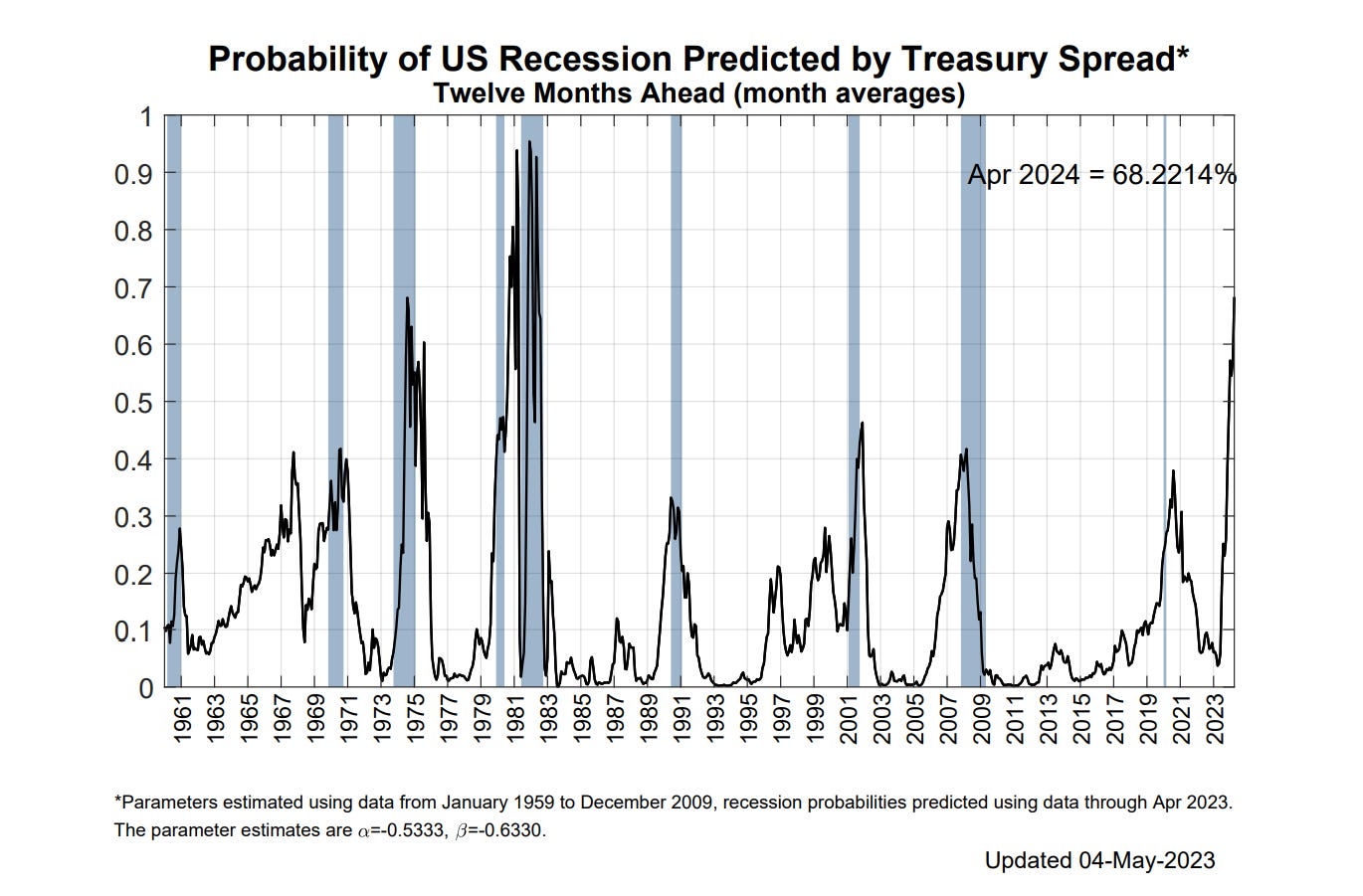

Firstly, NYFed recession odds near highest ever…

Empire State Mfg Index -31.8 actual -1.8 expected 10.8 prior Mega recession

From Peter Schiff “the April Empire State Manufacturing Survey "unexpectedly" collapsed 42.6 points, from +10.8 to -31.8. Outside of the Covid lockdown, that's the biggest MoM drop ever. New orders also fell the most since Covid, indicating the #recession the #Fed expects will be anything but mild.”

The above chart highlights the returns for various indices - and the underperforming micro caps and IWM index. Small caps are clearly leading the market into the recession.

