1/4 Weekly Macro Note: Kicking off a New Year, 2026 Outlook Part 1, Year of Differentiation & Our 2026 Predictions

We cover a year-ahead full of predictions for 2026, talk about the macro week ahead, get the wind in the sails for another very busy year, and talk about how this will be the year of 'differentiation'

Don Johnson (@DonMiami3), Chief Economist

Good Sunday evening MacroEdge Readers & Community,

This evening we’ll go over what we didn’t cover in our two previous reports - the Redeye Macro Note - and our special on Venezuela - highlighting opportunities in South America as the Administration takes a very ‘close-watch’ approach to the entire Western Hemisphere. This evening we’ll talk about what’s ahead, some broader macro trends and themes for the new year, and highlight our general 2026 outlook as it pertains to things like unemployment, inflation, markets (both domestically & internationally), and in other areas like geopolitical focus areas.

This week is an important labor data week, which will likely be the deciding factor (along with inflation data) and what the Fed actually does at the end of the month. Right now, we’ve almost fully priced out a cut for the month - and any sign of okay labor data, even with a Fed that’s expanding its balance sheet and providing short-term liquidity to markets and banks, will be enough to push a rate cut off likely to be late spring at the earliest.

If you missed our Venezuelan opportunity report - you can read it below - and catch all of our Macro Research Reports with MacroEdge Ozone - for one week below, through Substack:

Limited-time MacroEdge apparel is available through the order form below, for winter/spring 2026 merchandise:

Macro Week Ahead - Heavy Labor Focus

This week matters quite a bit for the FOMC meeting at the end of the month. We’re getting employment data (from both public and private sector sources) - including from us on the hiring & job cuts front.

Monday: ISM Manufacturing, Auto Sales

Wednesday: ADP Employment, JOLTS Job Openings, Japan Cash Earnings, ISM Services PMI

Thursday: Jobless Claims, Trade Balance

Friday: Nonfarm Payrolls, Wage Growth

We’re in an earnings dead-zone right now, watching for signs of a ‘2022-esque’ style repeat in markets. Earnings won’t kick off until late January, with the banks, and until then, it’ll be macro data, yields, and geopolitical data in the driver’s seat.

Geopolitical Flares Also in Focus

South America is likely to remain a major focus for this Administration (the entire Western Hemisphere, really) in 2026. We’re seeing resumed discussions about a higher level of involvement in Greenland, talks about overthrowing the current Cuban leadership, and we’ve already seen direct action in Venezuela and elsewhere (non-militarily) in South America, from Bolivia to now Colombia. This trend is going to continue, and opportunities for American investors should continue to present themselves across the Western Hemisphere under this ‘Donroe Doctrine’. As we’ve seen thus far in Venezuela - it appears the Administration is utilizing American military might and political influence first before taking an occupation approach - which keeps costs lower, and also likely means higher upside for opportunities in places like Chile, Bolivia, and now (Venezuela), where it’s likely the current regime stays in power, but under a much closer American eye.

