4/28 Weekly Ozone Report: FOMC Magic, Employment Data Ahead, Vision May Update, FOMC this Week

In this 4/28 weekly Ozone report - Don covers the very busy week of data ahead, CRE issues and more, while Six provides a Vision Equity Research desk update, and John covers the critical FOMC meeting

Don

Happy Sunday evening everyone -

Hope you all had a great weekend and are ready for another rollercoaster week of data this week in the markets. We’ve got exciting new things coming out at MacroEdge weekly - including new datasets this evening in the dashboard (so make sure to check them out) as well as a fabulous edition coming to MacroEdge Radio next Friday at noon EST with special guest Rudy Havenstein: https://x.com/MacroEdgeRes/status/1784723191966966190

We also announced a new partnership with week with Investing Angles (@InvestingAngles) to provide data access to their community of technical analysts and experts, which is very exciting news.

MacroEdge is currently discussing new features that may result in the creation of a new content creation team (ie: MacroEdge TV) that would cover some of the most important data features on a weekly basis + provide a new platform for our contributor team with a video outlet for those that are looking for new ways to connect with our readers across our various platforms.

Make sure to stay tuned to the latest updates to MacroEdge Vision as well, our new equity research desk led by Six, which will have updated visuals for all Vision/Ozone members in the coming days. This all can be found as a member of MacroEdge Ozone:

We’re making great progress as an organization and group and I wanted to thank you all again for playing such a core role in our growth.

In the report this week which we’ll dive right into, we’re covering:

Real Estate Overview

The real estate market (residential v commercial) continues to be a very mixed picture. Many of you have probably seen a lot of the CMBS/CRE data we’ve been posting - highlighting the scary picture in the commercial office/commercial mall spaces in many markets. Price markdowns of 50+% are becoming very common occurrences in major markets and there’s still about $1.5 trillion in outstanding debt set to mature over the next 16-18 months. (Expect the can to get kicked on a lot of this debt.)

There’s even been some interesting curveballs in the data such as with the Four Seasons Wailea in Maui hitting the default watchlist as it’s occupancy rate and financial stability have come into question. Other properties occupied by the Four Seasons portfolio like in San Francisco and New Orleans - have also defaulted as well.

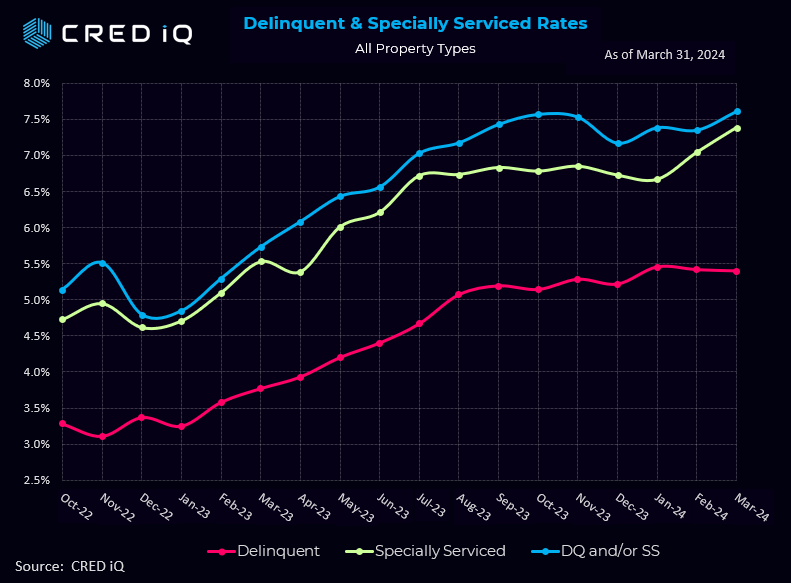

The distress rate for CLOs rose to a new all-time high, per CRED iQ.

