4/24 Report - Recession Indicators, CRE, and More

"Slowing economy: A cautionary tale of data and analysis"

Authors for this report: @DonMiami3, @CXCarroll, @SSun5555, @ManyBeenRinsed

Don @DonMiami3:

Super excited to be providing this great data to everyone - so much to digest and take in as we ride out a tumultuous year. Things are still flying high in mighty in certain sectors and areas around the country - although the leading economic indicators are pointing to more tumult ahead. I think the leading data gives provides us with a precautionary tale.

For this report I will be focusing on three different important economic indicators pointing to a coming recession - the first being the Conference Board’s Leading Economic Indicators (LEI) report, the second being the Philadelphia Fed’s Mfg Activity Index, and the third being the Dallas Fed’s Mfg and Service index’s for the South. For the Philadelphia Fed’s Mfg Activity Index - I ran a quick machine learning model looking at an increase in .5% in the unemployment rate versus the Index being below -35 for 3 consecutive months. I also looked at the Pearson correlation.

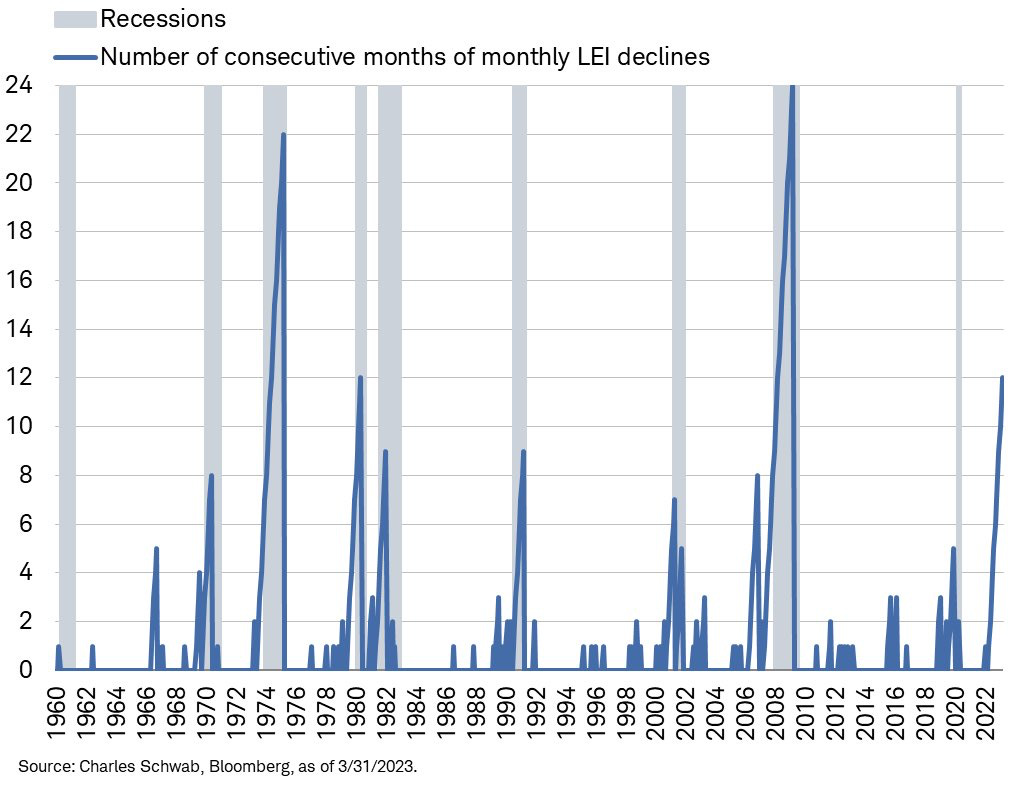

Conference Board’s Leading Economic Indicators (LEI)

The above chart highlights the number of consecutive months we’ve seen the LEI index decline - we’ve now seen almost a year worth of consecutive declines in the leading economic indicator index which has historically been a recession indicator.

The LEI chart itself highlights one of the worst declines seen over the last 25 years - along with the ‘Recession Signal’ line provided by the Conference Board. The LEI has seen a decline almost as severe as the Dotcom bust - pointing toward an economic slowdown ahead. I expect to continue to see this decline as we see the actual economy begin to slow - especially on things like the labor front which has still been fairly resilient.

Philly Fed’s Mfg Activity Index

There's a close relationship between the Philly Fed Economic Index and the Unemployment Rate. There is a positive correlation (0.4047) between the Index value being below -30 for at least 3 consecutive months, and the Unrate increasing by 0.5% or more within the next 6 months after the Index condition is met. When the Index drops to -35 - a logistic regression model (87.88% accuracy) predicted the likelihood of unemployment beginning to rise based on the Index values for a new data point of -35 as 0.714. The index is currently -31.3 for 4/1.

