12/3 Weekly Report: Unraveling Net Job Growth in the Winding Down Year, Yield Plunge, Rate Cut Hopes, and Equities' Roller Coaster, Closer to Home, Gold’s Dangerous Rally, and America’s Housing Market

@DonMiami3, MacroEdge Chief Economist; @SixFinance, MacroEdge Head of Research; @SquirtLagurtski, MacroEdge Contributor; @RealJohnGaltFla, MacroEdge Contributor; @GregCrennan, MacroEdge Contributor

Unraveling November's Net Job Growth in the Winding Down Year (@DonMiami3, Chief Economist)

Hi all -

Happy December and hope you’re all having a great first weekend of the holiday month as the year continues to fly by into New Years. Today I am providing a short update on the employment situation as I continue to view this as the most critical element of all of the different ‘landing camps’ people fall into. Not much has changed regarding the ISM/S&P Global Data between services/manufacturing - but employment continues to be a fluid situation.

I anticipate net job growth to show up in the November numbers given our job cut tracker # at 50,896 - which was down over 30,000 m/m from October.

The largest layoffs were in the banking sector, logistics sector, as well as technology. We saw a sharp decrease in layoffs in the automotive sector with the end of the UAW strike (as expected).

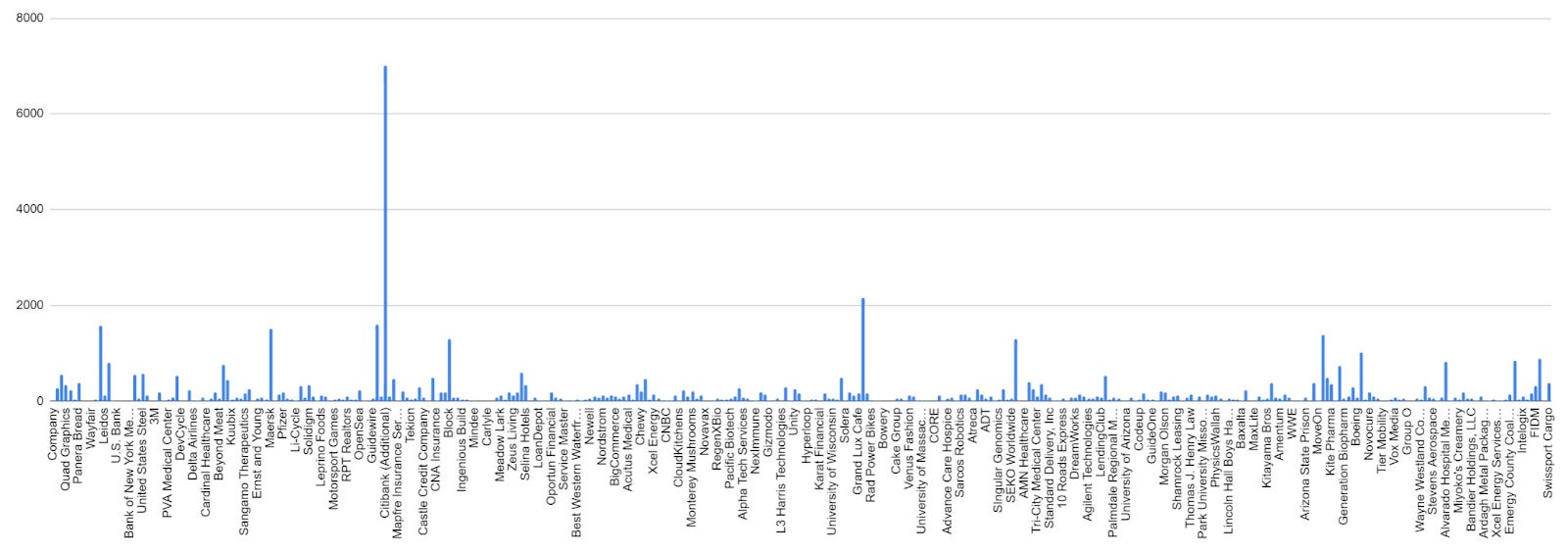

Continuing claims rose w/w to the highest level since 10 year 3 month inversion:

Continuing claims are definitely something to watch out for…

Full MacroEdge Weekly Report only available at MacroEdge.net.

Gold’s Dangerous Rally to New All Time Highs (@RealJohnGaltFla, MacroEdge Contributor)

The long time followers of this blog know that for this author to present the title above, something very bad might just be in the offing. Sadly, I fear this is truly the case as gold finally closed at a new all time high on Friday, December 1st, yet I feel a sense of foreboding rather than elation as the shiny metal of safety starts to behave as it should historically.