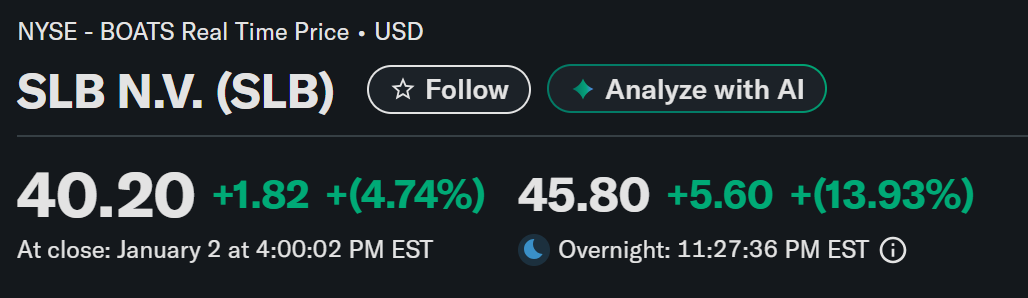

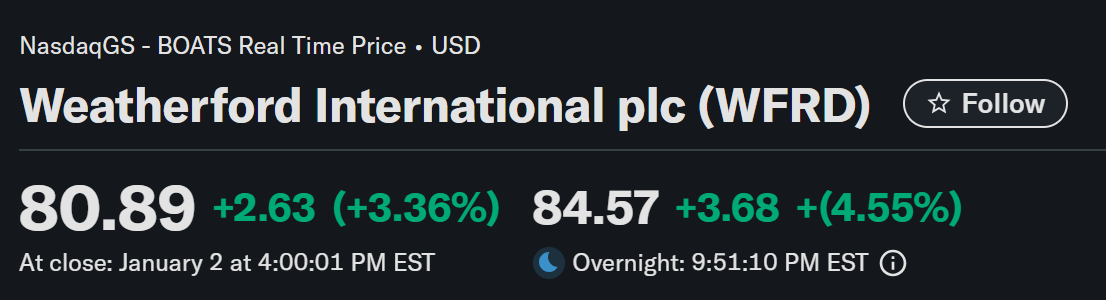

Outside of South America, Mexico is also coming into focus, with Trump deeply disliking Sheinbaum and the current Mexican Administration. While we’re seeing some anti-China alignment through shared tariffs, the leaders are politically non-aligned, and I expect that Mexico comes into greater focus in the 1st quarter, along with Cuba. The Venezuela mission is somewhat ‘accomplished’ for the time being from a political points standpoint - and now we’ll have to see what opportunities are presented to the private sector in the United States for opportunities in Venezuela - which will focus primarily on energy and minerals. Tonight we’re seeing steep increases in energy service providers - in companies like Halliburton - in response to the Venezuelan intervention.

(Halliburton up 14% in response to potential opportunities in Venezuela - note their high-levels of involvement in neighboring Guyana)...

SLB…

Weatherford:

Chevron is up nearly 10% - and like Weatherford, they already have a significant presence in Venezuela…

2026 Outlook Part 1

As we did in the 2025 year, we’ll make it known that the outlook for the year is more fluid than it is fixed. Analysts and forecasts get married to particular narratives and predictions, strapping onto them, and that’s a recipe for failure - especially from a return standpoint, which is really what matters above all else. Below, we’ll cover broad themes, and highlight expectations for this new year.

A mini-reversion in the ‘K-shaped’ or ‘I-shaped’ economy - we’ve heard more & more about a K-shaped economy in the second half of 2025 - especially as consumer confidence and current conditions have tanked.

A rising opposition to the data centers is already underway - but I expect it to gain even more momentum this year - becoming the 2nd or 3rd most important political issue in local and congressional races, behind the economy.

In addition to the above, I expect to see a single month with data center cancellations and postponements above 100 this year - December set a high for 2025 with 16.

There’s about a 50/50 chance for another government shutdown this year - and I expect anger to mount over the lapse in Obamacare subsidies that kicked in on 1/1.

Expect that we see increased involvement in the Western Hemisphere from the Trump Administration this year, and opportunities for US investors will follow (many have already been extremely lucrative), but the unlocking of South & Latin America would be significant because of huge populations & room for growth.

It’s unlikely that we see any flood of oil from Venezuela for at least the next year - there’s already a massive worldwide surplus from Guyana & the US - and even with OPEC on hold, Venezuela will take tens/hundreds of billions of dollars to see production move meaningfully higher.

More BoJ interventions are coming in Q1 with a super weak Yen, and carry trade being fully ‘recharged’ to levels we last saw before the April 2025 tariff tantrum.

Worldwide macro issues - particularly in the West - will start after or around the time the Bank of Japan needs to begin easing rates, which is not for at least the 1st half of the year.

Japanese yields will continue to push higher without fiscal restraint.

We see global bubbles in Japan, Spain, Canada, & Korea finally lose some momentum by the 2nd quarter of the year.

US unemployment could top 5% this year, given the lack of labor market momentum. We had forecast 4.7% to end 2025 - and we’re very close at the current time - if momentum worsens further, job openings could also fall below 7 million, though they’ve been quite constant for the last year now (measured by JOLTs).

Subscribe to MacroEdge Ozone below through Substack, and never miss a report:

Keep reading with a 7-day free trial

Subscribe to MacroEdge to keep reading this post and get 7 days of free access to the full post archives.