As did the distress rate for all CRE types:

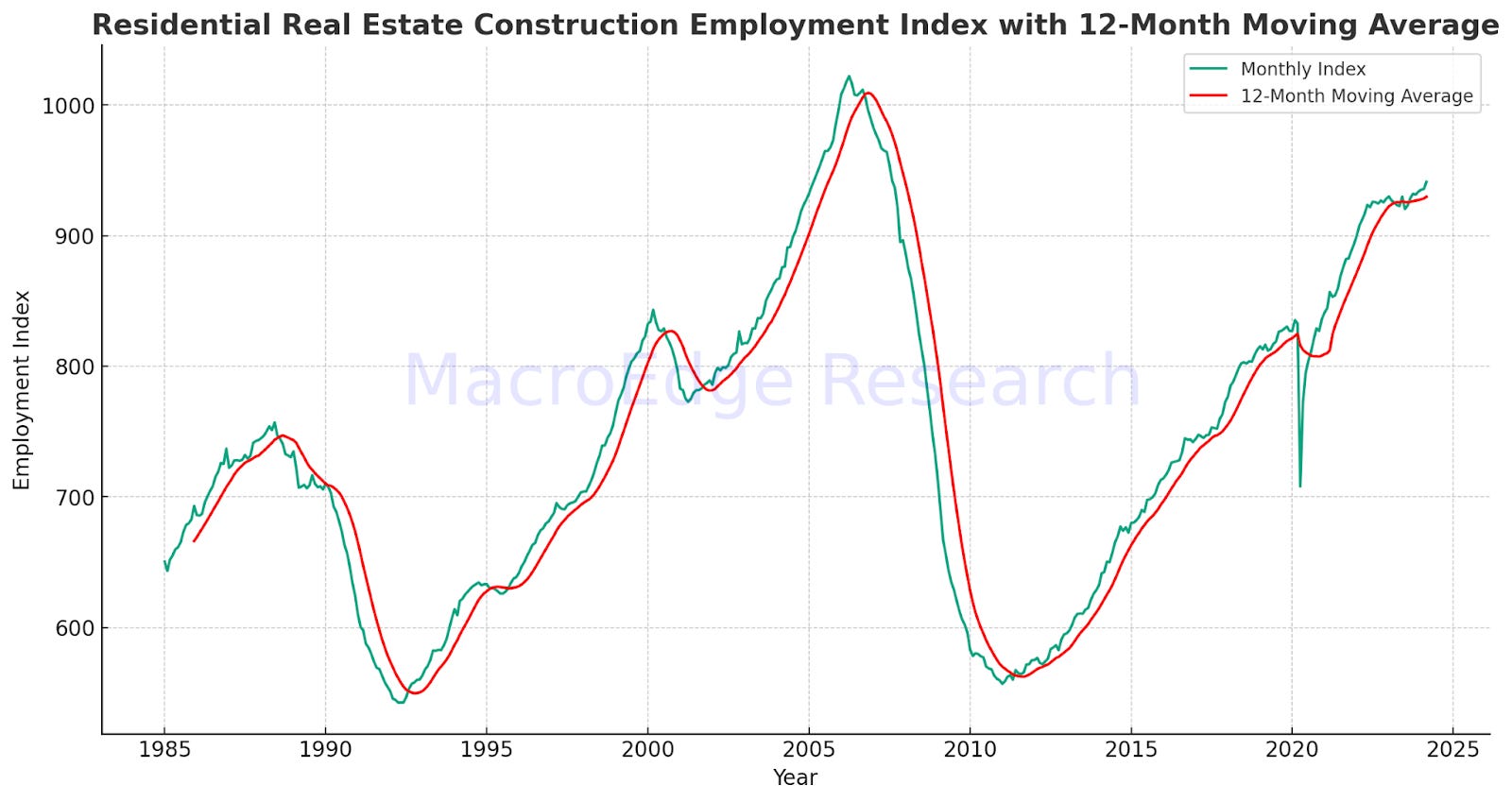

As the CRE stress continues to mount and weigh heavily on the smaller banks with heavy loan concentrations in the space - we’re also seeing some macro signs that a further slowdown may be headed towards the new home side of the equation. While overall headline for the residential construction sector has remained particularly hot:

we’re likely trending towards the necessary equation for a deacceleration of growth in this key cyclical employment area of the larger employment picture. The slowdown of active construction in multifamily is now under (as Awsumb refers to as ‘Niagara Falls’) and the price of lumber has been indicating a coming deceleration in the NAHB Index (which tracks the new home market).