Charts are going to provide some major clues, but allow me to present a point of discussion to my readers that is not being discussed in the goldbug community.

In times of global strife and geopolitical instability gold has always been viewed by nations and individuals as the “safe haven” trade. The modern online glibsters will have one believe that digital or cryptocurrencies are the new safe haven, failing to realize that their physical application as a safety trade is only as good as the data havens they are stored on and the convertibility into the currency of the nation they reside in.

Since a government has the ultimate final say over conversion to practical usage, there is no safety in digital assets; including stocks, bonds, and any other creation of our modern financial system.

As gold is now at new all time closing highs, and not quite to the point where I would declare this “the real deal” yet (see: Another Suspect Rally in Gold or the Real Deal?) let us take a second to review the known risks possibly fueling this rally even higher.

1. Geopolitical Risk

The United States is financially exhausted as the enemies of our nation have figured out how to make our military-industrial complex suffer a death by 1000 cuts almost weekly. The US manufacturing base is incapable of manufacturing the necessary daily supplies for a sustained first world conflict as illustrated by the shortages the Ukrainian Armed forces are experiencing. Now that the Hamas-Israel War is absorbing any remaining supplies, NATO and the US are at all time reserve lows with potential conflicts simmering in Taiwan, Venezuela, North and South Korea, Myanmar, Ethiopia and Eritrea, Libya, and other hot spots currently at a low boil.

2. Financial Instability

I’ll just leave this here:

A reminder, from the Federal Reserve website on the Bank Term Funding Program:

The Federal Reserve Board, on March 12, 2023, announced the creation of a new Bank Term Funding Program (BTFP). The BTFP offers loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par.

Thus if a 30 year US Treasury or MBS if valued at 70 cents on the dollar in a regional bank’s holdings as marked to market, the Fed will loan them money at par to keep them from taking a loss on that asset. Unfortunately for the Fed, there is no indication that there are fewer banks using this facility, but more institutions needing this lifeline.

Add in the declining ability of consumers to obtain credit from these same banks, delinquencies and defaults rising, and the embedded inflation not counted by the government data geeks and a formula for disaster worse than 2008 is increasing with every passing month.

3. Political Incompetence

The West, also known as the EU, Japan, Canada, the UK, and the United States, has never looked more pathetic than this since the 1970’s. In the US our national political structure looks something like a perverse reality TV show with graft, economic illiteracy, and globalism is rewarded with real and imaginary votes while adults are told to sit down and shut up. Canada has decided become France’s twin sister and soon it will burn like Paris has been for the last two years. The UK is an economic and political joke. Most of the EU is financially and militarily bankrupt. And Japan is attempting hyperinflation while trying to sell its citizenry that all is well, please remain calm and pick a robot to date from the online catalog.

God help us all.

4. Four Charts That Support this Rally

I shall keep the commentary short as the charts speak for themselves. First and foremost, Dr. Copper seems to confirm that this long term rally in gold has legs and could easily go higher.

Never argue with the Doctor, he went to college after all.

Next up, the warning the US 10 Year Treasury seems to be sending a clear signal that the bond rally is short lived and will fade next year.

The break where the US 10 year in price no longer rallies with gold indicates that the shiny metal might just be benefiting from a true flight to safety as long duration assets, although liquid, are at risk of further price declines due to sporadic inflationary impulses.

Next up, the comparison to the S&P 500 which screams long term embedded inflation.

If this was truly a disinflationary, deflation episode for the long term, there should be a visible divergence developing in the price of gold versus the long term trend for US equities. Thus the markets believe the Fed ‘put’ is still intact and the gambling can continue unabated regardless of economic reality.

Lastly, the US Dollar index versus gold:

Gold and the US Dollar behaved normally from the 2007 GFC through the Sitzkrieg era of monetary policy. However after the pandemic, gold held its gains while the US Dollar imploded briefly. After the 2022 elections however, a noticeable uptick in a flight to safety trade in gold and the dollar began and despite recent price declines versus other major currencies, is still intact over the long term.

The question becomes this then:

What is the “something wicked this way comes?”

In this era of financial distortions created by financial chicanery, government interference and insider trading by central banks it is very difficult to point to one aspect which could cause the cumulative event most individuals are looking for.

Unfortunately, in this author’s opinion, it probably will be a long term combination of events from the 2024 Presidential election to the implosion of shadow banking in the West along with wars and panic breaking out on a global scale.

The next price levels to watch are around $2150 per ounce and a break above that level leaves the path wide open to $2500 per ounce and ultimately $3000 or higher. If this occurs, then the world we live in today will cease to exist and a strange new shift on the economic and political axis will have happened, leaving chaos in its wake.

The safety trade, dangerous as it is, appears to be alive and well.