Current bank lending standards have tightened at one of the fastest paces on records - which proceeds bankruptcy filings as the cost of doing business rises dramatically for operators:

The market rallies continue to be extremely weak even on big moves from names like Apple that in our opinion look to be mostly exhausted. There’s little on the bullish side that can continue shifting the market headwinds in a more bullish manner. Right now the risk seems to be skewed heavily towards the downside as yield curves remain heavily inverted and the major indexes have largely stalled on movements over the last several weeks. Over the next few months, we could see the unemployment rate move finally as JOLTS falls - even on historically horrific demographics. Right now - we’re keeping our eyes on the #HOPE framework from Piper Sandler - and other factors like more regional bank failures that could present further risk for the financial markets.

Canadian Housing Update from ‘Woes’ @ManyBeenRinsed

Canada is currently in a dead cat bounce when it comes to housing. The games continue to be played with incentives being given out like cupcakes. Toronto is selling condos with a free trip to Cuba, iPads and gold bars. Wall street is pretty much running away from the housing market while the unsuspecting retail buyers are led to the slaughter. Low sales volume ramp has never ended well as Canada is currently at levels not seen in decades. Immigration is also been sold as the saviour of the Canadian housing market as it saw over 1M newcomers in 2022. Despite record immigration last year - the country still saw some parts of housing drop 30-40%. This week alone countrywide there were job fairs held where lineups of thousands of immigrants\students were seen to fill a small amount of job openings. How is this not a recipe for disaster?

Developers are targeting immigrants with sales pitches and FOMO tactics to get them to buy overpriced home in far fetched towns from Toronto. None of this is going to end well. This is like a slow train wreck. The months ahead are going to be very interesting. If you see a slight uptick in supply and\or unemployment could rattle the ponzi scheme.

Airbnb update from ‘Amy’ @TexasRunnerDFW

Airbnb will report quarterly earnings on Tuesday, May 9. I expect earnings to be closely in line with expectations. While many markets are experiencing oversaturation, demand for vacation rentals remains high. The stock market has rebounded a good bit from the lows of late 2022, and unemployment, if you take the BLS numbers at face value, is at record lows.

At this point in time, despite recent regional bank failures, America is still on vacation. Airbnb should still be quite profitable, even as some individual hosts with less desirable properties in over saturated markets begin to struggle or drop off the platform, opting to list their properties as Long Term Rentals or put them on the market for sale. As always, it’s a game of supply and demand. Areas where high demand is being outpaced by even higher supply are going to see inferior hosts suffer.

A recent report by Murray Cox from www.insideairbnb.com highlights the Dallas market as an example of what the distribution of Airbnb rental properties looks like in a major metropolitan area. It’s not pretty. 85% of the listings in Dallas are entire home or apartments, not “spare rooms.” Translation: they’re taking housing stock off the market for locals to live in.

What’s worse, only half the homes listed are owned and operated by hosts who identify as Dallas residents. This is fuel for the fire in local heated City Council town hall debates. Residents in local neighborhoods want these commercial-use properties owned by “outsiders” with no connection or personal investment in the community, to be heavily regulated or banned. Some cities in the surrounding Dallas suburbs have already implemented heavy regulations.

I surmise that Brian Chesky has seen and absorbed all this data, as Airbnb recently announced they’re adding “Rooms” to the platform. It’s being presented as an effort to return the Airbnb business model back to its roots. While a nostalgic PR move, it’s also a strategic business operation plan for an upcoming recession (rooms are much more affordable than whole house rentals). This move also positions the company nicely against future regulations. From a potential supply standpoint, there are a lot more rooms available in the world than there are entire homes. This enables the platform to grow their number of listings even faster, replacing home listings that are forced off the platform due to increasing regulations.

It’s a smart move, and Chesky does seem adept at staying one step ahead. As vocal as I’ve been on the Airbnbust concept, I have a lot of respect for Brian as a CEO. I do believe the company will be able to navigate the troubled waters ahead in a higher interest rate environment. But the rough waters will not be kind to over-leveraged apprentices of Tik Tok BRRR Investor University. This cohort may find themselves unable to stay afloat with their 20 TJ Maxx bargain bin properties, and go bust.