Dallas Fed’s Mfg and Service Index

Dallas Fed Mfg. Index (top) and Dallas Fed Services Index (bottom)

The Dallas Fed Manufacturing and Service Indexes contracted again in March (for the April report) showing continued weakness in both economic areas in the South. According to the latest report from the Dallas Federal Reserve, the manufacturing and service indexes for the South have contracted again in March, indicating continued weakness in these economic areas. The contraction in both indexes suggests that the region's economy is still struggling, and raises concerns about the overall health of the U.S. economy. It remains to be seen whether the indexes will recover in the coming months or if this trend will continue.

Cornelius @CXCarroll:

Much has been written about the impending commercial real estate collapse in the last few months. While the broad theme has been correct, there are some significant nuances to consider. Commercial real estate is a highly varied asset category. At a high level, you have the categories of Office, Multifamily, Hotel, Industrial, and Retail. However, each of those has its own subcategories. For retail, you have malls, "Big Box" centers, "Power" centers, anchored and unanchored retail strip centers, Single Tenant Net Retail (STNR)... the list goes on and on. Industrial, which to the outsider just seems like warehouses, is equally as varied.

At the core of commercial real estate, you have, essentially, three variables: the supply of a product, the demand for a product, and the cost of credit. Since we're talking about buildings, over a short period of time, the supply doesn't really change materially. In a "boom" year, the total square footage of commercial real estate in the U.S. might expand by 1% in the modern era. Demand is more elastic than supply and each category has its own factors driving demand but, over a short period of time, demand is generally pretty stable. This leaves the cost of credit as the ultimate short-term determinant of commercial real estate prices.

Simply put, if interest rates go up, the value of commercial real estate goes down and vice versa. This creates a problem for recent vintage commercial real estate purchases.

Let's take a simplified hypothetical example of a Chic-fil-A that sold in 2020 at a 3 CAP (an implied annualized current rate of return based on the net income produced by the property divided by the purchase price): net income $120,000, purchase price $4,000,000, financed 65% LTV interest-only at 2.85%. The buyer has positive carry and collects "mailbox money" right up until they have to refinance the property in 2024. Let's say that 2.85% turns into 6.85% under the same terms in 2024. The owner now has a negative carry to the tune of $100,000/year and likely has to bring cash to the table to refinance in order to meet DSCR and LTV requirements for their lender.

Let's say, for a second, that the owner is unable to refinance and is forced to sell the property. Will they be able to? Absolutely. At a 5 CAP, I could line up cash buyers from Palm Beach to Orlando to buy a Chic-fil-A: they're a juggernaut of a brand with the average store doing $8,000,000/year in sales. The real estate is fine. The financing structure is not.

There are thousands of contra-examples to my Chic-fil-A example in retail where the real estate is not fine, but I'm trying to illustrate a broader theme here: for the most part, the commercial real estate crisis is a financing structure crisis. Simply put, the industry got carried away with financing near the end of the Zero Lower Bound era.

I've been very vocal about 2023 and 2024 being the worst years for multifamily properties in decades. However, multifamily at its core, as an asset class, isn't going anywhere. About 35% of Americans rent their housing at present, which is right about the historical average going back to the 1970s. It's a very desirable asset class because it doesn't require any specialized management, and it's a fairly commoditized product that will sell (rent) on price. That's not true for the rest of commercial real estate. If it's so desirable, then, why does it face a crisis as well?

Simply put, it comes down to financing structure again.

Take that Chick-fil-A example again and layer on at least an additional 20% of LTV at purchase (many properties took on financing of 100%+ of their purchase price). Is the gross income (rent) up? Yes, probably, but lenders care about the net income and the value of the property. Real estate taxes, insurance, and operating expenses are all up (drastically in some cases) which largely offsets increases in rental income. When it comes time for the multifamily owner to refinance, they are going to have to come to the table with a HUGE check in order to refinance.

What happens if they don’t? Once again, at the right price, you will have a long line of buyers. In this case, that price will probably make the first-lien mortgage whole… Mezzanine lenders will likely not be made whole and may or may not assume control over the property… but all the while, the underlying end-user demand for the product is healthy. So, once again, it’s not the real estate that’s in crisis but the financing.

I’ll briefly run over the fundamental health of various categories of Commercial Real Estate:

Industrial: healthy, onshoring and reindustrialization is driving demand, short-term over-supply of warehouse space.

Retail: healthy-ish, banks hated the category post-‘08, LTVs stayed low, strong retail sales growth has occupancy costs as a percentage of sales rather low. Malls are an exception to this.

Multifamily: healthy from a fundamental demand perspective, but lending got out of control. Expect to see a wave of defaults.

Hotel: unhealthy. The post-pandemic travel boom temporarily hid oversaturation in most markets.

Office: dead (other than specialty and Class A).

The theme of this essay so far has been “it’s not a real estate crisis but a financing crisis.” Office is the exception to that theme. No matter how you spin the numbers, there’s no way to avoid the fact that the fundamental demand for Office has fallen significantly. It doesn’t matter if it’s 20%, 30%, or 60%. At the end of the day, we’re looking at hundreds of billions of dollars worth of properties and loans that are now impaired, and there’s no viable solution to that problem on a time scale of less than a decade.