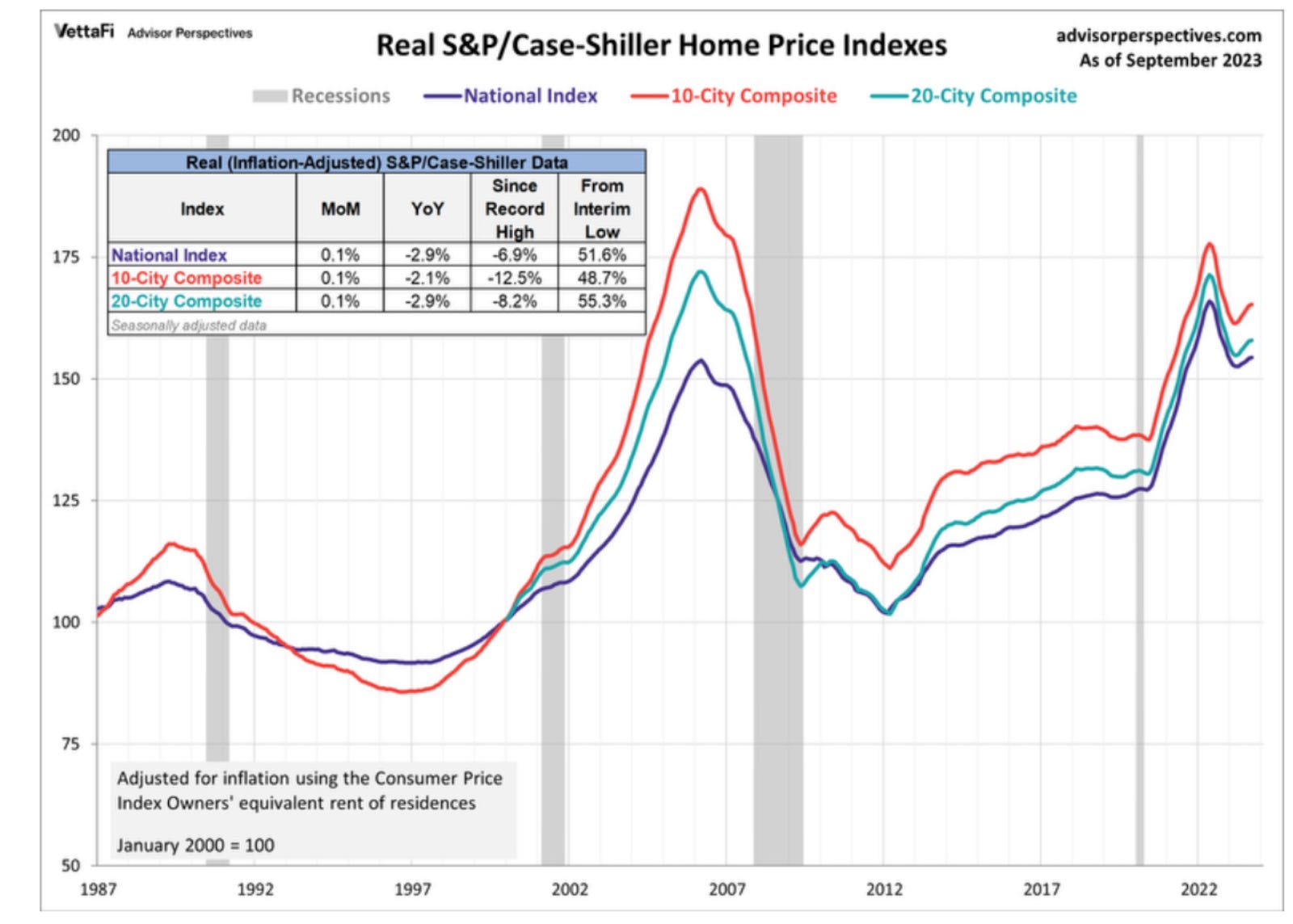

America’s Housing Market, “It Was All A Dream” (@GregCrennan, MacroEdge Contributor )

This month's data on Americas housing market paints a grim picture, shattering the dreams of current and prospective homeowners alike. As the legendary Notorious B.I.G. once rapped, "It was all a dream," and the haunting echo of that sentiment resonates through the current state of the housing market. The dream, it appears, could be turning into a nightmare, and the market's reality is about to deliver a rude awakening to those who dared

to dream of stable and lucrative deals in the housing market.