A Market Update from ‘$ix’ @SixFinance This week was an interesting one. Firstly, I want to touch on tech earnings. Earnings beats coming in are overshadowing the fact that on a year over year basis, earnings for many of the big tech companies are declining. META, while being up 12% after “beating” earnings, saw revenue fall 19% YoY. The analysts, as always in effort to keep funneling AUM into their buy and hold strategies, revised earnings projections down a little too far, thereby causing vastly misguided optimism in tech. Equities are living in dreamland. Nasdaq is smoking crack in the penthouse, blissfully unaware that the police are on the way. First Republic becomes the third large regional bank destined for conservatorship. This has caused financial markets to incorrectly price in rate cuts later this year, although the market seems to neglect that inflation is inertial, and not easily tamed. PCE came in slightly over expectations as well. Nothing crazy, but worth noting. With the BRICS alliance on a de-dollarization mission, the FED also has an additional unspoken obligation to defend the dollar. It is not something that the FED is likely to publicly acknowledge, less they risk giving BRICS agenda some credibility. Finally, the case for rate cuts at this point in time is very weak without a drastic spike in unemployment, which is extremely low historically. Let’s not forget the lessons of the 1970s era and repeat this ridiculous Fed Funds Rate pendulum. I am currently short the S&P 500 with leverage from the 4200 mark as a large amount of factors indicate that a large downturn is coming, including but certainly not limited to: • Year over year contracting money supply (last few times this has happened were: Great Depression of 1929, Depression of 1921, Panic of 1893, and the 1870s Banking Crisis) • Deeply inverted yield curve with the spread between the 10 year and 3 month treasury yields currently sitting at -172 basis points, the largest inversion in over 40 years. • Median housing price to median income sitting among the highest in history. • Government Debt to GDP sitting at all time highs. • Federal Reserve balance sheet being unwound, removing liquidity. • Interest rates rapidly rising, causing chaos in a system massively overexposed to low yield treasury debt. With 2 large banks already failed since January, and First Republic teetering on the brink of collapse as well. These banks held large amounts of low yielding treasuries that have declined largely in value as new debt is issued at a substantially higher yield. • As the fed funds rate rises, the debt service costs to the treasury drastically rise. • And much more…

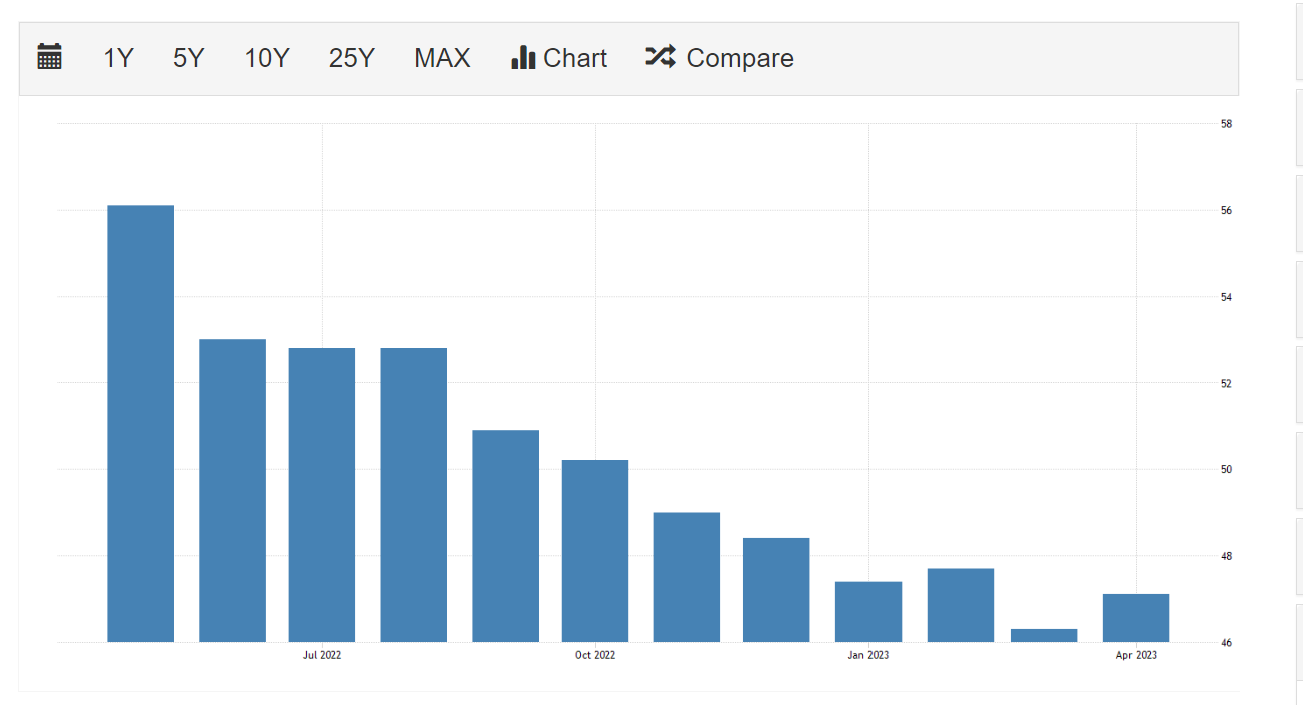

From Oppenheimer “the worst phase for the market is when the PMI is below 50 and contracting …”