Is this systemic? I don’t believe so. I do believe, however, that it will lead banks to tighten lending conditions across all categories, and that will invariably slow the economy.

Sun @Ssun5555: Since this is my first post, I will briefly introduce myself. People usually call me Sun. I am a real estate developer and builder in Southwest Florida. I have been in business for over 18 years and have built more than 500 homes to date. The majority of my business focuses on high-end luxury developments priced from 2 million – 12 million. I have also owned several other small companies, including a production-building company. I have been bearish only three times in my life, 2007, 2018 and NOW! In fact, in 2021 I was setting up a fairly large fund for single-family homes, but we luckily abandoned the project due to material delays and shortages.

Enough about me…let’s get into this market! We can’t dive into this market without talking about how COVID and specifically the trillions of dollars our government / FED dumped into the system. COVID cash is what I call it..... the stimies, PPP, ERC, and not to mention ZIRP. The trillions of dollars distorted home values by pushing assets through the roof, while ZIRP created a low-interest rate environment that allowed for easy access to credit. The combination of COVID cash and ZIRP was rocket fuel for the economy and specifically real estate prices. National home prices went up 30% + and regionally some places went 100-200% higher! It was like nothing anyone has seen before.

Fast forward to March 2022, when the FED began their most aggressive hiking cycle in history. We now sit at an FFR of soon to be 5% +. For those who don’t understand what Fed hiking is meant to do, let me explain briefly. FFR is a blunt instrument that is used to raise rates on credit through the banking system and other financial institutions. Essentially, it slowly strangles the economy into slowing growth. They do this to try and restore inflation back to their 2% target. Right, wrong, or indifferent, this is what is currently happening at a historic pace. The ramifications of most of these FFR hikes have not even taken effect yet. Typical lag for these hikes is anywhere between 6-18 months.

Now that everyone understands the basics, we can go into what is happening in housing and real estate. Since the start of QT (FFR hikes), the real estate market has been going through some turmoil. This cycle has thrown real estate into a continued downward spiral. Many large office buildings are just handing over the keys, large REIT funds are ganging, and home prices have been falling year over year. Usually when any asset price goes parabolic, it ends up coming back to earth (i.e., BTC, Tesla, Nasdaq, Tulips, GFC, etc.) and reverts to some sort of previous mean level. Essentially, what COVID cash did was pull demand forward by 6-8 years, creating a huge spike in prices. The FFR is essentially sucking the liquidity out of the system and tightening credit to pull this demand back to Earth. One can see evidence of the tightening cycle across all sectors of the economy right now, and in return will squeeze the consumer to the point in which they reduce consumption. Two of the largest purchases people will ever make are cars and homes. As the FFR cycles through the system, the consumer will continue to get weaker and weaker as the Feds grasp slowly strangles the consumer. At some point, in the near future, this lack of consumption will lead to a large spike in unemployment. Once we see unemployment start to rise, we should start seeing homes under $800k begin to decrease drastically. Demand will essentially be killed, and the psychological effects will take hold. Psychology plays a large effect in home prices and demand.

Once people realize that home prices don’t only go up, there will be a rush to the exits by investors and developers. In fact, it is already happening across the board in real estate. The luxury market has already been falling substantially in price, and demand is down around 45% YoY. (Anecdotally, I have been seeing the smartest money moving to the sidelines in real estate from billionaires....to major hedge fund players.) This psychological component, coupled with increasingly tight credit, will eventually cause home prices to drop substantially more and unemployment to start moving upwards. It is what many people in business have never experienced before, it is called a BUSINESS CYCLE! Next substack, I will get into greater detail on why home prices will be heading much lower. There are many small variables at play both nationally and regionally and too much to incorporate in our first issue. The devil is in the details, and we will be going in-depth soon! WELCOME TO THE SUNNY-SIDE!

Woes @ManyBeenRinsed:

The Canadian housing market has faced significant challenges in recent years, with drops of 30-40% in some areas in 2022. While there has been a small uptick in 2023, some believe that the bottom has already been reached. However, line ups, blind bidding, and overbidding continue to persist in certain pockets of the market.

Many believe that the pause by the Bank of Canada is a bullish sign, and rate cuts are anticipated in the near future. However, history has shown that rate cuts can actually trigger a sell-off, as was the case in the 1990s.

Ironically, there are protests for rate cuts, with some individuals actively seeking a market collapse. While there have been instances where low volume upticks in pricing have ended well, it is uncertain whether this will be the case for the 2023 Canadian housing market.

Currently, the market is stagnant, with a September 2022 listing at 1.75M having no takers, and an April 2023 listing at 1.4M not seeing any buyers so far. Despite this, some individuals are convinced that the bottom has already been reached, and are taking on massive mortgages with variable rates, hoping to lock in before the market declines further.

However, solely focusing on monthly payments in the face of uncertainty may not be a wise move, and could lead to disaster. The dead cat meow is luring in more bulls, and the next leg down could be a doozy.

This is the current Canadian real estate story, one that continues to evolve and present challenges to investors and individuals alike.