A Dream Unraveled by Interest Rates:

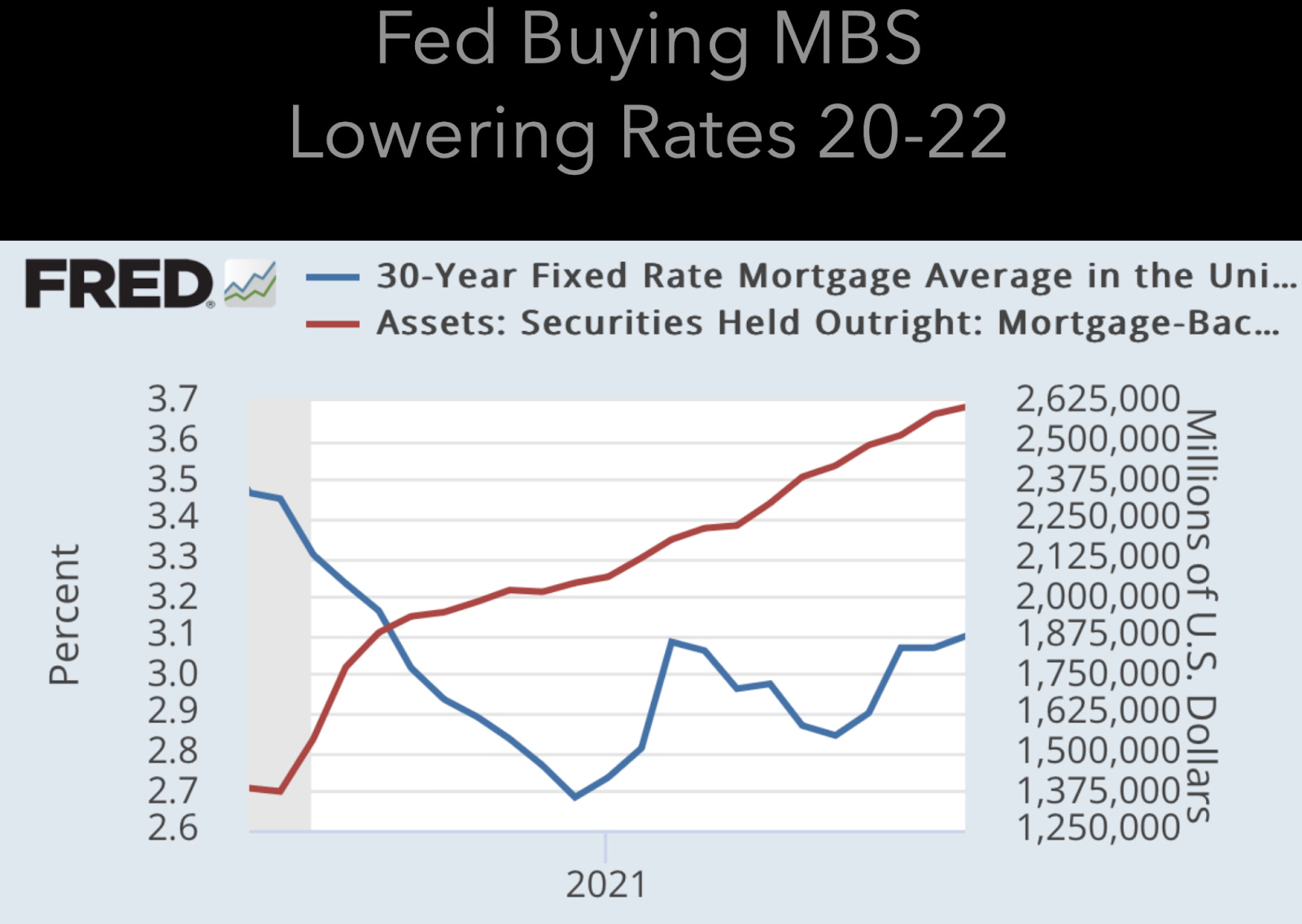

The Federal Reserve's digital purchase of Mortgage-Backed Securities (MBS) from 2020 to 2022, totaling $2.7 trillion, led to suppressed 30-year fixed interest rates (reaching as low as 2% for a brief period and averaged 3%). This made homeownership dreams seem within reach for many Americans. Due to the lower rates, monthly mortgage payments artificially became cheap, which contributed to the booming prices in housing that peaked between June 2022 and June 2023, depending on the region. However, the dream is now unraveling as interest rates hover around 7.5% (as of Nov 2023), reaching a two-decade high over 8% this year as the Fed has stopped buying MBS. These high interest rates make housing affordability at current prices the worst in US history

Reality's Crescendo: Declining Prices and Surging Supply:

