4/27 MacroEdge Redeye: Bending Reality... A Bank Failure, Market Conditions, Sentiment, Employment Data Ahead, and Fed Ahead

In this evening's MacroEdge Redeye - we dive into a discussion on 'bending reality', a Friday evening bank failure, market conditions, current sentiment, employment data, and more. *Excuse typos

Redeye @DonMiami3 (Don Johnson)

Happy Saturday evening everyone…

Will keep this one a little shorter than usual this evening due to the late hour and our Ozone report coming tomorrow.

Hope you all enjoyed last night’s edition of MacroEdge Radio as much as I did. If you haven’t joined us in the Ozone before we hop off of Substack in the coming weeks as John noted, catch two weeks of access to the new platform here:

Welcome to this edition of Redeye called ‘Bending Reality’ - where we’re going to dive right into several different important topics. Let’s break this one down into a few key areas:

A Bank Failure

Market Conditions

Sentiment

Employment Data (+ Fed Ahead)

A Bank Failure:

Yesterday evening we got another bank failure of a smaller regional bank (Republic First Bank) in Philadelphia… It appears that anything with ‘First’ and ‘Republic’ might have some sort of curse to it… but maybe that’s more coincidental than anything. They had about $6bn in assets and had been on the watchlist for about a year, I briefly discussed it back in August when its stock FRBK began to collapse and then was subsequently delisted by the Nasdaq. Since then they had attempted to pull off a last minute cash raise - but capital raises are no much for higher for longer and a toxic mortgage book which contributed to the downfall of FRBK.

If you zoom out and take a look at KRE (the regional bank basket ETF) it’s clear that the risks remain here for a number of these banks. Some banks that have been on the same watchlist, like VLY (Valley Bancorp) are having a hard time even catching momentum with the larger basket of regional banks as they bounced a bit.

Market Conditions:

Market conditions remain broadly softer after the face ripper that we saw to start Q1. As highlighted in our Sunday report from last weekend, my bias remains slightly bearish and agile as long as this setup remains on the Nadaq index and (similar charts) are seen across many other indices/names. The markets overextended themselves on hopes of rate cuts and now we’re moving into a combination of softer labor market data and ‘higher inflation’ for longer + rising yields that could spell turbulence ahead in risk assets.

This chart and the latest ‘bounce’ don’t inspire much confidence for me yet to start doing victory laps for more upside in the context of the broader data we’re seeing. Remaining nimble as Six highlights continues to be our theme at both MacroEdge and at the Vision Research Desk which has a more asset-heavy mission.

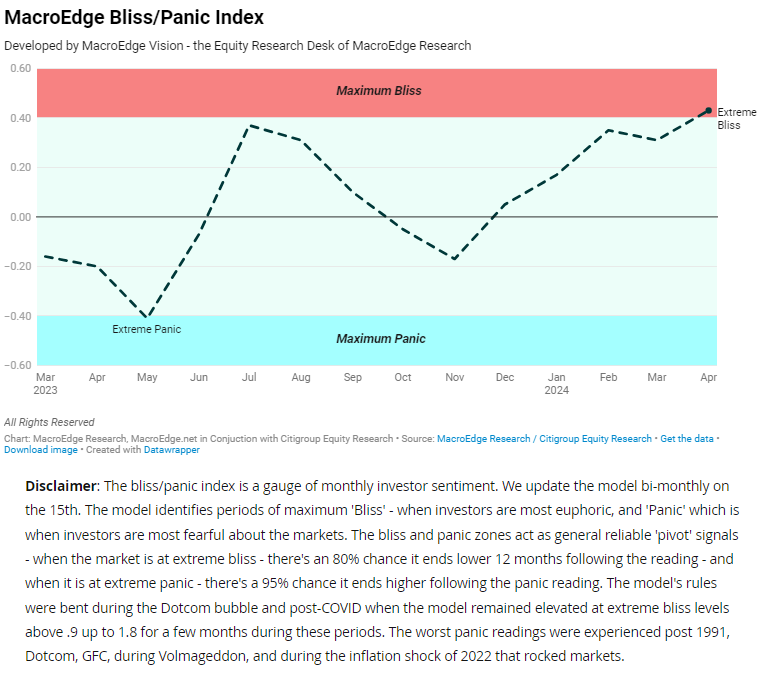

Sentiment:

Sentiment remains very euphoric and our Panic/Bliss Gauge remained unchanged on a week/week basis, per the MacroEdge Vision Research Desk (.43):

Employment Data(+ Fed Ahead)

The coming week is an important one… While we’ve been in a Fed blackout period we’ve gotten some more ‘hot’ inflation reads and missed out on comments from Fed speakers on the matter. Given the hawkish pivot that we experienced a few weeks ago (and now a bank failure) it will be an interesting week with the ‘play-by-play’ nature of the Fed of 2024 that has to talk about 450 times a week to keep things on the rails both for the markets and the broader economy with soft landing speak. April brought us an interesting combination of a higher more entrenched inflation narrative creeping into the equation along with softer labor market data in some areas - like job cuts and mass layoffs with the bankruptcy of the 99C franchise and large layoffs from companies like Tesla (which numbered around 10,000 in the United States). As we anticipate further labor market cooling in the months to come, we’ve also seen a softening in the NFIB/S&P Global employment data + KC Fed Labor Market Conditions Index + Fed Regional Surveys and elsewhere.

The current story remains one of a cooling labor market (less jobs, higher cuts, softening employment data) and higher inflation than expected… this makes the Fed’s job even harder in months to come:

Check out the latest update to our California Employment Index:

& our Job Cuts Tracker (setting a new high this month with over 105,000 job cuts)

& a last interesting point… Take note of the evolving housing dynamics in cooler housing markets that were red hot just months ago (particularly on the West Coast of FL):

Excited for another busy week ahead with you all and look forward to eventually calling our own platform home full-time.

Catch you tomorrow evening for the Sunday weekly Ozone report.

Your friend,

Don

Great read as always. Thanks Don 🤝

Thanks Doc, let’s keep this party going 🥃👍🏻