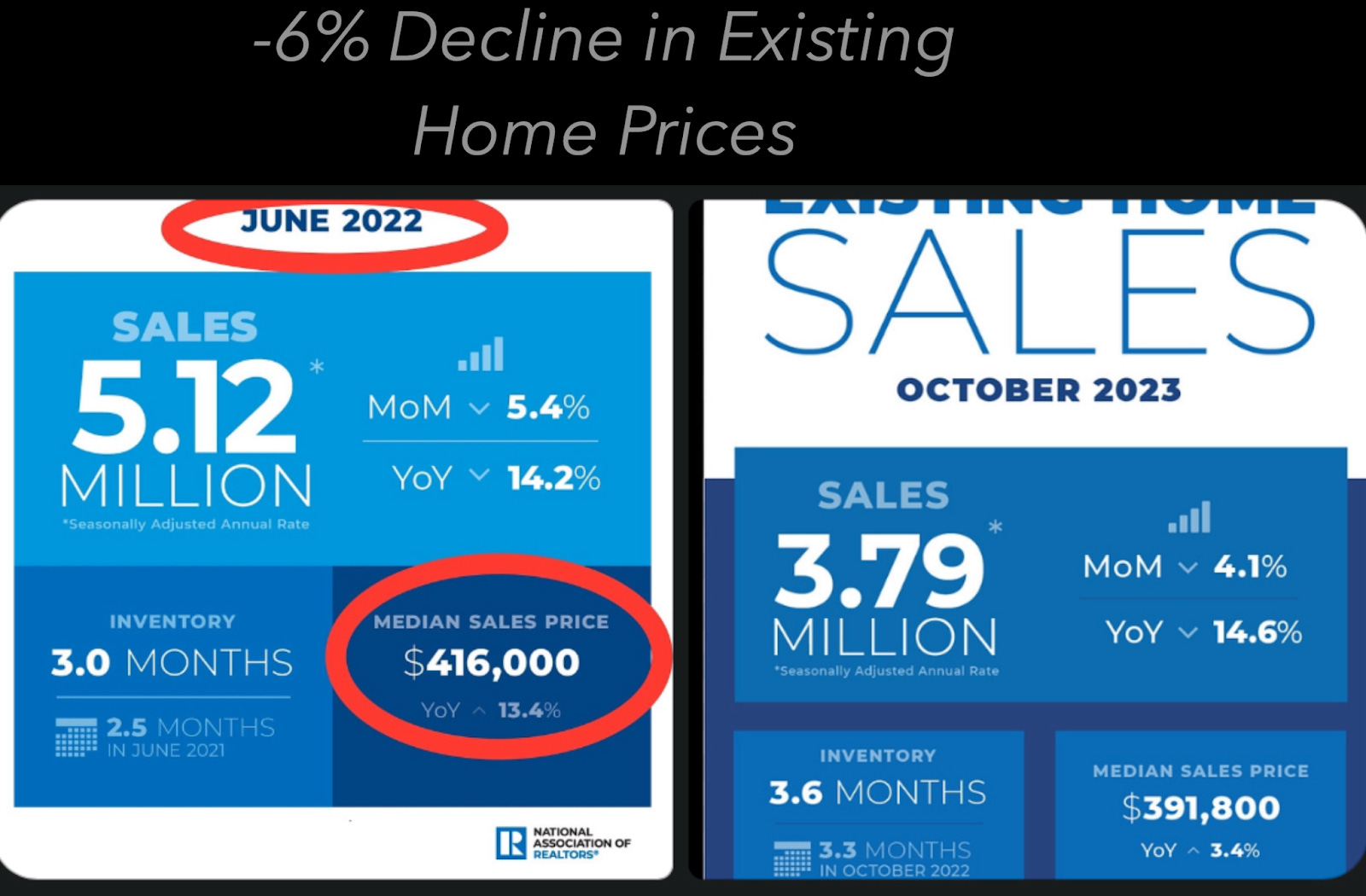

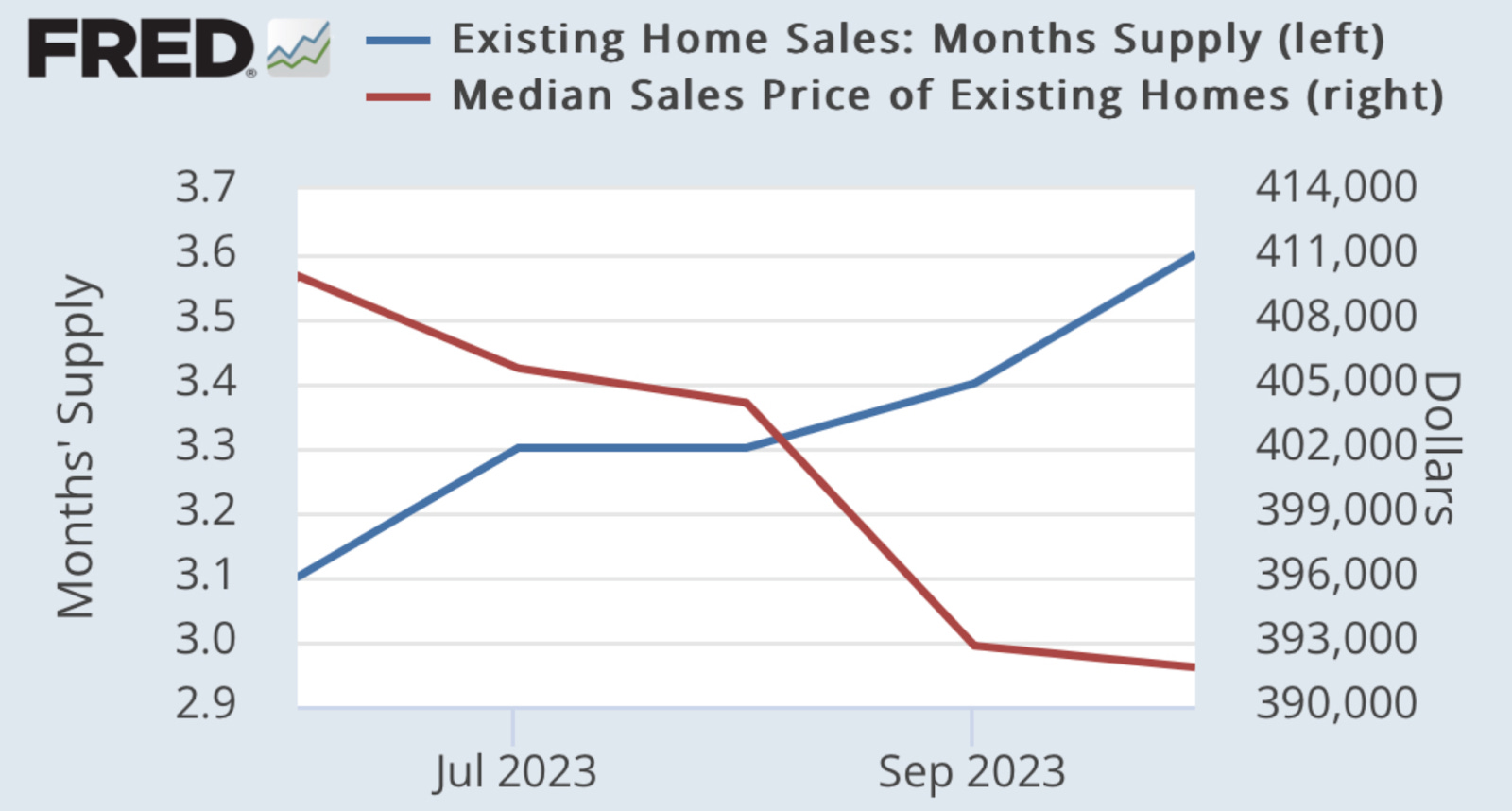

The dream of million-dollar homes is dissipating, with existing home sale prices experiencing a -6% decline from the peak, dropping from $416,000 to $391,000 (as of October 2023 data). New home sales prices have crashed even more dramatically, plummeting by -18% from their 2022 peak. Adding to the predicament, pending home sales have dropped to a record low (even worse than during the depths of the 2008 financial crisis), and the supply of housing is on the rise up almost 40% this year, creating a dissonance between falling demand and increasing inventory.

The Overture of Oversupply and Falling Demand:

Basic economic principles remind us that when demand decreases and existing home supply rises (40% year to date), prices must adjust lower. The current imbalance in the real estate market suggests a looming correction. What may appear as a housing shortage could indeed be an oversupply when there is little or even no demand (based on record low demand for mortgages for current supply). Current inventory is also lingering on the market for longer

Cancellation Surge and the Cash Crunch:

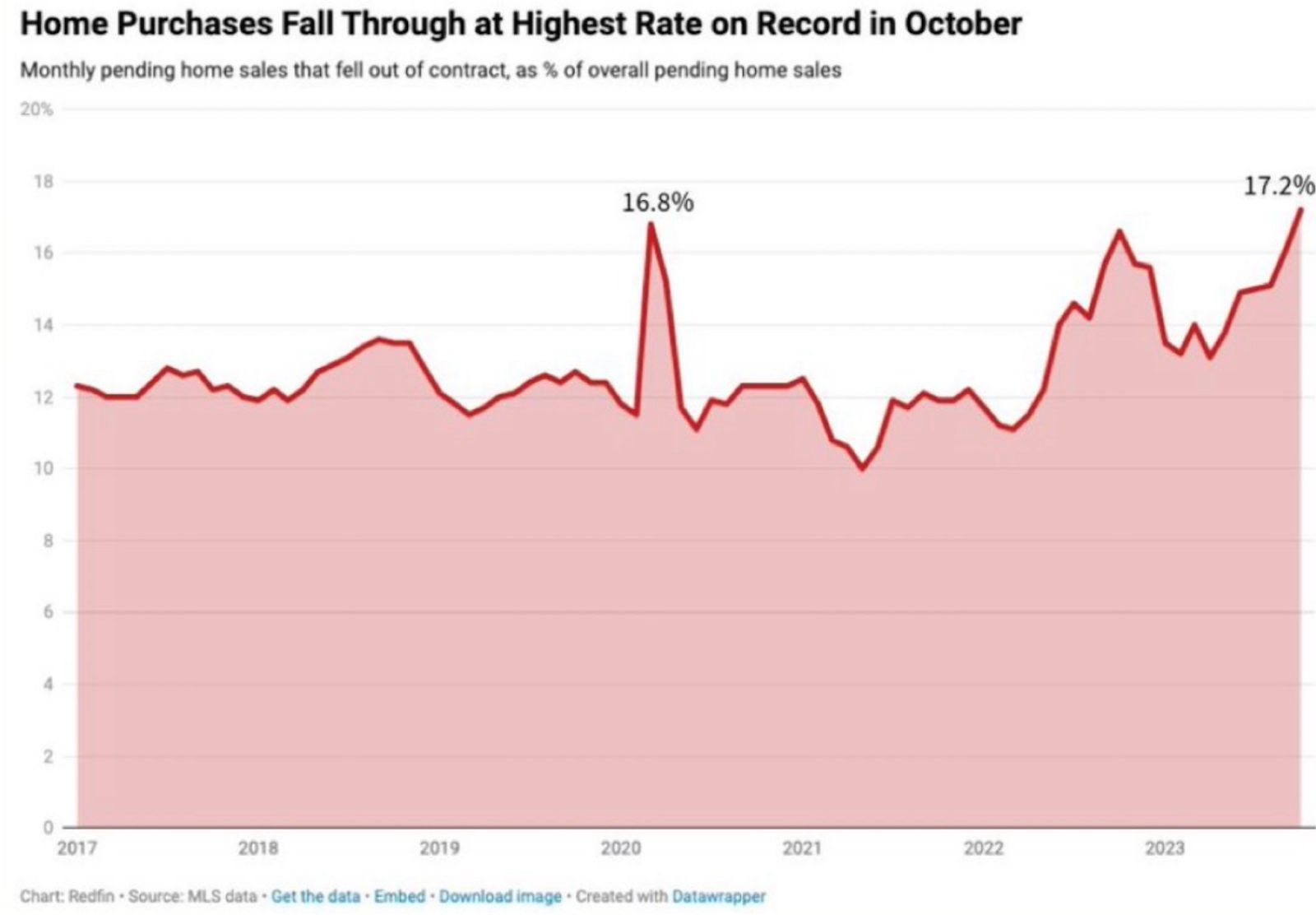

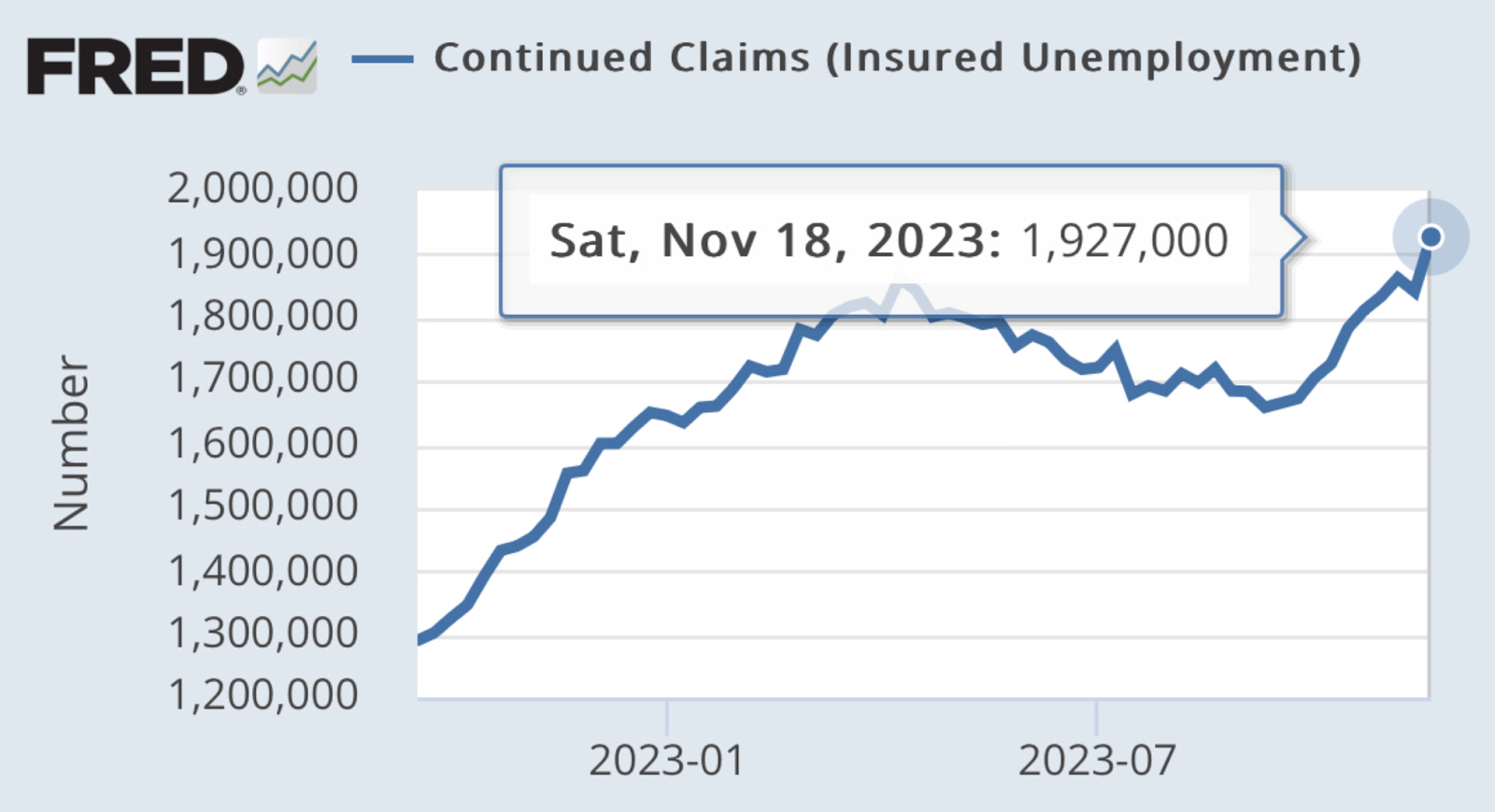

Redfin's latest report reveals a remarkable 17.2% surge in canceled real estate deals for October, marking an all-time high and signaling a mounting sense of apprehension among prospective homeowners. The question arises: why this sudden willingness to relinquish the American Dream? The answer lies in the ongoing inflationary pressures and the drastic rise in continued unemployment. Notably, the recent surge in unemployment figures has reached a staggering 1.9 million, surpassing levels not seen since November 2021 and exceeding any other period prior to the lockdowns of 2020. This surge has left homeowners financially strained. Furthermore, the situation is compounded by an increase in delinquencies in credit card and auto loan payments, with these data points acting as additional contributing factors to the growing unease in the real estate market.

Inflation's Eats Away at Homeownership Dreams:

As Americans check their Zillow app, hoping for a million-dollar valuation, they are facing inflation (a loss of -18% in purchasing power since January 2021), with higher property taxes, utilities, and maintenance costs. The dream of homeownership is now turning sour as recent data reveals that, adjusted for inflation, real estate values are actually losing

value, down by a significant -7%. These early data points also happened at the start of Great Recession of 2008, and today's trend is very worrisome for the future of the American Dream for all.

Homes go from Assets to Liabilities:

A home transforms into a significant concern if its value fails to keep up with inflation. Inflation's erosion of purchasing power not only diminishes the real worth of the property but also amplifies financial strain with escalating operating costs. The worry intensifies as fixed-rate mortgages

become comparatively more burdensome amid rising interest rates driven by inflation. Homeowners face the distressing prospect of missing out on potential investment gains like 5.5% guarantee returns in bonds doubling your money in 14 years, incurring a substantial opportunity cost. The anxiety deepens when considering that a declining real estate value may

force homeowners to sell at a loss, turning what was once an appreciating asset into a worrisome financial liability. Americans are awakening to this reality, and those who currently own seek to cash out, echoing Biggie's mantra: "Time to get paid

Living the Pre-Fame Struggle:

Yet, the irony persists—those needed to revitalize demand are living the pre-fame struggle, a prelude to financial solace that echoes Biggie's narrative words “just trying to make some money to feed my family, as all the families are in the struggle." In the midst of inflation and mounting debts, the American Dream remains elusive, and homeownership and financial freedom, for most, is an illusion.

Perhaps it's time to reconsider the notion that homeownership guarantees financial freedom. The legendary rapper’s cautionary words still hold today, "If you don’t know, now you know, my man."